Chip-on-wafer-on-substrate (CoWoS) with silicon bridge Market Insights

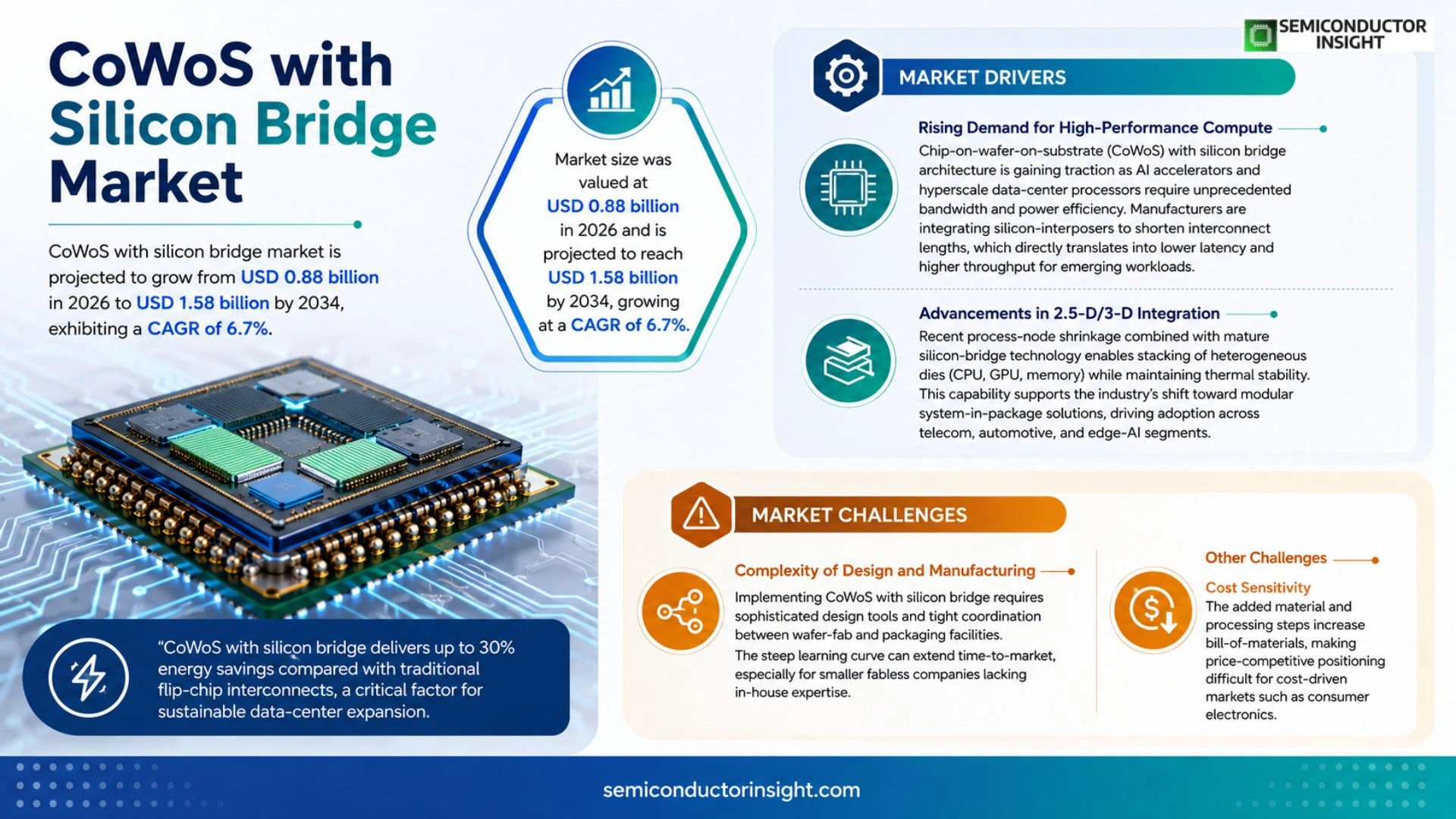

Global CoWoS with silicon bridge market size was valued at USD 0.82 billion in 2025. The market is projected to grow from USD 0.88 billion in 2026 to USD 1.58 billion by 2034, exhibiting a CAGR of 6.7% during the forecast period.

