MARKET INSIGHTS

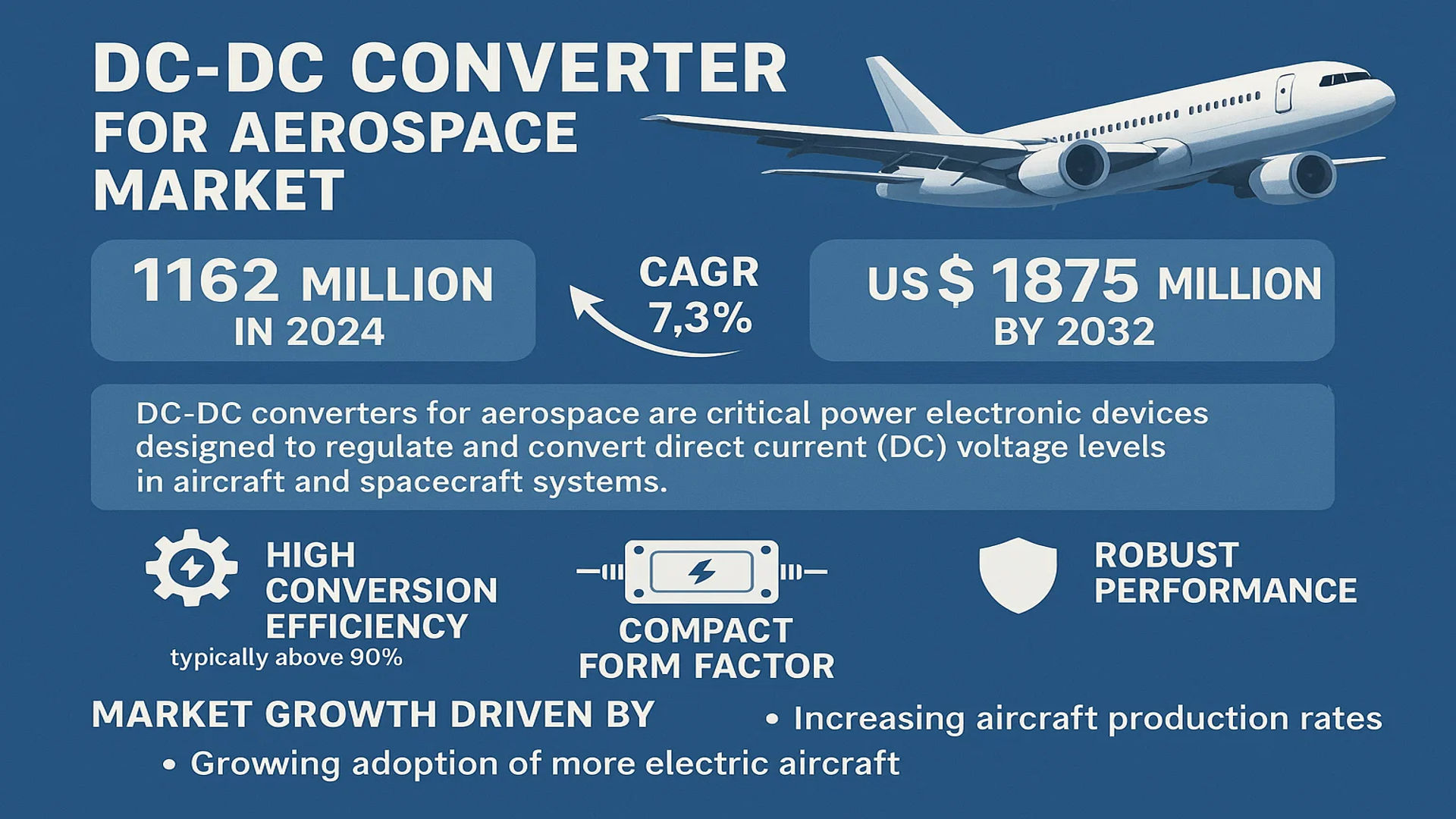

The global DC-DC Converter for Aerospace Market was valued at 1162 million in 2024 and is projected to reach US$ 1875 million by 2032, at a CAGR of 7.3% during the forecast period.

