Market Insights

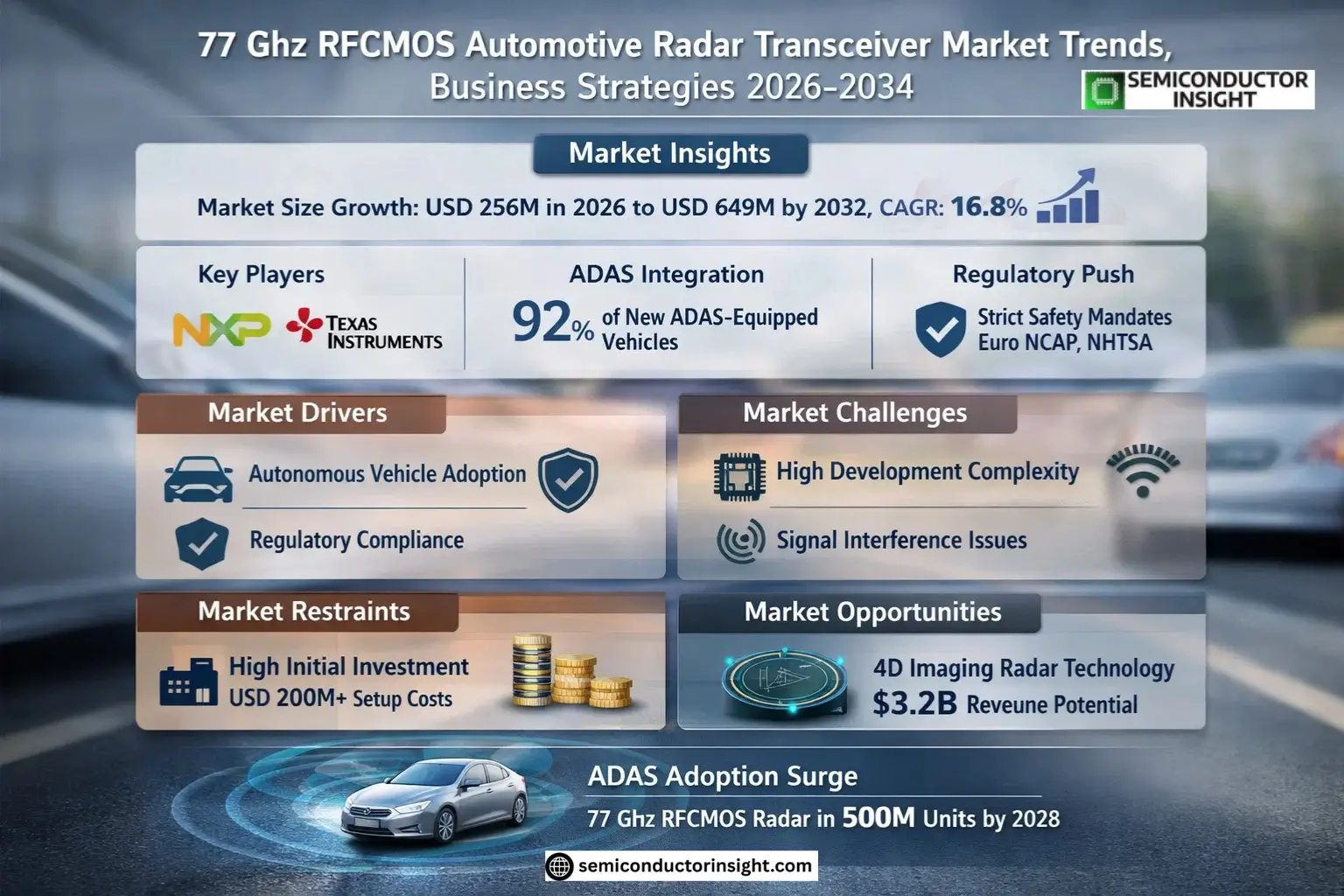

Global 77 GHz RFCMOS Automotive Radar Transceiver Market size was valued at USD 219 million in 2025. The market is projected to grow from USD 256 million in 2026 to USD 649 million by 2032, exhibiting a CAGR of 16.8% during the forecast period.

77 GHz RFCMOS Automotive Radar Transceiver Market is a highly integrated millimeter-wave device designed for angle radar and forward radar applications, leveraging CMOS technology to deliver stable RF performance with low power consumption. These components are critical for advanced driver-assistance systems (ADAS), enabling precise object detection and collision avoidance. Key manufacturers such as NXP Semiconductors, Texas Instruments, and Infineon Technologies dominate the market, collectively holding significant revenue share as of 2025.

