MARKET INSIGHTS

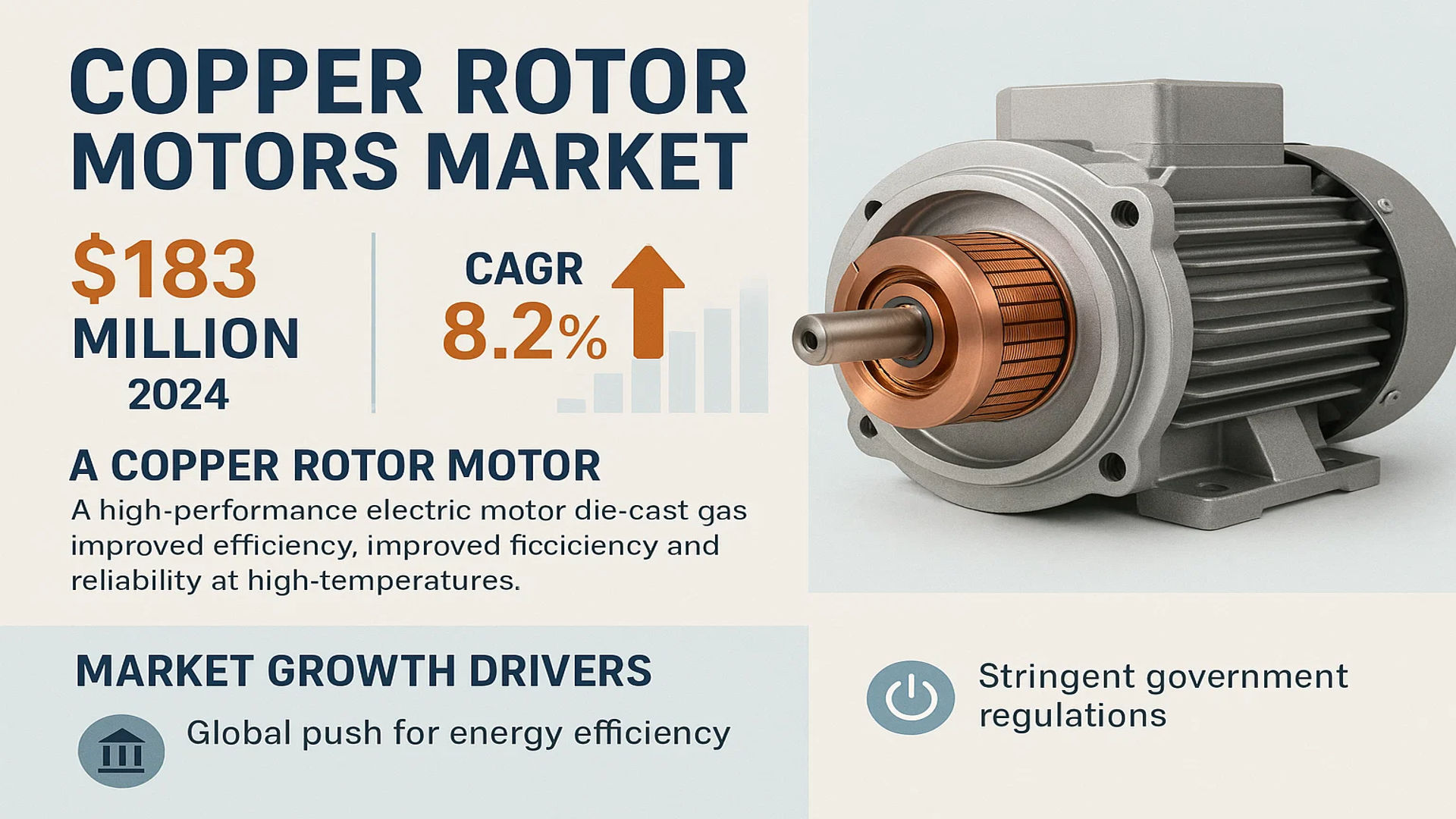

The global Copper Rotor Motors Market was valued at 183 million in 2024 and is projected to reach US$ 316 million by 2032, at a CAGR of 8.2% during the forecast period.

A copper rotor motor is a high-performance electric motor distinguished by its rotor, which is manufactured using a precision die-casting process with copper instead of the traditional aluminum. This fundamental design change leverages copper’s superior electrical conductivity, which is approximately 65% higher than aluminum, leading to significantly lower resistance losses and improved overall motor efficiency. These motors are engineered to operate reliably in high-temperature environments due to copper’s excellent thermal conductivity and high melting point, which enhances performance stability and extends operational lifespan. They are critical components in applications demanding high efficiency and durability, including industrial automation systems, HVAC units, and particularly the burgeoning electric vehicle sector.

