MARKET INSIGHTS

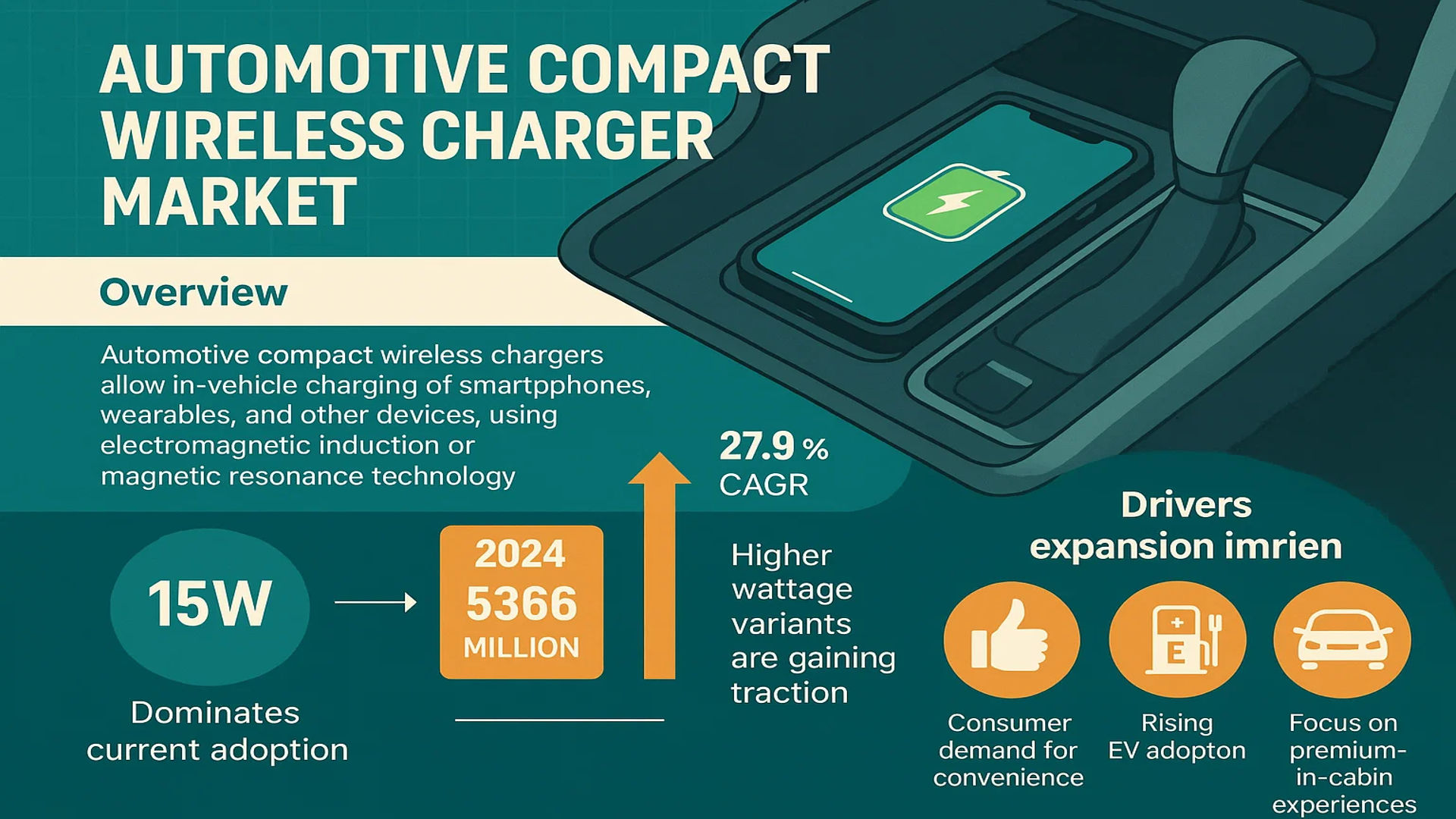

The global Automotive Compact Wireless Charger Market was valued at 941 million in 2024 and is projected to reach US$ 5366 million by 2032, at a CAGR of 27.9% during the forecast period.