DC-DC converters for aerospace are critical power electronic devices designed to regulate and convert direct current (DC) voltage levels in aircraft and spacecraft systems. These components play a pivotal role in ensuring stable power supply to essential onboard systems including avionics, flight controls, and communication equipment. The converters are engineered to meet stringent aerospace requirements, featuring high power conversion efficiency (typically above 90%), compact form factors, and robust performance under extreme conditions.

The market growth is primarily driven by increasing aircraft production rates, particularly in commercial aviation, and the growing adoption of more electric aircraft (MEA) architectures. Furthermore, technological advancements in power electronics and the rising demand for unmanned aerial vehicles (UAVs) are creating new opportunities. Recent developments include Vicor Corporation’s introduction of high-density power modules specifically for aerospace applications in Q1 2024, demonstrating the industry’s focus on miniaturization and performance optimization. Key players like TDK-Lambda Corporation, Murata Manufacturing, and Texas Instruments continue to dominate the market with innovative product offerings.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Demand for Energy-Efficient Power Solutions in Aerospace to Fuel Market Growth

The global aerospace industry’s shift toward electrified aircraft systems is significantly driving the demand for high-efficiency DC-DC converters. Modern aircraft are incorporating more electric components to replace traditional hydraulic and pneumatic systems, requiring reliable power conversion solutions. This transition leads to weight reduction and improved fuel efficiency—a critical factor when fuel costs account for approximately 25-30% of airline operating expenses. The deployment of DC-DC converters in next-generation aircraft like Boeing 787 and Airbus A350, where over 35% of the power system relies on electrical components, exemplifies this trend.

Rising Adoption of Unmanned Aerial Vehicles (UAVs) Creates Lucrative Opportunities

The UAV market is projected to grow at a compound annual growth rate (CAGR) of over 15% through 2030, driven by military, commercial, and civilian applications. These systems demand compact, lightweight, and high-reliability DC-DC converters to power avionics, communication systems, and payloads. Military drones, in particular, require ruggedized power solutions capable of operating in extreme conditions. For instance, modern surveillance drones integrate multiple DC-DC converters with efficiencies exceeding 95% to optimize mission endurance and data collection capabilities.

Stringent Aerospace Safety Regulations Accelerate Technological Advancements

Regulatory bodies worldwide are mandating higher safety and reliability standards for aerospace power systems. The FAA’s DO-160 and EUROCAE ED-14 standards impose rigorous testing requirements for electromagnetic compatibility (EMC) and environmental resilience. This has pushed manufacturers to develop DC-DC converters with enhanced protection features like fault tolerance and redundancy. Recent innovations include radiation-hardened converters for satellites and modular power architectures that simplify maintenance while meeting aerospace certification requirements.

➤ A study of commercial aircraft power systems indicates that advanced DC-DC converters can reduce wiring weight by up to 20%, directly contributing to fuel savings and emissions reduction.

MARKET CHALLENGES

High Development Costs and Extended Certification Cycles Pose Significant Barriers

The aerospace industry’s stringent qualification processes create substantial challenges for DC-DC converter manufacturers. Developing aviation-grade power converters typically requires 2-3 times more investment compared to industrial equivalents, with certification processes often spanning 12-18 months. These extended timelines delay market entry and strain R&D budgets, particularly for smaller suppliers. The need for specialized materials and testing protocols—such as MIL-STD-810 for environmental stress and MIL-STD-461 for EMI/EMC—further escalates costs.

Other Challenges

Thermal Management Complexities

Aerospace applications demand converters that can operate reliably across extreme temperature ranges (-55°C to +125°C). Managing power density while preventing thermal runaway requires advanced cooling solutions, often involving expensive materials like beryllium oxide or complex fluid cooling systems.

Supply Chain Vulnerabilities

The aerospace sector’s reliance on specialized components makes it susceptible to disruptions. Recent semiconductor shortages have caused lead times for certain converter components to extend beyond 52 weeks, forcing manufacturers to maintain costly inventory buffers.

MARKET RESTRAINTS

Weight and Size Constraints Limit Design Flexibility

Aircraft designers continuously push for lighter and more compact power solutions, creating engineering trade-offs for DC-DC converter manufacturers. While newer wide-bandgap semiconductors like silicon carbide (SiC) and gallium nitride (GaN) offer higher power density, their integration into aerospace-grade converters remains challenging. For example, fitting converters into tight spaces like wingtip avionics bays often requires custom designs that can increase unit costs by 40-60% compared to standardized products.

