MARKET INSIGHTS

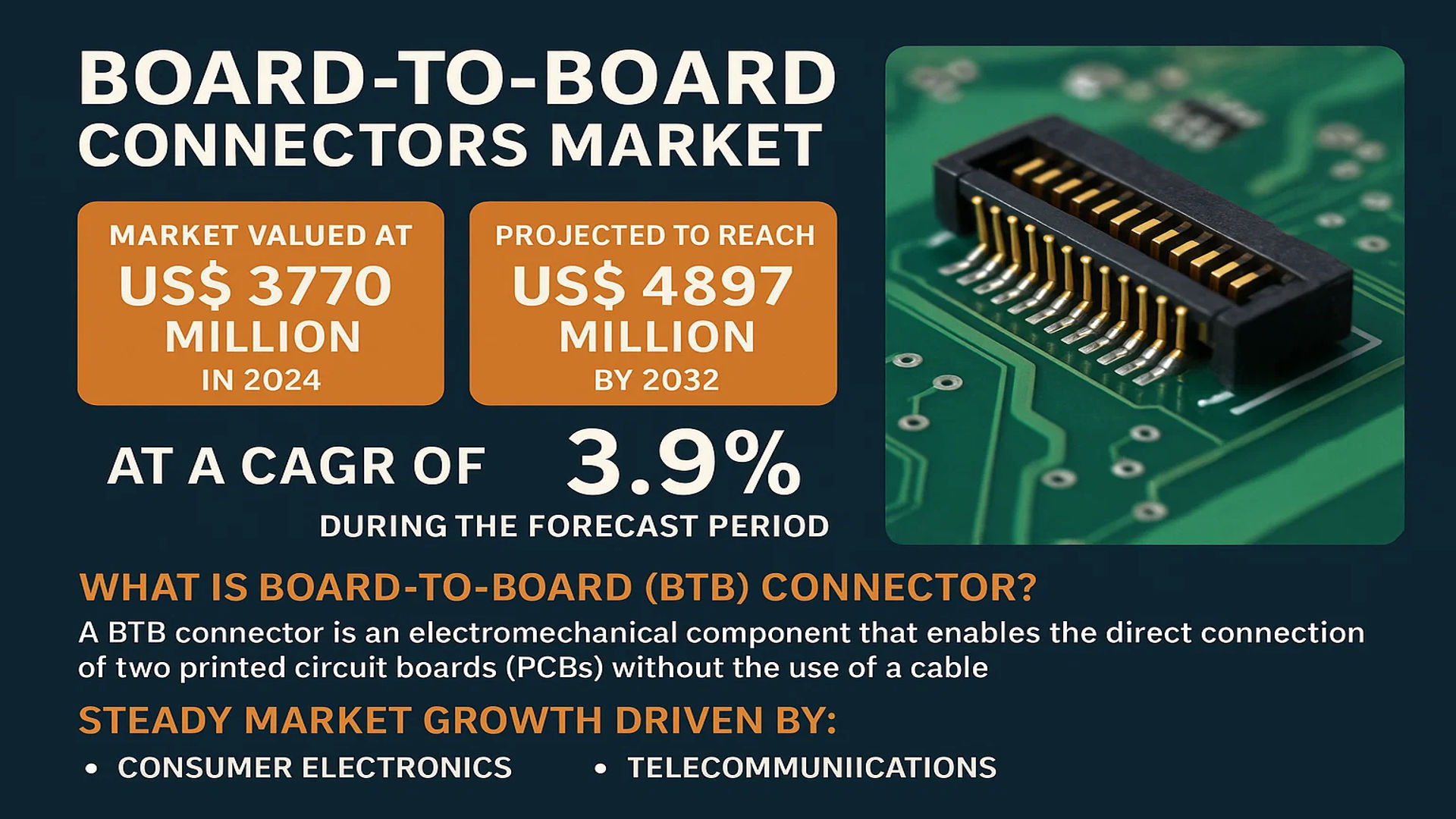

The global Board-to-Board Connectors Market was valued at 3770 million in 2024 and is projected to reach US$ 4897 million by 2032, at a CAGR of 3.9% during the forecast period.

