MARKET INSIGHTS

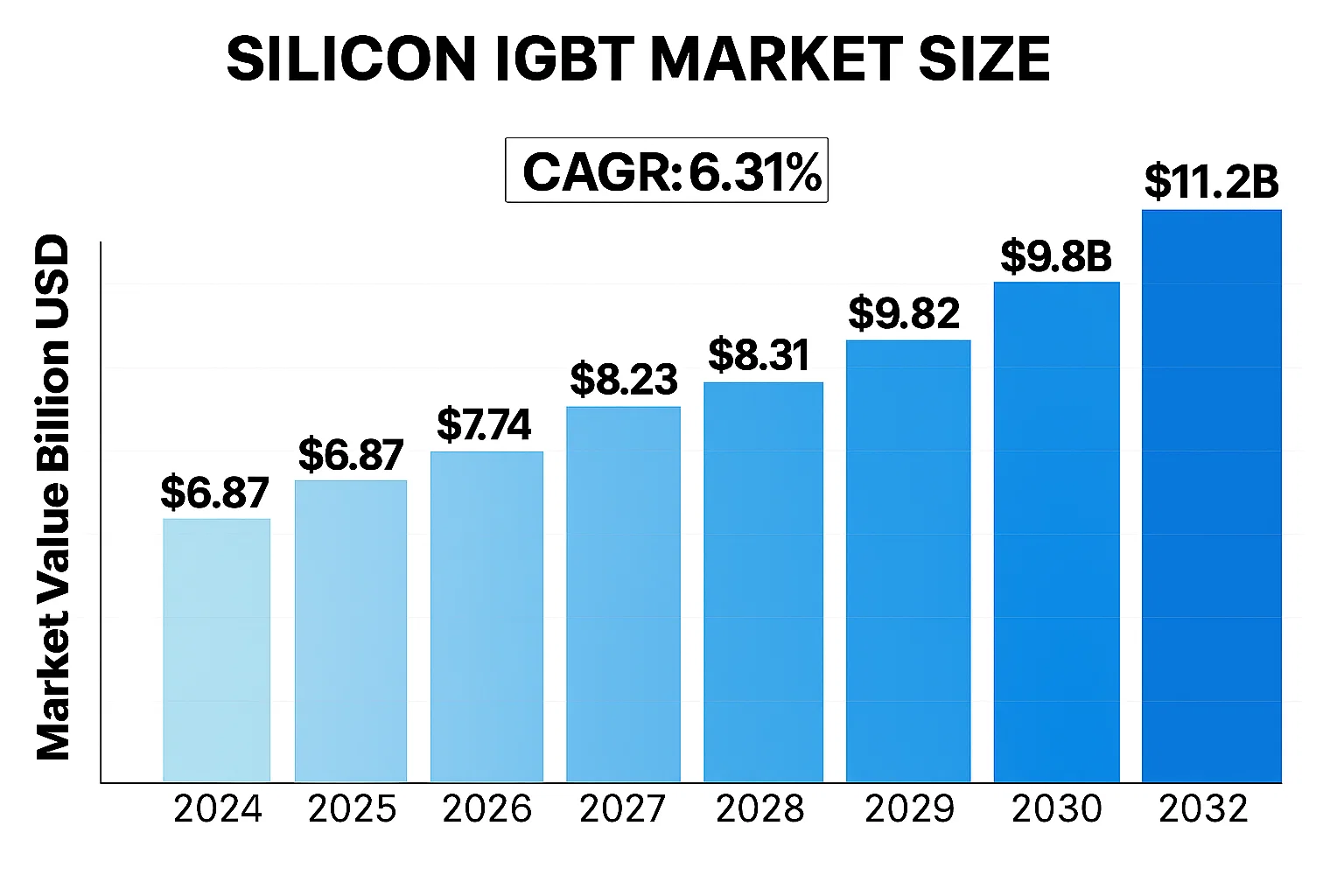

The global Silicon IGBT Market was valued at US$ 6.87 billion in 2024 and is projected to reach US$ 11.2 billion by 2032, at a CAGR of 6.31% during the forecast period 2025-2032.

