Automotive-grade neural processing unit chip for ADAS sensor fusion Market Insights

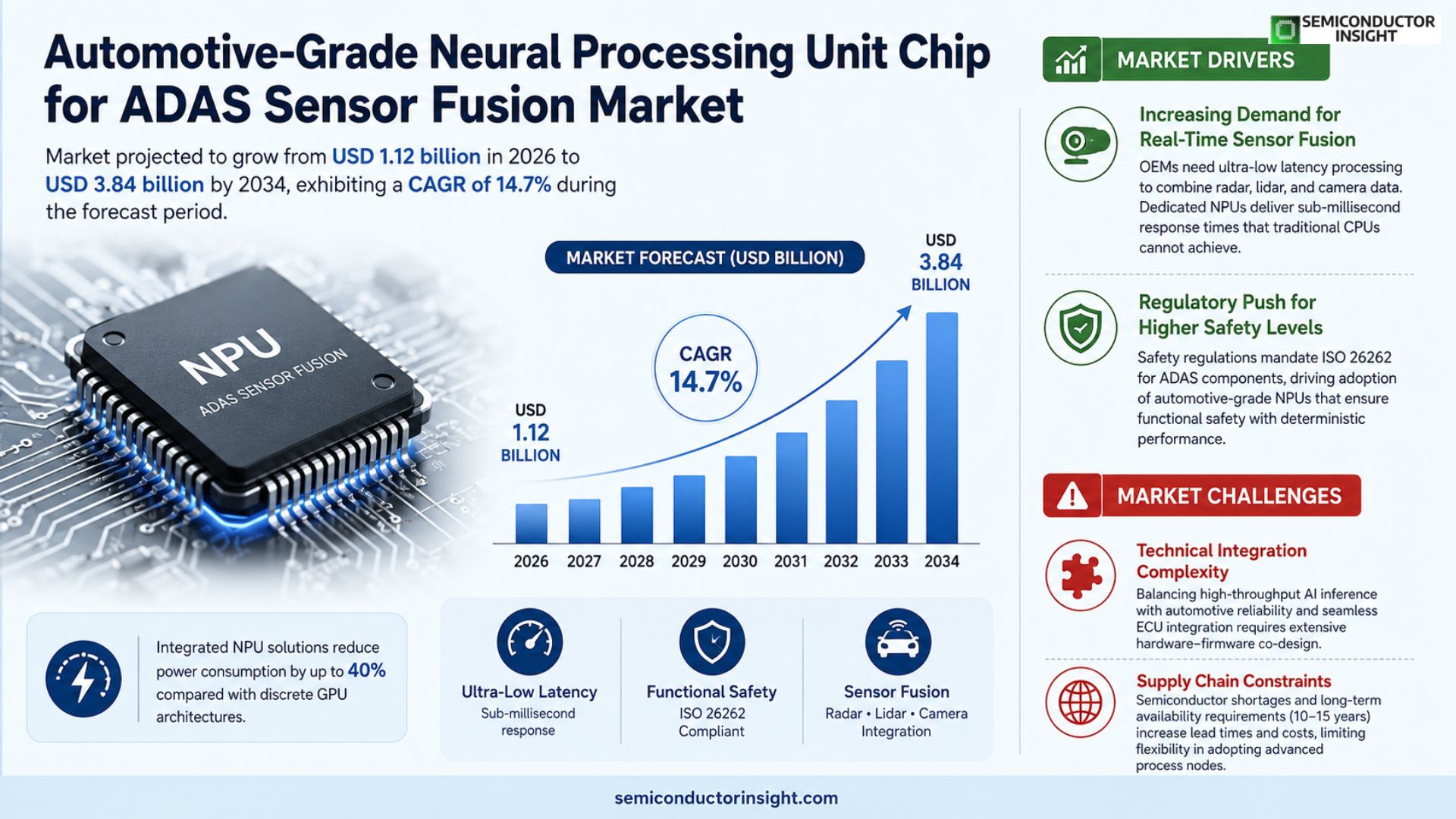

Global Automotive-grade neural processing unit chip for ADAS sensor fusion market size was valued at USD 1.05 billion in 2025. The market is projected to grow from USD 1.12 billion in 2026 to USD 3.84 billion by 2034, exhibiting a CAGR of 14.7% during the forecast period.

Automotive‑grade neural processing unit (NPU) chips are purpose‑built silicon accelerators that execute real‑time sensor‑fusion algorithms for advanced driver‑assistance systems (ADAS). They deliver high‑throughput matrix operations required for perception tasks,such as object detection and lane recognition,while complying with automotive reliability standards like AEC‑Q100.

