MARKET INSIGHTS

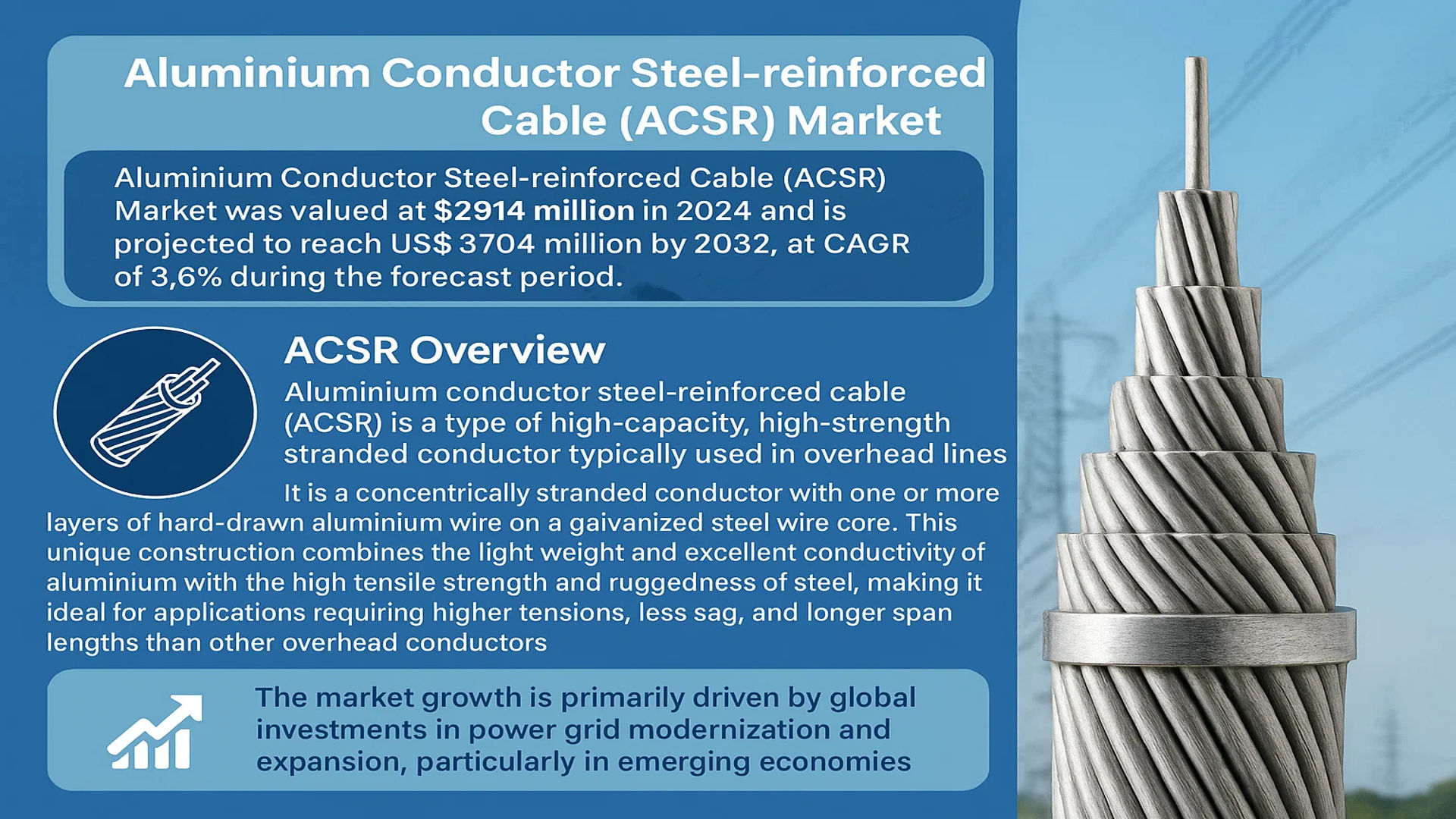

The global Aluminium Conductor Steel-reinforced Cable (ACSR) Market was valued at 2914 million in 2024 and is projected to reach US$ 3704 million by 2032, at a CAGR of 3.6% during the forecast period.

