GAAFET Market Insights

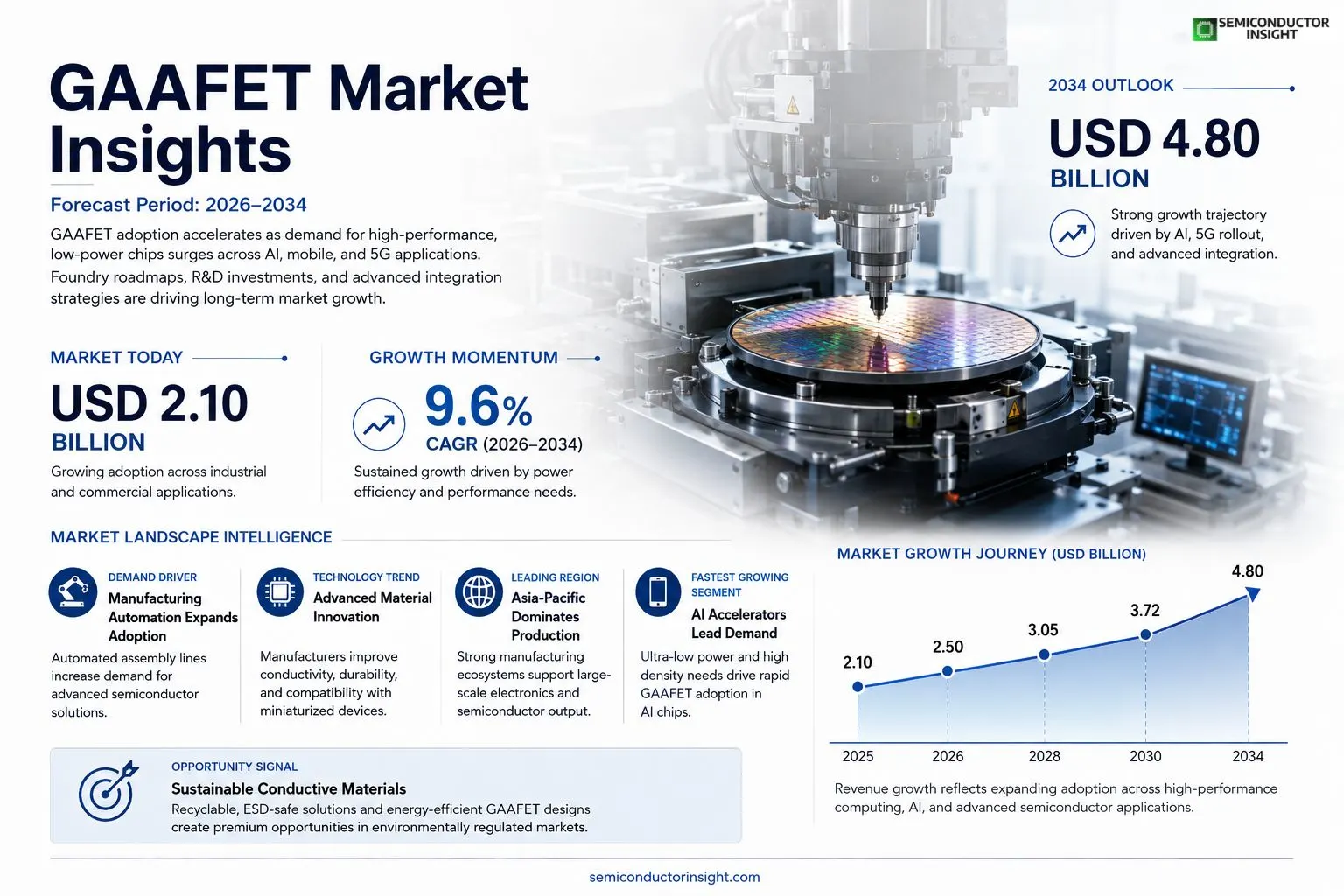

GAAFET market size was valued at USD 2.10 billion in 2025. The market is projected to grow from USD 2.10 billion in 2025 to USD 4.80 billion by 2034, exhibiting a CAGR of 9.6% during the forecast period.

