Deep UV (DUV) Nanosecond Laser Market Insights

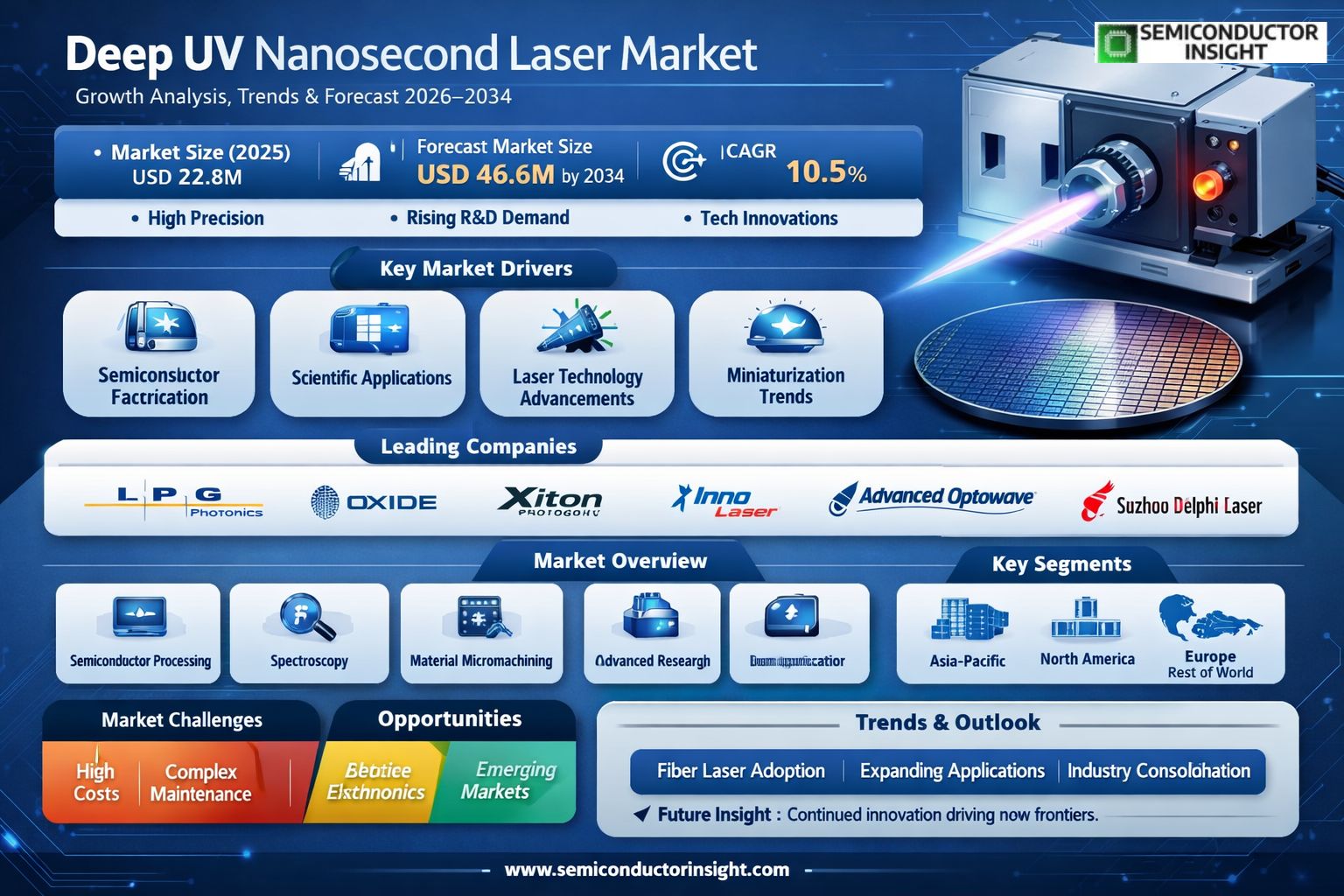

Global Deep UV (DUV) Nanosecond Laser market size was valued at USD 22.8 million in 2025. The market is projected to grow from USD 25.2 million in 2026 to USD 46.6 million by 2034, exhibiting a CAGR of 10.5% during the forecast period.

A Deep UV (DUV) Nanosecond Laser is a type of laser that emits light in the deep ultraviolet spectral range, generally considered to be from 100 to 280 nanometers, with pulse durations in the nanosecond regime (1 nanosecond = 10-9 seconds). This specific combination of short wavelength and pulse duration makes these lasers uniquely suited for high-precision material processing where minimal thermal damage is critical, such as micromachining, semiconductor scribing, and scientific applications like spectroscopy.

