IGBT and MOSFET Market MARKET INSIGHTS

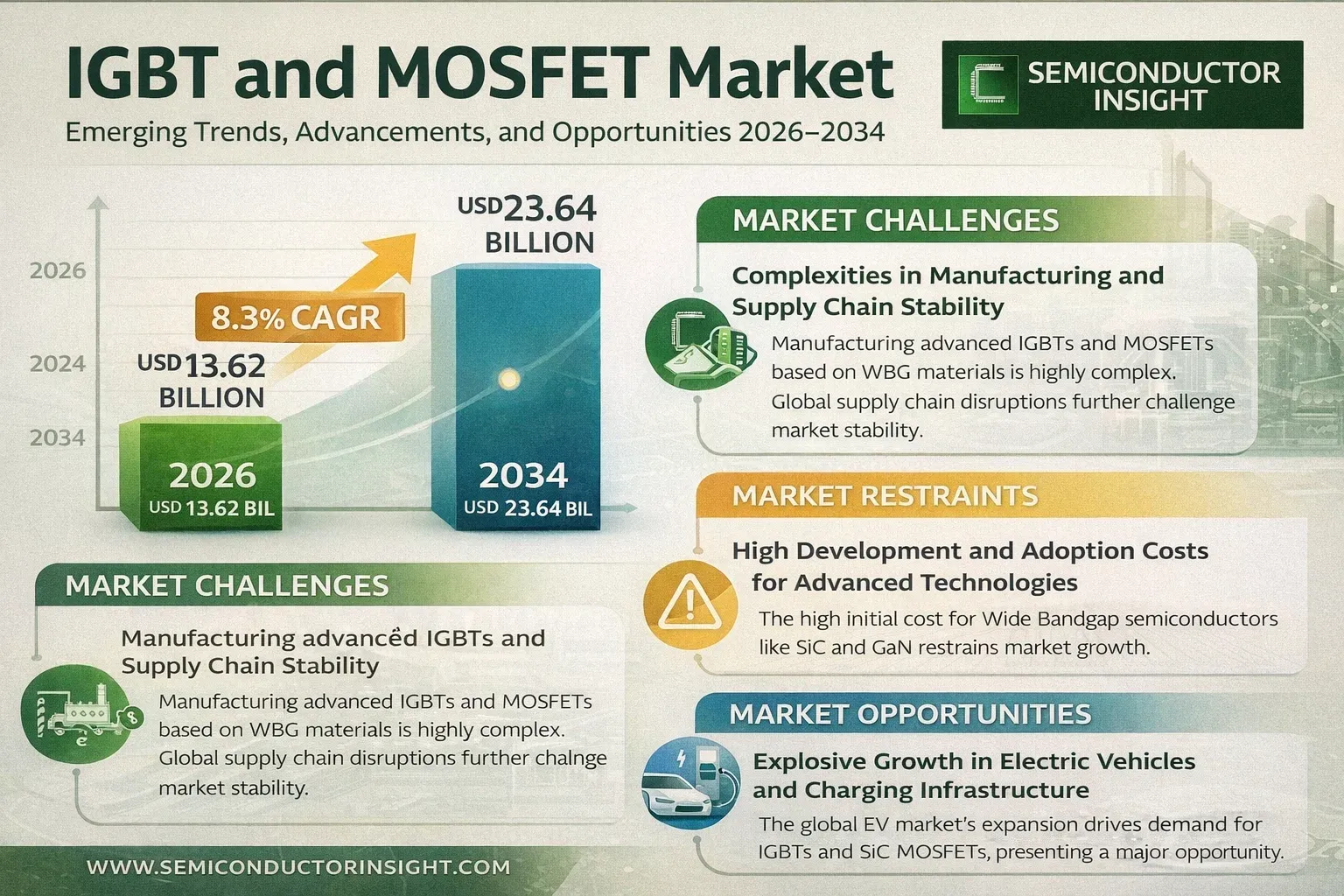

Global IGBT and MOSFET Market was valued at USD 13.62 billion in 2024 to USD 23.64 billion by 2032, exhibiting a CAGR of 8.3% during the forecast period.