GAA‑FET (Gate‑All‑Around Field‑Effect Transistor) represents an advanced transistor architecture where the semiconductor channel is completely surrounded by the gate electrode, delivering superior electrostatic control compared with planar or FinFET designs.The market is accelerating because semiconductor manufacturers are intensifying R&D investments to meet escalating demand for high‑performance computing, AI workloads, and mobile applications that require lower power consumption and higher density.

Furthermore, the rollout of 5G infrastructure and emerging heterogeneous integration strategies are driving adoption of GAA technology.

Key players such as Samsung Electronics (with its MBCFET production), Intel (announcing “RibbonFET” development), and TSMC (partnering with imec on nanosheet integration) are expanding their roadmaps, while collaborations between foundries and equipment suppliers are shortening time‑to‑market for next‑generation chips.

MARKET DRIVERS

Technological Advancements Driving Adoption

GAAFET Market is being propelled by the transition from planar FinFETs to gate‑all‑around (GAA) architectures, which deliver up to 30% lower power consumption and a 15% boost in drive current at the 3 nm node. These performance gains enable chipmakers to meet the escalating power‑efficiency requirements of mobile and data‑center processors.

Demand from High‑Performance Computing

High‑performance computing (HPC) workloads, especially those tied to AI model training, are creating a surge in demand for devices that can sustain high transistor density. Industry estimates suggest that 2024 shipment volumes of GAA‑based chips will exceed 5 million units, reflecting a rapid uptake in super‑computing clusters.

➤ Analysts project the GAAFET segment to achieve a 12% CAGR, reaching roughly $2.3 billion in revenue by 2030.

These drivers collectively reinforce the strategic importance of GAA technology, positioning it as a cornerstone for next‑generation silicon scaling.

MARKET CHALLENGES

Manufacturing Complexity and Yield Issues

Implementing GAA transistors requires new lithography steps and precise nanosheet patterning, which increase fab complexity. Early‑stage yield rates have been reported at 78% for initial 3 nm GAA lines, compelling manufacturers to invest heavily in process optimization.

Other Challenges

Cost Sensitivity

The capital outlay for GAA‑compatible equipment can exceed $1 billion per fab, creating cost‑sensitivity among mid‑size foundries that lack the financial bandwidth of the largest players.

MARKET RESTRAINTS

Capital‑Intensive Equipment Requirements

Transitioning to GAAFET production demands advanced extreme‑ultraviolet (EUV) scanners and novel atomic‑layer‑etch tools. The upfront investment, combined with the need for specialized training, restrains smaller fabs from immediate adoption.

MARKET OPPORTUNITIES

Emerging Applications in AI Accelerators

AI accelerator chips, which require unprecedented transistor density, present a lucrative growth avenue. Forecasts indicate that AI‑focused GAAFET designs could account for 40% of total GAA shipments by 2028, unlocking new revenue streams for silicon vendors.

GAAFET Market Trends

Accelerating Adoption in High‑Performance Computing

GAAFET Market is witnessing a decisive move away from planar and FinFET structures as chip designers prioritize electrostatic control and channel scaling. By wrapping the gate entirely around the channel, GAA FETs deliver lower leakage and higher drive current, attributes that directly support the power‑efficiency demands of AI accelerators and next‑generation data‑center processors. Industry surveys show that semiconductor manufacturers are reallocating design resources toward GAA architectures, reflecting a consensus that the technology is essential for sustaining performance growth beyond the limits of existing nodes. This shift is evident across the supply chain, from lithography equipment upgrades to on‑die interconnect innovations, reinforcing the strategic importance of GAA in the broader market landscape. The trend is further reinforced by the need for higher transistor density in edge‑computing devices.

Other Trends

R&D Investment and Roadmap Expansion

Leading foundries such as Samsung Electronics, Intel, and TSMC have publicly announced expanded roadmaps that embed GAA transistor generations into their 7‑nm and sub‑5‑nm process lines. Samsung’s MBCFET implementation, Intel’s “RibbonFET” program, and the TSMC‑imec nanosheet partnership illustrate a coordinated effort to accelerate time‑to‑market. These initiatives are accompanied by heightened R&D spending aimed at refining nanosheet uniformity, reducing line‑edge roughness, and improving manufacturability at high volume. Collaborative projects with equipment vendors are also streamlining the adoption curve, allowing design teams to evaluate GAA devices earlier in the product development cycle. The cumulative effect is a more predictable technology transition for customers seeking to leverage the density and power advantages of GAA in upcoming silicon releases.