The market is experiencing robust growth due to several factors, including the relentless drive for miniaturization and higher precision in the semiconductor industry, which remains the dominant application segment. Furthermore, increasing demand from scientific research institutions for advanced instrumentation and the ongoing development of new materials requiring cold ablation processes are contributing to market expansion. Initiatives by key players are also expected to fuel market growth. For instance, companies are continuously innovating to improve beam quality, power stability, and reliability of DUV ns lasers. Leading manufacturers operating in this specialized market with a wide range of portfolios include IPG Photonics, OXIDE Corporation, Xiton Photonics, Inno Laser Technology, Advanced Optowave Corporation, and Suzhou Delphi Laser.

MARKET DRIVERS

Expansion in High-Precision Microprocessing Applications

The primary growth engine for the Deep UV (DUV) Nanosecond Laser Market is its critical role in advanced manufacturing. These lasers are indispensable for high-precision micromachining, direct-writing, and surface texturing of materials like glass, ceramics, and polymers that are transparent to visible light. The escalating demand for miniaturized components in the semiconductor, medical device, and consumer electronics sectors directly fuels market adoption. The unique ability of DUV nanosecond lasers to deliver clean, cold ablation with minimal heat-affected zones makes them superior for delicate applications where precision is non-negotiable.

Advancements in Semiconductor Fabrication and Inspection

Beyond fabrication, DUV nanosecond lasers are becoming increasingly vital in the semiconductor value chain for inspection and metrology. As node sizes shrink below 10nm, the requirement for defect detection and precise measurement at the nanometer scale intensifies. DUV wavelengths provide higher resolution for optical inspection systems compared to visible or IR lasers. This drives significant investment from semiconductor capital equipment manufacturers, integrating these lasers into next-generation inspection tools to ensure yield and quality, thereby propelling the Deep UV (DUV) Nanosecond Laser Market forward.

➤ The proven reliability and established supply chain for nanosecond-pulse DUV sources lower the adoption barrier for OEMs compared to newer, more complex ultrashort-pulse alternatives.

Furthermore, ongoing technological improvements in laser diode pumping and nonlinear frequency conversion are enhancing the efficiency, stability, and power output of DUV nanosecond lasers. This evolution is reducing the total cost of ownership and operational complexity, opening up new industrial applications and making the technology more accessible to a broader range of manufacturers, which serves as a consistent market driver.

MARKET CHALLENGES

High Initial Investment and Operational Cost Constraints

A significant hurdle for the Deep UV (DUV) Nanosecond Laser Market is the substantial capital expenditure required for laser systems. The complex optics, specialized nonlinear crystals for wavelength conversion, and high-purity gas systems needed for reliable DUV generation contribute to a high unit cost. This pricing tier can deter small and medium-sized enterprises (SMEs) and limit widespread adoption primarily to large-scale industrial or research facilities with ample budgets.

Other Challenges

Technical Complexity and Maintenance

The operational lifetime of DUV optical components, which can degrade under intense UV radiation, necessitates frequent and skilled maintenance. This results in higher ongoing operational costs and potential downtime, posing a logistical challenge for end-users who require continuous, reliable production processes. The need for specialized technical expertise further adds to the total cost of ownership.

Competition from Alternative Technologies

The market faces competitive pressure from both shorter-pulse (femtosecond/picosecond) and longer-pulse (microsecond) laser technologies. While excimer lasers dominate certain high-power DUV applications, ultrafast lasers offer superior precision with even less thermal damage, appealing to high-value R&D and niche manufacturing, challenging the value proposition of DUV nanosecond lasers in some advanced applications.

MARKET RESTRAINTS

Maturation of Key End-Use Industries and Cyclical Demand

The growth trajectory of the Deep UV (DUV) Nanosecond Laser Market is partially tempered by the cyclical nature and maturation stages of its core end-user industries, particularly semiconductors and flat-panel display manufacturing. Capital investment in these sectors follows boom-and-bust cycles tied to global economic conditions and product lifecycles. During periods of reduced capital expenditure (CapEx), orders for new laser processing and inspection tools can slow significantly, creating a direct restraint on market revenue growth for laser manufacturers and system integrators.

Material Processing Limitations and Niche Application Scope

Despite their advantages, DUV nanosecond lasers are not a universal processing solution. Their effectiveness is highly material-dependent, and for many bulk material processing tasks, longer-wavelength infrared or green lasers are more cost-effective and efficient. This inherently limits the total addressable market for DUV nanosecond lasers to specialized, high-value applications. The market’s expansion is therefore restrained by the finite number of applications where its unique combination of wavelength and pulse duration provides a decisive economic and technical advantage.