Board-to-board (BTB) connectors are fundamental electromechanical components used to connect printed circuit boards (PCBs) without the need for a cable. These connectors consist of a housing, typically made from insulating plastic, and a specific number of terminals. The terminals, manufactured from conductive materials like copper alloy and often plated with gold or tin to enhance conductivity and prevent corrosion, are responsible for transmitting electrical current and signals between the connected PCBs. Their design ensures a reliable and repeatable connection, which is critical for the miniaturization and high-density packaging trends in modern electronics.

This steady market growth is primarily driven by the relentless expansion of the consumer electronics and telecommunications sectors, which demand increasingly compact and high-performance interconnection solutions. The proliferation of 5G infrastructure, Internet of Things (IoT) devices, and advanced automotive electronics are key contributors. However, the market faces pricing pressures and challenges related to the complexity of designing connectors for ever-smaller form factors. The competitive landscape is concentrated, with TE Connectivity and Amphenol collectively holding a significant share of approximately 30% of the global market, underscoring their dominance through extensive product portfolios and technological innovation.

MARKET DYNAMICS

MARKET DRIVERS

Proliferation of High-Density Electronics to Accelerate Market Expansion

The global electronics industry is experiencing unprecedented demand for miniaturized, high-performance devices across consumer electronics, telecommunications, and industrial automation sectors. Board-to-board connectors serve as critical components enabling the interconnection of increasingly dense printed circuit boards (PCBs) in compact electronic assemblies. The trend toward miniaturization and higher functionality per unit area drives the need for connectors with finer pitches, higher pin counts, and improved signal integrity. Recent technological advancements have enabled the development of connectors with pitches below 0.4mm, accommodating the space constraints of modern smartphones, wearables, and IoT devices. The consumer electronics segment alone accounts for approximately 42% of global board-to-board connector demand, reflecting the substantial market pull from this sector.

Automotive Electrification and Advanced Driver-Assistance Systems to Fuel Growth

The automotive industry’s rapid transition toward electrification and autonomous driving capabilities represents a significant growth driver for board-to-board connectors. Modern vehicles incorporate numerous electronic control units (ECUs), sensors, and infotainment systems that require reliable interconnections between PCBs. The average premium vehicle now contains over 150 ECUs, each requiring multiple board-to-board connections. The emergence of electric vehicles has further accelerated this trend, with battery management systems, power converters, and charging interfaces all demanding robust connector solutions. The automotive connector market is projected to grow at approximately 7% annually, substantially outpacing the overall connector market growth rate.

Furthermore, the implementation of 5G infrastructure and expansion of data centers are creating additional demand for high-speed, high-frequency board-to-board connectors capable of supporting data rates exceeding 25 Gbps. These applications require connectors with improved impedance matching, reduced crosstalk, and enhanced shielding capabilities.

➤ For instance, leading connector manufacturers have recently introduced products specifically designed for 112Gbps PAM4 applications in data center and networking equipment, addressing the need for higher bandwidth connectivity solutions.

The convergence of these technological trends across multiple industries ensures sustained demand for advanced board-to-board connector solutions, supporting market growth throughout the forecast period.

MARKET CHALLENGES

Increasing Complexity in Manufacturing and Quality Assurance to Pose Significant Challenges

As board-to-board connectors evolve toward finer pitches and higher performance specifications, manufacturers face substantial challenges in maintaining production quality and reliability. The manufacturing tolerances required for connectors with pitches below 0.5mm approach the limits of conventional precision manufacturing capabilities. This increased complexity results in higher production costs and more stringent quality control requirements. The industry experiences yield rates that can drop below 85% for the most advanced connector designs, particularly those incorporating mixed-signal capabilities or impedance-controlled characteristics.

Other Challenges

Thermal Management Constraints

The trend toward higher density interconnections creates significant thermal management challenges. As connector pitches decrease and pin counts increase, power density rises substantially, potentially leading to overheating and reliability issues. Designers must balance the conflicting requirements of miniaturization, electrical performance, and thermal management, often requiring innovative materials and cooling solutions that increase overall system cost.

Standardization and Compatibility Issues

The rapid pace of technological innovation has led to a proliferation of connector designs and standards, creating compatibility challenges for system integrators. While industry standards exist for many connector types, the continuous introduction of proprietary designs complicates the supply chain and increases inventory costs for manufacturers. This fragmentation necessitates additional engineering resources to ensure compatibility across different connector generations and manufacturers.