Integration with 5G and Heterogeneous Architectures

The rollout of 5G infrastructure is driving demand for radio‑frequency front‑ends and base‑station processors that operate at higher frequencies with reduced power budgets. GAA transistors, by virtue of their superior gate control, enable these components to meet the stringent linearity and efficiency targets required for massive‑MIMO and beam‑forming applications. Simultaneously, the rise of heterogeneous integration—combining logic, memory, and specialized accelerators on a single package—is creating new design windows where GAA devices can be co‑located with emerging technologies such as silicon photonics and advanced packaging. As the ecosystem matures, GAAFET Market is poised to benefit from a convergence of connectivity, compute, and packaging trends that together amplify the relevance of gate‑all‑around solutions across multiple product categories. These dynamics underscore GAAFET Market’s role as a foundational technology for the next decade of silicon innovation.

COMPETITIVE LANDSCAPEKey Industry Players

GAAFET Market Competitive Dynamics

GAAFET Market is currently dominated by semiconductor powerhouses that have integrated gate‑all‑around technology into their advanced node roadmaps. Samsung Electronics leads with its MBCFET (Multi‑Bridge‑Channel FET) production, targeting sub‑3 nm platforms and leveraging a vertically stacked nanosheet architecture that promises higher drive current and lower power per transistor. Intel follows closely, publicly announcing its “RibbonFET” development as part of the “Intel 4” and “Intel 3” process families, emphasizing a seamless transition from FinFET to GAAFET to sustain performance scaling for AI and high‑performance computing workloads. TSMC, the world’s largest pure‑play foundry, has partnered with imec to mature nanosheet integration, positioning its 2 nm and upcoming 1.4 nm technology nodes as the first commercial GAAFET offerings for a broad ecosystem of fabless customers. Collectively, these three players shape the market’s supply chain, dictate pricing benchmarks, and set the technical cadence that smaller foundries must follow.Beyond the tier‑one leaders, a cohort of specialized and niche players is accelerating the adoption of GAAFET through equipment, materials, and design‑enable services. ASML supplies the extreme‑ultraviolet lithography tools required for nanosheet patterning, while Applied Materials delivers the deposition and etch solutions that define gate architecture. imec continues to act as a research hub, collaborating with Foundries and Sony on prototype GAAFET devices for edge‑AI and automotive markets. Qualcomm and Nvidia drive demand by integrating GAAFET‑based silicon into next‑generation GPUs and mobile SoCs, whereas companies such as SK Hynix, Micron, and Renesas explore memory and embedded logic implementations that benefit from the density gains of gate‑all‑around structures.

List of Key GAAFET Companies Profiled

- Samsung Electronics

- Intel Corporation

- TSMC (Taiwan Semiconductor Manufacturing Company)

- imec

- ASML Holding

- Applied Materials

- Foundries

- Sony Semiconductor

- Qualcomm Incorporated

- Nvidia Corporation

- SK Hynix

- Micron Technology

- Renesas Electronics

- AMD (Advanced Micro Devices)

- IBM

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Nanosheet GAA is emerging as the preferred architecture because it balances manufacturability with performance.

|

| By Application |

|

AI Accelerators drive the most compelling use‑case for GAAFET technology.

|

| By End User |

|

Foundries are the leading segment because they own the process technology roadmaps.

|

| By Technology Maturity |

|

Mass Production is the leading segment as GAA transitions from prototype to high‑volume manufacturing.

|

| By Market Driver |

|

Power Efficiency stands out as the primary catalyst for GAAFET adoption.

|

Regional Analysis: North America

United States

The demand for advanced packaging technologies that leverage GAAFET to achieve higher integration levels and improved performance is a key area of growth. This includes 3D stacking and fan-out wafer-level packaging, crucial for meeting the demands of advanced computing platforms.