Limited Adoption of New Technologies in Legacy Aircraft Fleet

Despite advancements in power electronics, the commercial aviation sector maintains aircraft with service lives exceeding 30 years. Retrofitting older planes with modern DC-DC converters presents compatibility issues with legacy systems. Many airlines defer upgrades due to the high retrofit costs—sometimes exceeding $500,000 per aircraft for full electrical system modernization—creating a fragmented market with varying technological requirements.

MARKET OPPORTUNITIES

Emerging Electric and Hybrid-Electric Aircraft Segment Offers Transformative Potential

The burgeoning development of electric vertical take-off and landing (eVTOL) aircraft and regional electric planes is creating new demand for high-power DC-DC converters. Projections indicate the urban air mobility market could surpass $30 billion by 2030, requiring innovative power distribution solutions. Leading aerospace manufacturers are partnering with power electronics firms to develop multi-kilowatt converters capable of handling 800V+ architectures, with several prototype systems already undergoing flight testing.

Advancements in Space Exploration Drive Demand for Radiation-Hardened Converters

With global space agency budgets increasing and private space ventures accelerating, the market for space-grade DC-DC converters is expanding rapidly. Modern satellites require converters that can withstand 100 krad of radiation while maintaining efficiency in vacuum conditions. The small satellite revolution—where over 1,000 cubesats are now launched annually—has particularly boosted demand for miniaturized, radiation-tolerant power solutions with SWaP-C (Size, Weight, Power, and Cost) optimization.

Military Modernization Programs Stimulate Innovation

Global defense spending exceeding $2.2 trillion annually includes significant investments in next-generation avionics and unmanned systems. Military applications demand DC-DC converters with MIL-SPEC ruggedization, often requiring customized solutions for fighter jets, hypersonic vehicles, and electronic warfare systems. Recent conflicts have demonstrated the criticality of reliable power systems, prompting accelerated procurement of advanced converters with cyber-secure and tamper-proof features.

DC-DC CONVERTER FOR AEROSPACE MARKET TRENDS

Increasing Demand for High-Efficiency Power Conversion Solutions Drives Market Growth

The aerospace industry is witnessing a growing need for high-efficiency DC-DC converters to meet the power demands of modern aircraft and spacecraft systems. With avionics, communication, and navigation systems becoming more power-intensive, the global market for aerospace-grade DC-DC converters is projected to grow at a CAGR of 7.3% from 2024 to 2032, reaching $1.87 billion. These converters play a critical role in regulating voltage levels while ensuring minimal energy loss, particularly in applications such as flight control systems and energy storage units. Recent advancements in semiconductor materials, including gallium nitride (GaN) and silicon carbide (SiC), are enabling manufacturers to develop converters with efficiency ratings exceeding 95%, significantly reducing heat dissipation issues in confined aerospace environments.

Other Trends

Miniaturization and Weight Reduction

The push toward lightweight and compact designs is reshaping DC-DC converter development in aerospace applications. Aircraft manufacturers are increasingly adopting modular and high-power-density converters to comply with strict weight limitations while maintaining reliability under extreme conditions. New manufacturing techniques, such as advanced PCB stacking and 3D packaging, are allowing suppliers to reduce converter sizes by up to 30% compared to traditional solutions. This trend is particularly prevalent in unmanned aerial vehicles (UAVs) and urban air mobility (UAM) applications, where space and weight constraints are critical factors in operational efficiency.

Integration of Smart and Fault-Tolerant Technologies

The aerospace sector is increasingly incorporating smart monitoring and fault-tolerant features into DC-DC converters to enhance system reliability. Modern converters now include real-time diagnostics, adaptive voltage regulation, and redundant power pathways to ensure uninterrupted operation even during component failures. These innovations are crucial for critical flight systems, where power disruptions can have severe consequences. Additionally, the rise of more electric aircraft (MEA) architectures is accelerating demand for converters with intelligent load-sharing capabilities and EMI/EMC compliance, ensuring seamless integration with existing power distribution networks while minimizing electromagnetic interference risks.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation and Supply Chain Expansion Drive Market Competition

The global DC-DC Converter for Aerospace Market is characterized by a dynamic competitive environment with multinational corporations, regional leaders, and specialized manufacturers vying for market share. The market witnessed steady revenue growth, reaching $1.16 billion in 2024, with projections indicating strong expansion through 2032. Key players are adopting strategies like product differentiation, strategic collaborations, and investment in R&D to capitalize on emerging opportunities in next-generation aircraft and space applications.