MARKET RESTRAINTS

Price Sensitivity in Consumer Markets to Constrain Premium Solutions Adoption

Despite the technological advancements in board-to-board connectors, significant price sensitivity persists, particularly in the consumer electronics segment where cost pressures are most intense. Manufacturers in this sector often prioritize cost reduction over performance enhancement, creating a challenging environment for premium connector solutions. The consumer electronics industry typically operates with profit margins ranging from 3-8% for volume products, leaving limited budget for advanced interconnection solutions. This price sensitivity forces connector manufacturers to develop cost-optimized designs that meet minimum performance requirements rather than pushing the boundaries of technological innovation.

Additionally, the lengthy qualification processes required for automotive and industrial applications act as a restraint on market expansion. These sectors typically require 18-24 months of rigorous testing and validation before approving new connector designs for production use. This extended timeline delays the adoption of newer, more advanced connector technologies and maintains older, more established designs in production longer than their technological relevance would suggest.

The combination of intense price pressure and lengthy qualification cycles creates a conservative adoption environment that restrains the market’s growth potential, particularly for innovative but higher-cost connector solutions.

MARKET OPPORTUNITIES

Emergence of Next-Generation Applications to Create New Growth Frontiers

The ongoing digital transformation across industrial, automotive, and consumer sectors presents substantial opportunities for board-to-board connector manufacturers. The integration of artificial intelligence capabilities into edge devices requires increasingly sophisticated interconnection solutions that can handle both high-speed data transfer and power delivery in constrained spaces. AI processors and accelerators typically require multiple high-density connectors with data rates exceeding 56Gbps, creating demand for advanced products that represent higher value opportunities for manufacturers.

Additionally, the medical electronics sector offers significant growth potential, particularly in diagnostic imaging, patient monitoring, and portable medical devices. These applications require connectors that meet stringent reliability standards, often needing to withstand sterilization processes, mechanical stress, and environmental challenges. The medical device connector market is growing at approximately 6.5% annually, driven by increasing healthcare digitization and the development of new medical technologies.

The expansion of 5G infrastructure and subsequent deployment of 6G technologies will further drive demand for high-frequency, low-loss connectors capable of operating in millimeter-wave frequency ranges. These applications require specialized materials and designs that command premium pricing and higher profit margins, representing attractive opportunities for technologically advanced connector manufacturers.

BOARD-TO-BOARD CONNECTORS MARKET TRENDS

Miniaturization and High-Speed Data Transmission Drive Market Evolution

The relentless push towards miniaturization in electronics is fundamentally reshaping the board-to-board connectors landscape. As consumer and industrial devices become smaller and more powerful, the demand for connectors with pitches below 1.00 mm has surged dramatically, accounting for a significant portion of the market. This trend is intrinsically linked to the exponential growth in data consumption, necessitating connectors capable of supporting high-speed data transmission protocols like PCIe 5.0 and USB4. The global 5G infrastructure rollout, which requires dense, high-frequency interconnects in base stations and network equipment, is a primary catalyst. Consequently, manufacturers are heavily investing in advanced materials and contact designs to reduce signal loss and crosstalk while maintaining mechanical integrity in increasingly compact form factors.

Other Trends

Automotive Electrification and Automation

The transformation of the automotive sector is a powerful engine for board-to-board connector demand. The proliferation of electric vehicles (EVs) and advanced driver-assistance systems (ADAS) has created an insatiable need for reliable, high-power, and high-speed interconnects. A single modern vehicle can incorporate over 3,000 connectors, with board-to-board types being critical for infotainment systems, sensor fusion modules, and battery management systems. This application segment is projected to be one of the fastest-growing, driven by automotive OEMs’ continuous integration of more electronic control units (ECUs) to achieve higher levels of autonomy, which directly increases the average connector content per vehicle.