Chip‑on‑wafer‑on‑substrate (CoWoS) with silicon bridge integrates multiple high‑performance dies on a single silicon interposer that acts as a bridge, enabling ultra‑high bandwidth memory (HBM), AI accelerators, and networking chips to communicate through dense micro‑bumps and TSVs (through‑silicon vias). This architecture reduces signal latency, improves power efficiency, and supports heterogeneous integration of logic, memory, and RF components.

The market is accelerating because leading foundries such as TSMC and Intel are expanding their advanced packaging roadmaps, while demand for AI inference engines and data‑center accelerators drives adoption of high‑density interconnect solutions.

MARKET DRIVERS

Rising Demand for High‑Performance Compute

Chip‑on‑wafer‑on‑substrate (CoWoS) with silicon bridge architecture is gaining traction as AI accelerators and hyperscale data‑center processors require unprecedented bandwidth and power efficiency. Manufacturers are integrating silicon‑interposers to shorten interconnect lengths, which directly translates into lower latency and higher throughput for emerging workloads.

Advancements in 2.5‑D/3‑D Integration

Recent process‑node shrinkage combined with mature silicon‑bridge technology enables stacking of heterogeneous dies (CPU, GPU, memory) while maintaining thermal stability. This capability supports the industry’s shift toward modular system‑in‑package solutions, driving adoption across telecom, automotive, and edge‑AI segments.

➤ “CoWoS with silicon bridge delivers up to 30% energy savings compared with traditional flip‑chip interconnects, a critical factor for sustainable data‑center expansion.”

Investment from leading foundries in dedicated CoWoS production lines further reinforces supply confidence, encouraging OEMs to design next‑generation products around this technology.

MARKET CHALLENGES

Complexity of Design and Manufacturing

Implementing CoWoS with silicon bridge requires sophisticated design tools and tight coordination between wafer‑fab and packaging facilities. The steep learning curve can extend time‑to‑market, especially for smaller fabless companies lacking in‑house expertise.

Other Challenges

Cost Sensitivity

The added material and processing steps increase bill‑of‑materials, making price‑competitive positioning difficult for cost‑driven markets such as consumer electronics.

MARKET RESTRAINTS

Supply Chain Constraints

Limited availability of high‑purity silicon interposer wafers and the need for precise alignment equipment create bottlenecks that can restrict scaling of CoWoS with silicon bridge volumes, particularly during periods of geopolitical tension.

Furthermore, the reliance on a small pool of qualified packaging partners amplifies the risk of capacity shortages, slowing adoption in regions outside the primary semiconductor hubs.

MARKET OPPORTUNITIES

Emerging Edge‑AI Applications

Edge devices that require on‑device inference,such as autonomous drones, smart cameras, and industrial robots,benefit from the compact form factor and high bandwidth of CoWoS with silicon bridge. This opens a lucrative niche where traditional server‑grade solutions are impractical.

Collaborative ecosystems between foundries, OSATs, and EDA vendors are beginning to standardize design kits for silicon‑bridge integration, lowering entry barriers and creating a pipeline of innovative products that can capture market share over the next five years.

Chip-on-wafer-on-substrate (CoWoS) with silicon bridge Market Trends

Rising Adoption of AI Accelerators and Data‑Center Compute

Chip-on-wafer-on-substrate (CoWoS) with silicon bridge Market is experiencing a pronounced shift toward high‑performance artificial‑intelligence workloads. By embedding multiple dies on a dense silicon interposer, the architecture delivers ultra‑high bandwidth memory and AI inference engines with markedly lower latency. Data‑center operators are prioritizing these solutions to meet the surge in demand for real‑time processing while containing power budgets. As AI models expand, the ability to combine logic, memory, and RF functions on a single substrate becomes a decisive competitive advantage, driving a steady uptick in design wins across hyperscale clouds.

