MARKET INSIGHTS

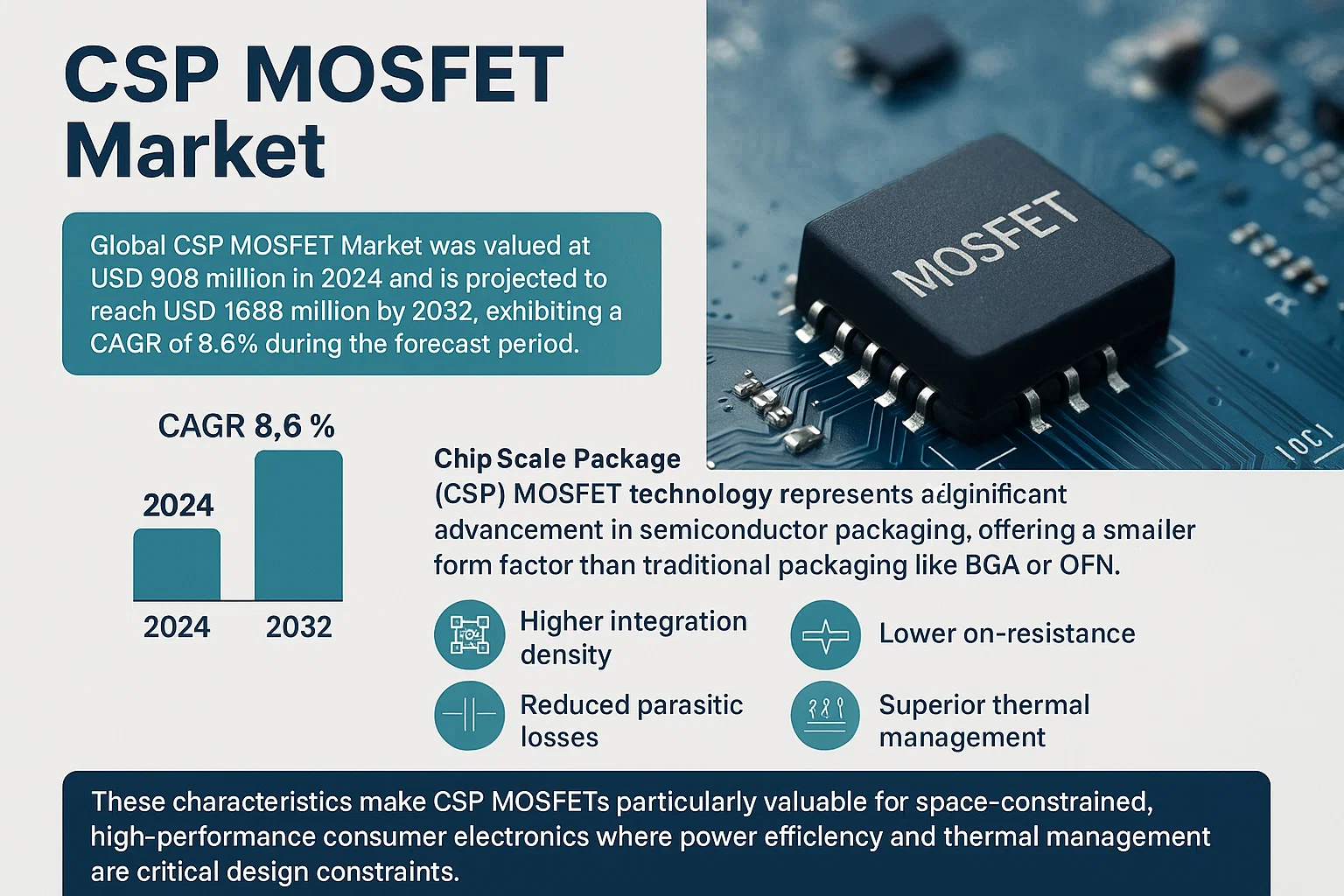

Global CSP MOSFET Market was valued at USD 908 million in 2024 and is projected to reach USD 1688 million by 2032, exhibiting a CAGR of 8.6% during the forecast period.