Aluminium conductor steel-reinforced cable (ACSR) is a type of high-capacity, high-strength stranded conductor typically used in overhead power lines. It is a concentrically stranded conductor with one or more layers of hard-drawn aluminium wire on a galvanized steel wire core. This unique construction combines the light weight and excellent conductivity of aluminium with the high tensile strength and ruggedness of steel, making it ideal for applications requiring higher tensions, less sag, and longer span lengths than other overhead conductors.

The market growth is primarily driven by global investments in power grid modernization and expansion, particularly in emerging economies. However, the growth pace is tempered by competition from alternative technologies and the mature nature of the market in developed regions. China dominates the global landscape, accounting for over 55% of the market share, followed by Europe and North America. In terms of product type, ACSR/AW (Aluminum Conductor Aluminum-Clad Steel-Reinforced) is the largest segment, holding approximately 40% of the market, due to its enhanced corrosion resistance. The primary application remains in primary and secondary distribution conductors, which is the largest end-use segment.

MARKET DYNAMICS

MARKET DRIVERS

Global Expansion of Power Grid Infrastructure to Drive ACSR Demand

The global push for electrification and grid modernization is significantly driving the ACSR market. With over 55% of the market concentrated in Asia, particularly China, massive investments in power infrastructure are fueling demand. China’s State Grid Corporation has committed to investing more than 65 billion dollars annually in grid infrastructure through 2025, creating substantial opportunities for ACSR manufacturers. The technology’s ability to provide higher tensions, less sag, and longer span lengths makes it ideal for both new installations and upgrades of existing power networks. Furthermore, the increasing demand for reliable electricity in emerging economies, coupled with urbanization trends, necessitates robust overhead transmission systems where ACSR conductors excel due to their proven performance and cost-effectiveness.

Renewable Energy Integration to Boost Market Growth

The global transition toward renewable energy sources is creating substantial demand for ACSR cables. Wind and solar farms, often located in remote areas, require extensive transmission networks to connect to main grids. ACSR’s superior strength-to-weight ratio and durability make it particularly suitable for these applications, especially in challenging terrains and harsh environmental conditions. The increasing installation of renewable energy capacity, projected to grow by over 280 gigawatts annually worldwide, directly correlates with the need for reliable overhead conductors. Additionally, grid interconnection projects between countries and regions are adopting ACSR technology for long-distance power transmission, further driving market expansion.

Technological Advancements in Conductor Design to Enhance Market Position

Continuous innovation in ACSR conductor design is strengthening its market position. Manufacturers are developing advanced variants with improved corrosion resistance and higher performance characteristics. The ACSR/AW segment, representing approximately 40% of the market, demonstrates how aluminum-clad steel reinforcement provides enhanced durability in corrosive environments. Recent developments include conductors with trapezoidal wire configurations that offer better packing density and reduced diameter, leading to improved electrical performance. These technological improvements are particularly valuable for extra-high voltage applications where corona effects and electrical losses are critical considerations. The ongoing research and development efforts by major players ensure that ACSR technology remains competitive against alternative conductor types.

Furthermore, the increasing focus on grid resilience in the face of climate change and extreme weather events is driving demand for robust transmission infrastructure. ACSR conductors, with their proven reliability across diverse environmental conditions, are becoming the preferred choice for utilities seeking to enhance their grid’s resilience capabilities.