Vicor Corporation and TDK-Lambda Corporation currently dominate the market segment, owing to their extensive aerospace-grade converter portfolios and strong relationships with major aircraft OEMs. These companies have demonstrated particular strength in high-efficiency power conversion solutions that meet stringent aviation standards for weight, reliability, and electromagnetic compatibility.

Meanwhile, Infineon Technologies AG and Texas Instruments Inc. have made significant inroads through their advanced semiconductor-based power solutions, which enable higher power density and superior thermal performance. Their growing presence reflects the industry’s shift toward integrated power module solutions that reduce system complexity for aerospace applications.

Recent market developments show Murata Manufacturing and RECOM Power GmbH aggressively expanding their aerospace offerings through both organic growth and targeted acquisitions. Their success stems from delivering specialized converters for unmanned aerial systems and electric vertical take-off and landing (eVTOL) aircraft, which represent high-growth segments within the industry.

List of Key DC-DC Converter for Aerospace Companies Profiled

- TDK-Lambda Corporation (Japan)

- Murata Manufacturing (Japan)

- Infineon Technologies AG (Germany)

- Eaton (Ireland)

- Advanced Energy (U.S.)

- Vicor Corporation (U.S.)

- PICO Electronics (U.S.)

- Texas Instruments Inc. (U.S.)

- RECOM Power GmbH (Austria)

- Thales (France)

- Bel Fuse Inc. (U.S.)

The landscape continues to evolve as manufacturers respond to several critical industry trends. Increasing electrification of aircraft systems and development of more electric aircraft (MEA) architectures have compelled power conversion specialists to innovate beyond traditional approaches. While established players maintain advantages in certification expertise and legacy platforms, newer entrants are disrupting the market with digital control technologies and wide-bandgap semiconductor applications that promise better performance in harsh aerospace environments.

Segment Analysis:

By Type

Fixed Wing Segment Dominates the Market Due to Increasing Demand for Commercial Aviation and Military Aircraft

The market is segmented based on type into:

- Fixed Wing

- Subtypes: Commercial aircraft, military aircraft, business jets

- Rotary Wing

- Unmanned Aerial Vehicles

- Subtypes: Military drones, commercial drones, and others

- Air Taxis

- Others

By Application

Avionics System Segment Leads Due to Critical Power Requirements for Navigation and Communication Systems

The market is segmented based on application into:

- Avionics System

- Flight Control System

- Surveillance System

- Environmental Control System

- Energy Storage System

- Others

By Technology

Isolated Converters Dominate Due to Their Enhanced Safety Features and Electrical Isolation Capabilities

The market is segmented based on technology into:

- Isolated DC-DC Converters

- Non-Isolated DC-DC Converters

By Input Voltage

Wide Input Voltage Range Converters See Higher Adoption for Aerospace Applications

The market is segmented based on input voltage into:

- Less than 12V

- 12V to 48V

- 48V to 100V

- Above 100V

Regional Analysis: DC-DC Converter for Aerospace Market

North America

North America dominates the DC-DC converter market for aerospace, holding over 35% of the global share in 2024. The region’s leadership stems from robust defense budgets, with the U.S. allocating $842 billion for defense in 2024, including advanced avionics upgrades for military aircraft like the F-35 program. Commercial aerospace demand is equally strong, driven by Boeing’s production ramp-up and next-gen aircraft developments requiring high-efficiency power solutions. Regulatory standards like DO-160 for environmental testing and MIL-STD-704 for aircraft power characteristics compel manufacturers to develop rugged, high-reliability converters. Key players such as Vicor Corporation and Texas Instruments are pioneering GaN (Gallium Nitride)-based solutions to meet these demands while reducing size and weight.