The market’s robust growth is primarily fueled by the global push for energy efficiency and stringent government regulations, such as the EU’s Ecodesign Directive, mandating higher efficiency classes for electric motors. The rapid expansion of the electric vehicle industry, which is projected to surpass 30 million units sold annually by 2030, represents a major demand driver, as automakers seek high-efficiency motors to maximize vehicle range. Furthermore, ongoing industrial automation and the adoption of smart manufacturing practices are compelling industries to upgrade to more efficient motor technologies to reduce operational costs. However, the market faces headwinds from the higher raw material cost of copper and the complex, capital-intensive manufacturing process required for die-casting copper, which presents a significant barrier to entry and cost challenge for widespread adoption.

MARKET DYNAMICS

MARKET DRIVERS

Global Energy Efficiency Mandates Accelerating Adoption of High-Efficiency Motors

Stringent global energy efficiency regulations are driving substantial demand for copper rotor motors across industrial and commercial sectors. International Energy Agency data indicates that electric motors account for approximately 45% of global electricity consumption, creating significant pressure for efficiency improvements. Copper rotor motors demonstrate 2-5% higher efficiency compared to conventional aluminum rotor designs, translating to substantial energy savings over operational lifetimes. The European Union’s Ecodesign Directive and similar regulations in North America and Asia are mandating minimum efficiency standards that favor copper rotor technology. These regulatory frameworks are progressively eliminating lower efficiency motor classes from markets, creating a structural shift toward premium efficiency motors that copper rotor technology effectively delivers.

Electric Vehicle Revolution Creating Unprecedented Demand for Advanced Motor Technologies

The global transition to electric vehicles represents a transformative driver for copper rotor motor adoption. Electric vehicle manufacturers require motors that deliver exceptional power density, thermal performance, and efficiency characteristics that align perfectly with copper rotor advantages. The superior thermal conductivity of copper allows for more compact motor designs while maintaining thermal stability under high-load conditions. With electric vehicle production projected to exceed 30 million units annually by 2030, the addressable market for high-performance traction motors has expanded dramatically. Major automotive manufacturers are increasingly specifying copper rotor designs for their premium electric vehicle platforms, recognizing the technology’s ability to extend driving range and improve overall vehicle performance.

Industrial Automation and Smart Manufacturing Driving Precision Motor Requirements

The rapid advancement of Industry 4.0 and smart manufacturing initiatives is creating robust demand for precision motors with enhanced performance characteristics. Copper rotor motors deliver superior speed regulation, reduced vibration, and improved dynamic response compared to conventional designs, making them ideal for automated production systems and robotic applications. The global industrial automation market expansion, valued at approximately $200 billion annually, directly correlates with increased adoption of advanced motor technologies. Manufacturing facilities implementing digital transformation initiatives consistently prioritize energy-efficient and high-performance motor systems to achieve operational excellence targets and reduce total cost of ownership.

MARKET CHALLENGES

Significant Price Premium Over Conventional Motors Limits Market Penetration

The substantial cost differential between copper rotor motors and conventional aluminum rotor designs presents a persistent challenge to wider market adoption. Copper rotor motors typically command a 25-40% price premium due to both material costs and manufacturing complexities. The copper content alone contributes significantly to this premium, with copper prices historically averaging approximately 3.5 times aluminum prices. This cost barrier is particularly impactful in price-sensitive market segments and developing regions where initial investment considerations often outweigh long-term operational savings. While lifecycle cost analyses demonstrate economic advantages, the higher upfront investment remains a decisive factor for many equipment manufacturers and end-users operating under constrained capital budgets.

Other Challenges

Manufacturing Complexity and Technical Barriers

The production process for copper rotors involves sophisticated die-casting techniques requiring specialized equipment and expertise. Copper’s higher melting point (1085°C compared to aluminum’s 660°C) necessitates advanced furnace technology and precise temperature control systems. The manufacturing process demands exceptional quality control measures to prevent defects such as porosity and incomplete filling, which can compromise motor performance. These technical requirements create significant entry barriers for new market participants and limit production scalability for established manufacturers seeking to expand capacity.

Supply Chain Vulnerabilities and Material Availability

Global copper supply constraints and price volatility present ongoing challenges for market stability. Copper mining production faces geographical concentration issues, with a significant portion of global supply originating from politically unstable regions. The increasing demand from renewable energy and electric vehicle sectors creates competitive pressure on copper availability, potentially exacerbating supply chain disruptions and price fluctuations that directly impact motor manufacturing costs and profitability.