MARKET RESTRAINTS

Volatility in Raw Material Prices to Constrain Market Growth

The ACSR market faces significant challenges from fluctuations in aluminum and steel prices. Aluminum prices have experienced volatility of up to 30% annually, directly impacting manufacturing costs and profit margins. Since aluminum constitutes the primary conductive material in ACSR cables, representing approximately 60-90% of the conductor cross-section depending on the specific type, price instability creates uncertainty in project budgeting and procurement decisions. Steel prices have similarly shown considerable volatility, affecting the core reinforcement component. This price instability often leads to delayed infrastructure projects as utilities and contractors wait for more favorable material pricing conditions, thereby restraining market growth.

Increasing Competition from Alternative Technologies to Limit Market Expansion

The ACSR market faces growing competition from emerging conductor technologies that offer improved performance characteristics. High-temperature low-sag conductors, composite core conductors, and other advanced designs are gaining traction in specific applications where their superior electrical or mechanical properties provide advantages over traditional ACSR. While ACSR maintains dominance in standard applications, these alternative technologies are capturing market share in specialized segments, particularly in projects requiring higher capacity or reduced sag characteristics. The development of carbon fiber composite core conductors and other innovative designs represents a technological challenge to the established ACSR market position, potentially limiting growth opportunities in premium application segments.

Environmental and Regulatory Challenges to Impact Market Dynamics

Environmental considerations and regulatory requirements are creating challenges for the ACSR market. The production of aluminum, a key component in ACSR conductors, is energy-intensive and subject to increasing environmental regulations regarding emissions and energy consumption. Additionally, visual impact concerns and right-of-way issues for overhead transmission lines are leading to growing preference for underground cabling in certain regions, particularly in densely populated areas and scenic locations. While underground solutions are significantly more expensive, regulatory pressures and public opposition to new overhead lines are creating barriers to market growth. These factors are particularly pronounced in developed markets where environmental regulations are stringent and public opposition to new infrastructure projects is more organized.

MARKET CHALLENGES

Technical Limitations in Extreme Environmental Conditions to Challenge Market Adoption

While ACSR conductors demonstrate excellent performance in most conditions, they face challenges in extreme environmental situations. In coastal areas with high salt content, corrosion can become a significant issue despite protective measures such as greasing and aluminum cladding. The combination of moisture, salt, and industrial pollutants can accelerate degradation, reducing the operational lifespan of the conductors. In extremely cold climates, ice accumulation on conductors can lead to excessive loading and potential structural failures. These environmental challenges require additional protective measures and more frequent maintenance, increasing the total cost of ownership and creating adoption barriers in regions with particularly harsh environmental conditions.

Other Challenges

Supply Chain Complexities

The global supply chain for ACSR manufacturing involves multiple raw material sources and processing stages, creating vulnerabilities to disruptions. Geographic concentration of aluminum production and processing facilities, coupled with logistics challenges, can lead to supply inconsistencies and extended lead times. These complexities are exacerbated by trade policies and tariffs that affect the movement of raw materials and finished products across borders.

Technical Skill Shortages

The industry faces challenges in maintaining adequate technical expertise for both manufacturing and installation. Proper installation of ACSR conductors requires specialized knowledge of tensioning, sagging, and hardware selection. The aging workforce in many developed markets and the need for knowledge transfer to new technicians create operational challenges that can affect project timelines and quality standards.

MARKET OPPORTUNITIES

Modernization of Aging Grid Infrastructure to Create Significant Growth Opportunities

The global need for upgrading aging power infrastructure presents substantial opportunities for the ACSR market. Many developed countries are facing the challenge of outdated transmission networks that require replacement or reinforcement. In North America and Europe, a significant portion of the existing grid infrastructure is approaching or has exceeded its designed lifespan, creating a substantial replacement market. ACSR conductors, with their proven reliability and cost-effectiveness, are well-positioned to capture this replacement demand. The opportunity is particularly significant in urban areas where increased power density requirements necessitate upgrades to higher capacity conductors while maintaining existing tower structures.

