Market Insights

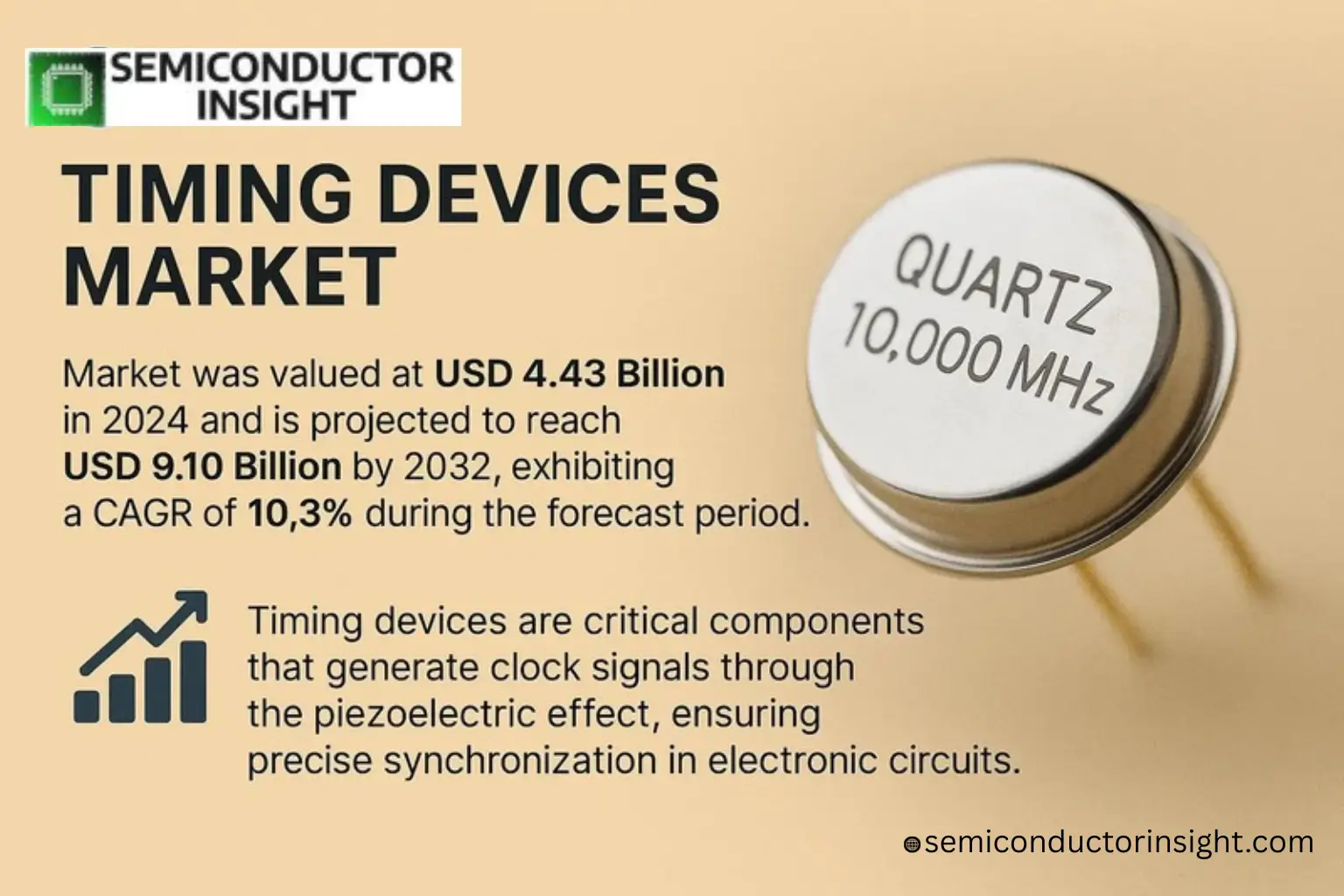

Global Timing Devices Market was valued at USD 4.43 billion in 2024 and is projected to reach USD 9.10 billion by 2032, exhibiting a CAGR of 10.3% during the forecast period.

Timing devices are critical components that generate clock signals through the piezoelectric effect, ensuring precise synchronization in electronic circuits. These devices are widely used in applications such as mobile phones, wearable devices, and AV/PC systems, providing stable oscillating signals for accurate data transmission and operational efficiency.