MARKET RESTRAINTS

Technical Limitations in High-Speed Applications Restrict Market Expansion

While copper rotor motors excel in numerous applications, they face inherent limitations in ultra-high-speed operational environments. The higher density of copper compared to aluminum creates centrifugal force challenges at extreme rotational speeds, potentially limiting their suitability for certain specialized applications requiring operation above 15,000 RPM. This technical constraint restricts market penetration in segments such as high-speed machining, aerospace systems, and certain precision instrumentation applications where alternative technologies maintain competitive advantages. The development of advanced rotor designs and material composites continues to address these limitations, but current technological boundaries remain a restraining factor for market expansion into high-speed domains.

Established Manufacturing Infrastructure for Aluminum Motors Creates Market Inertia

The extensive global manufacturing infrastructure dedicated to aluminum rotor production creates significant market inertia that restrains rapid transition to copper rotor technology. Manufacturers have invested decades in optimizing aluminum die-casting processes, developing supply chain relationships, and establishing quality control systems tailored to aluminum characteristics. Retooling production facilities for copper rotor manufacturing requires substantial capital investment and technical retraining, creating resistance to technology transition despite demonstrated performance advantages. This infrastructure legacy effect is particularly pronounced in price-sensitive market segments where manufacturing efficiency and established processes outweigh performance considerations.

MARKET OPPORTUNITIES

Renewable Energy Integration Creating New Application Frontiers

The global transition to renewable energy systems presents substantial growth opportunities for copper rotor motor applications. Wind turbine generators, solar tracking systems, and hydroelectric power installations increasingly utilize high-efficiency motors that benefit from copper rotor technology’s superior performance characteristics. The renewable energy sector’s emphasis on reliability, maintenance reduction, and operational efficiency aligns perfectly with copper rotor advantages. As global renewable energy capacity continues expanding at approximately 8-10% annually, the addressable market for specialized motors in this sector provides significant growth potential for manufacturers developing application-specific solutions.

Advanced Manufacturing Technologies Enabling Cost Reduction and Performance Enhancement

Innovations in manufacturing processes and materials science are creating opportunities to overcome traditional cost and performance barriers. Advanced die-casting techniques, including vacuum-assisted casting and controlled atmosphere processing, are improving production yields and reducing manufacturing costs. The development of copper alloys with enhanced mechanical properties enables design optimization for specific applications, potentially expanding market reach into previously inaccessible segments. These technological advancements, combined with increasing production automation, are gradually reducing the cost premium associated with copper rotor motors while simultaneously improving performance characteristics.

Emerging Economies Present Untapped Market Potential

Rapid industrialization in emerging economies represents a significant growth opportunity as these regions modernize their industrial infrastructure and implement energy efficiency standards. Countries across Southeast Asia, Latin America, and Africa are increasingly adopting international efficiency standards and investing in modern manufacturing equipment. This creates a substantial addressable market for high-efficiency motor technologies, particularly as these regions often leapfrog older technologies in favor of modern solutions. The combination of growing industrial capacity and increasing energy cost awareness positions emerging markets as crucial growth frontiers for copper rotor motor adoption over the coming decade.

COPPER ROTOR MOTORS MARKET TRENDS

Industrial Automation and Energy Efficiency Mandates Driving Market Adoption

The global push for industrial automation and stringent energy efficiency regulations is significantly accelerating the adoption of copper rotor motors. These motors offer up to 15% higher efficiency compared to traditional aluminum rotor models, making them particularly valuable in energy-intensive industries. The International Energy Agency reports that electric motor systems account for approximately 45% of global electricity consumption, creating substantial pressure for efficiency improvements. Recent regulatory developments, including the European Union’s Ecodesign Directive and similar standards in North America and Asia, are mandating higher efficiency levels in industrial motors. This regulatory environment, combined with the growing emphasis on reducing operational costs and carbon footprints, positions copper rotor motors as a strategic investment for manufacturing facilities, HVAC systems, and processing plants worldwide.

Other Trends

Electric Vehicle Revolution Creating New Demand Frontiers

The rapid expansion of the electric vehicle market represents a transformative trend for copper rotor motor manufacturers. Electric vehicles require highly efficient traction motors that provide excellent power density and thermal performance, characteristics where copper rotor technology excels. The superior conductivity of copper enables higher starting torque and better overload capacity compared to aluminum alternatives, directly translating to improved vehicle range and performance. With global electric vehicle sales projected to reach 26 million units annually by 2030, motor manufacturers are investing heavily in copper rotor production capacity. This automotive segment demand is particularly strong in China, Europe, and North America, where government incentives and consumer adoption are driving the fastest market growth.