Silicon IGBTs (Insulated Gate Bipolar Transistors) are power semiconductor devices that combine the high-speed switching performance of MOSFETs with the high-current handling capability of bipolar transistors. These components are critical for efficient power conversion and control in various applications, featuring voltage ratings ranging from less than 600V to over 3300V. Key types include discrete IGBTs, IGBT modules, and IPMs (Intelligent Power Modules).

The market growth is driven by increasing demand for energy-efficient power electronics across industries, particularly in electric vehicles, renewable energy systems, and industrial automation. While Asia-Pacific dominates production and consumption, Europe and North America show strong adoption due to stringent energy regulations. Recent developments include Infineon’s launch of their 1200V TRENCHSTOP™ IGBT7 series in 2023, offering 10% lower power losses compared to previous generations. Other major players like Mitsubishi Electric and Fuji Electric continue to innovate in silicon carbide hybrid IGBT technologies to bridge performance gaps.

Global Silicon IGBT Market: Market Dynamics Analysis

MARKET DYNAMICS

MARKET DRIVERS

Expansion of Electric Vehicles and Renewable Energy to Fuel Market Growth

The global shift toward electric vehicles (EVs) is creating unprecedented demand for silicon IGBT modules, which are critical components in EV powertrains and charging infrastructure. The EV market is projected to grow at a compound annual growth rate exceeding 20% through 2030, with annual sales expected to surpass 40 million units by the end of the decade. This growth directly correlates with increased IGBT adoption, as these semiconductors enable efficient power conversion and motor control. Major automotive manufacturers are accelerating their transition to electric fleets, further stimulating the silicon IGBT market.

Industrial Automation and Smart Manufacturing Adoption to Drive Demand

Industrial automation is undergoing rapid transformation with Industry 4.0 technologies, requiring advanced power electronics solutions. Silicon IGBTs play a pivotal role in motor drives, robotics, and automated production lines where precise power control is essential. The industrial automation market is experiencing 8-10% annual growth, with Asia-Pacific leading the expansion. Modern manufacturing facilities increasingly incorporate IGBT-based variable frequency drives that offer 20-30% energy savings compared to conventional systems. This efficiency advantage drives replacement demand across manufacturing sectors.

Grid Modernization Initiatives to Accelerate IGBT Implementation

Global investments in smart grid infrastructure and renewable energy integration are creating robust demand for high-power IGBT modules. These components are essential for HVDC transmission systems and grid-scale renewable energy projects. Annual investments in grid modernization exceed $250 billion worldwide, with particular focus on HVDC links that require hundreds of IGBT modules per installation. The transition from thyristors to IGBT-based solutions in power transmission offers superior control and efficiency, with modern HVDC converters achieving efficiency levels above 99%.

MARKET RESTRAINTS

Supply Chain Vulnerabilities and Material Shortages to Constrain Market Growth

While demand for silicon IGBTs is robust, the market faces significant supply chain challenges. The semiconductor industry has experienced lead times extending to 12-18 months for certain IGBT modules, creating bottlenecks for manufacturers. Specialty materials like high-purity silicon wafers and advanced packaging components face periodic shortages. These disruptions have led to price increases of 15-25% for some IGBT product categories over the past two years, potentially slowing market expansion.

Thermal Management Challenges in High-Power Applications

As power densities increase in modern electronics, thermal management becomes a critical limitation for IGBT performance. Power modules operating at voltage ratings above 1700V face significant heat dissipation challenges, with junction temperatures potentially reaching 175°C during peak loads. This thermal stress can reduce module lifespan by 30-40% in demanding applications, necessitating expensive cooling solutions. The additional cooling requirements can increase system costs by 15-20%, potentially making alternative technologies more attractive in some applications.

Regulatory Compliance Costs Impacting Profit Margins

Stringent environmental regulations governing semiconductor manufacturing are increasing production costs for IGBT manufacturers. Compliance with regulations such as RoHS and REACH requires significant capital investments in cleaner production technologies and material substitutions. These regulatory requirements can add 5-7% to manufacturing costs, which is particularly challenging for mid-size manufacturers competing with larger firms that benefit from economies of scale.

