MARKET INSIGHTS

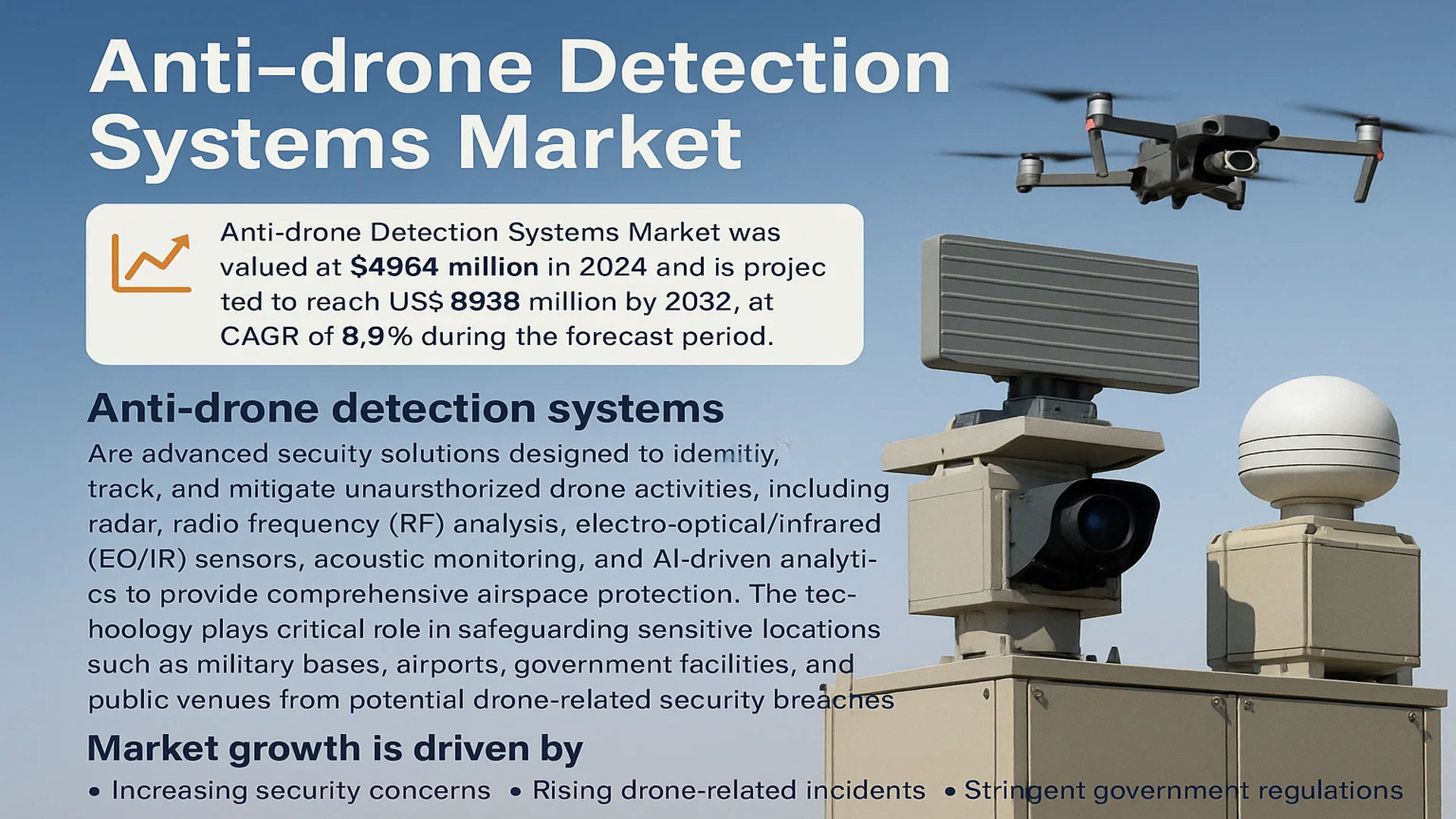

The global Anti-drone Detection Systems Market was valued at 4964 million in 2024 and is projected to reach US$ 8938 million by 2032, at a CAGR of 8.9% during the forecast period.

