MARKET INSIGHTS

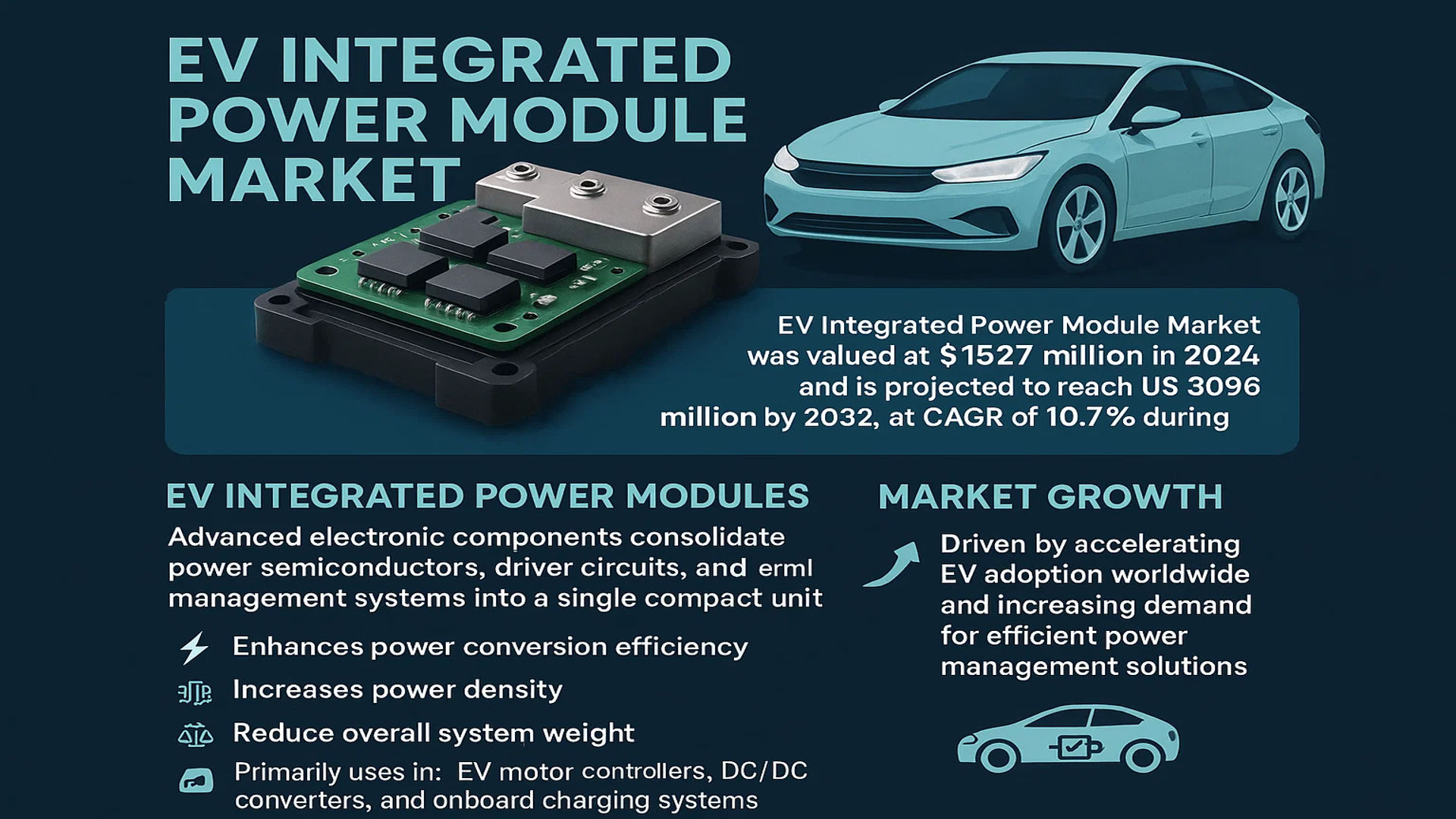

The global EV Integrated Power Module Market was valued at 1527 million in 2024 and is projected to reach US$ 3096 million by 2032, at a CAGR of 10.7% during the forecast period.