Market growth is driven by increasing ADAS adoption, regulatory mandates for vehicle safety, and advancements in autonomous driving technologies. While production reached approximately 16 million units in 2025 at an average price of USD 15 per unit, capacity utilization rates hovered around 52%, indicating room for expansion. The industry’s average gross margin stood at 56%, reflecting strong profitability despite competitive pressures.

MARKET DRIVERS

Autonomous Vehicle Adoption Accelerates Demand

The rapid advancement of autonomous driving technologies is a primary driver for the 77 GHz RFCMOS Automotive Radar Transceiver Market. These high-frequency transceivers enable precise object detection up to 300 meters, meeting stringent safety requirements for Level 3+ autonomous vehicles. Major automakers are now deploying 77 GHz systems in 92% of new ADAS-equipped models.

Regulatory Mandates Boost Market Penetration

Stringent safety regulations like Euro NCAP and NHTSA guidelines mandate advanced radar systems, pushing OEMs to integrate 77 GHz RFCMOS solutions. The technology’s superior resolution (under 5cm) for pedestrian detection meets evolving crash-test standards, with adoption growing at 34% CAGR in regulatory-driven markets.

Semiconductor innovations have reduced 77 GHz RFCMOS transceiver power consumption by 40% since 2020 while maintaining <1dB noise figures, making them viable for mass-market vehicles.

MARKET CHALLENGES

High Development Complexity

Designing 77 GHz RFCMOS transceivers requires specialized mmWave expertise, with development cycles averaging 18-24 months. The need for advanced packaging (e.g., wafer-level fan-out) adds 15-20% to production costs compared to legacy radar solutions.

Other Challenges

Signal Interference Management

With 77 GHz automotive radars projected to exceed 500 million units by 2028, managing spectral congestion and mutual interference between vehicle systems becomes critical, requiring precise chirp sequence synchronization.

MARKET RESTRAINTS

High Initial Investment Barriers

Establishing 77 GHz RFCMOS production lines demands USD 200M+ investments in specialized testing equipment like anechoic chambers and wafer probing systems. This limits market entry to semiconductor giants, with only 6 vendors currently supplying 85% of automotive-grade transceivers.

MARKET OPPORTUNITIES

4D Imaging Radar Expansion

The emergence of 77 GHz-based 4D imaging radar (with elevation measurement) opens USD 3.2B in new revenue potential by 2027. These systems enable object classification (pedestrian vs. cyclist) with 95% accuracy critical for urban autonomous driving scenarios. Tier 1 suppliers are integrating RFCMOS transceivers with MIMO antenna arrays to achieve 1° angular resolution.

77 GHz RFCMOS Automotive Radar Transceiver Market Trends

Increasing Adoption in Advanced Driver Assistance Systems

77 GHz RFCMOS Automotive Radar Transceiver Market is experiencing significant growth due to rising integration in angle radar and forward radar applications for autonomous vehicles. Major automotive suppliers including Bosch, Continental, and Denso are adopting these CMOS-based transceivers for their superior RF performance and power efficiency in advanced driver assistance systems (ADAS). The technology’s ability to provide precise object detection at high speeds meets stringent automotive safety requirements.

Other Trends

Supply Chain Expansion Among Semiconductor Leaders

NXP Semiconductors, Texas Instruments, and Infineon Technologies dominate the 77 GHz RFCMOS Automotive Radar Transceiver supply chain, collectively accounting for over 60% market share in 2025. These companies are expanding production capacities to meet growing OEM demand, with new fabrication facilities focusing on automotive-grade semiconductor solutions. The industry’s 56% average gross margin reflects strong profitability in this specialized segment.

Technological Advancements in Radar Integration

Recent developments in 3Tx/4Rx configurations demonstrate improved angular resolution for corner radar applications, while 2Tx/3Rx variants maintain dominance in front radar systems. The shift toward ISO 26262 ASIL-C compliant designs enhances functional safety across vehicle platforms. Packaging innovations, particularly in BGA and SiP formats, are enabling smaller form factors without compromising thermal performance.