The increasing adoption of GAAFET in high-performance computing (HPC) systems, particularly for scientific research and data analytics, is driving significant market opportunities. The superior performance and energy efficiency of GAAFET contribute to enhanced computational capabilities.

GAAFET is gaining traction in the automotive electronics sector due to its potential to enhance the performance and reliability of in-vehicle semiconductors. This includes applications in advanced driver-assistance systems (ADAS) and electric vehicle (EV) powertrains.

GAAFET is being explored as a key enabler for next-generation memory technologies, such as advanced SRAM and non-volatile memory, contributing to higher density and improved performance in memory systems.

Europe

Europe is witnessing a growing interest in GAAFET technology, primarily driven by the region’s strong focus on industrial automation, automotive innovation, and energy-efficient computing. While not yet at the scale of the US, the European semiconductor ecosystem is actively investing in GAAFET research and development, with several key players exploring its potential for various applications. Government support through initiatives like the European Chips Act is expected to accelerate the adoption of advanced technologies like GAAFET. The emphasis on sustainable technology solutions aligns well with the potential energy efficiency benefits offered by GAAFET. Key areas of focus include automotive semiconductors, industrial control systems, and data center applications seeking enhanced power efficiency. The collaborative nature of the European semiconductor industry is fostering partnerships and knowledge sharing to overcome technological challenges and drive GAAFET adoption across the continent.

Asia-Pacific

Asia-Pacific, particularly countries like China, Japan, and South Korea, represents a rapidly expanding market for GAAFET. The region’s significant investments in semiconductor manufacturing and consumer electronics are fueling demand for advanced transistor technologies. China’s ambitious plans to become a semiconductor leader are driving substantial investment in GAAFET research and development and manufacturing capabilities. South Korea, with its established semiconductor industry, is also actively pursuing GAAFET technology to maintain its competitive edge. Japan is focusing on niche applications within automotive and industrial sectors. The strong growth in 5G infrastructure and the burgeoning market for IoT devices are further contributing to the demand for GAAFET within the Asia-Pacific region. The competitive landscape is intense, with numerous domestic and international players vying for market share.

South America

GAAFET Market in South America is currently in its nascent stages, with limited adoption but potential for future growth. The region’s developing economies and increasing demand for electronics present opportunities for GAAFET applications in areas such as telecommunications infrastructure and industrial automation. While investment in semiconductor manufacturing is relatively low compared to other regions, the growing focus on technological advancement and digital transformation is expected to drive gradual adoption of advanced transistor technologies like GAAFET. The adoption will likely be spurred by the need for more energy-efficient and high-performance computing solutions within the region.

Middle East & Africa

The Middle East & Africa region represents a smaller but growing market for GAAFET. Driven by increasing investments in digitalization, smart city initiatives, and infrastructure development, the demand for advanced semiconductor solutions is expected to rise. The region’s focus on diversifying its economies and promoting technological innovation is creating opportunities for GAAFET applications in areas such as telecommunications, healthcare, and industrial automation. While the current market size is limited, the long-term growth potential of GAAFET in this region is promising, particularly as digital transformation gains momentum. Government initiatives aimed at fostering technological advancement are expected to play a key role in driving GAAFET adoption.

Report Scope

This market research report provides a comprehensive analysis of the GAAFET Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of GAAFET Market?

-> GAAFET Market was valued at USD 2.10 billion in 2025 and is expected to reach USD 4.80 billion by 2034.

Which key companies operate in GAAFET Market?

-> Key players include Samsung Electronics, Intel, and TSMC, with notable collaborations such as TSMC’s partnership with imec on nanosheet integration.

What are the key growth drivers?

-> Key growth drivers include intensified R&D investments, demand for high‑performance computing, AI workloads, mobile applications requiring lower power consumption, the rollout of 5G infrastructure, and emerging heterogeneous integration strategies.

Which region dominates the market?

-> The reference does not specify a dominant region.

What are the emerging trends?

-> Emerging trends include heterogeneous integration strategies, advanced nanosheet architectures, and the broader adoption of 5G infrastructure driving GAA technology deployment.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...