Dual quaternion based pose control for spacecraft on-orbit servicing Market Insights

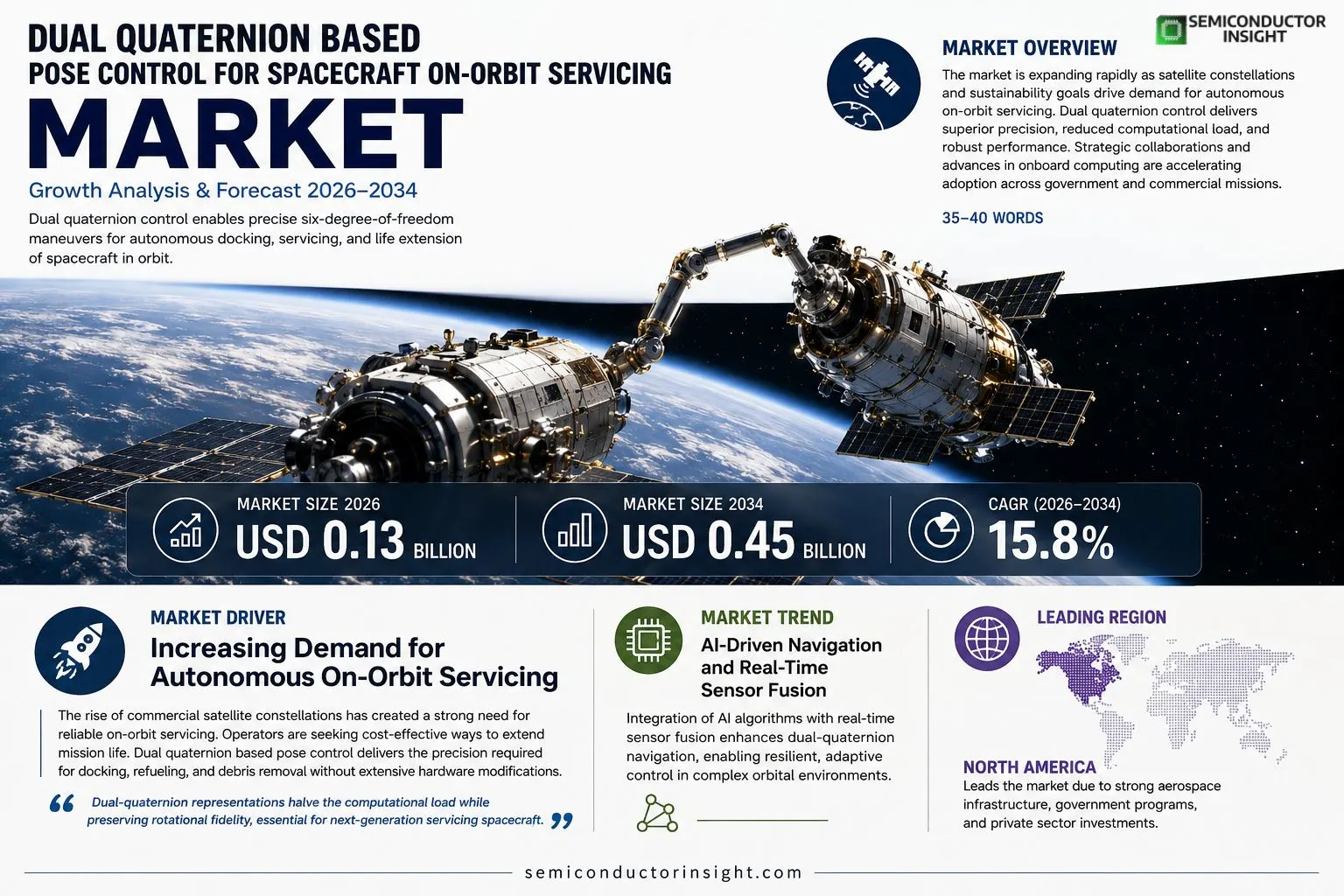

Dual quaternion based pose control for spacecraft on-orbit servicing market size was valued at USD 0.12 billion in 2025. The market is projected to grow from USD 0.13 billion in 2026 to USD 0.45 billion by 2034, exhibiting a CAGR of 15.8% during the forecast period.