The market is accelerating because OEMs are targeting higher autonomy levels that demand on‑chip AI performance beyond traditional CPUs; however, power consumption and thermal constraints remain challenges in vehicle environments. Furthermore, stringent functional‑safety regulations push manufacturers toward proven NPU solutions. Leading semiconductor players,including NVIDIA, Qualcomm and Renesas,are expanding their portfolios through collaborations with Tier‑1 suppliers, further driving adoption.

MARKET DRIVERS

Increasing Demand for Real‑Time Sensor Fusion

Automotive‑grade neural processing unit chip for ADAS sensor fusion Market is propelled by the rapid integration of advanced driver‑assistance systems across new vehicle models. OEMs require ultra‑low latency processing to combine radar, lidar, and camera data, and dedicated NPUs deliver sub‑millisecond response times that traditional CPUs cannot achieve.

Regulatory Push for Higher Safety Levels

Safety regulations in Europe, North America, and China now mandate functional safety standards such as ISO 26262 for ADAS components. This creates a clear incentive for manufacturers to adopt automotive‑grade NPUs that meet functional safety requirements while maintaining deterministic performance.

➤ Integrated NPU solutions reduce power consumption by up to 40% compared with discrete GPU architectures, extending vehicle range and lowering thermal design constraints.

Combined, these forces generate a robust growth trajectory for the market, with forecasts indicating double‑digit CAGR through 2032 as more vehicles target Level‑2+ automation.

MARKET CHALLENGES

Technical Integration Complexity

Designing an automotive‑grade NPU that seamlessly interfaces with existing electronic control units (ECUs) poses significant engineering challenges. Engineers must balance high‑throughput neural inference with strict automotive reliability standards, often requiring extensive co‑design of hardware and firmware.

Other Challenges

Supply Chain Constraints

Global semiconductor shortages and limited fab capacity for automotive‑qualified silicon increase lead times, driving up component costs and potentially delaying model launches that depend on advanced NPU technology.

Furthermore, the need for long‑term part availability (10‑15 years) adds pressure on manufacturers to secure stable supply agreements, which can restrict flexibility in adopting newer process nodes.

MARKET RESTRAINTS

High Development Costs

Developing an automotive‑grade NPU requires substantial R&D investment, including validation on harsh temperature cycles, vibration testing, and compliance with functional safety standards. These upfront costs can deter smaller suppliers from entering the market.

Stringent Qualification Standards

Certification processes such as AEC‑QS and IEC 61508 demand exhaustive testing and documentation, extending time‑to‑market and increasing the total cost of ownership for NPU‑based ADAS solutions.

MARKET OPPORTUNITIES

Emerging 5G‑Connected Vehicles

The rollout of 5G connectivity enables edge‑to‑cloud data exchange, allowing NPUs to offload non‑critical inference tasks while retaining real‑time processing for safety‑critical functions. This hybrid architecture opens new revenue streams for chipset vendors.

Growth of Level‑3 and Level‑4 Autonomy

As automakers target higher levels of autonomy, the computational demand for sensor fusion escalates dramatically. Automotive‑grade NPUs, optimized for parallel neural workloads, are uniquely positioned to meet these requirements, creating a sizable market niche.

Strategic Partnerships with Tier‑1 Suppliers

Collaborations between semiconductor firms and Tier‑1 automotive suppliers accelerate integration cycles, delivering pre‑qualified NPU modules that reduce engineering effort for OEMs and shorten deployment timelines.

Automotive-grade neural processing unit chip for ADAS sensor fusion Market Trends

Increasing Adoption of High‑Performance NPU Chips for Advanced Driver‑Assistance

Vehicle manufacturers are accelerating the integration of Automotive‑grade neural processing unit chips for ADAS sensor fusion Market as they pursue higher levels of autonomy. These purpose‑built silicon accelerators enable real‑time perception algorithms such as object detection, lane recognition, and sensor‑data correlation while meeting automotive reliability standards. The shift from legacy CPUs to dedicated NPUs improves computational throughput and reduces latency, which is critical for safety‑critical driving functions. At the same time, designers are focusing on power‑efficient architectures to address the thermal constraints inherent in vehicle environments.

Other Trends

Regulatory Influence on NPU Design

Functional‑safety regulations, including AEC‑Q100 certification and ISO 26262 compliance, are shaping the development roadmap of neural processing units. Manufacturers must demonstrate deterministic behavior and fault‑tolerant operation, prompting the adoption of hardened silicon and rigorous validation processes. These requirements are driving a convergence between automotive‑grade quality assurance and advanced AI capabilities, ensuring that each chip can sustain the safety expectations of modern ADAS deployments.

