Automotive Antenna Module Market MARKET INSIGHTS

Global Automotive Antenna Module Market was valued at USD 1.5 billion in 2024 to USD 1.86 billion by 2032, exhibiting a CAGR of 3.6% during the forecast period.

Automotive antenna modules are electrical components designed for vehicle mounting that receive and transmit information signals. These systems consist of metallic conductor elements connected to receivers or transmitters via transmission lines. When current flows through the antenna, it generates oscillating electromagnetic fields that radiate as transverse waves into space, enabling wireless communication functions including radio reception, GPS navigation, cellular connectivity, and satellite services.

The market is experiencing steady growth driven by increasing vehicle connectivity requirements and rising consumer demand for advanced infotainment systems. Furthermore, the transition toward connected and autonomous vehicles is accelerating adoption of sophisticated antenna technologies capable of supporting multiple frequency bands simultaneously. Key players such as Laird, Harada, Yokowo, Continental, and TE Connectivity dominate the competitive landscape with comprehensive product portfolios addressing diverse automotive applications.

Automotive Antenna Module Market MARKET DRIVERS

Accelerated Adoption of Connected Car Technologies

The rapid proliferation of connected vehicles is a primary force propelling the Automotive Antenna Module Market forward. Modern vehicles now require robust connectivity for features such as telematics, over-the-air (OTA) updates, real-time navigation, and vehicle-to-everything (V2X) communication. Global connected car market is projected to grow significantly, creating sustained demand for advanced antenna systems that can handle multiple frequencies and complex signal processing.

Integration of Advanced Driver-Assistance Systems (ADAS)

Government mandates for safety features and growing consumer demand for semi-autonomous driving capabilities are driving the integration of ADAS. These systems rely heavily on precise data from GNSS (Global Navigation Satellite System) antennas for positioning, radar, and cellular communication, necessitating sophisticated antenna modules. The move toward higher levels of autonomy (Level 2+ and above) is a key trend, with the ADAS market expected to experience substantial growth in the coming years.

Furthermore, the increasing consumer expectation for uninterrupted in-vehicle infotainment (IVI) services, including high-definition video streaming and multi-device connectivity, compels automakers to incorporate more powerful and integrated antenna solutions to ensure a seamless user experience.

Automotive Antenna Module Market MARKET CHALLENGES

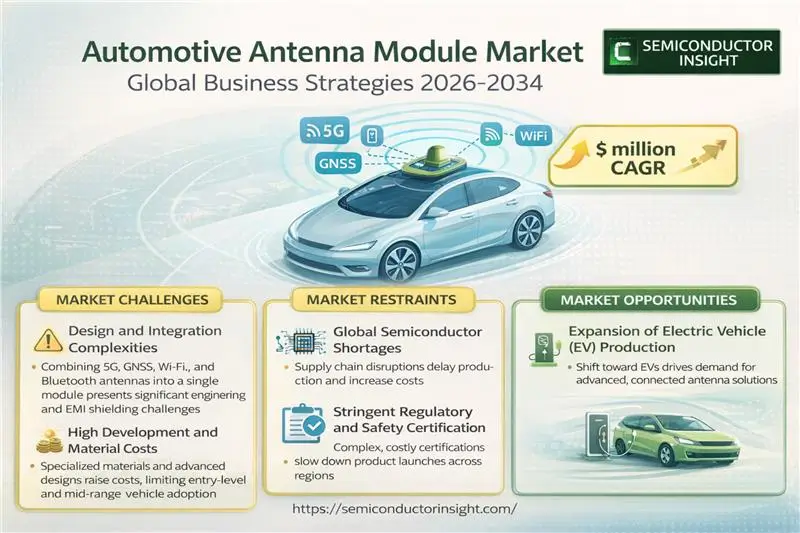

Design and Integration Complexities

Integrating multiple antennas for functions like 5G, GNSS, Wi-Fi, and Bluetooth into a single, aesthetically pleasing module without compromising performance presents a significant engineering hurdle. Shielding against electromagnetic interference (EMI) from the vehicle’s own electronic systems is a persistent challenge that can degrade signal quality.

Other Challenges

High Development and Material Costs

The use of specialized materials and the sophisticated design required for high-performance antenna modules contribute to elevated costs. This can limit adoption, particularly in the highly price-sensitive entry-level and mid-range vehicle segments.

Rapidly Evolving Connectivity Standards

The automotive industry must keep pace with the fast evolution of communication protocols (e.g., from 4G LTE to 5G NR). Designing modules that are both future-proof and cost-effective is a major challenge for suppliers and OEMs alike.