Chip Scale Package (CSP) MOSFET technology represents a significant advancement in semiconductor packaging, offering a smaller form factor than traditional packaging like BGA or QFN. The key differentiators include higher integration density, reduced parasitic losses, lower on-resistance, and superior thermal management due to direct die attach techniques. These characteristics make CSP MOSFETs particularly valuable for space-constrained, high-performance consumer electronics where power efficiency and thermal management are critical design constraints.

The market growth is primarily driven by the exponential growth in high-performance mobile devices, increasing adoption of Internet of Things (IoT) devices, and the ongoing miniaturization trend across all electronics sectors. The transition to 5G networks globally has also created additional demand for high-frequency, high-efficiency power components in both infrastructure and end-user devices.

Recent technological advancements include the development of Gallium Nitride (GaN) based CSP MOSFETs which offer superior switching characteristics and higher temperature operation compared to traditional Silicon-based devices. These are finding increasing adoption in high-end consumer electronics, automotive applications, and data center power management systems. Major manufacturers are also focusing on developing Silicon Carbide (SiC) variants for high-voltage applications above 600V.

The Asia-Pacific region dominates both production and consumption, accounting for approximately 78% of global CSP MOSFET manufacturing capacity and 65% of consumption in 2024. This concentration is primarily due to the region’s dominance in consumer electronics manufacturing and the presence of leading semiconductor foundries in China, Taiwan, South Korea, and Japan. North America and Europe remain significant markets for high-performance applications, particularly in automotive, industrial, and defense sectors where reliability requirements often justify premium pricing.

Recent supply chain disruptions and semiconductor shortages have accelerated the adoption of CSP MOSFETs in some applications as manufacturers seek higher integration and better component utilization. The ongoing recovery from the COVID-19 pandemic has also accelerated digital transformation initiatives across industries, further driving demand for efficient power management components.

MARKET DRIVERS

Proliferation of Power-Dense Electronics

The increasing miniaturization of consumer electronics, automotive systems, and telecommunications infrastructure is a primary driver. CSP (Chip Scale Package) MOSFETs offer a significantly smaller footprint and lower profile compared to traditional packages, enabling sleeker and more powerful devices. The demand for higher power density in applications like smartphones, wearables, and server power supplies directly fuels the adoption of these components.

Advancements in Efficiency and Thermal Performance

Continuous innovation in semiconductor materials and packaging technology has led to CSP MOSFETs with lower on-resistance (RDS(on)) and improved thermal characteristics. This results in higher energy efficiency and reduced heat generation, which is critical for battery life in portable devices and for reliability in high-performance computing. The push for greener electronics further accelerates this trend.

➤ The global shift towards electric vehicles and renewable energy systems represents a massive growth vector, as these applications require compact, efficient power management solutions.

Furthermore, the expansion of 5G infrastructure and Internet of Things (IoT) devices creates sustained demand. These technologies rely on efficient power amplifiers and voltage regulators, areas where CSP MOSFETs excel due to their high-frequency switching capabilities and miniaturized form factor.

MARKET CHALLENGES

Thermal Management and Reliability Concerns

While CSP MOSFETs are efficient, their extremely small size poses significant challenges for heat dissipation. Managing junction temperatures to prevent overheating and ensure long-term reliability requires sophisticated PCB design, thermal vias, and sometimes external heat sinks, adding complexity and cost to system integration. This is particularly critical in high-power applications.

Other Challenges

Manufacturing Complexity and Cost Sensitivity

The fabrication and assembly processes for CSP MOSFETs are more complex than for larger packages, involving delicate handling and precise mounting techniques. This can lead to higher initial production costs and requires significant investment in advanced manufacturing equipment, making the market sensitive to yield rates and material costs.

Testing and Inspection Difficulties

The miniature size of CSP packages makes traditional electrical testing and visual inspection more difficult. Ensuring quality control and identifying defects requires specialized, often more expensive, automated test equipment, which can be a barrier for smaller manufacturers.

MARKET RESTRAINTS

High Initial Costs and Economic Volatility

The advanced technology and materials required for producing high-performance CSP MOSFETs result in a higher price point compared to standard packages. During periods of economic uncertainty or reduced consumer spending, manufacturers of end devices may opt for more cost-effective, albeit less advanced, components, thereby restraining market growth.

Supply Chain Vulnerabilities

The global semiconductor supply chain has proven vulnerable to disruptions, as seen in recent chip shortages. CSP MOSFET production relies on a complex network of raw material suppliers and fabrication plants. Geopolitical tensions, trade restrictions, or logistical issues can lead to supply constraints, delaying product launches and increasing costs for OEMs.