EV Integrated Power Modules are advanced electronic components that consolidate power semiconductors, driver circuits, and thermal management systems into a single compact unit. These modules play a critical role in electric vehicle powertrains by enhancing power conversion efficiency, increasing power density, and reducing overall system weight. They are primarily used in EV motor controllers, DC/DC converters, and onboard charging systems to improve energy efficiency and vehicle performance.

The market growth is driven by accelerating EV adoption worldwide and increasing demand for efficient power management solutions. While the U.S. market is estimated at USD 450 million in 2024, China’s market is projected to reach USD 980 million by 2032. Furthermore, the Infotainment SiP Modules segment is expected to show significant growth potential. Key industry players including STMicroelectronics, Infineon, and Renesas are actively developing advanced power modules to meet the growing demand for high-performance EV components.

MARKET DYNAMICS

MARKET DRIVERS

Accelerating Global Adoption of Electric Vehicles to Fuel Demand for Integrated Power Modules

The rapid transition toward electric mobility is creating unprecedented demand for EV integrated power modules. With governments worldwide implementing stringent emissions regulations and offering purchase incentives, global EV sales reached approximately 10 million units in 2023, representing a 35% year-over-year increase. This surge directly correlates with growing requirements for efficient power management solutions that can optimize vehicle performance while extending battery life. Integrated power modules have become indispensable components in modern EVs, combining multiple functions that previously required separate systems. Their ability to reduce energy losses by 15-20% compared to discrete solutions makes them particularly attractive to automakers focused on maximizing range.

Technological Advancements in Power Electronics to Enhance Market Growth

Breakthroughs in semiconductor materials and packaging technologies are driving substantial improvements in power module performance and reliability. The industry has witnessed a 40% reduction in power losses for silicon carbide (SiC) based modules compared to traditional silicon solutions, while simultaneously increasing power density by 30%. These advancements enable more compact designs that save valuable space in electric vehicles while withstanding higher operating temperatures. Major manufacturers are investing heavily in next-generation wide bandgap semiconductors to maintain competitive advantage, with automotive-grade SiC power modules now demonstrating mean time between failures exceeding 100,000 hours under typical operating conditions.

Growing Emphasis on Vehicle Electrification Across Commercial Fleets to Expand Market Potential

Commercial vehicle electrification represents one of the fastest-growing segments for power module applications. With delivery vans, buses, and trucks accounting for 30-35% of transportation sector emissions, fleet operators are prioritizing electrification to meet sustainability targets. The heavier power requirements of commercial EVs create particularly strong demand for robust integrated solutions capable of handling 800-volt architectures and continuous high-current operation. This sector’s growth is further accelerated by government mandates, with several major markets requiring 100% zero-emission bus fleets by 2035, ensuring sustained demand for advanced power modules.

MARKET RESTRAINTS

High Development Costs and Complex Manufacturing Processes to Limit Market Penetration

While integrated power modules offer significant performance advantages, their sophisticated designs require substantial upfront investments that constrain market expansion. The development of automotive-grade modules typically involves 2-3 years of rigorous testing and validation, with qualification costs exceeding $10 million for new designs. Manufacturing these components demands specialized cleanroom facilities and precision assembly equipment, creating barriers to entry for smaller suppliers. Furthermore, the transition to wide bandgap semiconductors has increased material costs by 50-70% compared to conventional silicon solutions, prompting concerns about affordability in price-sensitive vehicle segments.

Thermal Management Challenges to Impact Reliability and Adoption Rates

Effective heat dissipation remains a persistent challenge for high-power integrated modules operating in demanding automotive environments. Despite advances in thermal interface materials and cooling systems, power electronics still account for approximately 25% of all EV warranty claims related to component failures. The industry continues to grapple with thermal cycling stresses that can reduce module lifespan by 30-40% in extreme operating conditions. These reliability concerns are particularly acute in regions with high ambient temperatures, where sustained operation at 125°C junction temperatures remains problematic for current generation devices.

Global Semiconductor Supply Chain Vulnerabilities to Constrain Market Growth

Recent disruptions in the semiconductor supply chain have exposed significant risks for power module production. The automotive industry’s transition to electrification has intensified competition for foundry capacity, with lead times for specialized power semiconductors extending to 50-60 weeks in some cases. Geopolitical tensions have further complicated material sourcing, particularly for rare earth elements and specialty substrates used in wide bandgap devices. These constraints come at a critical juncture when automakers require 40-50% more power electronics content per vehicle to support next-generation EV architectures.