Strategic Partnerships Accelerating Ecosystem Maturity

Leading semiconductor firms are forging collaborations with Tier‑1 suppliers and original equipment manufacturers to streamline the supply chain and co‑develop reference designs. Partnerships between NVIDIA, Qualcomm, Renesas, and major automotive suppliers facilitate faster technology transfer, standardized integration kits, and joint validation programs. This ecosystem synergy reduces time‑to‑market for new models and creates a more predictable roadmap for future AI‑driven safety features. As these alliances deepen, the overall market trajectory for Automotive‑grade neural processing unit chip for ADAS sensor fusion remains robust, reflecting a healthy blend of innovation, compliance, and collaborative execution.

COMPETITIVE LANDSCAPE

Key Industry Players

Automotive‑grade Neural Processing Unit (NPU) Chips Power ADAS Sensor Fusion

The market is dominated by a handful of large semiconductor firms that have leveraged deep‑learning expertise to create automotive‑grade NPU solutions meeting AEC‑Q100 safety standards. NVIDIA leads with its DRIVE Orin family, integrating high‑throughput tensor cores and a mature software stack that appeals to Tier‑1 system integrators. Qualcomm follows closely with the Snapdragon Ride platform, offering a balance of performance, low power consumption, and extensive 5G connectivity for over‑the‑air updates. Renesas complements these leaders by focusing on safety‑critical designs that integrate NPU blocks with existing microcontroller families, enabling OEMs to consolidate silicon footprints. Intel’s Mobileye Vision Pro, while rooted in vision‑processing, incorporates a specialized NPU to accelerate perception algorithms, reinforcing Intel’s push into high‑level autonomy. Collectively, these players shape market structure through strategic partnerships, extensive developer ecosystems, and a clear focus on meeting functional‑safety regulations.

Beyond the marquee names, a diverse set of niche innovators contributes specialized capabilities that enrich the competitive landscape. Samsung Electronics provides a full‑stack automotive solution that couples its Exynos Auto NPU with advanced memory technologies, targeting premium vehicle platforms. Texas Instruments offers edge‑optimized NPUs embedded within its automotive safety processors, emphasizing ultra‑low latency for real‑time sensor fusion. STMicroelectronics and NXP Semiconductors each deliver heterogeneous platforms that blend NPU cores with automotive‑grade MCUs, catering to cost‑sensitive models. Ambarella’s CVflow series and Horizon Robotics’ Sunrise platforms specialize in compact, power‑efficient designs for emerging ADAS functions. Smaller firms such as MediaTek, Infineon, ON Semiconductor, Lattice Semiconductor, and BlackBerry QNX focus on niche market segments ranging from low‑cost city cars to safety‑critical infotainment, often partnering with OEMs to customize silicon for specific sensor‑fusion workloads.

List of Key Automotive-grade Neural Processing Unit Companies Profiled

- NVIDIA

- Qualcomm

- Renesas Electronics

- Intel (Mobileye)

- Samsung Electronics

- Texas Instruments

- STMicroelectronics

- NXP Semiconductors

- Ambarella

- Horizon Robotics

- MediaTek

- Infineon Technologies

- ON Semiconductor

- Lattice Semiconductor

- BlackBerry QNX

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Vision‑focused NPU – Optimized for high‑resolution camera streams, delivering rapid object detection and lane‑mark recognition. – Provides dedicated tensor cores that lower inference latency for perception algorithms. – Meets stringent automotive reliability standards, ensuring stable performance across wide temperature ranges. |

| By Application |

|

Object detection & classification – Core driver‑assist function that requires real‑time perception of pedestrians, vehicles, and obstacles. – Drives design of NPU memory hierarchy to sustain high‑throughput feature extraction. – Aligns closely with safety‑critical certification paths, making it the focal point for OEM roadmaps. |

| By End User |

|

OEMs (Vehicle manufacturers) – Directly define functional‑safety requirements and integration timelines, shaping NPU feature sets. – Seek solutions that can be embedded early in vehicle architecture for seamless firmware updates. – Prioritize proven silicon that aligns with long product‑life cycles and stringent reliability mandates. |

| By Functional Safety Level |

|

ASIL D compliant – Represents the highest automotive safety integrity level, driving rigorous validation of NPU cores. – Encourages architectural redundancy and deterministic execution paths within the chip. – Positions the segment as the preferred choice for advanced autonomy features that cannot tolerate functional failures. |

| By Integration Form Factor |

|

Embedded NPU modules – Integrate NPU alongside memory and power‑management ICs, reducing board‑level complexity. – Offer thermal advantages by sharing heat‑spreading substrates, critical for vehicle interior environments. – Enable faster time‑to‑market for OEMs seeking compact, validated AI compute blocks. |

Regional Analysis: North America

North America

The continuous evolution of neural network architectures and chip designs is a key factor driving innovation in Automotive-grade neural processing unit chip market. Advancements in artificial intelligence (AI) algorithms are enabling more complex and accurate processing of sensor data. This includes improvements in deep learning models optimized for edge computing, allowing for faster and more efficient real-time decision-making within vehicles. Development of specialized hardware architectures tailored for AI workloads is also accelerating performance and reducing power consumption.

