MARKET INSIGHTS

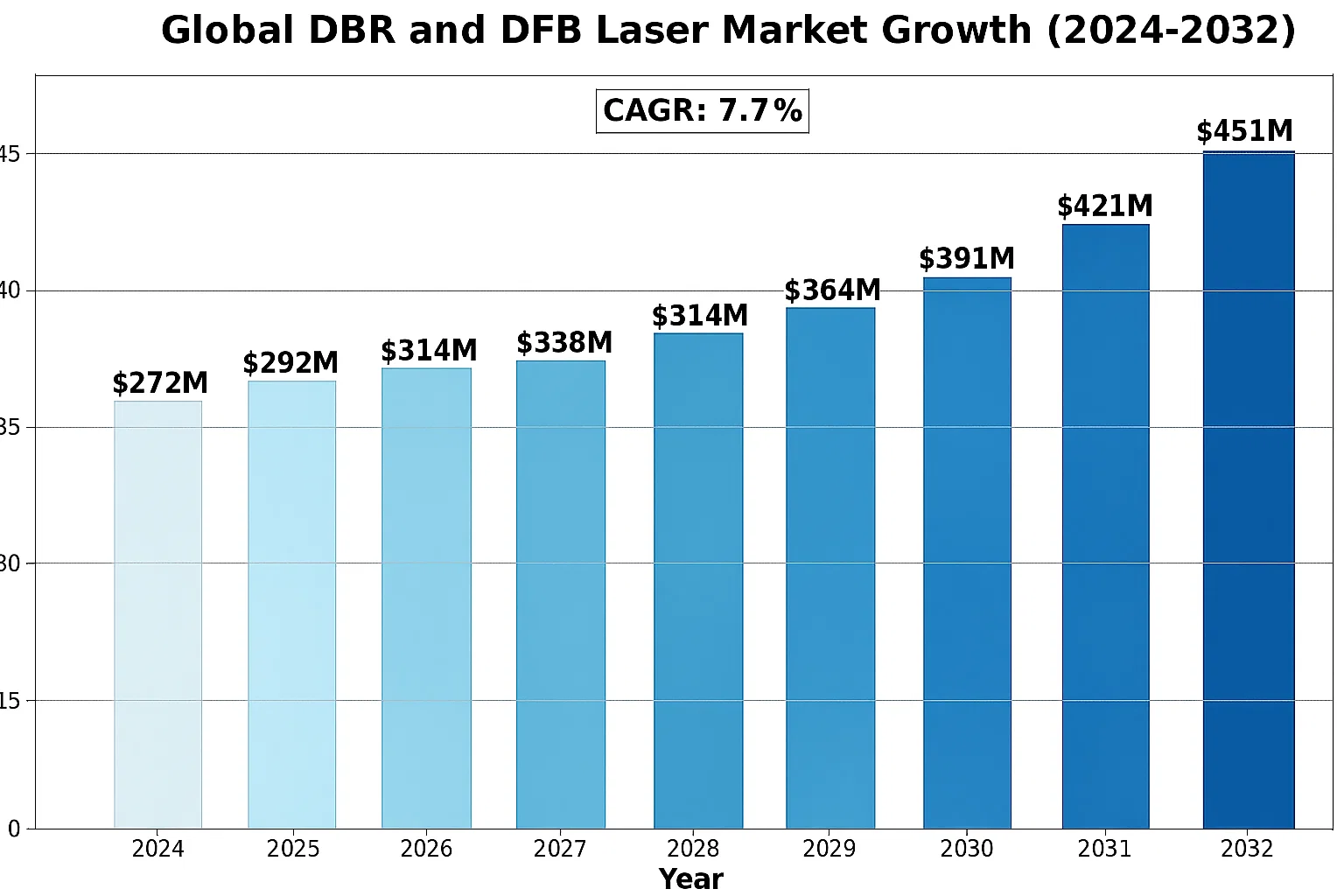

The global DBR and DFB Laser market was valued at 272 million in 2024 and is projected to reach US$ 451 million by 2032, at a CAGR of 7.7% during the forecast period.