Technological Advancements in Manufacturing Processes

While copper’s higher melting point and material costs present manufacturing challenges, significant advancements in die-casting technology and production automation are addressing these barriers. New vacuum die-casting techniques and improved mold designs have increased production yields while reducing material waste. The development of copper alloys with enhanced casting properties has further improved manufacturing efficiency, lowering the overall cost premium compared to aluminum rotors. Additionally, the integration of Industry 4.0 technologies, including real-time monitoring and predictive maintenance systems, is optimizing production lines and reducing downtime. These technological improvements are gradually narrowing the price differential while maintaining the performance advantages that make copper rotor motors particularly attractive for premium applications where energy savings justify higher initial investments.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Leverage Technological Innovation and Strategic Expansion to Capture Market Share

The global copper rotor motors market exhibits a semi-consolidated structure, characterized by the presence of established multinational industrial giants alongside specialized regional manufacturers and emerging technology-focused firms. This dynamic creates a competitive environment where scale, innovation, and geographic reach are critical determinants of success. While the high initial costs and complex manufacturing processes present significant barriers to entry, they also solidify the position of incumbents with advanced technical capabilities and robust supply chains.

ABB Ltd. (Switzerland) stands as a dominant force in this market, leveraging its extensive global distribution network and a comprehensive portfolio of high-efficiency motors tailored for industrial automation and heavy-duty applications. Their commitment to research and development has been pivotal in advancing copper die-casting techniques, enhancing motor reliability and performance. Similarly, Siemens AG (Germany) commands a substantial market share, driven by its stronghold in the European industrial sector and its integrated solutions that pair copper rotor motors with advanced drive systems and digitalization services for smart manufacturing.

Meanwhile, Toshiba Corporation (Japan) and Wolong Electric Group (China) have solidified their positions as key players, particularly in the Asia-Pacific region. Their growth is heavily attributed to the booming electric vehicle market and massive infrastructure development projects, which demand highly efficient motor systems. These companies compete aggressively on both technological innovation and cost-optimization strategies to cater to a diverse customer base.

Furthermore, companies like Regal Rexnord Corporation (U.S.) are strengthening their market presence through strategic acquisitions and significant investments in expanding their manufacturing capacities for energy-efficient motor products. This trend of consolidation and capacity expansion is expected to intensify as the market grows, with players aiming to offer more competitive pricing and shorter delivery times to gain a larger portion of the projected US$ 316 million market by 2032.

List of Key Copper Rotor Motors Companies Profiled

- ABB Ltd. (Switzerland)

- Toshiba Corporation (Japan)

- Siemens AG (Germany)

- Kitra Industries (Global)

- Regal Rexnord Corporation (U.S.)

- Wolong Electric Group Co., Ltd. (China)

- Shanghai Motor System Energy-saving Engineering Technology Co., Ltd. (China)

- Jiang Chao Motor Technology Co., Ltd. (China)

- Yunnan Copper Science Technology Development Co., Ltd. (China)

- Shanghai Qilong Stamping Co., Ltd. (China)

Segment Analysis:

By Type

Three-phase Asynchronous Motor Segment Dominates the Market Due to Superior Efficiency and Industrial Adoption

The market is segmented based on type into:

- Single-phase Asynchronous Motor

- Three-phase Asynchronous Motor

- Others

By Application

New Energy Vehicles Segment Leads Due to Stringent Efficiency Requirements and Global Electrification Push

The market is segmented based on application into:

- Chemical Industry

- Power Industry

- Petroleum and Petrochemical

- New Energy Vehicles

- Others

By Power Rating

Medium Power Motors (10kW – 200kW) Hold Significant Share Owing to Broad Industrial Utilization

The market is segmented based on power rating into:

- Low Power (<10kW)

- Medium Power (10kW – 200kW)

- High Power (>200kW)

By End-User Industry

Industrial Manufacturing Represents a Core End-User Segment Driven by Automation and Efficiency Mandates

The market is segmented based on end-user industry into:

- Industrial Manufacturing

- Automotive and Transportation

- Oil & Gas

- Energy and Utilities

- Others

Regional Analysis: Copper Rotor Motors Market

Asia-Pacific

The Asia-Pacific region is the dominant force in the global copper rotor motors market, accounting for the largest share of both production and consumption. This leadership is driven by massive industrial expansion, rapid urbanization, and significant government investments in infrastructure and manufacturing automation. China, as the world’s manufacturing hub, is the primary engine of growth, with its extensive use of these motors in industrial machinery, HVAC systems, and a burgeoning electric vehicle sector. The country’s push for energy efficiency, supported by national standards, is a key market driver. India is another major contributor, with its ‘Make in India’ initiative fostering domestic manufacturing and increasing demand for high-efficiency motors in various industries. While cost sensitivity remains a factor, the long-term operational savings offered by copper rotor motors are increasingly recognized, leading to a steady shift away from less efficient alternatives. Japan and South Korea contribute through their advanced technological manufacturing bases, particularly in robotics and precision equipment, where the superior performance of copper rotor motors is essential.