IGBT (Insulated Gate Bipolar Transistor) and MOSFET (Metal-Oxide-Semiconductor Field-Effect Transistor) are fundamental semiconductor devices used for power switching and amplification applications. IGBTs combine the high input impedance of MOSFETs with the high current-carrying capability of bipolar transistors, making them ideal for high-voltage, high-current applications like motor drives and power inverters. MOSFETs, particularly power MOSFETs, are optimized for high-frequency switching with low on-resistance, making them suitable for switch-mode power supplies and motor control. Both device types are critical for energy efficiency, power conversion, and the electrification of various industries.

The market is experiencing robust growth due to several factors, including the global push for energy efficiency and the electrification of transportation. The transition to electric vehicles (EVs) and hybrid electric vehicles (HEVs) is a major driver, as these vehicles require extensive power electronics for motor drives and battery management. Furthermore, the integration of renewable energy sources like wind and solar necessitates advanced power conversion systems that rely on IGBTs and MOSFETs. The proliferation of industrial automation and the Internet of Things (IoT) also increases demand for efficient power management solutions. Government regulations aimed at reducing carbon emissions are further accelerating the adoption of these technologies.

However, the market faces challenges such as supply chain constraints for raw materials like silicon wafers and the complexity of manufacturing advanced semiconductor devices. Geopolitical tensions affecting the semiconductor supply chain also pose a risk to market growth. Nonetheless, ongoing technological advancements, including the development of wide-bandgap semiconductors like silicon carbide (SiC) and gallium nitride (GaN), which offer superior performance but often integrate with traditional silicon-based IGBTs and MOSFETs, are expected to create new opportunities.

MARKET DRIVERS

Accelerated Electrification Across Industries

Global push for electrification is a primary driver for the IGBT and MOSFET Market. The automotive sector’s rapid transition to electric vehicles (EVs) and hybrid electric vehicles (HEVs) requires high-power IGBT modules for traction inverters and efficient MOSFETs for auxiliary systems like battery management and onboard chargers. This demand is complemented by the growth in renewable energy infrastructure, where these transistors are essential for solar inverters and wind turbine converters. Industrial motor drives, which increasingly utilize variable frequency drives for energy efficiency, also represent a significant and growing segment.

Technological Advancements in Power Density and Efficiency

Continuous innovation in semiconductor materials and packaging is a key market driver. The shift from traditional silicon to Wide Bandgap (WBG) semiconductors like Silicon Carbide (SiC) and Gallium Nitride (GaN) is creating next-generation MOSFETs and IGBTs that offer superior performance. These devices operate at higher frequencies, temperatures, and voltages with significantly lower switching losses. This enables the design of smaller, lighter, and more efficient power electronic systems, which is critical for applications with space constraints, such as EVs and consumer electronics.

The expansion of 5G infrastructure and data centers further propels demand. The massive power requirements for data processing and telecommunications equipment rely heavily on robust power management, where MOSFETs are indispensable for switched-mode power supplies (SMPS), ensuring stable and efficient operation.

MARKET CHALLENGES

Complexities in Manufacturing and Supply Chain Stability

Manufacturing advanced IGBTs and MOSFETs, particularly those based on WBG materials, involves highly complex and capital-intensive fabrication processes. Establishing and maintaining high-yield production lines for these sophisticated components is a significant challenge for manufacturers. Furthermore, the global semiconductor supply chain has faced severe disruptions, from raw material shortages to geopolitical tensions, leading to extended lead times and price volatility that hinder market stability and growth.

Other Challenges

Intense Price Pressure and Competition

The market is characterized by fierce competition among established global players and emerging manufacturers, primarily from Asia. This competitive landscape exerts constant pressure on pricing and profit margins, forcing companies to continuously innovate while managing costs. This is particularly challenging when developing expensive new technologies like SiC and GaN.

Thermal Management and Reliability Demands

As power densities increase, effectively dissipating heat becomes a critical design challenge. Ensuring long-term reliability under high-temperature and high-stress operating conditions in applications like automotive and industrial drives requires advanced packaging solutions and thermal interface materials, adding complexity and cost to the final product.

MARKET RESTRAINTS

High Development and Adoption Costs for Advanced Technologies

The high initial cost of Wide Bandgap semiconductors like SiC and GaN acts as a significant restraint on market growth. While these materials offer superior performance, the substrates are more expensive to produce than silicon, and the manufacturing processes are not yet fully matured. This results in a higher price point for the end components, which can slow their adoption in cost-sensitive applications and markets, despite the compelling long-term efficiency benefits.