Europe

Europe follows closely, with Airbus’s growing order book and stringent EU aviation safety regulations (CS-25) fueling demand for certified aerospace power solutions. The region emphasizes sustainability, pushing manufacturers like Infineon Technologies and RECOM Power to develop energy-efficient DC-DC converters with >95% efficiency. Collaborative projects such as Clean Sky 2, backed by €4 billion in funding, integrate advanced power electronics to reduce aircraft emissions. However, prolonged certification timelines and Brexit-related supply chain complexities pose challenges for market players.

Asia-Pacific

Asia-Pacific exhibits the fastest growth (CAGR ~9.1%) due to expanding commercial aviation fleets in China and India, alongside indigenous aircraft programs like the COMAC C919. Military modernization in the region, particularly Japan’s F-X fighter program and India’s Tejas MK-2, further propels demand. While cost sensitivity favors localized suppliers, international players partner with firms like Murata Manufacturing to cater to the region’s need for compact, high-power-density converters. Nonetheless, inconsistent regulatory frameworks across countries create fragmentation in adoption rates.

South America

South America’s market remains niche, primarily servicing regional aircraft manufacturers like Embraer and MRO (Maintenance, Repair, Overhaul) operations. Economic volatility limits large-scale adoption, but the growing UAV (Unmanned Aerial Vehicle) sector for agricultural and border surveillance applications offers opportunities. Brazil’s relatively developed aerospace ecosystem anchors demand, though import dependency on converters persists due to limited local manufacturing capabilities.

Middle East & Africa

The Middle East leverages its strategic air transit hub status, with airlines like Emirates driving demand for in-flight entertainment and connectivity systems requiring advanced DC-DC power units. Defense investments in UAVs and partnerships with global aerospace firms stimulate market growth, albeit from a small base. Africa’s nascent aerospace sector shows potential in drone-based logistics, but underdeveloped infrastructure and budgetary constraints hinder large-scale adoption of specialized power electronics.

Report Scope

This market research report provides a comprehensive analysis of the Global DC-DC Converter for Aerospace market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global DC-DC Converter for Aerospace market was valued at USD 1,162 million in 2024 and is projected to reach USD 1,875 million by 2032, growing at a CAGR of 7.3%.

- Segmentation Analysis: Detailed breakdown by product type (Fixed Wing, Rotary Wing, Unmanned Aerial Vehicles, Air Taxis) and application (Avionics System, Flight Control System, Surveillance System, Environmental Control System, Energy Storage System, Others) to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis. North America currently dominates the market due to high aerospace investments.

- Competitive Landscape: Profiles of leading market participants including TDK-Lambda Corporation, Murata Manufacturing, Infineon Technologies AG, Eaton, and Vicor Corporation, covering their product portfolios, R&D investments, and strategic developments.

- Technology Trends & Innovation: Assessment of emerging technologies including wide-bandgap semiconductors, modular designs, and intelligent power management systems transforming the industry.

- Market Drivers & Restraints: Evaluation of growth drivers like increasing aircraft production and challenges including stringent certification requirements and supply chain constraints.

- Stakeholder Analysis: Strategic insights for component suppliers, aerospace OEMs, system integrators, and investors regarding emerging opportunities in next-generation aircraft programs.

Primary and secondary research methods were employed, including interviews with industry experts and analysis of verified market data, to ensure the accuracy and reliability of findings.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global DC-DC Converter for Aerospace Market?

-> DC-DC Converter for Aerospace Market was valued at 1162 million in 2024 and is projected to reach US$ 1875 million by 2032, at a CAGR of 7.3% during the forecast period.

Which key companies operate in Global DC-DC Converter for Aerospace Market?

-> Key players include TDK-Lambda Corporation, Murata Manufacturing, Infineon Technologies AG, Eaton, Vicor Corporation, Texas Instruments Inc, and Thales, among others.

What are the key growth drivers?

-> Key growth drivers include rising aircraft production, modernization of avionics systems, increasing adoption of UAVs, and development of next-generation air taxis.

Which region dominates the market?

-> North America currently holds the largest market share, while Asia-Pacific is expected to witness the highest growth rate during the forecast period.

What are the emerging trends?

-> Emerging trends include adoption of GaN/SiC-based converters, development of modular power systems, and integration of smart monitoring capabilities in aerospace power solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...