Europe

Europe represents a mature and technologically advanced market for copper rotor motors, characterized by stringent energy efficiency regulations and a strong focus on sustainability. EU directives, such as the Ecodesign Directive (2009/125/EC) and its specific regulations for electric motors (EU 2019/1781), mandate minimum efficiency levels that heavily favor the adoption of premium efficiency technologies like copper rotor designs. This regulatory environment is the single most important market driver. The region’s well-established industrial sector, particularly in Germany, Italy, and France, is actively retrofitting and upgrading machinery to comply with these standards and reduce operational carbon footprints. Furthermore, the European automotive industry’s aggressive transition to electric mobility provides a significant and growing application segment for these high-performance motors. Innovation in motor design and integration with smart industrial systems (Industry 4.0) is also a key trend, with manufacturers focusing on developing connected, ultra-efficient motor solutions for the European market.

North America

The North American market is driven by a combination of regulatory standards, industrial modernization, and a focus on operational cost reduction. In the United States, energy efficiency standards set by the Department of Energy (DOE) have progressively raised the bar, making high-efficiency motors like those with copper rotors increasingly necessary for compliance. The strong presence of major oil and gas, chemical processing, and manufacturing industries creates substantial demand for reliable and efficient motor drives. Investments in infrastructure and a resurgence in domestic manufacturing activity further support market growth. Canada’s market follows a similar trajectory, with a focus on resource industries and alignment with energy efficiency goals. While the initial cost premium can be a consideration, the total cost of ownership calculation, which emphasizes energy savings over the motor’s lifespan, is a primary factor convincing commercial and industrial users to adopt this technology.

South America

The South American market for copper rotor motors is emerging and presents a landscape of significant potential tempered by economic challenges. Countries like Brazil and Argentina have sizable industrial and agricultural sectors where the application of efficient motor systems could yield considerable energy savings. Mining operations, a key economic activity in several countries, are another potential growth area. However, widespread adoption is hindered by economic volatility, which impacts capital investment capabilities, and less stringent enforcement of energy efficiency regulations compared to North America or Europe. The market is consequently more price-sensitive, often favoring lower-cost initial options despite higher long-term operating expenses. Nonetheless, as awareness of energy costs and environmental impacts grows, along with gradual infrastructure development, a slow but steady increase in demand for more efficient motor technologies is anticipated over the long term.

Middle East & Africa

The Middle East & Africa region is in the nascent stages of adoption for copper rotor motors. Market development is primarily concentrated in the more economically diversified nations of the Middle East, such as Saudi Arabia and the UAE, where Vision 2030 initiatives and other economic diversification plans are driving investment in new industrial and infrastructure projects. These projects increasingly specify higher efficiency equipment. The region’s extensive oil and gas industry also represents a potential application, though traditional practices and cost considerations have slowed the transition. In Africa, the market is even more limited, with growth constrained by infrastructural challenges, limited industrial capacity, and funding availability for capital equipment. However, the fundamental need for energy efficiency and the long-term economic benefits of such motors suggest that this region holds future growth potential as its economies continue to develop.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Copper Rotor Motors markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Copper Rotor Motors Market?

-> Copper Rotor Motors Market was valued at 183 million in 2024 and is projected to reach US$ 316 million by 2032, at a CAGR of 8.2% during the forecast period.

Which key companies operate in Global Copper Rotor Motors Market?

-> Key players include ABB, Toshiba, Siemens, Regal Rexnord, Wolong Electric Group, Kitra Industries, Shanghai Motor System Energy-saving Engineering Technology, Jiang Chao Motor Technology, Yunnan Copper Science Technology Development, and Shanghai Qilong Stamping, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for industrial automation, expansion of electric vehicle production, stringent energy efficiency regulations, and the superior performance characteristics of copper rotor motors including higher conductivity and thermal stability.

Which region dominates the market?

-> Asia-Pacific is the dominant market, accounting for over 45% of global market share in 2024, driven by manufacturing activities in China, Japan, and South Korea, while Europe shows strong growth due to energy efficiency directives.

What are the emerging trends?

-> Emerging trends include advancements in precision casting technologies, integration of IoT for motor monitoring, development of lightweight composite materials, and increasing adoption in renewable energy applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...