MARKET OPPORTUNITIES

Emergence of Next-Generation Electronics and Photonics

The development of new electronic forms, such as flexible electronics, photonic integrated circuits (PICs), and micro-LED displays, presents a substantial opportunity. These fields require ultra-fine patterning and processing of novel, often sensitive, materials. The Deep UV (DUV) Nanosecond Laser Market is poised to benefit as these technologies transition from R&D to volume manufacturing, where the lasers’ precision and compatibility with new substrates will be crucial.

Growth in Scientific Research and Biomedical Instrumentation

There is increasing demand in life sciences for instruments utilizing DUV wavelengths for applications like spectroscopy, bioimaging, and cell sorting. DUV nanosecond lasers serve as reliable, stable light sources for these analytical tools. As pharmaceutical and biotechnology research intensifies, and point-of-care diagnostic devices advance, the need for compact, robust DUV laser sources in instrumentation will grow, opening a specialized but high-value segment for the market beyond traditional industrial processing.

Geographic Expansion and Adoption in Emerging Industrial Hubs

While established in technological powerhouses, the Deep UV (DUV) Nanosecond Laser Market has significant room for geographic growth. The rapid industrialization and increasing technological sophistication in regions like Asia-Pacific (excluding traditional leaders) and parts of Eastern Europe present new frontiers. As local manufacturers in these regions move up the value chain into high-precision manufacturing, the demand for advanced laser tools like DUV nanosecond systems is expected to rise, creating fresh sales channels and partnerships for global market players.

Key Trends in the Deep UV (DUV) Nanosecond Laser Market

Semiconductor Industry Driving Precision Applications

The most prominent trend shaping the Deep UV (DUV) Nanosecond Laser market is its critical adoption within the semiconductor industry. For advanced microfabrication, processes such as silicon scribing, wafer dicing, and memory repair demand lasers with high photon energy and short pulse durations. The deep ultraviolet wavelength of these systems, typically between 100 to 280 nanometers, allows for extremely fine feature resolution and minimal thermal damage. As semiconductor nodes continue to shrink, manufacturers are integrating these lasers to enhance yield and component density, making them indispensable in modern electronics production lines globally.

Other Trends

Solid-state and Fiber Laser Technology Competition

The market is witnessing a key technological trend in the competition and development between solid-state lasers and fiber lasers. Both types are central to the DUV nanosecond segment, each offering distinct advantages in stability, power output, and maintenance requirements. Leading global manufacturers are investing in R&D to improve the conversion efficiency and operational lifespan of these systems. This competition is accelerating technological refinements, leading to more cost-effective and reliable laser sources for diverse industrial applications.

Regional Market Expansion and Specialized R&D

Significant expansion is occurring across key geographic regions, including North America, Europe, and particularly Asia, which is a major manufacturing hub. Countries like China, Japan, and South Korea are not only high-volume consumers for semiconductor applications but are also centers for specialized scientific research using DUV nanosecond lasers. The presence of major manufacturers in these regions fosters a robust supply chain and drives localized innovation. Consequently, the industry is experiencing a trend towards more specialized, application-specific solutions to meet the precise demands of sectors from electronics to materials science.

COMPETITIVE LANDSCAPE

Key Industry Players

Consolidated Market with Leading Innovators

Global Deep UV (DUV) Nanosecond Laser market exhibited a consolidated structure in 2025, with the top five manufacturers holding a significant collective revenue share. IPG Photonics stands as a preeminent leader, leveraging its extensive expertise in high-power fiber laser technology to offer robust DUV solutions for demanding industrial applications like semiconductor processing. Alongside established giants, technology-focused companies such as OXIDE Corporation and Xiton Photonics have carved out substantial niches. These players compete intensely on parameters of pulse stability, wavelength precision, and power output, catering to the critical needs of semiconductor lithography and advanced materials research, which are the primary application drivers for this market.

Beyond the market share leaders, a diverse set of specialized manufacturers drives innovation and competition. Inno Laser Technology and Advanced Optowave Corporation represent key challengers, focusing on delivering cost-effective and high-reliability DUV lasers for scientific and industrial research laboratories. Regional players, particularly in Asia, such as Suzhou Delphi Laser, are gaining traction by addressing localized demand with competitive pricing and responsive support. The competitive landscape for DUV Nanosecond Lasers is thus characterized by a core group of dominant, vertically-integrated suppliers surrounded by agile, application-focused companies that collectively service Global demand from the semiconductor, scientific research, and other high-tech sectors.