Other Trends

Advancements in Silicon Interposer Technology

Recent progress in micro‑bump density and through‑silicon‑via (TSV) reliability has elevated the performance envelope of Chip-on-wafer-on-substrate (CoWoS) with silicon bridge Market. Manufacturers are leveraging finer pitch interposers to support higher I/O counts without compromising signal integrity. Improved thermal pathways and copper‑based interconnect stacks are also extending the operational envelope for power‑intensive AI chips. These technical refinements enable tighter integration of heterogeneous components, which in turn reduces board‑level complexity and shortens time‑to‑market for next‑generation processors.

Strategic Partnerships Expanding Capacity

Collaborative agreements between leading foundries and packaging specialists are a cornerstone of Chip-on-wafer-on-substrate (CoWoS) with silicon bridge Market’s momentum. Joint ventures focusing on next‑generation silicon bridges are increasing wafer‑level throughput while driving down per‑unit costs. Such partnerships also facilitate shared R&D pipelines, accelerating the rollout of newer interposer materials and design‑for‑manufacturing guidelines. Enterprises that adopt these co‑engineered solutions benefit from a more predictable supply chain and a clearer upgrade path as compute density requirements continue to rise.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive Overview of CoWoS with Silicon Bridge Market

CoWoS with silicon bridge segment is anchored by a few dominant foundries that dictate roadmap cadence and capacity. Taiwan Semiconductor Manufacturing Company (TSMC) commands the largest share, leveraging its 5‑nm and 3‑nm advanced nodes to offer high‑density interposers that integrate HBM and AI accelerators. Intel follows closely, promoting “EMIB‑plus” and its own silicon‑bridge solutions as part of the Intel‑Xeon platform, which targets data‑center inference workloads. Samsung Electronics, through its partnership with ASE Technology Holding, is accelerating volume production of silicon‑bridge interposers, positioning itself as a secondary hub for memory‑centric designs. These leaders benefit from deep R&D budgets, extensive IP libraries, and strategic OEM relationships that lock in multi‑year contracts, creating a tiered market structure where smaller players must align with one of the top three for access to state‑of‑the‑art packaging infrastructure.

Beyond the core trio, a cadre of niche specialists is enriching the ecosystem. ASE Technology Holding remains a critical outsourced‑assembly partner, providing advanced substrate services and co‑development support for emerging AI chip makers. Amkor Technology offers cost‑effective fan‑out and wafer‑level packaging that complements silicon‑bridge adoption in mid‑range products. GLOBALFOUNDRIES supplies specialized silicon‑interposer options for custom ASICs, while Micron Technology and SK Hynix contribute memory‑centric IP that drives demand for HBM‑enabled CoWoS stacks. Companies such as Qualcomm, Broadcom, NXP Semiconductors, and IBM are integrating silicon‑bridge modules into their high‑performance processors, expanding the addressable market and fostering a collaborative supply chain that balances scale with specialization.

List of Key CoWoS with Silicon Bridge Companies Profiled

- Taiwan Semiconductor Manufacturing Company (TSMC)

- Intel Corporation

- Samsung Electronics

- ASE Technology Holding

- Amkor Technology

- GLOBALFOUNDRIES

- Micron Technology

- SK Hynix

- Qualcomm

- Broadcom

- NXP Semiconductors

- IBM

- Renesas Electronics

- Texas Instruments

- Marvell Technology Group

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Silicon‑bridge enabled CoWoS is emerging as the preferred architecture because it directly addresses latency and power‑efficiency concerns in high‑performance compute.