Expansion in Emerging Markets to Drive Future Growth

Rapid economic development in emerging markets creates extensive opportunities for ACSR deployment. Countries across Southeast Asia, Africa, and South America are investing heavily in electrification projects to support economic growth and improve living standards. The relatively low cost of ACSR technology compared to alternative solutions makes it particularly attractive for these markets where budget constraints are often a consideration. The ongoing urbanization trends in these regions, with millions of people moving to cities annually, require substantial investments in power distribution infrastructure where ACSR conductors play a crucial role in both primary and secondary distribution networks.

Technological Innovation and Product Development to Open New Application Areas

Continuous innovation in ACSR design and manufacturing processes is creating opportunities in new application segments. Developments in corrosion-resistant coatings, improved strength alloys, and enhanced manufacturing techniques are expanding the suitability of ACSR conductors for challenging environments. The integration of smart grid technologies and monitoring systems with transmission infrastructure presents additional opportunities for value-added products. Manufacturers that can develop ACSR conductors with integrated monitoring capabilities or improved environmental performance are likely to capture premium market segments and differentiate themselves in a competitive marketplace.

ALUMINIUM CONDUCTOR STEEL-REINFORCED CABLE (ACSR) MARKET TRENDS

Global Grid Modernization and Renewable Energy Integration Driving Market Expansion

The global push for grid modernization and the integration of renewable energy sources are primary catalysts for the ACSR market’s steady growth. Aging power infrastructure in developed economies necessitates replacement with more robust and efficient conductors, while emerging economies are rapidly expanding their electricity grids to support industrialization and urbanization. The global ACSR market, valued at approximately $2.9 billion in 2024, is projected to reach $3.7 billion by 2032, reflecting a compound annual growth rate of 3.6%. This growth is intrinsically linked to massive investments in the power sector; for instance, global investment in electricity networks surpassed $300 billion annually in recent years. ACSR cables are particularly favored for long-span transmission projects connecting remote wind and solar farms to the main grid because of their superior strength-to-weight ratio and proven reliability in diverse environmental conditions.

Other Trends

Technological Advancements in Conductor Design

While the fundamental design of ACSR is well-established, continuous innovation in material science and manufacturing is enhancing product performance. There is a growing trend towards developing conductors with higher aluminum content and specialized steel cores to achieve greater ampacity without compromising mechanical strength. Manufacturers are also focusing on advanced corrosion protection systems, such as grease-infused cores and aluminum-clad steel wires (ACSR/AW), to extend the operational lifespan of cables in coastal and high-pollution areas. These improvements are crucial for reducing lifecycle costs and increasing the resilience of power networks against extreme weather events, a key consideration for utilities worldwide.

Asia-Pacific Dominance and Regional Infrastructure Development

The Asia-Pacific region, led by China, is the undisputed epicenter of the ACSR market, accounting for over 55% of global demand. This dominance is fueled by unprecedented investments in national power infrastructure. China’s State Grid Corporation, for example, has been consistently executing ultra-high-voltage (UHV) transmission projects that require vast quantities of high-strength conductors like ACSR. Similarly, countries like India are aggressively expanding their grid reach through initiatives like the ‘One Nation, One Grid’ project, which aims to integrate regional power networks into a national grid. This regional concentration of demand means that manufacturing capacity and technological development are also heavily focused in Asia, with Chinese players holding a significant share of the global production landscape. This trend is expected to persist as Southeast Asian nations also ramp up their power generation and transmission capabilities to support economic growth.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Capacity Expansion and Technological Innovation Drive Market Leadership

The global Aluminium Conductor Steel-reinforced Cable (ACSR) market exhibits a semi-consolidated competitive structure, characterized by the presence of several established international players alongside numerous regional manufacturers. This dynamic is largely driven by the extensive infrastructure demands across power transmission and distribution sectors worldwide. The market’s top five players collectively held a share exceeding 15% in 2024, indicating a competitive environment where no single entity dominates, but where scale, technological capability, and geographic reach are critical determinants of success.