MARKET OPPORTUNITIES

Emergence of 800V Vehicle Architectures to Create New Revenue Streams

The industry-wide shift toward 800-volt systems presents significant growth potential for advanced power module solutions. These high-voltage architectures enable 50% faster charging and 15-20% improved energy efficiency compared to conventional 400V systems, driving strong adoption among premium EV manufacturers. Power modules specifically designed for 800V operation command 30-40% higher average selling prices while addressing critical needs for reduced weight and improved thermal performance. With 25% of new EV platforms expected to adopt 800V architectures by 2026, suppliers have a clear pathway to premium market segments.

Expansion of Bidirectional Power Flow Capabilities to Enhance Value Proposition

Vehicle-to-grid (V2G) and vehicle-to-load (V2L) functionalities are creating fresh opportunities for power module innovation. Modern integrated solutions now incorporate bidirectional conversion capabilities that allow EVs to serve as mobile energy storage units, with demonstrated efficiency improvements of 5-7% over discrete implementations. This functionality has become particularly valuable as grid flexibility becomes increasingly important, with projections indicating 35% of fleet operators will require V2G compatibility by 2027. Power module manufacturers that can deliver compact, cost-effective solutions for bidirectional applications stand to gain substantial market share in coming years.

Regional Manufacturing Localization to Address Supply Chain and Cost Challenges

The growing emphasis on regional supply chains offers manufacturers strategic opportunities to strengthen market positions. Several governments are implementing incentive programs worth $50-100 billion collectively to establish domestic semiconductor and power electronics production capabilities. Localized manufacturing not only mitigates geopolitical risks but also reduces logistics costs by 15-20% while enabling faster response to automaker requirements. Major power module suppliers are establishing production facilities in key automotive regions, with 40% of new capacity investments targeting North American and European markets to capitalize on these trends.

MARKET CHALLENGES

Intense Competition and Pricing Pressures to Squeeze Profit Margins

The power module market faces growing price competition as new entrants attempt to capitalize on the EV boom. Intensifying rivalry has driven average selling prices down by 8-10% annually despite rising material and manufacturing costs. Established suppliers must balance the need for continued R&D investment against demands for cost reductions from automakers targeting 30-40% decreases in power electronics expenses by 2030. This challenging environment particularly affects suppliers lacking vertical integration, as they face margin compression from both upstream component suppliers and downstream automakers.

Rapid Technology Obsolescence to Increase Development Risks

The accelerated pace of innovation in power electronics creates significant challenges for product lifecycle management. New module architectures are becoming obsolete within 3-4 years as superior semiconductor materials and packaging techniques emerge, forcing suppliers to maintain aggressive development cycles. This rapid turnover imposes substantial engineering costs, with leading manufacturers allocating 15-25% of revenue to R&D to maintain technological leadership. The situation is further complicated by the automotive industry’s lengthy qualification processes, which can delay returns on innovation investments by 18-24 months.

Standardization Gaps to Hinder Widespread Adoption

The lack of uniform technical standards across the industry continues to impede market efficiency and scalability. With 10-15 competing module form factors currently in production, automakers face integration challenges that increase development costs by 20-30%. The absence of standardized thermal interfaces, electrical connections, and control protocols forces redundant engineering efforts across supply chains. While industry consortia have made progress in developing common specifications, full harmonization remains elusive due to competing commercial interests and divergent regional requirements.

EV INTEGRATED POWER MODULE MARKET TRENDS

Increased Vehicle Electrification to Drive Market Growth

The global EV Integrated Power Module market is witnessing significant expansion due to the rapid adoption of electric vehicles (EVs) worldwide. With a projected valuation of US$ 3096 million by 2032, growing at a CAGR of 10.7%, the demand for highly efficient power modules is accelerating. These modules play a crucial role in consolidating power semiconductor components, driver circuits, and thermal management into a single integrated solution, enhancing performance while reducing size and weight. Countries like China and the U.S. are leading investments in EV infrastructure and manufacturing, further boosting market demand.