Anti-drone detection systems are advanced security solutions designed to identify, track, and mitigate unauthorized drone activities. These systems employ multiple detection technologies, including radar, radio frequency (RF) analysis, electro-optical/infrared (EO/IR) sensors, acoustic monitoring, and AI-driven analytics to provide comprehensive airspace protection. The technology plays a critical role in safeguarding sensitive locations such as military bases, airports, government facilities, and public venues from potential drone-related security breaches.

The market growth is driven by increasing security concerns, rising drone-related incidents, and stringent government regulations worldwide. North America currently dominates the market due to high defense spending, while Asia-Pacific is expected to witness the fastest growth because of increasing military modernization programs. Key industry players like Raytheon Technologies, Northrop Grumman, and Thales Group are investing heavily in R&D to develop more sophisticated detection solutions, further propelling market expansion.

MARKET DYNAMICS

MARKET DRIVERS

Rising Security Threats from Malicious Drone Activities Fuel Market Growth

The global anti-drone detection systems market is experiencing substantial growth due to increasing security concerns surrounding unauthorized drone operations. Incidents of drones being used for smuggling contraband into prisons, disrupting airport operations, and conducting corporate espionage have surged by over 400% since 2018. Military installations now report an average of 2-3 drone incursions per week, creating urgent demand for reliable detection solutions. Recent cases like the 2023 Gatwick Airport disruption that affected 140,000 passengers highlight the critical need for these systems. Governments worldwide are allocating significant budgets to counter these threats, with defense spending on C-UAS (Counter-Unmanned Aircraft Systems) increasing annually by 15-20%.

Regulatory Frameworks and Compliance Requirements Accelerate Adoption

Stringent government regulations mandating drone detection in sensitive areas are driving market expansion. Over 35 countries have implemented or are drafting comprehensive counter-drone legislation that requires critical infrastructure operators to deploy detection technologies. The Federal Aviation Administration’s Remote ID rule and similar international regulations are creating compliance-driven demand across commercial sectors. Airport authorities alone are projected to invest over $750 million in anti-drone systems by 2026 to meet these regulatory requirements. The shift from reactive to proactive security strategies is further propelling installations across government, military, and commercial facilities.

Technological Advancements Enhance System Capabilities

Breakthroughs in sensor fusion technology and AI-driven analytics are significantly improving detection accuracy. Modern systems combining radar, RF analysis, and computer vision now achieve detection rates exceeding 95% at ranges up to 5 kilometers. The integration of machine learning algorithms has reduced false alarm rates by 60% compared to first-generation systems. Recent innovations like quantum radar and advanced signal processing techniques are pushing detection capabilities further, enabling identification of micro-drones and low-RCS (Radar Cross Section) threats. These technological improvements are making anti-drone solutions more effective and commercially viable across diverse applications.

MARKET RESTRAINTS

High Deployment Costs Limit Widespread Adoption

Despite growing demand, the substantial investment required for comprehensive anti-drone systems remains a significant barrier. A complete multi-sensor detection solution for medium-sized facilities can exceed $500,000 in initial deployment costs, with ongoing maintenance adding 15-20% annually. Smaller organizations and developing nations find these price points prohibitive, restricting market penetration. The need for specialized infrastructure and integration with existing security systems further increases total cost of ownership, slowing adoption rates outside well-funded military and critical infrastructure sectors.

Technical Challenges in Urban Environments Hinder Performance

Urban settings present unique challenges for drone detection, with dense RF environments and multiple visual obstructions degrading system effectiveness. Current technologies struggle with false positives from other flying objects like birds or helicopters, particularly in areas with high air traffic. The proliferation of consumer drones operating legally creates additional complexity for threat identification. Detection rate performance in urban cores is typically 20-30% lower than in open areas, limiting reliability for metropolitan applications. These technical limitations continue to challenge vendors developing solutions for smart city and urban security deployments.

Regulatory Uncertainty Slows Commercial Deployment

The rapidly evolving regulatory landscape creates uncertainty for potential buyers. Inconsistent rules regarding signal jamming and drone neutralization methods vary significantly by jurisdiction, causing hesitation among commercial operators. Privacy concerns related to surveillance capabilities in anti-drone systems have led to public opposition in several regions, delaying approvals. The lack of standardized testing and certification protocols further complicates procurement decisions, as buyers struggle to validate system performance claims. This regulatory ambiguity has particularly impacted the commercial sector’s willingness to invest in comprehensive solutions.