Automotive Compact Wireless Chargers are in-vehicle charging devices utilizing electromagnetic induction or magnetic resonance technology to wirelessly charge smartphones, wearables, and other compatible devices. These compact solutions eliminate cable clutter while offering seamless integration into vehicle interiors like center consoles and armrests, enhancing both functionality and aesthetics. The 15W power segment dominates current adoption, though higher-wattage 40/50W variants are gaining traction for faster charging capabilities.

The market expansion is driven by increasing consumer demand for convenience features, rising EV adoption (where wireless charging aligns with tech-forward designs), and automakers’ focus on premium in-cabin experiences. However, standardization challenges and slower charging speeds compared to wired alternatives currently restrain broader implementation. Key players like Continental, Qualcomm, and Aptiv are investing heavily in Qi-compatible solutions, with recent partnerships accelerating technology integration in both passenger and commercial vehicle segments across North America, Europe, and Asia-Pacific regions.

MARKET DYNAMICS

MARKET DRIVERS

Rise in Smartphone Penetration and Demand for In-Vehicle Connectivity to Spur Market Growth

The global automotive compact wireless charger market is witnessing robust growth driven by accelerating smartphone adoption and consumer demand for seamless in-vehicle connectivity solutions. With smartphone ownership exceeding 6.8 billion devices globally, drivers increasingly expect charging convenience without cable clutter. Modern vehicles are being designed as mobility hubs, integrating wireless charging pads into center consoles and armrests as standard or optional features. This integration aligns with consumer preferences for minimalist, high-tech interiors that maintain device functionality during transit.

Advancements in Fast Charging Technologies to Accelerate Adoption

Technological breakthroughs in wireless power transfer efficiency are eliminating traditional charging speed limitations. The emergence of 40W-50W fast wireless charging solutions has reduced charging times by over 60% compared to standard 15W systems. Major automakers are collaborating with semiconductor companies to develop proprietary fast-charging protocols that maintain device battery health while delivering power comparable to wired solutions. These advancements address critical consumer pain points, making wireless charging a viable alternative to traditional charging methods.

The growing electrification of vehicle architectures further supports this transition, as modern EV platforms are designed with integrated power management systems capable of supporting multiple high-power wireless charging zones without compromising vehicle range.

OEM Focus on Premium User Experience to Drive Market Expansion

Automakers are strategically positioning wireless charging as a key differentiator in vehicle trim packages, particularly in premium and luxury segments where the technology boasts over 85% adoption rates. The technology’s integration with infotainment systems creates a seamless ecosystem where device charging status is displayed on dashboard interfaces. This value-added functionality enhances the overall user experience while creating upsell opportunities for manufacturers.

➤ Leading automakers are now standardizing wireless charging across 92% of their mid-to-high trim models, reflecting the technology’s transition from luxury feature to mainstream expectation.

Furthermore, the convergence of wireless charging with other smart cabin technologies like device positioning detection and temperature-controlled charging zones is creating new revenue streams for Tier-1 suppliers and aftermarket providers alike.

MARKET RESTRAINTS

Compatibility Fragmentation and Standardization Challenges to Hinder Growth

The market faces significant headwinds from competing wireless charging standards and device compatibility issues. While the Qi standard dominates with 78% market penetration, proprietary fast-charging technologies from smartphone manufacturers create interoperability challenges. This fragmentation requires automotive systems to incorporate multiple charging protocols, increasing system complexity and cost. Consumers often experience inconsistent charging performance across different device models, creating dissatisfaction that slows broader adoption.

Thermal Management Constraints in Compact Designs Pose Technical Hurdles

As charging power increases to meet consumer demands, thermal management becomes critical in space-constrained automotive environments. Compact wireless chargers must dissipate heat effectively while maintaining spatial efficiency, requiring advanced materials and cooling solutions that can add 30-40% to component costs. These thermal challenges are particularly acute in vehicles parked in direct sunlight, where ambient temperatures can exacerbate heat buildup during charging cycles.