Dual quaternion based pose control utilizes the algebra of dual quaternions to encode both rotation and translation of a servicer vehicle in a single eight‑parameter entity. This representation eliminates gimbal lock, reduces computational load compared with separate Euler angle or matrix methods, and enables smooth interpolation of six‑degree‑of‑freedom trajectories essential for precise docking, debris removal, and refuelling operations.The market is experiencing rapid expansion because large satellite constellations demand autonomous rendezvous capabilities while launch costs remain high; however, regulatory scrutiny around space debris adds complexity that drives investment in robust guidance solutions. Furthermore, advances in onboard processing power and sensor fusion make real‑time dual‑quaternion algorithms feasible aboard small platforms.

Key industry participants such as Lockheed Martin Space Systems, Northrop Grumman Innovation Systems, Airbus Defence & Space, Maxar Technologies and Thales Alenia Space are actively integrating dual‑quaternion controllers into their on‑orbit servicing prototypes.

Recent collaborations include NASA’s On‑Orbit Servicing Mission–3 partnership with Maxar announced in early 2024 and ESA’s joint venture with Airbus announced later that year to demonstrate autonomous capture using dual‑quaternion navigation.

MARKET DRIVERS

Increasing Demand for Autonomous On‑Orbit Servicing

The rise of commercial satellite constellations has created a strong need for reliable on‑orbit servicing. Operators are seeking cost‑effective ways to extend mission life, and Dual quaternion based pose control for spacecraft on-orbit servicing Market solutions provide the precision required for docking, refueling, and debris removal without extensive hardware modifications.

Advancements in Attitude Determination Algorithms

Recent breakthroughs in sensor fusion and real‑time computation have reduced latency in pose estimation. These algorithmic improvements enhance the robustness of dual‑quaternion frameworks, making them attractive for missions that demand high‑accuracy orientation control in dynamically changing orbital environments.

➤ “Dual‑quaternion representations halve the computational load while preserving rotational fidelity, essential for next‑generation servicing spacecraft.”

Government space agencies are allocating increased budgets for on‑orbit servicing research, further accelerating adoption. The combined effect of market demand, technological progress, and policy support positions Dual quaternion based pose control for spacecraft on-orbit servicing Market for rapid growth.

MARKET CHALLENGES

Technical Integration Complexity

Integrating dual‑quaternion control modules into legacy spacecraft architectures often requires redesign of existing guidance, navigation, and control (GNC) subsystems. Engineers must ensure compatibility with diverse propulsion and sensor suites, a process that can extend development timelines and increase risk.

Other Challenges

Regulatory and Certification Hurdles

Spaceflight safety regulations vary across jurisdictions, and certification of new control algorithms demands extensive testing. The lack of standardized certification pathways for dual‑quaternion based solutions adds uncertainty for commercial participants.

MARKET RESTRAINTS

High Development Costs

Developing and validating dual‑quaternion control software involves significant investment in simulation infrastructure, hardware‑in‑the‑loop testing, and flight‑qualified hardware. These upfront costs can deter smaller firms from entering Dual quaternion based pose control for spacecraft on-orbit servicing Market.Furthermore, the scarcity of engineers with deep expertise in quaternion algebra and spacecraft dynamics limits the ability to scale development teams quickly, creating a talent bottleneck that restrains broader market participation.

MARKET OPPORTUNITIES

Emerging Commercial Satellite Servicing Platforms

New entrants are launching dedicated servicing vehicles designed to perform autonomous rendezvous and capture operations. These platforms require lightweight, high‑precision attitude control systems, making dual‑quaternion based pose control a natural fit and opening sizable revenue streams for technology providers.Strategic partnerships between software vendors and satellite manufacturers are also emerging, enabling joint development of turnkey solutions that embed dual‑quaternion controllers directly into next‑generation bus architectures. This collaborative model accelerates market penetration and creates cross‑selling opportunities across the on‑orbit servicing ecosystem.

Dual quaternion based pose control for spacecraft on-orbit servicing Market Trends

Rapid Adoption Driven by Satellite Constellations

Dual quaternion based pose control for spacecraft on-orbit servicing Market has moved from niche research to mainstream engineering due to the scaling of large satellite constellations. Valued at USD 0.12 billion in 2025, the market is projected to expand to USD 0.45 billion by 2034, reflecting a compound annual growth rate of roughly 15.8 percent. This acceleration is anchored in the technology’s ability to encode rotation and translation in a single eight‑parameter entity, eliminating gimbal lock and cutting computational load relative to traditional Euler or matrix approaches. Operators benefit from smoother six‑degree‑of‑freedom trajectory interpolation, which translates to higher docking precision, more reliable debris capture, and efficient refuelling maneuvers. The convergence of lower launch costs, higher demand for autonomous rendezvous, and increasingly powerful onboard processors has created a fertile environment for dual‑quaternion algorithms on both large service vehicles and compact platforms.