List of Key Deep UV (DUV) Nanosecond Laser Companies Profiled

- IPG Photonics

- OXIDE Corporation

- Xiton Photonics

- Inno Laser Technology

- Advanced Optowave Corporation

- Suzhou Delphi Laser

- Coherent, Inc.

- CYNERGY (Cymer)

- Trumpf GmbH + Co. KG

- Spectra-Physics (MKS Instruments)

- EKSMA Optics

- Lumentum Holdings Inc.

- Amplitude Laser Group

- EKSPLA

- Huari LongYuan Laser Technology

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Fiber Laser is recognized as the leading segment due to its superior operational efficiency and adaptability. The core value proposition centers on high beam quality and robust performance required for precision micromachining, which is a cornerstone application across major end-use sectors. Furthermore, the technology’s inherent advantages in thermal management and maintenance schedules offer a compelling total cost of ownership, driving its preference among system integrators and manufacturers focused on high-volume, reliable production environments. The segment benefits from continuous innovation in pulse control and energy stability. |

| By Application |

|

Semiconductor Industry is the dominant application segment, underpinned by the technology’s critical role in next-generation chip manufacturing and inspection. The deep ultraviolet wavelength is uniquely suited for advanced lithography techniques and high-precision defect analysis, enabling the production of smaller, more powerful semiconductor devices. The sustained global demand for electronics and the transition to more complex chip architectures create a powerful, long-term growth driver for DUV nanosecond lasers in this space. The segment’s requirements for extreme precision and reliability continually push laser manufacturers towards higher performance benchmarks. |

| By End User |

|

Foundries constitute the leading end-user segment, as they are the primary volume purchasers for advanced manufacturing processes. Their business model, centered on providing cutting-edge fabrication services to fabless semiconductor companies, necessitates continuous investment in the latest equipment, including DUV nanosecond laser systems for lithography, wafer scribing, and inspection. The competitive pressure among global foundries to offer superior process technology and yield acts as a persistent catalyst for laser adoption and upgrades. This segment drives specifications focused on throughput, uptime, and integration with existing semiconductor fabrication tools. |

| By Technology Adoption |

|

Leading-edge/Advanced Nodes segment represents the most strategic and demanding area for DUV nanosecond laser deployment. The development and volume manufacturing of semiconductors at nodes below 10nm rely heavily on the unique capabilities of DUV lasers for multiple patterning and intricate direct-write processes. The complexity of these processes creates a high barrier to entry for laser suppliers but also ensures strong customer loyalty and recurring demand for service and upgrades. Innovation in this segment is focused on achieving narrower pulse widths and higher repetition rates to meet the relentless roadmap of the semiconductor industry. |

| By System Integration Level |

|

Integrated Sub-systems are emerging as the leading value segment, moving beyond the sale of mere laser sources. This trend reflects the market’s demand for pre-engineered solutions that include beam delivery, motion control, and process monitoring, which significantly reduce integration time and risk for OEMs and end-users. Suppliers who provide these optimized sub-systems command stronger customer relationships and can capture more value from the overall equipment sale. The growth of this segment is particularly pronounced in the semiconductor and advanced materials processing fields, where system performance and reliability are paramount. |

Regional Analysis: Global Deep UV (DUV) Nanosecond Laser Market

Asia-Pacific

The region’s dominance is anchored in its semiconductor industry, where DUV nanosecond lasers are critical for precise backside wafer thinning, via drilling, and defect inspection. The concentration of foundries and OSAT providers creates unparalleled, sustained demand for these laser systems, making Asia-Pacific the primary consumption region for this market.

Strategic national policies, such as China’s “Made in China 2025” and South Korea’s K-Semiconductor Strategy, provide substantial funding and clear roadmaps for next-generation manufacturing. These initiatives directly benefit the Deep UV (DUV) Nanosecond Laser Market by creating a favorable environment for adoption and local technology development.

A mature and integrated supply network for photonics and precision optics exists across Japan, China, and Taiwan. This allows for efficient production, customization, and rapid servicing of DUV laser systems, reducing lead times and costs for end-users and strengthening the region’s market position.

Beyond semiconductors, growth is fueled by emerging applications in high-precision display manufacturing for OLEDs and micro-LEDs, scientific research in advanced photonics, and the nascent but promising use in medical device fabrication. This diversification mitigates risk and opens multiple growth avenues for the market.

North America

North America is a major innovation and high-end application center for the Deep UV (DUV) Nanosecond Laser Market, characterized by its strong focus on research, development, and specialized manufacturing. The United States, in particular, hosts leading national laboratories, universities, and corporations that pioneer new applications in defense, aerospace, and advanced instrumentation, driving demand for custom, high-specification DUV laser systems. The market benefits from close collaboration between laser manufacturers and end-users in sectors requiring extreme precision, such as in the production of specialized sensors and communication components. While its volume consumption may trail Asia-Pacific, North America’s influence is pivotal in setting technological benchmarks and developing next-generation processes that later proliferate globally.