The regulatory environment plays a significant role in shaping Automotive-grade neural processing unit chip market. Increasing safety regulations and mandates for ADAS features are driving demand for advanced sensor fusion capabilities. Government initiatives promoting autonomous driving research and development are also creating favorable market conditions. Compliance with cybersecurity standards is becoming increasingly important as vehicles become more connected and reliant on software. The evolving regulatory landscape necessitates continuous innovation and adaptation in chip design and functionality.

The global supply chain for automotive-grade neural processing unit chips is complex and subject to various factors. Geopolitical tensions and component shortages have impacted the availability and pricing of these chips. Efforts to diversify supply chains and establish regional manufacturing hubs are gaining momentum. Collaboration between chip manufacturers and automotive OEMs is crucial for ensuring a stable and reliable supply of these critical components. Development of more resilient and localized supply chains is a key focus area for market participants.

Automotive-grade neural processing unit chip market is characterized by intense competition among established semiconductor companies and emerging startups. Key players are investing heavily in R&D to develop cutting-edge chip architectures and expand their product portfolios. Strategic partnerships and collaborations are common as companies seek to leverage each other’s strengths and accelerate innovation. The competitive landscape is evolving rapidly, with new entrants and disruptive technologies emerging regularly.

Europe

The European market for automotive-grade neural processing unit chips for ADAS sensor fusion is experiencing robust growth, propelled by stringent safety regulations and a strong focus on electric vehicle (EV) development. European automakers are aggressively integrating ADAS technologies into their vehicle offerings to meet increasingly demanding safety standards. The region’s advanced automotive manufacturing base and strong technological capabilities provide a solid foundation for market expansion. Furthermore, government initiatives promoting sustainable transportation and autonomous driving are contributing to market growth. The emphasis on data privacy and security is influencing chip design and functionality within the European market.

Asia-Pacific

Asia-Pacific represents a significant and rapidly expanding market for automotive-grade neural processing unit chips. China, in particular, is emerging as a major hub for automotive manufacturing and technology innovation. The increasing affordability of vehicles in the region, coupled with a growing middle class, is driving demand for ADAS features. Government support for the automotive industry and investments in R&D are further fueling market growth. The region’s strong electronics manufacturing ecosystem provides a competitive advantage for chip production. Focus on connected and autonomous vehicle technologies is a key driver for adoption.

United States

The United States market for automotive-grade neural processing unit chips is characterized by a strong emphasis on innovation and a well-established automotive industry. The country is a leader in autonomous driving research and development, with major automakers and technology companies investing heavily in this area. Stringent safety regulations and consumer demand for advanced safety features are driving market growth. The US market benefits from a robust supply chain and a strong R&D ecosystem. Competition is intense, with both domestic and international chip manufacturers vying for market share.

South America

South America represents a smaller but growing market for automotive-grade neural processing unit chips. The increasing adoption of safety features in new vehicles and the growing demand for connected car technologies are driving market growth. Economic development in the region is contributing to increased vehicle sales and demand for advanced features. Government initiatives promoting the automotive industry are also supporting market expansion. The market is relatively price-sensitive, with a focus on cost-effective solutions.

Middle East & Africa

The Middle East & Africa market for automotive-grade neural processing unit chips is characterized by emerging growth potential. Increasing disposable incomes and a growing interest in advanced automotive technologies are driving demand for ADAS features. Government investments in infrastructure development and urban planning are also supporting market growth. The region’s automotive industry is undergoing significant transformation, with a growing focus on electric vehicles and autonomous driving. The market is influenced by regional economic conditions and political stability.

Report Scope

This market research report provides a comprehensive analysis of the Automotive-grade neural processing unit chip for ADAS sensor fusion Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Automotive-grade neural processing unit chip for ADAS sensor fusion Market?

-> Automotive-grade neural processing unit chip for ADAS sensor fusion Market was valued at USD 1.05 billion in 2025 and is expected to reach USD 3.84 billion by 2034.

Which key companies operate in Automotive-grade neural processing unit chip for ADAS sensor fusion Market?

-> Key players include NVIDIA, Qualcomm, Renesas, among others.

What are the key growth drivers?

-> Key growth drivers include higher autonomy level demand, need for on‑chip AI performance, and stringent functional‑safety regulations.

Which region dominates the market?

-> The market is global with significant activity across North America, Europe, and Asia‑Pacific.

What are the emerging trends?

-> Emerging trends include integration of AI/ADAS functions into NPU chips, power‑efficient designs, and collaborations between semiconductor firms and Tier‑1 automotive suppliers.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...