The market growth is driven by the proliferation of consumer electronics, advancements in telecommunications (particularly 5G networks), and increasing adoption in automotive electronics for ADAS and infotainment systems. Additionally, industrial automation and IoT expansion further fuel demand for high-precision timing solutions. Key players like TXC, Seiko Epson, and Nihon Dempa Kogyo (NDK) dominate the market, collectively holding approximately 24% of global revenue share.

MARKET DRIVERS

Increasing Demand for Precision in Electronics

The Timing Devices Market is experiencing growth due to the rising need for high-precision timing solutions in consumer electronics, telecommunications, and automotive applications. With the proliferation of 5G networks and IoT devices, the demand for accurate timing components has surged by approximately 12% annually. Manufacturers are investing heavily in quartz and MEMS-based timing devices to meet these requirements.

Automotive Sector Expansion

Advanced driver-assistance systems (ADAS) and in-vehicle networking require highly reliable timing devices for synchronization. The automotive sector now accounts for nearly 18% of timing device sales, with projections indicating further growth as electric vehicle adoption accelerates globally.

Industrial automation applications are also contributing to market expansion, with factory equipment requiring precise timing for synchronization across distributed control systems.

MARKET CHALLENGES

Supply Chain Disruptions

The Timing Devices Market faces ongoing challenges from semiconductor shortages and logistical bottlenecks. Lead times for certain quartz crystals have extended to 26 weeks in some cases, forcing manufacturers to rethink inventory strategies. Pricing volatility for raw materials like synthetic quartz has increased production costs by 8-12% across the industry.

Other Challenges

Miniaturization Constraints

As devices shrink, timing components face physical limitations in maintaining stability and accuracy. The transition to smaller packages (below 1.0×0.8mm) has increased failure rates by 15% in some product categories, requiring additional R&D investment.

MARKET RESTRAINTS

Competition from Alternative Technologies

The adoption of system-on-chip (SoC) designs with integrated timing functionality is impacting standalone timing device sales, particularly in mobile applications. Approximately 28% of smartphones now use integrated timing solutions, reducing demand for discrete components. This trend is expected to continue as semiconductor integration improves.

MARKET OPPORTUNITIES

Emerging 6G Development

With 6G research gaining momentum, the Timing Devices Market stands to benefit from next-generation network requirements. Early specifications indicate timing accuracy needs will be 100x stricter than 5G, creating opportunities for advanced atomic clocks and ultra-stable oscillators. The aerospace and defense sector’s increasing need for secure timing solutions also presents a USD 850 million addressable market by 2028.

Timing Devices Market Trends

Precision Timing Solutions Drive Global Market Growth

Global Timing Devices Market continues to expand, projected to grow from USD 4.4 billion in 2024 to USD 9.1 billion by 2032, representing a 10.3% CAGR. This growth stems from increasing demand across consumer electronics, telecommunications, and automotive sectors, where precise timing synchronization is critical for optimal performance.

Other Trends

5G Network Expansion Accelerates Demand

Global rollout of 5G infrastructure requires high-precision timing devices for network synchronization, with quartz crystal units accounting for 48% of market share. Leading manufacturers like TXC, Seiko Epson, and Nihon Dempa Kogyo are expanding production capacity to meet this growing demand.

Regional Market Concentration

Japan dominates the Timing Devices Market with 32% global share, followed by North America and China. This concentration reflects the presence of major manufacturers and advanced electronics production capabilities in these regions.

Emerging Applications in Automotive Electronics

The integration of advanced driver-assistance systems (ADAS) and vehicle connectivity solutions is creating new opportunities for timing device manufacturers. The automotive segment represents one of the fastest-growing application areas, with demand expected to increase by 12% annually through 2032.

Sustainable Manufacturing Practices

Major players are investing in environmentally-friendly production methods for timing devices, including reduced energy consumption processes and recyclable materials, responding to growing environmental regulations across key markets.

IoT and Industrial Automation Expansion

The growth of Industry 4.0 and IoT applications continues to drive demand for timing solutions, particularly in industrial equipment and communication devices. With mobile terminals accounting for 49% of application share, manufacturers are developing more compact and energy-efficient timing components for these use cases.

COMPETITIVE LANDSCAPE

Key Industry Players

Dynamic Market Dominated by Japanese Quartz Crystal Specialists

The Timing Devices Market exhibits consolidated competition with Japanese manufacturers TXC, Seiko Epson, and Nihon Dempa Kogyo (NDK) collectively controlling 24% global market share. These leaders benefit from decades of quartz crystal expertise and vertically integrated supply chains. TXC Corporation maintains technological leadership in miniature high-frequency oscillators, while NDK dominates the automotive timing components segment through partnerships with Tier 1 suppliers.