Design Complexity and Specialized Expertise Shortage

Effectively integrating advanced IGBTs and MOSFETs into systems requires specialized engineering expertise. The high-speed switching characteristics of WBG devices, for instance, demand careful attention to circuit layout and gate driving to avoid issues like electromagnetic interference (EMI). A shortage of engineers with deep expertise in high-frequency power electronics can slow down design cycles and act as a bottleneck for the adoption of the latest technologies.

MARKET OPPORTUNITIES

Explosive Growth in Electric Vehicles and Charging Infrastructure

The unprecedented global expansion of the electric vehicle market presents the most significant opportunity. Every EV requires multiple IGBTs or SiC MOSFETs in its main powertrain, alongside dozens of MOSFETs in various subsystems. This is compounded by the parallel need to build out extensive fast-charging infrastructure worldwide, which relies on high-power conversion systems utilizing these same power semiconductors, creating a sustained, long-term demand cycle.

Renewable Energy Integration and Smart Grid Development

Global commitment to renewable energy sources like solar and wind power directly fuels demand for power conversion systems. IGBTs and MOSFETs are fundamental components in inverters that convert DC power from solar panels and wind turbines into grid-compatible AC power. The modernization of electrical grids into smart grids, which require sophisticated power control and management for stability and efficiency, further opens up substantial new markets for these devices.

Adoption in Consumer Electronics and IoT Devices

The relentless miniaturization and increasing functionality of consumer electronics and the proliferation of Internet of Things (IoT) devices create continuous opportunities. There is a growing need for highly efficient, compact power management solutions to maximize battery life. This drives innovation and demand for advanced MOSFETs that can handle power conversion in smartphones, laptops, wearables, and a vast array of connected devices with minimal energy loss.

IGBT and MOSFET Market TrendsRobust Growth Driven by Electrification and Energy Efficiency

Global IGBT and MOSFET Market is on a significant growth trajectory, with its valuation projected to surge from USD 13.67 billion in 2024 to USD 23.64 billion by 2032, representing a compound annual growth rate (CAGR) of 8.3%. This expansion is fundamentally driven by the global push for electrification and improved energy efficiency across numerous industries. The transition to electric vehicles, the expansion of renewable energy infrastructure, and the proliferation of smart, energy-efficient appliances are creating sustained demand for these high-performance power semiconductors. Asia-Pacific dominates the market, accounting for over 57% of global share, largely due to its strong manufacturing base for consumer electronics and its rapid adoption of new energy technologies, particularly in China.

Other Trends

MOSFETs Lead in Market Share

In terms of product segmentation, MOSFETs are the dominant force, holding over 60% of the market share. Their widespread adoption is attributed to advantages in high-frequency switching applications, lower driving power requirements, and simpler drive circuits compared to IGBTs. MOSFETs are extensively used in applications like switch-mode power supplies, motor drives, and amplification circuits in consumer devices. Meanwhile, IGBTs remain critical for high-power applications requiring high voltage and current handling capabilities, such as industrial motor drives, inverters for renewable energy systems, and traction drives in electric vehicles.

Consumer Electronics as the Primary Application

The application landscape is diverse, but consumer electronics stands as the largest segment, commanding over 30% of the market. The relentless demand for smartphones, laptops, televisions, and gaming consoles, which require efficient power management and compact form factors, fuels this segment. Following consumer electronics, the industrial, new energy, and communications sectors are significant drivers. The growth in 5G infrastructure deployment and data centers, in particular, is creating substantial demand for robust power management solutions provided by both IGBTs and MOSFETs.

Consolidated Competitive Landscape with Focus on Innovation

The market is characterized by a consolidated competitive landscape, with the top five players including Infineon Technologies, ON Semiconductor, and STMicroelectronics collectively accounting for approximately 55% of the market. These leading companies are heavily investing in research and development to enhance device performance, reduce power losses, and improve thermal management. Key strategic trends include the development of wide-bandgap semiconductor materials like silicon carbide (SiC) and gallium nitride (GaN), which are being integrated with traditional silicon-based IGBT and MOSFET technologies to create next-generation power devices that offer higher efficiency, smaller size, and greater power density for the evolving demands of the automotive and industrial sectors.