Supply Chain Resilience and Regional Manufacturing Shifts

Recent global disruptions have underscored the critical importance of supply chain resilience, prompting a notable trend towards regionalization and strategic inventory management. While Asia-Pacific remains the dominant manufacturing hub, accounting for over 60% of global production and consumption, there is a concerted effort in North America and Europe to bolster local semiconductor and electronic component supply chains. This is supported by government initiatives and significant corporate investment in nearshoring and friendshoring. Furthermore, leading players are diversifying their production bases and adopting more robust inventory strategies to mitigate future disruptions, ensuring a steadier flow of these essential components to downstream industries like telecommunications and industrial automation.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Focus on Miniaturization and High-Speed Connectivity to Maintain Dominance

The global board-to-board connectors market exhibits a semi-consolidated structure, characterized by intense competition among a mix of large multinational corporations and specialized medium to small-sized manufacturers. TE Connectivity and Amphenol collectively command a significant portion of the market, holding an estimated combined share of approximately 30% as of 2024. Their leadership is anchored in extensive product portfolios, robust global distribution networks, and deep-rooted relationships with key OEMs across the consumer electronics, automotive, and industrial sectors.

Molex (a subsidiary of Koch Industries) and Foxconn (Hon Hai Precision Industry) are also pivotal players, leveraging their massive scale and vertical integration capabilities. These companies consistently invest in developing connectors for next-generation applications, including 5G infrastructure, high-performance computing, and electric vehicles, which require higher data rates and power delivery in increasingly compact form factors.

Furthermore, Japanese firms like JST, Hirose Electric, and JAE are renowned for their precision engineering and stronghold in high-density and miniaturized connector solutions, particularly within the Asian consumer electronics and automotive markets. Their growth is fueled by continuous innovation in pitch sizes below 1.00 mm to meet the demands for thinner and lighter end devices.

To solidify their positions, these key players are actively pursuing strategies such as strategic mergers and acquisitions, expanding manufacturing capacities in low-cost regions, and heavy investment in R&D for advanced materials and contact plating technologies. This ensures improved signal integrity, higher durability, and compliance with evolving industry standards, which is critical for maintaining a competitive edge.

List of Key Board-to-Board Connector Companies Profiled

- TE Connectivity Ltd. (Switzerland)

- Amphenol Corporation (U.S.)

- Molex, LLC (U.S.)

- Foxconn (Hon Hai Precision Industry Co., Ltd.) (Taiwan)

- Japan Aviation Electronics Industry, Ltd. (JAE) (Japan)

- Samtec, Inc. (U.S.)

- JST Mfg. Co., Ltd. (Japan)

- Hirose Electric Co., Ltd. (Japan)

- HARTING Technology Group (Germany)

- ERNI Electronics (a member of the TE Connectivity family) (Germany)

- Kyocera Corporation (Japan)

- Advanced Interconnect (U.S.)

- YAMAICHI Electronics Co., Ltd. (Japan)

Segment Analysis:

By Type

1.00 mm~2.00 mm Pitch Segment Dominates the Market Due to its Optimal Balance of Density and Reliability

The market is segmented based on type into:

- Below 1.00 mm

- Subtypes: Micro pitch, Mezzanine, and others

- 1.00 mm~2.00 mm

- Above 2.00 mm

- Subtypes: Standard pitch, Power, and others

By Application

Consumer Electronics Segment Leads Due to High Volume Demand from Smartphones and Portable Devices

The market is segmented based on application into:

- Consumer Electronics

- Communications

- Transportation

- Industries

- Military

- Others

By End User

OEMs Represent the Largest End User Segment Due to Direct Integration in Electronic Assembly

The market is segmented based on end user into:

- Original Equipment Manufacturers (OEMs)

- Electronic Manufacturing Services (EMS)

- Aftermarket

Regional Analysis: Board-to-Board Connectors Market

Asia-Pacific

The Asia-Pacific region is the undisputed global leader in the Board-to-Board Connectors market, accounting for over 60% of global consumption by volume. This dominance is fueled by its position as the world’s electronics manufacturing hub, particularly in consumer electronics and communications equipment. China is the epicenter of both production and consumption, driven by massive domestic demand and its role as the primary exporter of electronic goods. Countries like Japan, South Korea, and Taiwan are critical for high-end, precision connector manufacturing, serving global automotive and industrial automation sectors. India is emerging as a significant growth market, supported by government initiatives like the Production Linked Incentive (PLI) scheme for electronics manufacturing, which is attracting investment and boosting local demand. The region’s growth is characterized by high-volume production of connectors with pitches below 1.00 mm and 1.00 mm~2.00 mm, primarily for smartphones, laptops, and networking devices. However, intense price competition and supply chain volatility remain persistent challenges.