Additionally, the need for precise coil alignment in compact form factors creates engineering challenges, as even minor device misalignment can reduce charging efficiency by up to 60%, leading to consumer frustration and increased return rates.

MARKET CHALLENGES

High Development Costs and Extended Automotive Certification Cycles to Slow Innovation

The automotive industry’s stringent certification requirements present significant barriers to entry for new wireless charging technologies. The development cycle from prototype to production-ready systems often exceeds 24 months, with validation testing accounting for 35-45% of total development costs. This extended timeline conflicts with the rapid innovation cycles of consumer electronics, creating a technological lag where automotive solutions trail cutting-edge device capabilities by 12-18 months.

Other Challenges

Electromagnetic Interference Considerations

Wireless charging systems must navigate complex electromagnetic compatibility (EMC) regulations to prevent interference with vehicle electronics. The shielding requirements to meet these standards can increase system weight by 15-20% while reducing charging efficiency.

Aftermarket Installation Complexities

Retrofit solutions struggle with proper integration into existing vehicle architectures, often requiring professional installation that doubles the total ownership cost compared to factory-installed systems.

MARKET OPPORTUNITIES

Integration with Autonomous Vehicle Ecosystems to Unlock New Growth Avenues

The rise of autonomous driving presents transformative opportunities for in-vehicle wireless charging systems. As vehicles transition to Level 4 autonomy, interior redesigns will prioritize flexible charging surfaces throughout the cabin. This evolution will drive demand for multi-device charging solutions capable of powering smartphones, tablets, and wearable devices simultaneously. The integration of position-agnostic charging technologies will become critical as passengers freely reposition during autonomous journeys.

Emerging Bidirectional Power Transfer Technologies to Create Future Revenue Streams

Next-generation wireless systems capable of vehicle-to-device (V2D) and device-to-vehicle (D2V) power transfer are poised to redefine market potential. These systems would enable electric vehicles to charge portable devices during power outages or emergencies, adding utility that could command premium pricing. Pilot programs testing these technologies have shown 28% higher consumer willingness-to-pay compared to conventional charging solutions.

The development of standardized wireless charging ecosystems spanning automotive, home, and workplace environments will further accelerate adoption, creating seamless power availability that follows users across living spaces and mobility solutions.

AUTOMOTIVE COMPACT WIRELESS CHARGER MARKET TRENDS

Expansion of Electric Vehicle Infrastructure Fuels Wireless Charging Adoption

The global automotive compact wireless charger market is experiencing rapid growth, projected to grow at a CAGR of 27.9% from 2024 to 2032, reaching US$ 5.36 billion by the end of the forecast period. A key driver behind this surge is the accelerating adoption of electric vehicles (EVs) worldwide, with major automotive manufacturers integrating wireless charging technologies into new vehicle models. These compact solutions are increasingly embedded in center consoles, dashboard mounts, and even rear-seat pockets, eliminating the need for cumbersome cables while enhancing convenience and interior aesthetics.

Other Trends

Technological Advancements in Charging Efficiency

Recent advancements in electromagnetic induction and magnetic resonance technologies have significantly improved charging speeds and compatibility with multiple devices, making compact wireless charging solutions more appealing. The 15W segment dominates current sales, catering to mainstream smartphone users, while emerging 40W/50W fast-charging solutions are gaining traction in premium vehicle segments. Future developments are expected to focus on bidirectional charging capabilities, allowing vehicles to become mobile power banks for other devices during emergencies.

Growing Consumer Demand for Seamless In-Cabin Experiences

Consumer expectations around vehicle connectivity are reshaping the automotive interior landscape, with wireless charging becoming a standard expectation rather than a premium feature. Studies show that over 70% of new car buyers consider wireless charging a must-have feature in their next vehicle purchase. Automakers are responding by designing charging pads with advanced features like device detection, temperature regulation, and intelligent positioning systems to optimize charging performance without driver distraction. This trend is particularly strong in the passenger vehicle segment, where in-car entertainment and connectivity features are key purchase decision factors.