Distributed Bragg Reflector (DBR) and Distributed Feedback (DFB) lasers are specialized semiconductor laser technologies used in high-precision applications. DBR lasers utilize a high-reflectivity surface grating for broadband tunability, while DFB lasers employ a buried grating structure to achieve stable single-mode operation with narrow linewidth. These lasers are critical components in optical communications, medical equipment, and sensing systems.

The market growth is driven by increasing demand for high-speed fiber-optic networks, 5G infrastructure deployment, and advancements in photonics technologies. While the communications industry remains the dominant application segment, emerging uses in automotive LIDAR and medical diagnostics are creating new opportunities. Key players like II-VI Incorporated, Lumentum, and Hamamatsu are investing in R&D to develop more efficient and compact laser solutions to meet evolving industry requirements.

MARKET DYNAMICS

MARKET DRIVERS

Explosive Growth in Data Transmission Demand Accelerates DBR & DFB Laser Adoption

The global surge in data consumption, projected to exceed 180 zettabytes by 2025, is fundamentally transforming optical communication networks. Both Distributed Bragg Reflector (DBR) and Distributed Feedback (DFB) lasers have become indispensable components in high-speed fiber-optic systems due to their superior performance characteristics. Recent advances in 5G infrastructure deployment, requiring dense wavelength division multiplexing (DWDM) capabilities, have particularly benefited DFB lasers which dominate 80% of long-haul communication applications. The transition to 400G and 800G networks has further cemented their position as the backbone of modern telecommunication architectures.

Medical Laser Applications Create New Growth Vectors

The medical industry’s shift toward minimally invasive procedures has opened substantial opportunities for both DBR and DFB lasers. DBR lasers, with their tunable wavelength capabilities between 760-790nm, have become critical components in advanced ophthalmic surgical systems. Meanwhile, DFB lasers operating at 1,310nm and 1,550nm wavelengths are gaining traction in precision dermatological treatments and optical coherence tomography (OCT) systems. The medical laser market is expected to maintain a 12.4% CAGR through 2030, with therapeutic applications accounting for nearly 60% of this growth.

➤ The recent FDA clearance of novel DFB laser-based surgical navigation systems has created significant momentum in the medical robotics segment.

Furthermore, automotive LiDAR systems are increasingly incorporating both laser types, with major OEMs investing heavily in autonomous vehicle technologies. This cross-industry demand creates a robust growth ecosystem for manufacturers across the value chain.

MARKET RESTRAINTS

Complex Manufacturing Processes Restrict Market Expansion

The epitaxial growth and grating fabrication processes required for DBR and DFB lasers present substantial technical challenges that limit production scalability. Achieving the necessary sub-nanometer precision in grating periods demands specialized molecular beam epitaxy (MBE) equipment, with a single machine costing upwards of $3 million. Yield rates for high-performance DFB lasers currently average just 65-70% in commercial production environments, creating persistent supply constraints. This manufacturing complexity translates directly to higher unit costs, particularly for medical-grade lasers where quality standards are most stringent.

Thermal Sensitivity Impacts Field Reliability

Both laser types demonstrate notable performance degradation when operating outside optimal temperature ranges, typically 15-35°C for most commercial units. In telecommunications applications where ambient conditions fluctuate significantly, this necessitates expensive thermoelectric cooling systems that can account for 40% of total module costs. Recent field data indicates thermal-related failures represent nearly 28% of all premature laser failures in installed base stations, creating ongoing reliability concerns for network operators. While advances in heterostructure designs have improved temperature stability, fundamental physics limitations continue to constrain performance in harsh environments.