Europe

Europe maintains a significant and stable position in the Deep UV (DUV) Nanosecond Laser Market, underpinned by its excellence in high-quality engineering, automotive innovation, and a strong presence in the industrial manufacturing sector. Countries like Germany, France, and the Netherlands are key players, utilizing DUV lasers for precision tasks in automotive electronics, high-end consumer device manufacturing, and sophisticated medical technology production. The market is supported by stringent EU regulations emphasizing manufacturing quality and precision, which align perfectly with the capabilities of DUV nanosecond laser processing. European firms often focus on developing integrated, automated laser workstations that offer high reliability, catering to manufacturers with a strong emphasis on process stability and minimal downtime.

South America

The Deep UV (DUV) Nanosecond Laser Market in South America is in a developing phase, with growth primarily linked to academic research institutions and niche industrial applications. Brazil and Argentina are focal points, where universities and government research centers utilize these lasers for scientific studies in materials science and photonics. On the industrial front, adoption is slowly increasing in sectors like specialized medical device assembly and precision engraving for security and authentication marks. Market expansion is currently constrained by factors such as limited local manufacturing of high-tech components and reliance on imported systems, but interest is growing as regional industries seek to modernize and add value to their production processes.

Middle East & Africa

The market for Deep UV (DUV) nanosecond lasers in the Middle East & Africa region is nascent but shows emerging potential driven by strategic investments in diversification. In the Middle East, particularly in Gulf nations, investments in technology parks and academic cities are creating initial demand for DUV lasers in university research settings focused on nanotechnology and advanced materials. The African market is currently minimal, with sporadic use primarily confined to a few top-tier research universities. Overall, the region’s market dynamics are defined by a developing technological infrastructure, with future growth highly dependent on sustained investment in education, research, and high-value manufacturing sectors as part of broader economic diversification strategies.

Report Scope

This market research report provides a comprehensive analysis of the Deep UV (DUV) Nanosecond Laser Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

-

✅ Market Overview: The report begins with an overview defining a Deep UV (DUV) Nanosecond Laser, outlining the current market scenario, key growth indicators, and industry transformation drivers.

- ✅ Market Size & Forecast: Historical data and future projections for revenue (USD millions) and unit shipments across the forecast period, including 2020-2026 and 2026-2034.

- ✅ Segmentation Analysis: Detailed breakdown by Type (Fiber Laser, Solid-state Laser) and by Application (Semiconductor Industry, Scientific Research, Others), including market size, development potential, and segment percentages.

- ✅ Regional Insights: Quantitative analysis of market size and development potential across North America, Europe, Asia, South America, and the Middle East & Africa, including key country-level markets.

- ✅ Competitive Landscape: Profiles of leading market participants, including their sales, revenue, market share, latest developments, mergers, and acquisitions.

- ✅ Technology Trends & Innovation: Assessment of industry trends, technological drivers, and the evolving applications of DUV nanosecond lasers.

- ✅ Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, obstacles, potential risks, and relevant industry policies.

- ✅ Stakeholder Insights: Insights for manufacturers, suppliers, distributors, OEMs, investors, and policymakers to develop business/growth strategies and make informed decisions.

Primary and secondary research methods are employed, including surveys of manufacturers and industry experts, and data from verified sources to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Deep UV (DUV) Nanosecond Laser Market?

-> Global Deep UV (DUV) Nanosecond Laser market was valued at USD 22.8 million in 2025 and is projected to reach USD 46.6 million by 2034, growing at a CAGR of 10.5% during the forecast period.

Which key companies operate in Deep UV (DUV) Nanosecond Laser Market?

-> Key players include IPG Photonics, OXIDE Corporation, Xiton Photonics, Inno Laser Technology, Advanced Optowave Corporation, and Suzhou Delphi Laser, among others.

What are the key growth drivers?

-> Key growth drivers include advancements in semiconductor fabrication, increasing demand from scientific research applications, and ongoing technological innovations in laser precision and efficiency.

Which region dominates the market?

-> The market features significant activity across major regions. The U.S. and China are key country-level markets, with detailed size estimations and growth potential analyzed for North America, Europe, Asia, and other regions.

What are the emerging trends?

-> Emerging trends include the growing adoption of fiber laser technology, expansion of applications beyond traditional sectors, and industry consolidation through strategic mergers and acquisitions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...