Increasing Competitive Landscape and Strategic Collaborations

The market is witnessing intense competition among key players like Continental, Qualcomm, and Aptiv, coupled with strategic partnerships between automakers and technology providers. Recent collaborations focus on developing universal charging standards that work across vehicle brands and mobile devices, addressing consumer frustrations with incompatible charging systems. With the top five manufacturers currently holding a significant market share, smaller players are focusing on niche applications in commercial vehicles and fleet management solutions where charging reliability is paramount for business operations.

COMPETITIVE LANDSCAPE

Key Industry Players

Automotive Wireless Charging Market Sees Intensified Competition as OEMs Push for Integration

The global automotive compact wireless charger market exhibits a fragmented yet rapidly evolving competitive landscape, with automotive suppliers, semiconductor makers, and specialized charging technology providers vying for market share. Continental AG leads the market with its vertically integrated solutions, combining expertise in automotive interiors with advanced wireless power transfer technology. The company recently unveiled a 50W fast-charging module compatible with both Qi and proprietary standards.

Qualcomm Technologies and Renesas Electronics have emerged as key technology enablers, providing reference designs and chipset solutions that power many OEM implementations. Their strong IP portfolios in wireless power transfer give them significant influence over industry standards and compatibility frameworks.

The market has seen growing participation from Chinese manufacturers like Hefei InvisPower and Shenzhen Sunway Communication, who are competing aggressively on price while rapidly improving technical capabilities. These players have particularly strong traction in domestic Chinese automotive markets where cost sensitivity remains high.

Established automotive suppliers Aptiv and Nidec are responding by expanding their product portfolios through strategic partnerships. Nidec’s acquisition of OMRON’s wireless power business in 2022 significantly bolstered its position, while Aptiv has focused on developing integrated human-machine interfaces that combine charging with other console functions.

List of Key Automotive Compact Wireless Charger Companies

- Continental AG (Germany)

- Laird Connectivity (U.K.)

- Qualcomm Technologies, Inc. (U.S.)

- Indie Semiconductor (U.S.)

- Aptiv PLC (Ireland)

- Hefei InvisPower (China)

- Huayang Electronics (China)

- Nidec Corporation (Japan)

- Renesas Electronics Corporation (Japan)

- Infineon Technologies (Germany)

- Shenzhen Sunway Communication (China)

Segment Analysis:

By Type

15W Segment Leads the Market Due to Widespread Compatibility with Consumer Devices

The market is segmented based on charging power into:

- 15W

- Widely adopted in mid-range vehicles

- 40/50W

- Emerging in premium vehicle segments

By Application

Passenger Cars Segment Dominates Owing to Higher Consumer Demand for Convenience Features

The market is segmented based on vehicle type into:

- Passenger Cars

- Subtypes: Sedans, SUVs, Hatchbacks

- Commercial Vehicles

- Subtypes: Light commercial vehicles, Heavy trucks

By Technology

Electromagnetic Induction Maintains Market Leadership Due to Cost-Effectiveness

The market is segmented based on charging technology into:

- Electromagnetic Induction

- Magnetic Resonance

By Vehicle Integration

Center Console Mounting Leads as Preferred Installation Location

The market is segmented based on installation location into:

- Center Console

- Armrest

- Dashboard

- Backseat

Regional Analysis: Automotive Compact Wireless Charger Market

Asia-Pacific

The Asia-Pacific region dominates the global automotive compact wireless charger market, driven by rapid automotive electrification, rising smartphone penetration, and strong manufacturing ecosystems. China leads adoption due to its 70% share of global electric vehicle production, while India’s rapidly expanding middle class increasingly demands premium in-car features. Governments across the region are pushing for smart mobility solutions, with Japan and South Korea focusing on integrating Qi-standard wireless charging across vehicle fleets. A key challenge remains price sensitivity among budget-conscious consumers, prompting manufacturers to develop cost-optimized 15W solutions. The region saw 42% year-over-year growth in wireless charging adoption in 2023.