MARKET CHALLENGES

Intellectual Property Barriers Constrain Innovation Pace

The DBR/DFB laser sector remains heavily patent-encumbered, with core technologies protected through complex patent thickets spanning multiple jurisdictions. A recent analysis identified over 2,300 active patents covering essential laser diode structures and fabrication methods, with 75% controlled by just five industry leaders. This concentration creates significant barriers for new entrants and limits collaborative innovation. The average time-to-market for novel laser designs has extended to 7-9 years due to exhaustive freedom-to-operate analyses required during development cycles.

Other Challenges

Material Sourcing Volatility

Gallium arsenide (GaAs) and indium phosphide (InP) wafer supplies remain vulnerable to geopolitical tensions, with price fluctuations exceeding 30% year-over-year in recent periods. These III-V compound semiconductors represent 55-60% of total laser production costs and lack viable substitutes for high-performance applications.

Precision Alignment Requirements

Sub-micron alignment tolerances in laser packaging create persistent bottlenecks in high-volume production. Automated active alignment systems required for consistent performance add $150,000-$200,000 per workstation to manufacturing lines.

MARKET OPPORTUNITIES

Emerging Silicon Photonics Platforms Create Integration Breakthroughs

The maturation of silicon photonics fabrication techniques is enabling unprecedented integration of DBR and DFB lasers with CMOS electronics. Recent demonstrations of hybrid silicon lasers show 40% cost reductions compared to traditional III-V implementations while maintaining comparable performance metrics. This convergence creates significant opportunities in data center interconnects, where co-packaged optics solutions could capture 35% of the market by 2028. Major foundries are now offering dedicated silicon photonics process design kits (PDKs) that simplify laser integration for system designers.

Quantum Technology Applications Open New Frontiers

Ultra-narrow linewidth DFB lasers (below 1 kHz) are becoming essential components in quantum sensing and computing systems. The quantum technology market is projected to grow at 28% CAGR through 2035, with laser subsystems representing 25-30% of total system costs. Recent breakthroughs in frequency-stabilized DBR lasers for atomic clocks and quantum memory applications indicate particularly strong growth potential in defense and scientific research segments. Industry leaders are forming specialized quantum divisions to capitalize on this emerging demand.

➤ Government investments in quantum research programs have exceeded $3 billion globally in 2024 alone, creating substantial funding flows into precision laser development.

DBR AND DFB LASER MARKET TRENDS

Expanding 5G and Data Center Networks Fuel Market Growth

The global DBR and DFB laser market is experiencing robust growth, driven by exponential demand for high-speed data transmission in 5G networks and hyperscale data centers. With the 5G infrastructure rollout accelerating worldwide, DFB lasers—which provide the precision and stability required for wavelength division multiplexing (WDM) systems—are becoming indispensable. Recent reports indicate that over 70% of new optical transceivers deployed in 5G fronthaul networks now incorporate DFB lasers, owing to their single-mode emission and low power consumption. Meanwhile, DBR lasers are gaining traction in tunable laser applications, particularly in reconfigurable optical add-drop multiplexers (ROADMs), where their wavelength agility supports dynamic network optimization. The combined effect of these trends is expected to sustain a compound annual growth rate (CAGR) of 7.7% through 2032, propelling the market to $451 million.

Other Trends

Medical and Sensing Applications Drive Niche Adoption

Beyond telecommunications, medical diagnostics and industrial sensing are emerging as high-growth verticals for DBR and DFB lasers. In healthcare, DFB lasers are increasingly used in optical coherence tomography (OCT) systems for retinal imaging, where their narrow linewidth (<1 MHz) enables micron-level resolution. The global OCT market, valued at $1.3 billion in 2024, is projected to grow at 9% annually, further amplifying demand. Similarly, DBR lasers are proving critical in gas sensing applications, especially for environmental monitoring of methane and CO2. Their ability to target specific absorption lines with <0.1 nm wavelength accuracy makes them ideal for real-time emission tracking in oil and gas facilities. These specialized applications now account for nearly 18% of total laser shipments, up from 12% in 2020.