|

| By Application |

|

AI inference engines dominate the application landscape as designers seek to squeeze maximum throughput from limited power envelopes.

|

| By End User |

|

Cloud service providers are the most influential end‑user segment, driving demand for dense, energy‑efficient compute nodes.

|

| By Integration Strategy |

|

Hybrid silicon‑bridge approach is gaining traction because it balances the design flexibility of heterogeneous stacking with the manufacturability of monolithic interposers.

|

| By Value Chain Collaboration |

|

Foundry‑OSAT alliances are the leading collaborative model, fostering rapid adoption of silicon‑bridge technology.

|

Regional Analysis: Asia-Pacific

Taiwan remains a pivotal hub for CoWoS with silicon bridge, boasting world-class foundries and a mature ecosystem. The region’s focus on leading-edge process technologies drives innovation in advanced packaging.

South Korea’s strong presence in memory and logic chip manufacturing contributes significantly to the demand for sophisticated packaging solutions like CoWoS with silicon bridge. The country’s investments in next-generation semiconductor technologies are boosting market growth.

China’s rapidly expanding semiconductor industry presents a substantial opportunity for CoWoS with silicon bridge. Government support and increasing domestic demand for advanced electronics are key catalysts for market penetration.

Japan’s expertise in precision manufacturing and advanced materials positions it as a key player in CoWoS with silicon bridge market, particularly for high-reliability applications.

North America

North America, particularly the United States, is witnessing increasing adoption of CoWoS with silicon bridge driven by the growing demand for AI accelerators and high-performance GPUs. While historically a strong player in chip design and some manufacturing, the region is actively investing in domestic fabrication capabilities to bolster its supply chain resilience. The focus is on specialized packaging solutions for demanding applications.

Europe

Europe’s semiconductor industry is undergoing a period of significant transformation, with substantial investments being made to enhance manufacturing capacity and promote innovation in advanced packaging technologies like CoWoS with silicon bridge. Government initiatives aimed at fostering a strong European semiconductor ecosystem are playing a crucial role. The region’s strengths lie in design and specialized component manufacturing, creating demand for advanced interconnection solutions.

South America

South America represents a nascent market for CoWoS with silicon bridge, with growth primarily driven by increasing adoption of electronic devices and the expansion of telecom infrastructure. However, the market is relatively small compared to other regions, and significant investments are needed to develop a robust ecosystem.

Middle East & Africa

The Middle East & Africa region presents a long-term growth opportunity for CoWoS with silicon bridge, fueled by increasing investments in infrastructure development and the expansion of digital services. The region’s growth is tied to broader economic development and the adoption of advanced technologies across various sectors.

Report Scope

This market research report provides a comprehensive analysis of the Chip-on-wafer-on-substrate (CoWoS) with silicon bridge Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Chip-on-wafer-on-substrate (CoWoS) with silicon bridge Market?

-> Chip-on-wafer-on-substrate (CoWoS) with silicon bridge Market was valued at USD 0.82 billion in 2025 and is expected to reach USD 1.58 billion by 2034 with a CAGR of 6.7%.

Which key companies operate in Chip-on-wafer-on-substrate (CoWoS) with silicon bridge Market?

-> Key players include TSMC, Intel, Samsung, and ASE Technology Holding, among others actively developing advanced silicon bridge solutions.

What are the key growth drivers?

-> Key growth drivers include rising demand for AI inference engines, data‑center accelerators, and the need for ultra‑high bandwidth memory (HBM) integration, which drive adoption of high‑density interconnect packaging.

Which region dominates the market?

-> Asia‑Pacific dominates the market, propelled by major foundries such as TSMC in Taiwan and Intel’s expanding advanced packaging facilities.

What are the emerging trends?

-> Emerging trends include next‑generation silicon interposer technologies, tighter integration of heterogeneous components (logic, memory, RF), and strategic partnerships that lower cost per wafer while enhancing compute density.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...