Automotive Antenna Module Market MARKET RESTRAINTS

Global Semiconductor Shortages and Supply Chain Disruptions

Automotive Antenna Module Market is highly dependent on the availability of specialized semiconductors and electronic components. The recent global chip shortage has highlighted the vulnerability of the supply chain, causing production delays and increased costs for vehicle manufacturers. This ongoing constraint continues to hinder the smooth growth of the market, as antenna modules are integral to a vehicle’s electronic architecture.

Stringent Regulatory and Safety Certification Processes

Antenna modules must comply with a complex web of regional and international regulations concerning radio frequency emissions, signal strength, and safety. Achieving certification across different markets (such as North America, Europe, and Asia-Pacific) is a time-consuming and costly process that can delay product launches and increase the overall cost of development for manufacturers.

Automotive Antenna Module Market MARKET OPPORTUNITIES

Expansion of Electric Vehicle (EV) Production

Global shift toward electric vehicles represents a significant growth avenue. EVs are inherently “connected” platforms that rely heavily on advanced antenna modules for battery management, remote diagnostics, and enhanced user interface systems. With EV sales projected to make up a substantial portion of new car sales within the decade, the demand for specialized antenna solutions is set to rise accordingly.

Emergence of Software-Defined Vehicles (SDVs)

The trend toward software-defined vehicles, where features and functionality can be updated via OTA updates, creates a need for highly capable and flexible antenna architectures. These systems require modules that can support dynamic reconfiguration and handle increasing data loads, opening up opportunities for innovation in antenna design and integration services.

Automotive Antenna Module Market Trends

Steady Market Growth Driven by Connectivity Demands

Global Automotive Antenna Module Market is on a trajectory of steady expansion, valued at approximately D 1500 million in 2024 and projected to reach D 1861 million by 2032, reflecting a Compound Annual Growth Rate (CAGR) of 3.6%. This sustained growth is fundamentally driven by the automotive industry’s accelerating shift towards connected, autonomous, shared, and electric (CASE) vehicles. Modern vehicles require robust and multifaceted antenna systems to support an increasing number of functions, including GPS navigation, cellular communication (4G/5G), satellite radio (SDARS), Wi-Fi, Bluetooth, and V2X (vehicle-to-everything) communication. The antenna module has evolved from a simple component for AM/FM radio reception into a critical, integrated system essential for safety, infotainment, and telematics.

Other Trends

Dominance of the Asia-Pacific Region and Passenger Vehicle Segment

The geographical and application landscapes of the market are clearly defined. The Asia-Pacific region is the largest market, accounting for approximately 55% of the global share. This dominance is fueled by high vehicle production volumes, particularly in China and Japan, and the rapid adoption of advanced automotive technologies by consumers. In terms of application, the passenger vehicle segment is the largest, holding a significant 67% share of the market. This is a direct result of the widespread integration of advanced connectivity features in personal vehicles. The commercial vehicle segment is also growing as fleet management and telematics become standard for logistics and transportation efficiency.

Consolidated Competitive Landscape and Product Type Evolution

The market features a consolidated competitive environment, with the top five manufacturers including Laird, Harada, Yokowo, Continental, and TE Connectivity collectively holding about 67% of the market share. This concentration underscores the importance of technological expertise, global supply chains, and strong relationships with major automotive OEMs. Regarding product types, the fin-type antenna module is the most prevalent, commanding a 39% market share. This design is widely adopted due to its aerodynamic properties and ability to seamlessly integrate multiple antenna elements for various signals into a single, aesthetically pleasing housing on the vehicle’s roof.

Integration and Miniaturization as Key Technological Drivers

A prominent trend shaping the future of antenna modules is the move towards greater integration and miniaturization. As the number of required communication bands increases, manufacturers are developing sophisticated modules that combine multiple antennas into compact units to save space and reduce complexity. This trend is critical for the design of electric vehicles, where aerodynamics and interior space are paramount. Furthermore, the development of “antenna-in-glass” and other hidden antenna solutions is gaining traction, aligning with consumer preferences for sleek vehicle designs without compromising on connectivity performance. The industry continues to face challenges related to signal interference and the need for materials that can withstand harsh automotive environments, driving ongoing innovation in design and componentry.

COMPETITIVE LANDSCAPE

Key Industry Players

A Concentrated Market Driven by Global Giants and Regional Specialists

Global Automotive Antenna Module Market is characterized by a high degree of consolidation, with the top five manufacturers collectively holding a significant share of approximately 67%. Technological expertise, extensive global supply chains, and strong relationships with major automotive OEMs are critical success factors in this market. Laird leads the market, renowned for its robust portfolio of antenna solutions catering to connected vehicles, including advanced shark-fin designs that integrate multiple functionalities like GPS, cellular, and satellite radio. Harada and Yokowo are other dominant players, with a strong heritage in antenna manufacturing and a significant market presence, particularly in the Asia-Pacific region which constitutes the largest market share of about 55%. Continental and TE Connectivity leverage their broader expertise in automotive electronics to provide highly integrated and reliable antenna modules that are essential for modern infotainment, telematics, and V2X communication systems.