COMPETITIVE LANDSCAPE

Key Industry Players

A market characterized by technological dominance and strategic specialization

Global IGBT and MOSFET Market is a consolidated space dominated by a handful of multinational semiconductor giants, with the top five players collectively holding a significant portion of the market share. Infineon Technologies leads the industry, leveraging its comprehensive portfolio of power semiconductors and strong presence across automotive, industrial, and renewable energy sectors. ON Semiconductor and STMicroelectronics are other key pillars of the market, consistently competing for leadership through continuous innovation in silicon and wide-bandgap technologies. The market structure is defined by intense competition in R&D to improve power efficiency, thermal performance, and miniaturization, particularly driven by the demands of electric vehicles, industrial automation, and green energy applications. This dominance by established players creates high barriers to entry, solidifying their positions.

Beyond the top-tier leaders, numerous other companies have carved out significant niches by specializing in particular product types, applications, or regional markets. Fuji Electric and Mitsubishi Electric are prominent players with strongholds in high-power IGBT modules for industrial drives and traction systems. Companies like Vishay, Littelfuse, and ROHM Semiconductor are major forces in the MOSFET segment, focusing on a broad range of discrete components for consumer electronics and power supplies. The competitive landscape is further diversified by the growing influence of Chinese manufacturers such as CR Micro, Starpower, and CRRC, which are expanding their market share, particularly within the Asia-Pacific region, by catering to the booming domestic demand for consumer electronics, home appliances, and new energy infrastructure.

List of Key IGBT and MOSFET Companies Profiled

- Infineon Technologies

- ON Semiconductor

- Toshiba

- STMicroelectronics

- Renesas Electronics

- Fuji Electric

- Vishay

- Mitsubishi Electric

- Nexperia

- AOS (Alpha and Omega Semiconductor)

- Semikron

- Littelfuse

- ROHM Semiconductor

- Hitachi

- CR Micro

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

MOSFET is the dominant product type due to its widespread adoption in high-frequency switching applications and consumer electronics, offering advantages in efficiency and cost-effectiveness for lower power requirements. The IGBT segment, while holding a smaller share, is critical for high-voltage and high-current applications such as industrial motor drives and power conversion systems, where it provides superior performance in handling substantial power levels with robustness and reliability that MOSFETs cannot match in those specific conditions. |

| By Application |

|

Consumer Electronics represents the most significant application area, driven by the immense volume of smartphones, laptops, and other portable devices that require efficient power management and switching components. The industrial and new energy sectors are also key growth drivers, with increasing demand for motor control, renewable energy inverters, and electric vehicle powertrains creating substantial opportunities. The communications industry relies on these components for infrastructure resilience, while home appliances continue to integrate more sophisticated power electronics for energy savings and improved performance. |

| By End User |

|

Original Equipment Manufacturers (OEMs) are the predominant end users, as they incorporate IGBTs and MOSFETs directly into finished products ranging from consumer gadgets to industrial machinery. System integrators represent an important segment, designing and assembling complex power conversion systems for specialized applications where component performance and reliability are paramount. The distributors and aftermarket segment supports the broader ecosystem by providing components for repairs, upgrades, and smaller-scale manufacturing, ensuring a steady supply chain for diverse market needs. |

| By Voltage Rating |

|

Low Voltage components are in the highest demand, primarily driven by the massive consumer electronics and automotive sectors where efficiency and miniaturization are critical design goals. The medium voltage segment serves a broad range of industrial automation and home appliance applications, balancing performance with cost considerations. High voltage IGBTs are essential for specialized, high-power applications in industries like renewable energy generation and heavy-duty industrial drives, where they provide the necessary robustness and control for managing significant electrical loads effectively. |

| By Sales Channel |

|

Direct Sales is the leading channel for large-volume OEMs and major industrial customers who require close technical collaboration, customized solutions, and guaranteed supply chain security. Distributors play a vital role in reaching a wider base of small and medium-sized enterprises and providing logistical support and inventory management. The burgeoning online retail channel is increasingly important for hobbyists, research institutions, and small-scale procurers seeking accessibility and rapid fulfillment for prototyping and low-volume projects, reflecting a diversification in how these critical components are accessed globally. |

Regional Analysis: IGBT and MOSFET Market

Asia-Pacific

The region’s push for electric mobility is a primary driver. Major automotive manufacturers and new EV startups are heavily invested, creating immense demand for IGBT modules in powertrains and MOSFETs in battery management and on-board chargers, supported by government incentives.