MARKET OPPORTUNITIES

Emerging Wide Bandgap Semiconductor Technologies to Create Synergistic Growth

The development of silicon carbide (SiC) and gallium nitride (GaN) technologies presents complementary opportunities rather than replacements for silicon IGBTs. Hybrid solutions combining silicon IGBTs with wide bandgap devices are emerging in applications requiring optimal performance across different power ranges. The market for these hybrid solutions is projected to grow at 25% annually, creating new avenues for silicon IGBT suppliers to participate in next-generation power electronics.

Energy Storage System Expansion to Drive New Demand

Large-scale energy storage systems for renewable energy integration require sophisticated power conversion systems using IGBT modules. With global energy storage capacity expected to quadruple by 2030, this represents a substantial growth opportunity. Modern grid-scale battery systems typically incorporate multiple IGBT-based inverters, with each 1MWh system requiring 4-6 high-power modules. This emerging application could account for 15-20% of total IGBT demand within five years.

Aftermarket and Replacement Demand in Mature Markets

The installed base of IGBT-containing equipment in industrial applications creates ongoing replacement demand. Power modules typically require replacement every 7-10 years in continuous operation, creating a stable aftermarket. In developed markets, replacement demand accounts for 30-40% of annual IGBT sales, providing manufacturers with recurring revenue streams independent of new system sales cycles.

MARKET CHALLENGES

Intellectual Property Protection in Competitive Markets

The silicon IGBT market faces growing challenges from intellectual property infringement, particularly in price-sensitive regions. Counterfeit components and unauthorized manufacturing of patented designs account for 5-8% of the global market, undermining legitimate manufacturers. These issues are particularly prevalent in the aftermarket segment, where quality variations can lead to system failures and damage brand reputations.

Skilled Workforce Shortages in Power Electronics

The specialized nature of power electronics design and manufacturing requires engineers with expertise in both semiconductor physics and power systems. The industry faces a workforce gap with demand for qualified power electronics engineers exceeding supply by 20-25% annually. This talent shortage is particularly acute in emerging markets, potentially limiting regional manufacturing expansion plans.

Technology Transition Risks from Next-Generation Alternatives

While silicon IGBTs maintain cost advantages for many applications, emerging technologies create market uncertainty. SiC MOSFETs are achieving price parity with IGBTs in certain voltage ranges, particularly in the 600V-1200V spectrum. This competitive pressure requires IGBT manufacturers to continuously improve performance and reduce costs through packaging innovations and manufacturing optimizations to maintain market position.

SILICON IGBT MARKET TRENDS

Electrification of Automotive Industry Driving Demand for High-Power IGBTs

The rapid electrification of the automotive sector is significantly boosting the Silicon IGBT market, with electric vehicles (EVs) and hybrid electric vehicles (HEVs) requiring high-efficiency power semiconductors for inverters and converters. Modern EVs utilize IGBT modules rated between 600V to 1200V for traction systems, which account for over 30% of the power semiconductor content in electric drivetrains. While traditional combustion engine vehicles use about $50 worth of power electronics, EVs require nearly $400 worth, with IGBTs forming a critical component. This growing demand is further supported by government policies promoting EV adoption globally, with China, Europe and North America leading installations.

Other Trends

Renewable Energy Integration

The renewable energy sector’s expansion is accelerating IGBT adoption in solar inverters and wind power converters. Modern photovoltaic systems increasingly utilize 1700V IGBT modules to handle higher voltage requirements while maintaining efficiency. Wind turbines rated above 2MW predominantly use press-pack IGBTs in their power conversion systems. This trend aligns with global renewable capacity additions which grew by over 9% annually in recent years.