Technological Innovations in Material Science and Packaging

Advancements in indium phosphide (InP) and silicon photonics are reshaping the DBR/DFB laser landscape. Manufacturers are transitioning from conventional butterfly packages to compact, hermetically sealed TO cans, reducing footprint while improving thermal stability. For instance, recent developments in epitaxial growth techniques have enabled DFB lasers with sidewall gratings, achieving higher yield and consistency. On the DBR front, sampled grating designs now allow >40 nm tuning ranges—a 30% improvement over earlier iterations. These innovations align with the broader industry shift toward co-packaged optics (CPO), where lasers are integrated directly with switches to cut latency and power usage in data centers. Investments in 3D heterogeneous integration suggest further efficiency gains, with prototype modules already demonstrating <1 pJ/bit energy consumption.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation and Strategic Expansion Drive Market Competition

The global DBR (Distributed Bragg Reflector) and DFB (Distributed Feedback) Laser market is characterized by a mix of established industry leaders and emerging players. Key participants are leveraging technological advancements and strategic acquisitions to enhance their market positions. The market is expected to grow significantly, driven by rising demand in the communications and medical sectors, with a projected valuation of $451 million by 2032 at a CAGR of 7.7%.

II-VI Incorporated (now Coherent Corp.) dominates the market, offering a broad portfolio of high-performance lasers. Their strategic merger with Coherent has further strengthened their R&D capabilities, enabling them to cater to diverse applications in telecommunications and automotive LiDAR systems. Similarly, Lumentum Operations has cemented its position through continuous innovation in high-power DFB lasers, widely used in data center interconnects.

Another critical player, Hamamatsu Photonics, focuses on niche applications in medical diagnostics and spectroscopy. Their expertise in low-noise, high-stability DFB lasers has proven essential for precision-driven industries. Meanwhile, Broadcom and Inphenix are aggressively expanding their footprint through collaborations with telecom giants, addressing the surging demand for high-speed fiber-optic networks.

Smaller yet innovative companies like Nanoplus and Innolume specialize in customized laser solutions, particularly for sensing and metrology applications. These firms capitalize on unique value propositions, such as ultra-narrow linewidth DFB lasers, to differentiate themselves in a competitive landscape.

List of Key DBR and DFB Laser Manufacturers Profiled

- II-VI Incorporated (U.S.)

- Inphenix (U.S.)

- Lumentum Operations (U.S.)

- Frankfurt Laser (Germany)

- AdTech Optics (U.S.)

- Nanoplus (Germany)

- Innolume (Germany)

- Modulight (Finland)

- Hamamatsu (Japan)

- Broadcom (U.S.)

- Laser Components (Germany)

- Vescent (U.S.)

Segment Analysis:

By Type

DFB Laser Segment Dominates Due to High Demand in Fiber-Optic Communications

The market is segmented based on type into:

- DBR Laser

- DFB Laser

By Application

Communications Industry Leads Due to Increasing Data Transmission Needs

The market is segmented based on application into:

- Communications Industry

- Automobile Industry

- Medical Industry

- Others

By Wavelength

1310nm and 1550nm Bands Hold Significant Market Share

The market is segmented based on wavelength into:

- 1310nm

- 1550nm

- Other Wavelengths

By End User

Telecom Operators Drive Market Growth Through 5G Deployments

The market is segmented based on end user into:

- Telecom Operators

- Medical Device Manufacturers

- Automotive Suppliers

- Research Institutions

- Others

Regional Analysis: DBR and DFB Laser Market

North America

North America dominates the DBR and DFB laser market, driven by robust demand from the telecommunications and data center industries. The rapid deployment of 5G networks and increasing investments in fiber-optic infrastructure are key growth catalysts, with the U.S. leading regional adoption. Major tech hubs like Silicon Valley and Boston fuel innovation, with companies such as Lumentum and II-VI Incorporated spearheading laser diode R&D. However, high production costs and stringent regulatory standards for optical components pose challenges for smaller manufacturers. North America’s established semiconductor ecosystem ensures steady supply chain stability.