Other Trends

Regulatory Landscape and Investment

Heightened scrutiny of space debris has prompted agencies worldwide to tighten certification requirements for on‑orbit activities. This regulatory pressure, while adding compliance complexity, is also stimulating private‑sector investment in robust guidance solutions. Major players are allocating capital to enhance sensor fusion pipelines that feed dual‑quaternion controllers, thereby ensuring real‑time performance under strict safety standards. The resulting funding surge supports the development of next‑generation autonomous capture systems, which are expected to become a baseline capability for future servicing contracts.

Emerging Partnerships and Technology Integration

Key industry participants,including Lockheed Martin Space Systems, Northrop Grumman Innovation Systems, Airbus Defence & Space, Maxar Technologies, and Thales Alenia Space,are actively embedding dual‑quaternion controllers into their prototype service modules. Notable collaborations such as NASA’s On‑Orbit Servicing Mission‑3 with Maxar (announced early 2024) and ESA’s joint venture with Airbus (later that year) demonstrate a trend toward joint validation of autonomous capture using the dual‑quaternion navigation framework. These partnerships accelerate technology transfer, reduce development risk, and create a shared knowledge base that strengthens the overall market ecosystem. Looking ahead, broader adoption across government and commercial missions is anticipated, driven by proven performance, cost efficiencies, and the strategic imperative to sustain a safe orbital environment.

COMPETITIVE LANDSCAPEKey Industry Players

Dual quaternion based pose control for spacecraft on‑orbit servicing

The market is currently anchored by a handful of large aerospace integrators that possess both the heritage in guidance, navigation and control (GNC) and the deep‑lagging computational resources required for dual‑quaternion implementations. Lockheed Martin Space Systems leads the segment, leveraging its legacy in on‑orbit servicing demonstrators and recent contracts with NASA for autonomous docking missions. Northrop Grumman Innovation Systems follows closely, integrating dual‑quaternion controllers into its robotic arm prototypes for debris removal. Airbus Defence & Space and Maxar Technologies have secured joint ESA funding to showcase end‑to‑end capture scenarios, positioning them as co‑leaders in the European arena. Thales Alenia Space rounds out the core tier, providing turnkey flight‑software packages that embed dual‑quaternion mathematics within its satellite servicing kits. The concentration of R&D budgets among these four firms creates a de‑facto oligopoly, while their strategic partnerships with national space agencies reinforce a high barrier to entry for newcomers.Beyond the primary tier, a diverse set of niche specialists is accelerating innovation through focused applications. Sierra Nevada Corporation contributes proprietary vision‑based sensor fusion that complements dual‑quaternion kinematics for its Dream Chaser payloads. SpaceX, through its Starlink service‑fleet upgrades, is experimenting with lightweight dual‑quaternion nodes to enable autonomous rendezvous. Blue Origin’s orbital refuelling vehicle incorporates a hybrid GNC stack where dual‑quaternion algorithms reduce latency during fuel transfer. Rocket Lab’s Photon platform is piloting low‑cost dual‑quaternion processors for small‑satellite servicing. L3Harris Technologies, Relativity Space, Astroscale, LeoLabs, OneWeb, and Planetary Resources each supply either component‑level hardware, advanced simulation environments, or data‑analytics services that enrich the broader ecosystem, ensuring robust competition and rapid diffusion of the technology across commercial and governmental programs.

List of Key Dual Quaternion based Pose Control for Spacecraft On‑Orbit Servicing Companies Profiled

- Lockheed Martin Space Systems

- Northrop Grumman Innovation Systems

- Airbus Defence & Space

- Maxar Technologies

- Thales Alenia Space

- Sierra Nevada Corporation

- SpaceX

- Blue Origin

- Rocket Lab

- L3Harris Technologies

- Relativity Space

- Astroscale

- LeoLabs

- OneWeb

- Planetary Resources

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Rigid‑body dual‑quaternion controllers are favored because they:

|

| By Application |

|

Autonomous docking and capture stands out as the leading application, driven by:

|

| By End User |

|

Government space agencies drive adoption because they:

|

| By Mission Complexity |

|

Medium‑complexity missions emerge as a growth niche, characterized by:

|

| By Integration Level |

|

Integrated flight‑software suites capture market attention as they:

|

Regional Analysis: North America

North America

Ongoing research and development efforts are continuously refining dual quaternion algorithms and hardware, leading to enhanced precision and efficiency in spacecraft pose control. The integration of artificial intelligence and machine learning further optimizes these systems for autonomous operation and adaptability to varying mission scenarios.