Other Trends

Advancements in SiP Technology

System-in-Package (SiP) technology is revolutionizing the EV Integrated Power Module market by enabling higher energy efficiency and miniaturization. Modules such as Infotainment SiP and Driver Assistance SiP are increasingly integrated into modern EVs to improve connectivity and autonomous driving capabilities. As automotive manufacturers push for greater power density and reduced energy loss, semiconductor companies are focusing on advanced materials like silicon carbide (SiC) and gallium nitride (GaN) to optimize performance.

Expansion of Semiconductor Suppliers and Collaborations

The market is seeing strategic collaborations among key semiconductor players such as Infineon, STMicroelectronics, and Renesas, who collectively held a significant revenue share in 2024. These companies are expanding production capacities to meet the rising demand for EV power modules, particularly in regions like Asia-Pacific and Europe. Furthermore, innovations in DC/DC converters and onboard charging systems are improving power efficiency, ensuring longer battery life and faster charging for EV consumers. As regulatory frameworks tighten on emissions, automakers are under pressure to adopt these advanced modules, further propelling market expansion.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Manufacturers Focus on R&D and Market Expansion to Capture Growth

The global EV Integrated Power Module market features a competitive landscape dominated by semiconductor and automotive electronics specialists. The industry remains highly dynamic, with companies aggressively investing in research to develop energy-efficient power modules that meet the evolving demands of electric vehicle manufacturers. As of 2024, the top five players collectively hold a significant market share, though the space continues to attract new entrants aiming to capitalize on the rapid EV adoption worldwide.

STMicroelectronics and Infineon Technologies emerged as frontrunners, owing to their comprehensive product portfolios and strong relationships with automotive OEMs. Both companies have made substantial progress in silicon carbide (SiC) and gallium nitride (GaN) based power modules, which are gaining traction for their superior thermal performance and efficiency. Their continued R&D investments position them favorably in the high-growth EV sector.

Meanwhile, ROHM Semiconductor and Renesas Electronics are strengthening their positions through strategic partnerships and vertical integration. These players have focused on developing compact, high-power-density modules that meet the space constraints of modern EV designs. Recent collaborations with battery manufacturers and thermal management specialists have further enhanced their competitive edge in integrated power solutions.

The market also sees active participation from established players like Texas Instruments and onsemi, who are leveraging their analog and power management expertise to deliver optimized solutions for traction inverters and onboard chargers. Their extensive distribution networks and application support capabilities make them preferred partners for EV manufacturers scaling production globally.

List of Key EV Integrated Power Module Manufacturers

- STMicroelectronics (Switzerland)

- Infineon Technologies (Germany)

- Diodes Incorporated (U.S.)

- ROHM Semiconductor (Japan)

- Renesas Electronics (Japan)

- Fuji Electric (Japan)

- Texas Instruments (U.S.)

- Microchip Technology (U.S.)

- onsemi (U.S.)

- Toshiba Electronic Devices & Storage Corporation (Japan)

Segment Analysis:

By Type

Infotainment SiP Modules Segment Leads Due to Rising Demand for Advanced In-Vehicle Connectivity

The market is segmented based on type into:

- Infotainment SiP Modules

- Subtypes: Navigation systems, multimedia interfaces, and others

- Driver Assistance SiP Modules

- Voice Control SiP Modules

- Power Management Modules

- Subtypes: Motor controllers, DC/DC converters, and charging systems

- Others

By Application

Passenger Cars Segment Dominates Owing to Higher EV Adoption in Personal Transportation

The market is segmented based on application into:

- Passenger Cars

- Commercial Vehicles

- Subtypes: Electric buses, delivery vans, and heavy-duty trucks

By Functionality

Motor Control Modules Hold Significant Share for Efficient Power Conversion

The market is segmented based on functionality into:

- Motor Control Modules

- Battery Management Modules

- Charging System Modules

- Others

By Vehicle Class

Premium Vehicle Segment Emerges as Key Adopter of Advanced Power Modules

The market is segmented based on vehicle class into:

- Economy Vehicles

- Mid-range Vehicles

- Premium Vehicles

Regional Analysis: EV Integrated Power Module Market

Asia-Pacific

Asia-Pacific dominates the global EV Integrated Power Module market, driven by rapid EV adoption and strong manufacturing ecosystems. China, Japan, and South Korea accounted for over 60% of global EV production in 2024, creating massive demand for power modules. Local players like BYD and Tata Motors innovate aggressively while global suppliers like Fuji Electric and ROHM expand regional facilities. Government mandates such as India’s FAME-II subsidies and China’s NEV credit system accelerate market penetration, though supply chain bottlenecks occasionally disrupt production.