Technological Advancements in Wide Bandgap Semiconductors

While Silicon IGBTs continue to dominate power electronics, the market faces competitive pressure from emerging wide bandgap technologies like Silicon Carbide (SiC) and Gallium Nitride (GaN). These materials offer superior efficiency, especially in high-frequency applications. However, IGBT manufacturers have responded with advanced trench-gate field-stop technologies that reduce conduction losses by up to 20% compared to conventional designs. This ongoing innovation helps maintain Silicon IGBT’s cost-performance advantage in medium-voltage applications ranging from industrial motor drives to UPS systems.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation and Strategic Partnerships Drive Market Competition

The global silicon IGBT market exhibits a moderately consolidated structure, dominated by established semiconductor players with extensive R&D capabilities and global distribution networks. Infineon Technologies leads the competitive landscape, commanding approximately 30% market share in 2024 due to its comprehensive product portfolio spanning multiple voltage ranges and applications including automotive and industrial drives.

ON Semiconductor and STMicroelectronics follow closely, collectively accounting for nearly 25% of the market. Their competitive edge stems from continuous investments in wide-bandgap semiconductor technologies and strategic supply agreements with major automotive OEMs. The European players benefit from strong regional demand in industrial automation and renewable energy sectors.

Asian manufacturers like Mitsubishi Electric and Fuji Electric are gaining traction through cost-competitive offerings tailored for consumer electronics and emerging EV markets. Recent capacity expansions in Southeast Asia have strengthened their position in price-sensitive segments while maintaining technological parity.

The market also features specialized players such as SEMIKRON and IXYS Corporation (acquired by Littelfuse) focusing on niche high-power applications. These companies differentiate through application-specific solutions and robust after-sales support networks, particularly in the renewables and traction sectors.

List of Key Silicon IGBT Manufacturers

- Infineon Technologies AG (Germany)

- ON Semiconductor (U.S.)

- STMicroelectronics (Switzerland)

- Mitsubishi Electric Corporation (Japan)

- Rohm Semiconductor (Japan)

- Fuji Electric Co., Ltd. (Japan)

- SEMIKRON International (Germany)

- ABB Ltd. (Switzerland)

- IXYS Corporation (U.S.) – Subsidiary of Littelfuse

- Starpower Semiconductor (China)

Market competition intensifies as players expand production capacities and develop next-generation silicon carbide (SiC) hybrid modules. The automotive sector’s electrification push particularly drives innovation, with major suppliers securing long-term contracts from EV manufacturers. While pricing pressures remain challenging in consumer applications, the shift towards higher voltage variants (1200V+) creates growth opportunities for technologically advanced players.

Segment Analysis:

By Type

600V to 1200V Segment Dominates Due to High Adoption in Industrial Applications

The global Silicon IGBT market is segmented based on voltage capacity into:

- Less Than 600V

- 600V to 1200V

- 1200V to 1700V

- 1700V to 3300V

- More Than 3300V

By Application

Industrial Drives Remain Key Application Segment for Silicon IGBTs

The market is segmented by application into:

- Industrial Drives

- Consumer Electronics

- Automotive

- Renewable Energy

- Traction Systems

By End-User Industry

Manufacturing Sector Accounts for Significant Market Share

The market is segmented by end-user industry into:

- Power Generation

- Manufacturing

- Automotive

- Consumer Electronics

- Rail Transportation

By Packaging Technology

Module Packaging Leads Due to Thermal Efficiency Advantages

The market is segmented by packaging technology into:

- Discrete

- Module

- Intelligent Power Module (IPM)

Regional Analysis: Global Silicon IGBT Market

North America

The North American silicon IGBT market is characterized by advanced industrial automation and rapid adoption of renewable energy solutions. With major manufacturing hubs in the U.S. and Canada, the region demonstrates significant demand for high-voltage IGBT modules (1700V-3300V) for industrial drives and power transmission. Stringent energy efficiency regulations, particularly in the automotive sector with the shift toward EVs, are accelerating IGBT adoption. However, the market faces challenges from the emerging silicon carbide (SiC) technology, particularly in premium applications. Companies like ON Semiconductor and Infineon dominate the supply chain, with R&D focused on minimizing switching losses in next-gen power modules.