MARKET OPPORTUNITIES

Expansion in Electric Vehicle Power Systems

The rapid electrification of the automotive industry presents a substantial opportunity. CSP MOSFETs are ideal for on-board chargers, battery management systems (BMS), and DC-DC converters in electric vehicles (EVs) due to their high efficiency and space-saving properties. As EV production scales globally, demand for these components is expected to surge.

Growth in Advanced Data Centers and AI Hardware

The exponential growth in data consumption and the rise of artificial intelligence are driving the need for more powerful and efficient data centers. CSP MOSFETs are critical for power delivery networks within servers and AI accelerators, where maximizing power density and minimizing losses are paramount. This sector offers a high-growth trajectory for advanced power semiconductors.

Adoption in Next-Generation Consumer Tech

Emerging consumer technologies such as augmented reality (AR)/virtual reality (VR) headsets, foldable displays, and advanced wearables require components that are both powerful and incredibly compact. CSP MOSFETs are perfectly positioned to enable these next-generation designs, opening new avenues for market expansion.

CSP MOSFET Market Trends

Sustained Growth Driven by Miniaturization Demands

The global CSP MOSFET market is demonstrating robust expansion, with its value projected to rise from $908 million in 2024 to $1,688 million by 2032, representing a compound annual growth rate of 8.6%. This strong growth trajectory is primarily fueled by the electronics industry’s relentless drive towards miniaturization and enhanced performance. CSP (Chip Scale Package) technology offers significant advantages over traditional packaging like BGA and QFN, including a smaller form factor, higher integration, and superior thermal management, which are critical for modern, compact electronic devices. The ability of CSP MOSFETs to minimize chip package size directly supports the development of smaller, lighter, and more power-efficient end-products, aligning with key industry trends.

Other Trends

Market Concentration and Competitive Landscape

The market structure is characterized by a high degree of concentration, with the top three manufacturers collectively holding approximately 59% of the global market share. Nuvoton is the dominant leader, accounting for more than 38% of the market. Other key players include Shenzhen Vergiga Semiconductor, Jiangsu Changjing Electronics Technology, AOS, and Vishay. This concentration underscores the importance of technological expertise and manufacturing scale in this specialized segment. Competition is largely based on product performance, reliability, and the ability to meet the stringent size and power requirements of leading OEMs.

Dominance of 12V CSP MOSFETs in Smartphone Applications

A clear product and application trend is the overwhelming dominance of the 12V CSP MOSFET segment, which holds more than 81% of the market share. This is closely tied to its primary application in Smartphone Lithium-Ion Batteries (LiB), which constitutes about 86% of the downstream market. The high demand is driven by the critical role these components play in power management within smartphones, managing battery charging, discharge, and protection circuits. The growth in smartphone adoption and the increasing complexity of their power systems continue to propel this segment. Wearable devices and tablets represent smaller but growing application areas as they similarly benefit from the miniaturization advantages of CSP packages.

Regional Market Dynamics

Geographically, the Asia-Pacific region, led by China, is the epicenter of both production and consumption for CSP MOSFETs. China is not only a major manufacturing hub with key domestic players but also the largest market due to its vast electronics production and consumer base. North America and Europe remain significant markets, driven by high-end consumer electronics and industrial applications. The regional analysis indicates that market growth potential is highest in emerging economies within Asia, where increasing smartphone penetration and local electronics manufacturing are creating substantial demand.

COMPETITIVE LANDSCAPE

Key Industry Players

A High-Growth Market Dominated by Specialized Suppliers

The global CSP MOSFET market is highly concentrated, with the top three manufacturers, Nuvoton, Shenzhen Vergiga Semiconductor, and Jiangsu Changjing Electronics Technology, collectively holding approximately 59% of the market share. Nuvoton stands as the unequivocal market leader, commanding a significant share of more than 38%. This concentration is driven by the technical expertise and manufacturing scale required to produce these advanced, miniaturized components. The competitive dynamics are shaped by the intense demand from the smartphone industry, which accounts for the vast majority of CSP MOSFET applications, compelling manufacturers to focus on cost-efficiency, reliability, and thermal performance.