North America

North America represents a mature yet technologically advanced market for Board-to-Board Connectors, characterized by demand for high-reliability and specialized products. The region’s strength lies in its innovation-driven sectors, including aerospace, defense, medical devices, and advanced telecommunications infrastructure, such as the ongoing rollout of 5G networks. The United States is the largest market within the region, with significant contributions from Canada’s burgeoning tech sector. Demand is heavily skewed towards connectors with pitches above 2.00 mm for industrial applications and highly miniaturized, high-speed connectors for next-generation computing and data centers. The presence of leading global players like TE Connectivity and Amphenol, who are headquartered in the region, fosters a strong ecosystem for research and development. Market growth is steady, supported by reinvestment in domestic manufacturing and stringent quality standards that prioritize performance and durability over cost.

Europe

Europe’s Board-to-Board Connectors market is defined by its robust automotive industrial base and strict regulatory standards. Germany, as the automotive capital of the region, drives significant demand for connectors used in vehicle electrification, advanced driver-assistance systems (ADAS), and in-vehicle infotainment. The region also has a strong presence in industrial automation, medical technology, and renewable energy systems, all of which require highly reliable and often customized connector solutions. European manufacturers are leaders in developing environmentally compliant products, adhering to directives like RoHS and REACH. While the market growth is more measured compared to Asia-Pacific, it is stable and value-oriented, with a focus on engineering excellence, product longevity, and meeting the specific needs of high-margin B2B sectors. The United Kingdom, France, and Italy are other key contributors to the regional market.

South America

The South American market for Board-to-Board Connectors is in a developing phase, with growth potential tied to the gradual modernization of its industrial and communications infrastructure. Brazil is the largest economy and thus the primary market, with demand stemming from the automotive sector and increasing investments in telecommunications. Argentina also presents opportunities, though economic instability often leads to market volatility and constrains larger investments. The region predominantly relies on imported connectors, with cost sensitivity leading to higher demand for standard, lower-pitch products. The adoption of advanced connector technologies is slower compared to other regions, hindered by economic challenges and a less mature local electronics manufacturing ecosystem. Nonetheless, long-term prospects are tied to economic recovery and increased digitalization efforts across the continent.

Middle East & Africa

The Board-to-Board Connectors market in the Middle East & Africa is nascent and fragmented. Growth is primarily concentrated in a few key areas: the oil and gas industry’s need for industrial automation, telecommunications infrastructure projects in Gulf Cooperation Council (GCC) nations like Saudi Arabia and the UAE, and consumer electronics markets in more developed urban centers. Israel stands out as a technology hub, generating specialized demand for connectors in its renowned tech and defense sectors. However, across much of Africa, market development is challenged by limited local manufacturing, reliance on imports, and infrastructural constraints. The region represents a long-term opportunity as digital transformation initiatives gain traction, but current market volume remains a small fraction of the global total.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Board-to-Board Connectors market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Board-to-Board Connectors Market?

-> Board-to-Board Connectors Market was valued at 3770 million in 2024 and is projected to reach US$ 4897 million by 2032, at a CAGR of 3.9% during the forecast period.

Which key companies operate in Global Board-to-Board Connectors Market?

-> Key players include TE Connectivity, Amphenol, Molex, Foxconn, JAE, Delphi, Samtec, JST, Hirose, HARTING, ERNI Electronics, Kyocera Corporation, Advanced Interconnect, and YAMAICHI, among others.

What are the key growth drivers?

-> Key growth drivers include increasing demand for consumer electronics, expansion of 5G infrastructure, automotive electrification, and industrial automation.

Which region dominates the market?

-> Asia-Pacific dominates the market, accounting for over 60% of global revenue, driven by strong manufacturing presence in China, Japan, and South Korea.

What are the emerging trends?

-> Emerging trends include miniaturization of connectors, high-speed data transmission capabilities, development of waterproof and high-temperature resistant connectors, and integration of smart manufacturing processes.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...