Europe

Europe maintains a strong position in the DBR and DFB laser market, supported by advancements in industrial sensing and automotive LiDAR applications. Germany and the UK are pivotal, with firms like Hamamatsu and Laser Components contributing to technological advancements. The region’s focus on energy-efficient photonics solutions aligns with EU sustainability goals, accelerating DFB laser adoption in green technologies. While regulatory compliance increases operational costs, collaborative R&D initiatives between universities and corporations mitigate innovation barriers. Europe’s aging communication infrastructure also drives demand for high-performance laser upgrades.

Asia-Pacific

Asia-Pacific is the fastest-growing market for DBR and DFB lasers, propelled by China’s aggressive telecom expansions and Japan’s leadership in optoelectronics. Countries like India and South Korea are emerging hotspots due to rising data consumption and government-backed broadband projects. The region benefits from cost-competitive manufacturing, though quality inconsistencies in mid-tier products persist. Local players like Broadcom and Innolume are gaining traction, but intellectual property concerns remain a hurdle. With 60% of global fiber-optic deployments concentrated here, APAC’s demand for precision lasers shows no signs of slowing.

South America

South America exhibits moderate growth in laser adoption, primarily for medical and automotive applications. Brazil accounts for over half of the regional market, with Argentina showing promising niche demand. Limited local manufacturing compels reliance on imports, creating pricing volatility. While economic instability deters large-scale investments, sectors like mining and oil exploration increasingly utilize DBR lasers for remote sensing. The lack of specialized workforce training programs further restricts market expansion, though gradual digital transformation initiatives offer long-term potential.

Middle East & Africa

The MEA region presents untapped opportunities, particularly in UAE and Saudi Arabia’s smart city projects. Israel’s thriving tech sector contributes to specialized DFB laser applications in defense and agriculture. Africa’s market remains nascent due to inadequate infrastructure, though undersea cable projects hint at future demand. High import dependency and limited technical expertise slow adoption rates, but partnerships with global suppliers are bridging knowledge gaps. The region’s focus on renewable energy could spur growth in laser-based monitoring systems over the next decade.

Report Scope

This market research report provides a comprehensive analysis of the global and regional DBR and DFB Laser markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global DBR and DFB Laser market was valued at USD 272 million in 2024 and is projected to reach USD 451 million by 2032, growing at a CAGR of 7.7% during the forecast period.

- Segmentation Analysis: Detailed breakdown by product type (DBR Laser, DFB Laser), application (Communications Industry, Automobile Industry, Medical Industry, Others), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant. Asia-Pacific dominates the market due to rapid industrialization and technological advancements.

- Competitive Landscape: Profiles of leading market participants, including II-VI Incorporated, Lumentum Operations, Hamamatsu, Broadcom, and Thorlabs, among others, covering their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT in laser applications, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth (increasing demand for high-speed communication, medical advancements) along with challenges (high manufacturing costs, supply chain constraints).

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global DBR and DFB Laser Market?

->DBR and DFB Laser market was valued at 272 million in 2024 and is projected to reach US$ 451 million by 2032, at a CAGR of 7.7% during the forecast period.

Which key companies operate in Global DBR and DFB Laser Market?

-> Key players include II-VI Incorporated, Lumentum Operations, Hamamatsu, Broadcom, and Thorlabs, among others.

What are the key growth drivers?

-> Key growth drivers include increasing demand for high-speed optical communication, advancements in medical laser applications, and rising adoption in automotive LiDAR systems.

Which region dominates the market?

-> Asia-Pacific is the dominant market, driven by technological advancements and growing industrialization, while North America leads in innovation and R&D investments.

What are the emerging trends?

-> Emerging trends include integration of AI in laser systems, development of energy-efficient lasers, and increasing applications in quantum computing.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...