Beyond the dominant players, the market includes several important international and regional suppliers that serve specific niches or geographic segments. Companies such as Texas Instruments (TI), Toshiba, and ON Semiconductor bring established global distribution and robust R&D capabilities, particularly for higher voltage segments and applications beyond smartphones like wearable devices and tablets. Other notable manufacturers, including AOS, Vishay, and OmniVision Group, along with specialized Chinese firms like Shenzhen China Micro Semicon and Wuxi NCE Power, compete by offering tailored solutions and competing aggressively on price, contributing to a diverse and dynamic competitive environment.

List of Key CSP MOSFET Companies Profiled

- Nuvoton

- Shenzhen Vergiga Semiconductor

- Jiangsu Changjing Electronics Technology

- AOS

- ON Semiconductor

- Vishay

- Shenzhen China Micro Semicon

- Shenzhen CF-xpower Semiconductor

- Niko Semiconductor

- Toshiba

- OmniVision Group

- Wuxi NCE Power

- Texas Instruments (TI)

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

12V CSP MOSFET leads the type segment, primarily driven by its critical role in low-voltage, high-efficiency power management applications essential for modern portable electronics. The widespread adoption in devices like smartphones has cemented its dominance, as this voltage rating offers an optimal balance between performance and power consumption for battery-operated systems. Furthermore, advancements in semiconductor fabrication have enhanced the performance characteristics of 12V variants, making them the preferred choice for designers aiming to minimize the footprint of power circuits without compromising on thermal management or switching capabilities. |

| By Application |

|

Smartphone LiB dominates the application landscape, with CSP MOSFETs being integral to sophisticated battery management and power switching functions that ensure device longevity and safe charging. The relentless drive for thinner and lighter smartphones necessitates components like CSP MOSFETs that offer superior miniaturization advantages over traditional packages. This segment benefits from continuous innovation in fast-charging technologies and the increasing power density requirements of modern smartphone platforms, creating sustained and robust demand for high-performance CSP MOSFET solutions tailored to this high-volume market. |

| By End User |

|

Consumer Electronics OEMs represent the most significant end-user segment, leveraging CSP MOSFETs to achieve critical design goals of miniaturization and enhanced thermal performance in products like smartphones, wearables, and tablets. This leadership is fueled by the segment’s high-volume production, intense competition, and rapid product cycles that consistently demand the latest component technologies. The trend towards more compact and power-efficient devices ensures that consumer electronics OEMs remain the primary driver for innovation and volume consumption, with suppliers prioritizing this segment for new product development and capacity allocation. |

| By Package Advantage |

|

Miniaturization Focus is the leading driver within the package advantage segmentation, as the primary value proposition of CSP technology is its significantly reduced footprint compared to traditional BGA or QFN packages. This advantage is critically important for manufacturers of portable and space-constrained electronic devices, enabling sleeker product designs and higher component density on printed circuit boards. The evolution towards ever-smaller form factors across the electronics industry ensures that the demand for components that contribute to miniaturization remains exceptionally strong, with CSP MOSFETs being a key enabler in this ongoing trend. |

| By Regional Demand Dynamics |

|

Asia-Pacific Manufacturing Hub exhibits the most influential demand dynamics, characterized by the concentration of major consumer electronics assembly plants and a strong base of semiconductor manufacturing and packaging. This region’s dominance is reinforced by the presence of key market leaders and a robust supply chain ecosystem that facilitates high-volume production and cost-effective manufacturing. The synergistic relationship between local component suppliers and global device manufacturers in this region creates a powerful demand pull, making it the central axis for both production and consumption of CSP MOSFETs, driven by the relentless output of smartphones and other portable devices. |

Regional Analysis: CSP MOSFET Market

The region’s dominance is anchored by its extensive network of semiconductor fabrication and advanced packaging facilities. Countries like Taiwan, China, and South Korea possess world-leading capabilities in wafer-level packaging and other technologies crucial for producing high-density CSP MOSFETs at competitive costs. This concentrated manufacturing ecosystem provides unparalleled scale and supply chain efficiencies for global electronics brands.

Explosive demand from consumer electronics, automotive electrification, and industrial automation within the region itself creates a powerful pull for CSP MOSFETs. The world’s largest markets for smartphones, EVs, and IoT devices are located here, requiring the miniaturization and power efficiency that CSP packaging offers. This internal consumption drives continuous innovation and production volume.