North America

Stringent emissions regulations under the U.S. Inflation Reduction Act (IRA), which allocates $370 billion for clean energy, are propelling EV component investments. Domestic automakers like Tesla and Rivian collaborate with semiconductor firms to develop proprietary power modules, reducing dependency on Asian imports. Canada’s Critical Minerals Strategy further strengthens regional supply chains. Challenges include high R&D costs and competition from established foreign manufacturers, but recent TSMC fab expansions in Arizona signal growing semiconductor localization.

Europe

The EU’s 2035 ICE vehicle ban and Euro 7 standards create urgent demand for efficient power modules. Germany’s automotive giants leverage partnerships with Infineon and STMicroelectronics to develop next-generation SiC-based solutions. France and the UK prioritize domestic production through initiatives like the European Chips Act, though reliance on Asian foundries remains. Stringent cybersecurity requirements for connected EVs add complexity, driving innovation in module-level encryption and failsafe mechanisms across the region.

South America

Brazil leads the region with 75% of its EV components imported, mainly from China. Argentina’s lithium reserves attract module manufacturers for localized battery production, but macroeconomic instability delays large-scale investments. Chile’s copper resources offer long-term potential for conductive components. While the regional market grows slowly due to infrastructure gaps, trade agreements with Asia promise future collaboration in technology transfer and localized assembly plants.

Middle East & Africa

The UAE and Saudi Arabia drive adoption through government fleet electrification programs and tax incentives. Turkish companies partner with European firms to establish module assembly units, while South Africa serves as an export hub. Africa’s lack of charging infrastructure limits growth, though Morocco’s automotive industry shows promise with Stellantis’ local EV production. Political and currency risks deter semiconductor investments, keeping the region dependent on imports despite abundant raw material availability.

Technology Spotlight: The shift to silicon carbide (SiC) and gallium nitride (GaN) semiconductors marks a key industry trend, enabling 15-20% efficiency gains in power modules. However, European and North American manufacturers face material sourcing challenges, while Asian firms benefit from established rare earth supply chains. This technological divergence will shape regional competitive advantages through 2030.

Report Scope

This market research report provides a comprehensive analysis of the global EV Integrated Power Module market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global EV Integrated Power Module market was valued at USD 1,527 million in 2024 and is projected to reach USD 3,096 million by 2032, growing at a CAGR of 10.7%.

- Segmentation Analysis: Detailed breakdown by product type (Infotainment SiP Modules, Driver Assistance SiP Modules, Voice Control SiP Modules, Others), application (Passenger Cars, Commercial Cars), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant. The U.S. market is estimated at USD million in 2024, while China is projected to reach USD million.

- Competitive Landscape: Profiles of leading market participants including STMicroelectronics, Infineon, Diodes Incorporated, ROHM, Renesas, Fuji Electric, Texas Instruments, Microchip, onsemi, and Toshiba, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments.

- Technology Trends & Innovation: Assessment of emerging technologies in power semiconductor integration, thermal management solutions, and evolving industry standards for EV power modules.

- Market Drivers & Restraints: Evaluation of factors driving market growth such as increasing EV adoption and government incentives, along with challenges like supply chain constraints and high development costs.

- Stakeholder Analysis: Insights for component suppliers, EV manufacturers, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global EV Integrated Power Module Market?

-> EV Integrated Power Module Market was valued at 1527 million in 2024 and is projected to reach US$ 3096 million by 2032, at a CAGR of 10.7% during the forecast period.

Which key companies operate in Global EV Integrated Power Module Market?

-> Key players include STMicroelectronics, Infineon, Diodes Incorporated, ROHM, Renesas, Fuji Electric, Texas Instruments, Microchip, onsemi, and Toshiba.

What are the key growth drivers?

-> Key growth drivers include rising EV adoption, government incentives for clean energy vehicles, and demand for more efficient power conversion systems.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region due to strong EV manufacturing presence in China, while North America shows significant growth potential.

What are the emerging trends?

-> Emerging trends include higher power density modules, advanced thermal management solutions, and integration of wide-bandgap semiconductors.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...