A considerable number of manufacturers operate in specialized niches or regional markets, contributing to the diversity of the competitive landscape. Companies such as Northeast Industries, Ace Tech, and Fiamm have established strong positions by focusing on specific application segments, vehicle types, or geographical areas. For instance, Asian suppliers like Suzhong, Shenglu, Shien, and Tianye play a crucial role in the regional supply chain, offering cost-competitive solutions that support the massive passenger vehicle production base in China and neighboring countries. Other players like Tuko and Riof contribute to the ecosystem by providing specialized antenna components and modules, often competing on price and customization capabilities for specific OEM requirements. This structure ensures a dynamic market with options ranging from high-end, multi-functional integrated modules to more basic, application-specific antenna systems.

List of Key Automotive Antenna Module Companies Profiled

- Laird

- Harada

- Yokowo

- Continental AG

- TE Connectivity

- Northeast Industries

- Ace Tech

- Tuko

- Suzhong

- Shenglu

- Fiamm

- Riof

- Shien

- Tianye

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Fin Type antennas are the undisputed market leader, prized for their streamlined and aesthetically integrated design that aligns seamlessly with modern vehicle aerodynamics. This design dominance is reinforced by superior performance for modern telematics, GPS, and satellite radio applications. The integration capabilities of fin types offer automakers significant flexibility, allowing for placement that minimizes drag and preserves the vehicle’s design language. Screen type antennas are gaining relevance in premium electric vehicles where hidden, flush-mounted solutions are essential for achieving optimal aerodynamic efficiency, indicating a key area for future growth as vehicle electrification advances. |

| By Application |

|

Passenger Vehicle applications command the highest demand, fueled by the relentless consumer demand for advanced connectivity features, infotainment systems, and safety technologies like emergency calling (eCall). The sheer volume of passenger vehicle production globally ensures this segment’s dominance. The commercial vehicle segment represents a critical growth avenue, driven by the logistics and transportation industry’s need for robust fleet management, real-time telematics for route optimization, and regulatory mandates for safety and tracking. The growing sophistication of telematics in logistics is creating a highly specialized and demanding market for antenna modules designed for durability and reliable performance over long distances. |

| By End User |

|

OEM (Original Equipment Manufacturer) integration is the primary route to market, as antenna modules are critical, factory-installed components for modern vehicle functionality. This segment holds the strongest influence, with automakers driving specifications for performance, size, and integration. The aftermarket segment caters to upgrades, replacements, and the retrofitting of connectivity features into older vehicle models, serving a niche but stable demand. Fleet operators are emerging as a distinct and influential end-user group, requiring specialized antenna solutions for comprehensive telematics systems that monitor vehicle health, driver behavior, and logistics data, leading to custom integration requirements for large-scale vehicle deployments. |

| By Frequency Band |

|

Cellular (4G/5G) capable antenna modules are experiencing the most dynamic growth, propelled by the automotive industry’s push towards connected car ecosystems, over-the-air updates, and enhanced vehicle-to-everything (V2X) communication. The transition to 5G is particularly critical for supporting high-bandwidth applications like autonomous driving data exchange. GNSS antennas remain a foundational and highly stable segment, essential for navigation, location-based services, and security features in virtually every modern vehicle. High-frequency bands for traditional radio and television continue to be important but are increasingly being integrated into multi-functional antenna modules rather than operating as standalone systems. |

| By Vehicle Connectivity Level |

|

Premium Connectivity represents the core growth segment, encompassing features like embedded modems, Wi-Fi hotspots, and advanced infotainment that are becoming standard expectations in mid-to-high-tier vehicles. This segment drives demand for more complex, multi-band antenna systems. The Advanced/V2X Connectivity segment, while currently a smaller portion of the market, is the strategic focal point for innovation, demanding highly sophisticated antenna modules capable of supporting low-latency communication critical for safety and autonomous driving functions. Entry-level connectivity, covering basic radio and navigation, remains a significant volume driver, especially in emerging markets and economy vehicle segments, relying on cost-effective, single-function antenna solutions. |

Regional Analysis: Automotive Antenna Module Market

Asia-Pacific

The region’s extensive automotive and electronics manufacturing base provides a significant advantage. Proximity to suppliers of key components like printed circuit boards and semiconductors allows for efficient, integrated production of antenna modules. This robust supply chain ensures cost-effectiveness and rapid time-to-market for new technologies, meeting the high-volume demands of both domestic and international automakers.