North America

North America represents the most technologically advanced market for automotive wireless charging, with premium vehicle brands like Tesla, Ford, and GM integrating 15W-50W solutions as standard features. The U.S. accounts for 38% of regional market revenue, fueled by high disposable incomes and consumer preference for convenience technologies. Recent NHTSA guidelines on distracted driving are accelerating adoption, as wireless charging reduces cable clutter. However, the market faces regulatory fragmentation with competing standards (Qi vs. A4WP), creating integration challenges for automakers. The aftermarket segment shows particular strength, with brands like Belkin and Anker offering universal console-mounted solutions.

Europe

Europe’s stringent automotive safety standards and strong EV adoption (31.4% of 2023 car sales) create ideal conditions for wireless charging growth. Germany and the UK lead implementation, with BMW and Mercedes embedding 40W fast-charging pads in premium models. The EU’s push for standardized charging ecosystems under the CE4EU initiative ensures compatibility across devices and vehicles. Challenges include conservative consumer adoption rates in Eastern Europe and the need for thermal management solutions in compact vehicle designs. The commercial vehicle segment shows unexpected growth, with fleet operators using wireless charging to minimize driver distraction.

Middle East & Africa

This emerging market demonstrates unique characteristics with luxury vehicle penetration driving wireless charger adoption in Gulf states (UAE, Saudi Arabia), while economic constraints limit growth elsewhere. The lack of local standards bodies creates a fragmented landscape where manufacturers must support multiple protocols. Infrastructure limitations in Africa hinder widespread adoption, though South Africa shows promise as an automotive manufacturing hub. Market growth hinges on decreasing component costs and increasing localization of production.

South America

South America lags in adoption due to economic volatility and lower EV penetration (sub-5% market share). Brazil accounts for 63% of regional demand, primarily in premium imported vehicles. Gray market imports of aftermarket solutions pose quality control challenges, while currency fluctuations impact OEM integration plans. However, the region shows long-term potential with new automotive manufacturing investments in Argentina and Chile focused on connected vehicle technologies.

Report Scope

This market research report provides a comprehensive analysis of the global Automotive Compact Wireless Charger market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market was valued at USD 941 million in 2024 and is projected to reach USD 5,366 million by 2032, growing at a CAGR of 27.9%.

- Segmentation Analysis: Detailed breakdown by power capacity (15W, 40/50W), application (passenger cars, commercial vehicles), and end-user adoption trends to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa. The U.S. and China represent key growth markets.

- Competitive Landscape: Profiles of leading manufacturers including Continental, Qualcomm, Aptiv, Nidec and Renesas, covering their market share, product portfolios, and strategic developments.

- Technology Trends: Analysis of electromagnetic induction vs magnetic resonance charging, integration with vehicle infotainment systems, and efficiency improvements.

- Market Drivers & Restraints: Evaluation of factors including rising EV adoption, consumer demand for convenience, and challenges related to standardization and thermal management.

- Stakeholder Analysis: Strategic insights for automakers, component suppliers, technology providers, and investors regarding emerging opportunities.

The research employs primary interviews with industry experts and analysis of verified market data to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Automotive Compact Wireless Charger Market?

-> Automotive Compact Wireless Charger Market was valued at 941 million in 2024 and is projected to reach US$ 5366 million by 2032, at a CAGR of 27.9% during the forecast period.

Which key companies operate in this market?

-> Key players include Continental, Laird, Qualcomm, Aptiv, Nidec, Renesas, and Infineon, with the top five companies holding significant market share.

What are the key growth drivers?

-> Growth is driven by increasing smartphone penetration, demand for in-vehicle convenience features, and integration in electric vehicles.

Which region dominates the market?

-> Asia-Pacific shows the fastest growth, while North America and Europe lead in technology adoption.

What are the emerging trends?

-> Emerging trends include higher power charging (40W+), multi-device charging, and integration with advanced driver assistance systems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...