Nexans S.A. (France) stands as a preeminent force in the global ACSR landscape, leveraging its extensive portfolio of high-voltage and extra-high-voltage conductors and a robust manufacturing footprint across Europe, North America, and Asia. The company’s leadership is further cemented by continuous investment in research and development, focusing on enhancing conductor efficiency and durability for demanding applications like long-span river crossings. Similarly, Southwire Company, LLC (U.S.) maintains a formidable position, particularly in the North American market, due to its integrated operations—from raw material processing to finished cable production—ensuring consistent quality and supply chain reliability for utility clients.

Apar Industries Limited (India) and Hengtong Group (China) have emerged as dominant players, capitalizing on the massive infrastructure development and grid modernization projects within the Asia-Pacific region, which accounts for over 55% of the global market. Their growth is propelled by cost-competitive manufacturing and strong relationships with national utility providers. These companies are aggressively pursuing geographical expansions and product diversification to capture a larger share of the international market.

Meanwhile, other significant participants like General Cable (now part of Prysmian Group), Sumitomo Electric Industries (Japan), and LS Cable & System (South Korea) are strengthening their positions through strategic mergers and acquisitions, technological partnerships, and the development of advanced ACSR variants such as ACSR/AW (Aluminum-Clad Steel-Reinforced) for improved corrosion resistance. Their focus on innovation and sustainability is expected to be a key differentiator, ensuring continued growth and adaptation to evolving global energy infrastructure needs.

List of Key Aluminium Conductor Steel-reinforced Cable (ACSR) Companies Profiled

- Nexans S.A. (France)

- Southwire Company, LLC (U.S.)

- General Cable (Part of Prysmian Group) (U.S.)

- Apar Industries Limited (India)

- Hengtong Group Co., Ltd. (China)

- Sumitomo Electric Industries, Ltd. (Japan)

- LS Cable & System Ltd. (South Korea)

- Tongda Cable Co., Ltd. (China)

- Hanhe Cable Co., Ltd. (China)

- Saudi Cable Company (Saudi Arabia)

- K M Cables & Conductors (India)

Segment Analysis:

By Type

ACSR/AW Segment Dominates the Market Due to Superior Corrosion Resistance and Extended Lifespan

The market is segmented based on type into:

- ACSR – Aluminum Conductor Steel-Reinforced

- ACSR/AW – Aluminum Conductor Aluminum-Clad Steel-Reinforced

- ACSR/TW – Trapezoidal Aluminum Conductor Steel-Reinforced

By Application

Primary and Secondary Distribution Conductor Segment Leads Due to Global Grid Modernization and Rural Electrification Initiatives

The market is segmented based on application into:

- Bare Overhead Transmission Conductor

- Primary and Secondary Distribution Conductor

- Messenger Support

- Others

By End User

Utility Sector Represents the Largest End-User Segment Driven by Infrastructure Expansion and Renewable Energy Integration

The market is segmented based on end user into:

- Utility Companies

- Industrial Sector

- Railway Electrification

- Telecommunications Infrastructure

By Voltage Rating

High Voltage Segment Maintains Significant Market Share Owing to Long-Distance Power Transmission Requirements

The market is segmented based on voltage rating into:

- Low Voltage (Up to 1 kV)

- Medium Voltage (1 kV to 33 kV)

- High Voltage (33 kV to 230 kV)

- Extra High Voltage (Above 230 kV)

Regional Analysis: Aluminium Conductor Steel-reinforced Cable (ACSR) Market

Asia-Pacific

The Asia-Pacific region dominates the global ACSR market, accounting for over 55% of total consumption, driven by massive investments in power infrastructure. China, the world’s largest market, is aggressively expanding its ultra-high voltage (UHV) transmission network to connect renewable energy sources from western provinces to coastal load centers. India’s ambitious power sector reforms and rural electrification programs, including the Saubhagya scheme, are fueling substantial demand for ACSR conductors. While cost-effective standard ACSR variants remain prevalent, there is a growing shift toward advanced types like ACSR/AW for enhanced corrosion resistance in coastal and high-pollution areas. The region’s rapid urbanization, industrial growth, and government commitments to grid modernization underpin its leadership position.