Strong governmental initiatives, particularly in China, Japan, and South Korea, aim to bolster domestic semiconductor sovereignty. These policies include substantial subsidies for R&D and manufacturing capacity expansion, specifically targeting advanced packaging technologies like those used for CSP MOSFETs. This strategic focus ensures long-term investment and technological advancement in the region.

A dense concentration of leading semiconductor companies and research institutions fosters a highly competitive and innovative environment for CSP MOSFET development. Collaborative efforts between foundries, IDMs, and academic centers in the region are consistently pushing the boundaries of thermal performance, power density, and reliability for next-generation applications.

North America

North America remains a critical and highly advanced market for CSP MOSFETs, characterized by strong demand from the aerospace, defense, and high-performance computing sectors. The region is a hub for innovation, with significant R&D activities focused on developing next-generation power semiconductors for demanding applications like data centers, renewable energy systems, and electric vehicle power trains. Leading semiconductor companies and fabless design houses in the United States and Canada drive specifications for high-reliability and high-frequency CSP MOSFETs. While manufacturing capacity is more limited compared to Asia-Pacific, the region’s strength lies in its design expertise, intellectual property creation, and its focus on premium, high-margin applications that require cutting-edge performance and quality.

Europe

Europe holds a strong position in the CSP MOSFET market, particularly within the automotive and industrial sectors. The region’s stringent energy efficiency regulations and ambitious green deal initiatives are powerful drivers for the adoption of efficient power components like CSP MOSFETs. Major automotive OEMs and tier-one suppliers in Germany, France, and Italy are integrating these components into a new generation of electric and hybrid vehicles, as well as advanced driver-assistance systems. The presence of several major semiconductor manufacturers with specialized automotive-grade product lines supports this demand. Europe’s market is defined by a focus on quality, reliability, and compliance with rigorous environmental and safety standards, often catering to premium application segments.

South America

The CSP MOSFET market in South America is in a developing stage, with growth primarily fueled by the gradual modernization of industrial automation and the nascent electric vehicle sector, particularly in Brazil and Argentina. The market is characterized by import dependency, with most components sourced from Asia and North America. Local demand stems from consumer electronics assembly, industrial equipment upgrades, and telecommunications infrastructure projects. While the market volume is smaller compared to other regions, it presents a growth opportunity as economic conditions stabilize and investment in technological infrastructure increases, creating a gradual but steady uptake for efficient power management solutions.

Middle East & Africa

The Middle East & Africa region represents an emerging market for CSP MOSFETs, with growth potential linked to infrastructure development and economic diversification efforts. In the Middle East, investments in smart city projects, telecommunications (especially 5G), and renewable energy installations are beginning to generate demand for advanced power semiconductors. Africa’s market is more fragmented, with demand emerging from the telecommunications sector and the gradual expansion of consumer electronics markets in urban centers. The region overall is characterized by a developing supply chain and a focus on cost-effective solutions, with significant potential for future growth as digitalization and industrialization initiatives gain momentum.

Report Scope

This market research report provides a comprehensive analysis of the CSP MOSFET Market , covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of CSP MOSFET Market?

-> Global CSP MOSFET Market was valued at USD 908 million in 2024 and is projected to reach USD 1688 million by 2032, growing at a CAGR of 8.6% during the forecast period.

Which key companies operate in CSP MOSFET Market?

-> Key players include Nuvoton, Shenzhen Vergiga Semiconductor, Jiangsu Changjing Electronics Technology, AOS, OmniVision Group, Vishay, Shenzhen China Micro Semicon, Shenzhen CF-xpower Semiconductor, Niko Semiconductor, Toshiba, Onsemi, Wuxi NCE Power, and TI, among others.

What are the key growth drivers?

-> Key growth drivers include the superior package advantages of CSP technology, such as smaller size, higher integration, lower energy consumption, and better thermal management, which support the miniaturization and lightweight design of electronic devices.

Which region dominates the market?

-> China is a key market, with major manufacturers like Nuvoton holding a dominant share. The Asia region leads in terms of production and consumption.

What are the emerging trends?

-> Emerging trends include high adoption of 12V CSP MOSFETs, which hold over 81% market share, and the dominance of Smartphone LiB applications, accounting for approximately 86% of the market.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...