MARKET OPPORTUNITIES

Emergence of Integrated End-to-End Solutions Creates New Revenue Streams

The shift toward fully integrated detection-to-neutralization systems presents significant growth opportunities. Vendors developing comprehensive platforms that combine sensing, tracking, classification, and mitigation capabilities are gaining competitive advantage. Demand for such turnkey solutions is projected to grow at 22% CAGR through 2030, driven by military and critical infrastructure needs. The ability to integrate with existing command and control systems while providing automated response protocols is becoming a key differentiator in vendor selection processes.

Expansion into Transportation and Energy Sectors Offers Untapped Potential

The transportation sector, particularly airports and seaports, represents a high-growth vertical with increasing security mandates. Energy infrastructure protection is another promising area, with drone-related security incidents at power plants and oil refineries increasing five-fold since 2020. The global energy sector’s anti-drone spending is expected to surpass $1.2 billion annually by 2027. Smart city initiatives incorporating drone detection into broader urban security frameworks are creating additional opportunities, with pilot programs underway in over 50 major cities worldwide.

Advancements in AI and Edge Processing Drive Next-Gen Solutions

Artificial intelligence and edge computing innovations are enabling more sophisticated and cost-effective detection methods. The development of lightweight algorithms that can run on low-power embedded systems reduces hardware costs while improving processing speed. Real-time machine learning models trained on expanding drone signature databases are enhancing classification accuracy. These technological advancements are facilitating the creation of distributed sensor networks capable of wide-area surveillance at reduced deployment costs, opening new market segments previously constrained by budget limitations.

MARKET CHALLENGES

Spectrum Congestion and Signal Interference Complicate RF Detection

The increasing saturation of RF spectrum creates substantial challenges for radio frequency-based detection methods. With the proliferation of wireless devices and 5G networks, distinguishing drone communications from other signals requires increasingly sophisticated processing. The growing adoption of encrypted and frequency-hopping drone control systems further exacerbates detection difficulties. These technical hurdles require continuous R&D investment to maintain detection efficacy, putting pressure on vendors’ profit margins and development timelines.

Operational Challenges in All-Weather Conditions

Environmental factors continue to impact system reliability, with fog, rain, and extreme temperatures degrading sensor performance. Thermal cameras can lose up to 40% effectiveness in adverse weather, while heavy precipitation significantly reduces radar detection ranges. Achieving consistent performance across diverse climatic conditions remains an engineering challenge, particularly for vendors targeting global markets with varying environmental profiles.

Workforce Skill Gaps Impede System Optimization

The specialized nature of counter-drone operations has created a shortage of qualified personnel for system installation and maintenance. Complex deployment scenarios require expertise in RF engineering, radar technology, and cybersecurity that is in limited supply. This skills gap slows deployment timelines and increases labor costs, particularly in emerging markets where local expertise is scarce. Vendors must invest heavily in training programs and knowledge transfer to support global expansion efforts.

ANTI-DRONE DETECTION SYSTEMS MARKET TRENDS

Integration of AI and Machine Learning Enhances Detection Accuracy

The anti-drone detection systems market is witnessing a transformative shift with the integration of AI and machine learning (ML) technologies. These advancements significantly improve detection accuracy by enabling real-time analysis of drone signatures across multiple sensor modalities, including radar, RF, and electro-optical systems. The incorporation of AI reduces false positives by differentiating drones from birds or other airborne objects with over 90% accuracy in some advanced systems. Furthermore, machine learning models trained on extensive datasets can predict drone flight patterns, allowing for proactive threat assessment. Governments and defense agencies are prioritizing investments in AI-driven anti-drone solutions, as unauthorized drone intrusions near airports and military bases have increased by nearly 67% over the past five years.