North America

North America represents a mature yet steadily growing market for ACSR, characterized by high regulatory standards and a focus on grid resilience. The U.S. Infrastructure Investment and Jobs Act has allocated significant funding for grid modernization and resilience projects, driving demand for high-performance conductors that can withstand extreme weather events. Utilities are increasingly adopting ACSR/TW (Trapezoidal Wire) conductors for their ability to carry higher ampacity in existing right-of-ways, a critical factor in urban and environmentally sensitive areas. The region’s aging power infrastructure requires ongoing replacement and upgrades, with a strong emphasis on reliability and efficiency. Major players like Southwire and General Cable have a strong presence, supplying products that meet stringent ASTM standards.

Europe

Europe’s ACSR market is driven by the integration of renewable energy sources and the modernization of cross-border interconnection projects. Strict EU regulations regarding material sustainability and energy efficiency are pushing manufacturers toward developing more environmentally friendly production processes and products. The region shows growing preference for ACSR/AW conductors, which offer superior corrosion protection crucial for coastal and harsh environmental applications prevalent in Northern Europe. Projects like the North Sea Wind Power Hub and various interconnectors are creating sustained demand for high-capacity transmission conductors. However, the market faces challenges from increasing competition from alternative technologies like GIL (Gas Insulated Lines) for specific high-load applications.

South America

South America presents significant growth opportunities for ACSR manufacturers, particularly in Brazil and Argentina, where hydroelectric power generation and transmission projects are expanding. The region’s diverse geography, featuring long river crossings and challenging terrains, makes ACSR conductors particularly suitable due to their high strength-to-weight ratio. However, economic volatility and inconsistent regulatory frameworks have sometimes delayed major infrastructure projects. Recent developments include Brazil’s focus on integrating Amazon hydropower to population centers and Argentina’s investments in renewable energy transmission from Patagonia. While the market remains price-sensitive, there is growing awareness about the long-term benefits of quality ACSR products over cheaper alternatives.

Middle East & Africa

The Middle East & Africa region represents an emerging market with substantial potential, driven by rapid urbanization and economic diversification efforts. Gulf Cooperation Council countries, particularly Saudi Arabia and the UAE, are investing heavily in power infrastructure as part of their Vision 2030 programs, creating demand for reliable transmission conductors. In Africa, countries like South Africa, Nigeria, and Kenya are expanding their grids to address electricity access challenges. The harsh desert environments in the Middle East require ACSR conductors with enhanced corrosion protection, making ACSR/AW variants particularly relevant. While the market shows promise, growth is sometimes constrained by budget limitations and political instability in certain African nations. Nonetheless, ongoing urban development and industrial growth indicate strong long-term potential for ACSR adoption.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Aluminium Conductor Steel-reinforced Cable (ACSR) markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of advanced materials, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Aluminium Conductor Steel-reinforced Cable (ACSR) Market?

->Aluminium Conductor Steel-reinforced Cable (ACSR) Market was valued at 2914 million in 2024 and is projected to reach US$ 3704 million by 2032, at a CAGR of 3.6% during the forecast period.

Which key companies operate in Global Aluminium Conductor Steel-reinforced Cable (ACSR) Market?

-> Key players include Nexans, Southwire Company, General Cable, Apar Industries, Hengtong Group, Sumitomo Electric Industries, and LS Cable, among others.

What are the key growth drivers?

-> Key growth drivers include global power grid expansion, renewable energy integration, urbanization, and infrastructure modernization projects.

Which region dominates the market?

-> Asia-Pacific dominates the market with over 55% share, primarily driven by China’s massive infrastructure development.

What are the emerging trends?

-> Emerging trends include development of high-temperature low-sag conductors, advanced corrosion-resistant coatings, and integration of smart grid technologies.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...