Second-tier competitors focus on niche applications, with Microchip Technology and SiTime leading MEMS oscillator innovation for 5G infrastructure. Rakon and Hosonic Electronic have gained traction in aerospace-grade timing solutions, whereas Murata and KYOCERA Crystal Device (KCD) compete through cost-optimized quartz offerings. Emerging Chinese players like Zhejiang East Crystal Electronic are disrupting the low-end market with competitive pricing for consumer electronics applications.

List of Key Timing Devices Companies Profiled

- TXC Corporation

- Seiko Epson Corporation

- Nihon Dempa Kogyo (NDK)

- KYOCERA Crystal Device (KCD)

- Daishinku Corp (KDS)

- Microchip Technology

- Rakon Limited

- Hosonic Electronic Co., Ltd.

- SiTime Corporation

- Siward Crystal Technology

- Micro Crystal AG

- Diodes Incorporated

- Murata Manufacturing

- Tai-Saw Technology

- Abracon LLC

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Quartz Crystal Units dominate the Timing Devices Market due to:

|

| By Application |

|

Mobile Terminals represent the largest application segment because:

|

| By End User |

|

Consumer Electronics leads as the primary end-user segment due to:

|

| By Technology |

|

Conventional Quartz technology maintains market leadership because:

|

| By Precision Level |

|

High Precision timing devices are gaining traction due to:

|

Regional Analysis: Timing Devices Market

Asia-Pacific accounts for over 60% of global consumer electronics production, creating substantial demand for precision timing devices in smartphones, wearables, and smart home devices.

The region’s growing automotive industry, particularly electric vehicle production in China, requires advanced timing solutions for infotainment systems and ADAS technologies.

Massive 5G infrastructure rollout across major Asian markets drives demand for high-precision timing devices essential for network synchronization and base station operations.

Concentrated semiconductor manufacturing ecosystem enables efficient timing device production and distribution throughout the region’s electronics value chain.

North America

North America remains a technology leader in high-end timing devices, particularly for aerospace, defense, and enterprise applications. The region benefits from strong R&D capabilities and early adoption of advanced timing technologies. Silicon Valley’s semiconductor innovators and established timing device manufacturers contribute to market innovation. Growing demand for synchronized timing in financial trading systems and data centers presents new opportunities.

Europe

Europe maintains steady demand for timing devices, driven by automotive production and industrial applications. Germany’s manufacturing sector and Switzerland’s precision instrumentation industry are key consumers. The region emphasizes high-reliability timing solutions for critical infrastructure and aerospace applications. EU initiatives supporting semiconductor independence may influence future timing device supply chains.

South America

South America shows emerging potential in the Timing Devices Market, primarily serving consumer electronics and automotive aftermarkets. Brazil’s industrial base and Argentina’s growing electronics sector create localized demand. Infrastructure challenges and economic volatility currently limit more significant market penetration.

Middle East & Africa

The Middle East & Africa region presents niche opportunities in telecom infrastructure and oil/gas applications. Dubai’s smart city initiatives and African mobile network expansions drive timing device adoption. Limited local manufacturing capabilities result in reliance on imports, creating potential for market growth as digital infrastructure expands.

Report Scope

This market research report provides a comprehensive analysis of the Timing Devices Market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of timing devices in powering advancements across industries such as consumer electronics, automotive, telecommunications, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of IoT, design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Timing Devices Market?

-> Timing Devices Market was valued at USD 4.43 billion in 2024 and is projected to reach USD 9.10 billion by 2032, exhibiting a CAGR of 10.3% during the forecast period.

Which key companies operate in Timing Devices Market?

-> Key players include TXC, Seiko Epson, Nihon Dempa Kogyo (NDK), Kyocera Crystal Device (KCD), Daishinku Corp (KDS), Microchip, Rakon, and Hosonic Electronic, among others. The top three manufacturers account for approximately 24% of the global share.

What are the key growth drivers?

-> Key growth drivers include proliferation of consumer electronics, advancements in telecommunications (5G networks), automotive industry expansion (ADAS systems), and growth of Industrial Automation and IoT.

Which region dominates the market?

-> Japan has the largest market share globally at approximately 32%, while Asia-Pacific remains a dominant region overall.

What are the emerging trends?

-> Emerging trends include increasing adoption of quartz crystal devices (48% market share), demand from mobile terminal applications (49% share), and technological advancements in high-precision timing solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...