Consumer demand for advanced connectivity features is exceptionally high in Asia-Pacific. Markets like China and South Korea are at the forefront of integrating telematics, satellite navigation, and high-speed data connectivity as standard features. This drives the need for multi-functional antenna modules capable of handling multiple frequency bands, including GPS, 4G/5G, and dedicated short-range communications.

National initiatives, such as China’s “New Infrastructure” plan that emphasizes 5G and IoT, directly benefit the automotive antenna market. Governments are actively investing in V2X communication infrastructure, creating a necessary ecosystem that incentivizes automakers to equip vehicles with compatible, advanced antenna systems, thereby stimulating market growth from the demand side.

There is a strong concentration of R&D centers from both automotive OEMs and technology firms focused on next-generation vehicles. This has led to significant innovation in antenna design, particularly for applications in electric vehicles and autonomous driving prototypes, where sleek, integrated antenna modules are essential for aesthetics and performance without compromising aerodynamic efficiency.

North America

The North American Automotive Antenna Module Market is characterized by high consumer demand for premium connectivity and safety features. Strong regulatory frameworks and high disposable income drive the adoption of vehicles equipped with advanced telematics systems, satellite radio, and emerging V2X technology. The presence of major technology companies and automotive OEMs fosters a competitive environment focused on innovation, particularly in integrated ‘shark-fin’ antenna designs that consolidate multiple functions. The region’s push towards autonomous vehicle development and the ongoing expansion of 5G networks create a sustained demand for sophisticated antenna modules capable of supporting high-data-rate communication and precise positioning required for semi-autonomous and fully autonomous driving functionalities.

Europe

Europe is a significant and mature Automotive Antenna Module Market, driven by stringent regulatory standards for vehicle safety and emissions, which increasingly incorporate eCall and other telematics mandates. The region’s strong premium and luxury automotive sector demands high-performance antenna systems for connectivity, digital radio, and navigation. European automakers are leaders in integrating antenna modules seamlessly into vehicle designs, focusing on aesthetic appeal. There is a growing emphasis on antenna systems for electric vehicles, where efficient cellular and navigation connectivity is crucial for battery management and route planning. Collaborative projects between automakers and telecom providers to test and deploy C-V2X technology across the continent are creating new opportunities for advanced antenna module integration.

South America

The South American Automotive Antenna Module Market is evolving, with growth primarily driven by the increasing penetration of mid-range vehicles featuring basic connectivity features. While adoption of advanced telematics is slower compared to other regions, there is a steady demand for antenna modules supporting FM/AM radio and GPS navigation. The market potential is linked to economic stability and infrastructure development, particularly the expansion of cellular networks in urban areas. Some countries are beginning to see the introduction of regulations similar to Europe’s eCall, which could spur future demand for more sophisticated antenna systems. The aftermarket segment also presents opportunities for antenna module upgrades as consumers seek better connectivity.

Middle East & Africa

The Middle East & Africa region presents a diverse landscape for the Automotive Antenna Module Market. In wealthier Gulf Cooperation Council countries, there is strong demand for luxury vehicles equipped with full suite connectivity features, driving the market for advanced antenna modules. In contrast, other parts of the region see demand focused on essential AM/FM radio and basic GPS functionality. The market growth is closely tied to economic conditions and the development of communication infrastructure. The hot and arid climate in many areas also influences antenna module design requirements, necessitating robust solutions capable of withstanding extreme environmental conditions while maintaining performance reliability for navigation and communication systems.

Report Scope

This market research report provides a comprehensive analysis of the Automotive Antenna Module Market , covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Automotive Antenna Module Market?

-> Automotive Antenna Module Market was valued at USD 1.5 billion in 2024 to USD 1.86 billion by 2032, exhibiting a CAGR of 3.6% during the forecast period.

Which key companies operate in Automotive Antenna Module Market?

-> Key players include Laird, Harada, Yokowo, Continental, and TE Connectivity, among others. Global top 5 manufacturers hold a share of about 67%.

What are the key growth drivers?

-> Key growth drivers include the increasing integration of advanced connectivity features in vehicles, rising demand for passenger vehicles, and technological advancements in telecommunication systems.

Which region dominates the market?

-> Asia Pacific is the largest market, with a share of about 55%.

What are the emerging trends?

-> Emerging trends include the development of advanced fin-type antenna modules, integration of multiple antennas for diverse functions, and the growing application in commercial vehicles.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...