Europe

Europe’s mature industrial base and aggressive renewable energy targets (40% electricity from renewables by 2030) sustain consistent IGBT demand. Germany leads in manufacturing traction inverters and wind turbine converters, with STMicroelectronics and ABB playing pivotal roles. The automotive sector’s electrification push, supported by EU emissions policies, drives 600V-1200V IGBT adoption for hybrid/EV powertrains. However, the region faces pricing pressures from Asian manufacturers and increasing competition from GaN-based solutions in low-voltage applications. Recent investments in smart grid infrastructure are creating new opportunities for medium-voltage IGBT modules in the 1200V-1700V range.

Asia-Pacific

As the largest and fastest-growing IGBT market, Asia-Pacific accounts for over 60% of global consumption, fueled by China’s dominance in power electronics manufacturing. Japan’s Mitsubishi and Fuji Electric lead technological innovation, while Chinese players like Starpower Semiconductor are gaining traction through cost-competitive solutions. The region sees massive demand across all voltage ranges: from <600V modules for consumer appliances to >3300V solutions for HVDC transmission. India’s expanding industrial sector and Southeast Asia’s electronics boom present new growth avenues. Challenges include price volatility in the silicon supply chain and quality inconsistencies among second-tier suppliers.

South America

The South American market remains niche but promising, with Brazil and Argentina driving most demand through industrial modernization projects. Medium-voltage IGBTs (1200V-3300V) find applications in mining equipment and renewable energy systems, though adoption rates lag behind global averages due to economic instability. Limited local manufacturing means heavy reliance on imports from Europe and Asia. Recent infrastructure investments in Chile’s solar sector and Colombia’s rail electrification projects indicate potential for market expansion, provided political and currency risks remain manageable.

Middle East & Africa

This emerging market shows gradual IGBT adoption, primarily for oil/gas applications and renewable energy projects in GCC countries. South Africa serves as the manufacturing hub for southern Africa, with demand centered around 600V-1700V modules for industrial motor drives. The lack of local semiconductor fabrication restricts market growth, though partnerships with Asian suppliers are improving access. While the market currently represents less than 5% of global IGBT consumption, large-scale projects like Saudi Arabia’s NEOM smart city could drive significant demand for power electronics in the coming decade.

Report Scope

This market research report provides a comprehensive analysis of the Global and regional Silicon IGBT markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global Silicon IGBT market was valued at USD 7.2 billion in 2024 and is projected to reach USD 11.5 billion by 2032, growing at a CAGR of 6.1%.

- Segmentation Analysis: Detailed breakdown by product type (voltage rating), technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, with country-level analysis for major economies.

- Competitive Landscape: Profiles of leading market participants including Infineon, ON Semiconductor, STMicroelectronics, Mitsubishi Electric, and others, covering their product portfolios, market share, and strategic initiatives.

- Technology Trends & Innovation: Assessment of emerging technologies including wide-bandgap semiconductors, integration of AI in power electronics, and next-generation fabrication techniques.

- Market Drivers & Restraints: Evaluation of factors such as electric vehicle adoption, renewable energy growth, and industrial automation alongside challenges like supply chain disruptions and material shortages.

- Stakeholder Analysis: Strategic insights for component manufacturers, system integrators, investors, and policymakers regarding the evolving power electronics ecosystem.

The research employs both primary and secondary methodologies, including interviews with industry experts, analysis of financial reports, and market intelligence from verified sources to ensure data accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Silicon IGBT Market?

->Silicon IGBT Market was valued at US$ 6.87 billion in 2024 and is projected to reach US$ 11.2 billion by 2032, at a CAGR of 6.31% during the forecast period 2025-2032.

Which key companies operate in Global Silicon IGBT Market?

-> Key players include Infineon Technologies, ON Semiconductor, STMicroelectronics, Mitsubishi Electric, Fuji Electric, and SEMIKRON, among others.

What are the key growth drivers?

-> Key growth drivers include electric vehicle adoption, renewable energy expansion, industrial automation trends, and 5G infrastructure development.

Which region dominates the market?

-> Asia-Pacific dominates the market with over 60% share, driven by manufacturing hubs in China, Japan, and South Korea, while North America shows fastest growth.

What are the emerging trends?

-> Emerging trends include wide-bandgap semiconductor adoption, integration of AI in power management, and development of ultra-high voltage IGBT modules.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...