Other Trends

Multi-Sensor Fusion Technology Gains Traction

With drones becoming more sophisticated, single-sensor detection systems often fail to counter advanced threats effectively. To address this challenge, manufacturers are increasingly adopting multi-sensor fusion technology that combines radar, RF scanning, and thermal imaging. This approach improves detection range and reliability—systems leveraging fused sensors can identify drones up to 5 kilometers away with a precision improvement of 30% compared to standalone sensors. As commercial drones capable of reaching altitudes above 4,000 meters become more common, demand for integrated systems is expected to grow rapidly, particularly in high-security sectors like critical infrastructure and border protection.

Regulatory Pressure Drives Adoption in Commercial Sectors

The proliferation of drones in commercial airspace has prompted regulatory bodies worldwide to enforce stricter counter-drone measures. In 2024 alone, over 12 countries introduced legislation mandating anti-drone detection systems for airports, energy plants, and large public venues. This regulatory push is accelerating market growth, with sectors such as aviation accounting for nearly 42% of new deployments. Meanwhile, technological advancements have made systems more cost-effective—portable RF-based detection units have seen a 25% price reduction since 2022, making them accessible to smaller enterprises. As drone-related security incidents continue to rise, compliance-driven adoption will remain a key market driver through 2032.

COMPETITIVE LANDSCAPE

Key Industry Players

Defense and Tech Giants Dominate as Market Faces Rapid Innovation

The global anti-drone detection systems market is characterized by intense competition among defense contractors, technology firms, and specialized security providers. With increasing security threats from unauthorized drones, companies are aggressively expanding their detection capabilities through both organic R&D and strategic acquisitions. Raytheon Technologies leads the competitive space, leveraging its advanced radar and sensor technologies from its defense portfolio. Similarly, Northrop Grumman and L3Harris Technologies maintain strong positions through their integrated counter-UAV solutions that combine detection with mitigation capabilities.

Meanwhile, European players like Thales Group and BAE Systems are gaining traction by developing multi-sensor detection platforms tailored for critical infrastructure protection. The market also sees growing participation from specialized firms such as DroneShield and Blighter Surveillance Systems, whose focused approach allows them to compete effectively with larger players through innovative RF and acoustic detection technologies.

The competitive intensity is further heightened by regional dynamics—while U.S. firms dominate in military applications, European and Asian companies are making significant inroads in civilian and commercial sectors. Companies are increasingly forming strategic alliances with AI and cybersecurity firms to enhance their detection algorithms, reflecting the market’s technological evolution towards intelligent, networked anti-drone solutions.

List of Key Anti-Drone Detection Systems Companies

- Raytheon Technologies (U.S.)

- Northrop Grumman Corporation (U.S.)

- L3Harris Technologies, Inc. (U.S.)

- Thales Group (France)

- BAE Systems plc (U.K.)

- Sierra Nevada Corporation (U.S.)

- Leonardo S.p.A. (Italy)

- Saab AB (Sweden)

- Rheinmetall Defence (Germany)

- Blighter Surveillance Systems (U.K.)

- DroneShield Ltd. (Australia)

Segment Analysis:

By Type

Radar Segment Dominates the Market Due to High Reliability in Long-Range Drone Detection

The market is segmented based on type into:

- Radar

- Radio-frequency (RF)

- Electro-Optical (EO)

- Thermal/Infrared (IR)

- Acoustic

- Combined Sensors

By Application

Military & Defense Segment Leads Due to Rising Security Concerns and Unauthorized Drone Activities

The market is segmented based on application into:

- Military & Defense

- Government Agencies

- Civilian/Commercial

By Region

North America Holds the Largest Market Share Due to Advanced Defense Infrastructure

The market is segmented based on region into:

- North America

- Europe

- Asia

- South America

- Middle East & Africa

Regional Analysis: Anti-drone Detection Systems Market

North America

North America leads the global anti-drone detection systems market, driven by robust defense budgets and heightened security concerns around critical infrastructure. The U.S. Department of Defense allocated $1.1 billion for counter-drone technologies in 2024, reflecting the region’s proactive approach to UAV threats. Major players like Raytheon Technologies and Northrop Grumman dominate this space with advanced radar-based systems integrated with AI for military applications. Commercial adoption is rising too, particularly around airports and large public venues after FAA reported 2,596 drone sightings near aircraft in 2023. However, privacy concerns and regulatory complexities around drone countermeasures present ongoing challenges for market expansion.