Rapid industrialization and the adoption of Industry 4.0 principles across manufacturing sectors fuel the need for motor drives, robotics, and UPS systems. IGBTs and MOSFETs are critical components, with local production ensuring cost-effective supply for this growing industrial base.

As the global center for consumer electronics production, the region’s massive output of smartphones, laptops, and appliances requires vast quantities of power MOSFETs for efficient power management, voltage regulation, and switching applications within these devices.

Significant government and private investments in solar and wind power generation necessitate advanced power conversion systems. IGBT-based inverters are essential for grid integration, creating a strong, long-term demand pipeline within the region’s energy sector.

North America

The North American market is characterized by strong demand from the automotive and industrial sectors, with a particular focus on technological innovation and high-performance applications. The region’s well-established electric vehicle industry, led by key manufacturers, requires sophisticated IGBT and MOSFET solutions for next-generation powertrains and charging infrastructure. Furthermore, the data center and telecommunications sectors demand highly efficient power management components for server farms and network equipment. The presence of major technology companies and a focus on renewable energy projects, especially in solar and wind, also contribute to steady demand. While manufacturing is less concentrated than in Asia, the region’s emphasis on R&D and high-value applications ensures its significant market position.

Europe

Europe holds a strong position in the IGBT and MOSFET Market, driven by its leading automotive industry’s aggressive transition to electrification. Strict environmental regulations and ambitious carbon neutrality goals are accelerating the adoption of electric vehicles, which in turn boosts demand for power semiconductors. The region also has a robust industrial automation sector and a growing focus on renewable energy, particularly wind power, where IGBTs are critical for turbine inverters. While facing competitive pressure from Asia-Pacific in terms of volume manufacturing, Europe maintains an edge in high-reliability and automotive-grade components, supported by a strong base of semiconductor suppliers and research institutions focused on energy efficiency.

South America

The South American market for IGBTs and MOSFETs is developing, with growth primarily driven by the gradual modernization of industrial infrastructure and initial steps toward renewable energy adoption. The industrial sector’s need for motor drives and power supplies presents opportunities, though the market size is smaller compared to other regions. The automotive industry is in the early stages of electrification, limiting current demand for high-power automotive semiconductors. Investment in infrastructure, particularly in larger economies, could stimulate future growth, but the market currently faces challenges related to economic volatility and less mature semiconductor supply chains compared to global leaders.

Middle East & Africa

This region represents an emerging market with potential driven by infrastructure development and diversification efforts away from oil-dependent economies. Investments in construction, industrial projects, and initial forays into renewable energy, such as large-scale solar farms, create niche demand for IGBTs and MOSFETs in power conversion and control systems. The automotive market is predominantly focused on conventional vehicles, with electric vehicle adoption still in its infancy. Overall market growth is expected to be gradual, tied to economic development programs and the building of essential industrial and energy infrastructure across the region.

Report Scope

This market research report provides a comprehensive analysis of the IGBT and MOSFET Market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of IGBT and MOSFET Market?

-> IGBT and MOSFET Market was valued at USD 13.62 billion in 2024 to USD 23.64 billion by 2032, exhibiting a CAGR of 8.3% during the forecast period.

Which key companies operate in IGBT and MOSFET Market?

-> Key players include Infineon Technologies, ON Semiconductor, Toshiba, STMicroelectronics, and Renesas Electronics, among others. The top five companies account for about 55% of the global market share.

What are the key growth drivers?

-> Key growth drivers include increasing demand from the consumer electronics and new energy industries, technological advancements in power semiconductors, and the expansion of industrial automation and telecommunications infrastructure.

Which region dominates the market?

-> Asia-Pacific is the largest market, holding a share of over 57%, driven by strong manufacturing bases and high adoption in key countries like China, Japan, and South Korea.

What are the emerging trends?

-> Emerging trends include the rising adoption of MOSFETs (which hold over 60% product segment share), growth in the new energy sector, and the integration of advanced power semiconductors in smart consumer electronics and electric vehicles.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...