Government agencies like NASA and the Department of Defense are actively supporting the development and deployment of on-orbit servicing technologies, including dual quaternion based pose control. These initiatives provide funding for research, development, and technology demonstrations, fostering market growth and innovation.

The proliferation of large-scale satellite constellations for communication, Earth observation, and navigation necessitates advanced on-orbit servicing capabilities to maintain their operational health and extend their lifespan. Dual quaternion based pose control plays a critical role in enabling these servicing missions.

Increased investment from private space companies is driving the development and commercialization of on-orbit servicing solutions. These companies are actively seeking innovative pose control technologies, including dual quaternions, to offer cost-effective and reliable servicing services.

Europe

Europe represents a significant and steadily growing market for dual quaternion based pose control for spacecraft on-orbit servicing. Driven by a strong tradition in space exploration and a proactive approach to space technologies, the region is witnessing increasing investments in on-orbit servicing capabilities. The European Space Agency (ESA) and national space agencies are actively promoting the development of advanced servicing missions, creating opportunities for dual quaternion technology providers. The focus on sustainability in space is also a key driver, with on-orbit servicing crucial for debris removal and extending the lifespan of existing satellites.

Asia-Pacific

The Asia-Pacific region is emerging as a dynamic and high-growth market for dual quaternion based pose control in the spacecraft on-orbit servicing sector. Rapidly expanding space programs in countries like China, India, and Japan, coupled with growing commercial space activities, are fueling demand for advanced servicing solutions. The region’s increasing investment in satellite constellations and its focus on developing indigenous space capabilities are creating significant opportunities for technology providers. The development of reusable launch vehicles and the expansion of the commercial space sector further contribute to the growth of this market.

South America

South America presents a nascent but promising market for dual quaternion based pose control for spacecraft on-orbit servicing. While currently smaller compared to other regions, the region is witnessing increasing interest in space activities, particularly in areas like satellite communications and Earth observation. Government initiatives and private sector investments are gradually fostering the development of space capabilities, creating potential demand for on-orbit servicing technologies. As space programs mature and the commercial space sector expands, the market for dual quaternion based pose control is expected to grow steadily.

Middle East & Africa

The Middle East and Africa region represents a relatively new and emerging market for dual quaternion based pose control for spacecraft on-orbit servicing. Although space activities in this region are currently in their early stages, there is growing interest in satellite technology for communication, remote sensing, and navigation. Government initiatives aimed at developing national space programs and the increasing involvement of private sector players are expected to drive demand for on-orbit servicing solutions in the coming years. The region’s strategic location and growing economic development present long-term opportunities for the adoption of dual quaternion based pose control technology.

Report Scope

This market research report provides a comprehensive analysis of the Dual quaternion based pose control for spacecraft on-orbit servicing Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Dual quaternion based pose control for spacecraft on-orbit servicing Market?

-> Dual quaternion based pose control for spacecraft on-orbit servicing Market was valued at USD 0.12 billion in 2025 and is expected to reach USD 0.45 billion by 2034, reflecting a CAGR of 15.8% over the forecast period.

Which key companies operate in Dual quaternion based pose control for spacecraft on-orbit servicing Market?

-> Key players include Lockheed Martin Space Systems, Northrop Grumman Innovation Systems, Airbus Defence & Space, Maxar Technologies, and Thales Alenia Space, among others.

What are the key growth drivers?

-> Key growth drivers include the rise of large satellite constellations demanding autonomous rendezvous, high launch costs encouraging on‑orbit servicing, regulatory focus on space‑debris mitigation, and advances in onboard processing power and sensor‑fusion algorithms.

Which region dominates the market?

-> North America leads due to the concentration of major aerospace contractors and government programs, while Europe also shows strong activity.

What are the emerging trends?

-> Emerging trends include integration of AI‑driven guidance, real‑time sensor‑fusion for dual‑quaternion navigation, and collaborative missions between commercial operators and space agencies to demonstrate autonomous capture capabilities.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...