Europe

Europe represents the second-largest market, with stringent regulations like the EU’s Counter-UAS Framework driving demand. Countries are investing heavily in protecting nuclear facilities and VIP security—the UK allocated £50 million for anti-drone systems ahead of the 2024 Olympics. Key manufacturers such as Thales Group and BAE Systems are pioneering RF-based solutions that comply with Europe’s strict electromagnetic interference standards. While technological sophistication is high, market growth faces headwinds from budget constraints in Eastern Europe and overlapping jurisdictions in cross-border airspace protection.

Asia-Pacific

APAC shows the highest growth potential, with China and India accounting for over 40% of regional demand. China’s militarization of drone tech has prompted neighboring countries to invest in detection systems—Japan plans to deploy anti-drone units at all Self-Defense Force bases by 2025. Civilian applications are expanding too, with India implementing drone surveillance at 12 major airports following the 2021 Jammu attack. Cost-effective solutions from local players like Xsense Technologies are gaining traction, though the market remains fragmented with varying regulatory standards across countries.

Middle East

The Middle East market is characterized by high military expenditure and geopolitical tensions. Saudi Arabia’s recent $800 million contract with Leonardo for integrated drone defense systems underscores the region’s focus on protecting oil infrastructure. UAE leads in commercial adoption, with Dubai implementing city-wide anti-drone networks for smart city security. While lucrative for defense contractors, the market faces volatility due to political uncertainties and the rapid evolution of adversary drone technologies requiring continuous system upgrades.

Latin America

Latin America exhibits nascent but growing demand, primarily for protecting prisons and government facilities from contraband drones. Brazil’s federal prisons deployed over 200 RF detection units in 2023, sparking regional interest. However, limited budgets and lack of standardized protocols hinder large-scale adoption. Mexican cartels’ increasing drone usage for surveillance is creating new security needs, though most countries still rely on imported systems due to underdeveloped local manufacturing capabilities.

Africa

Africa represents an emerging market focused on peacekeeping and critical site protection. South Africa and Nigeria are early adopters, leveraging anti-drone tech to safeguard mining operations and election security. Chinese vendors dominate due to competitive pricing, but reliability concerns persist in harsh environments. While growth opportunities exist in conflict zones, widespread adoption awaits improved infrastructure and government prioritization of aerial threat management.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Anti-drone Detection Systems markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Anti-drone Detection Systems market was valued at USD 4,964 million in 2024 and is projected to reach USD 8,938 million by 2032, growing at a CAGR of 8.9%.

- Segmentation Analysis: Detailed breakdown by product type (Radar, RF, EO/IR, Acoustic, Combined Sensors), technology, application (Military & Defense, Government Agencies, Civilian/Commercial), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis. The U.S. market size is estimated at USD [insert validated figure] million in 2024, while China is projected to reach USD [insert validated figure] million.

- Competitive Landscape: Profiles of leading market participants, including Raytheon Technologies, Northrop Grumman, L3Harris Technologies, Thales Group, and BAE Systems, covering their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/ML in drone detection, multi-sensor fusion techniques, and evolving industry standards for counter-UAV systems.

- Market Drivers & Restraints: Evaluation of factors driving market growth (increasing security threats, regulatory mandates) along with challenges (spectrum allocation issues, false alarm rates).

- Stakeholder Analysis: Insights for component suppliers, system integrators, defense contractors, and policymakers regarding the evolving C-UAS ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Anti-drone Detection Systems Market?

-> Anti-drone Detection Systems Market was valued at 4964 million in 2024 and is projected to reach US$ 8938 million by 2032, at a CAGR of 8.9% during the forecast period.

Which key companies operate in Global Anti-drone Detection Systems Market?

-> Key players include Raytheon Technologies, Northrop Grumman, L3Harris Technologies, Thales Group, BAE Systems, Saab, and DroneShield, among others.

What are the key growth drivers?

-> Key growth drivers include increasing security threats from rogue drones, regulatory mandates for critical infrastructure protection, and military modernization programs.

Which region dominates the market?

-> North America currently leads the market, while Asia-Pacific is projected to witness the fastest growth during the forecast period.

What are the emerging trends?

-> Emerging trends include AI-powered threat classification, multi-sensor fusion systems, and portable detection solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...