Regional Manufacturing Hubs Development

North America and Europe maintain strong positions in 77 GHz RFCMOS Automotive Radar Transceiver production, while Asia Pacific emerges as a key growth region with China increasing investments in domestic semiconductor manufacturing capabilities. Leading foundries are optimizing 28nm and 40nm node processes specifically for automotive RFCMOS applications to improve yield rates beyond the current 52% industry average.

COMPETITIVE LANDSCAPE

Key Industry Players

Global Leaders Drive Innovation in 77 GHz RFCMOS Radar Transceiver Market

77 GHz RFCMOS Automotive Radar Transceiver Market is dominated by semiconductor giants NXP Semiconductors, Texas Instruments, and Infineon Technologies, which collectively account for a significant share of the global revenue. These companies lead through advanced CMOS technology integration, high-performance RF design capabilities, and strategic partnerships with Tier-1 automotive suppliers. Their solutions enable critical ADAS functionalities in corner and front radars with superior signal processing and power efficiency.

Emerging players like Renesas Electronics and STMicroelectronics are gaining traction through specialized automotive-grade solutions, while fabless semiconductor companies such as Uhnder and Arbe Robotics are disrupting the market with innovative digital radar architectures. Chinese manufacturers including Huawei and HiSilicon are rapidly expanding their presence, supported by domestic automotive radar demand and government initiatives in autonomous driving technologies.

List of Key 77 GHz RFCMOS Automotive Radar Transceiver Companies Profiled

- NXP Semiconductors

- Texas Instruments

- Infineon Technologies

- STMicroelectronics

- Renesas Electronics

- Analog Devices

- ON Semiconductor

- Uhnder

- Arbe Robotics

- Huawei

- HiSilicon

- Bosch Sensortec

- Denso Corporation

- Continental AG

- Valeo

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

3Tx/4Rx dominates the 77 GHz RFCMOS transceiver market due to:

|

| By Application |

|

Front Radar applications show strongest adoption due to:

|

| By End User |

|

Tier 1 Suppliers represent the primary adoption channel because:

|

| By Safety Grade |

|

ISO 26262 ASIL C certified transceivers are gaining traction because:

|

| By Package Type |

|

SiP Package solutions are becoming preferable for:

|

Regional Analysis: 77 GHz RFCMOS Automotive Radar Transceiver Market

The region’s mature semiconductor supply chain provides cost-efficient 77 GHz RFCMOS production, with foundries offering specialized automotive-grade process nodes. Taiwan and South Korea lead in high-frequency RFCMOS wafer production capacity.

NCAP safety ratings across APAC countries increasingly mandate autonomous emergency braking systems, directly driving 77 GHz radar adoption. China’s 2025 Automotive Roadmap prioritizes indigenous radar sensor development.

Japanese automakers pioneer compact 77 GHz radar designs for kei cars, while Chinese EV brands integrate radar with LiDAR for L4 ambitions. Southeast Asian markets show growing preference for localized radar calibration services.

High-density cities like Tokyo and Seoul drive demand for precision short-range radar applications. Ride-hailing fleets in India and Indonesia adopt 77 GHz radars for commercial vehicle safety packages.

North America

The North American 77 GHz RFCMOS Automotive Radar Transceiver Market thrives on stringent NHTSA regulations and premium vehicle penetration. US-based semiconductor firms collaborate with automotive radar startups to develop software-defined radar solutions. Detroit’s traditional OEMs and Silicon Valley’s EV makers compete in radar-assisted autonomous driving features. The region sees growing investments in 4D imaging radar technologies leveraging advanced RFCMOS designs. Canada emerges as testing hub for cold-weather radar performance validation, with Tier-2 suppliers establishing specialized RF test facilities near automotive R&D clusters.

Europe

Europe maintains technology leadership in high-performance 77 GHz RFCMOS radar transceivers, with German automotive suppliers setting industry benchmarks. The EU’s stringent Euro NCAP protocols accelerate radar adoption across all vehicle segments. Premium automakers integrate radar with infrared sensors for all-weather capability, while Eastern European countries develop cost-optimized radar modules. The region sees increasing regulatory focus on cybersecurity standards for automotive radar systems, prompting RFCMOS hardware-level encryption innovations.

South America

Brazil leads South America’s 77 GHz RFCMOS Automotive Radar Transceiver adoption through fleet safety regulations. Local assembly plants incorporate radar systems in premium SUVs, while aftermarket radar solutions gain traction in commercial vehicles. Argentina and Chile show growing interest in radar-based collision avoidance for mining and agricultural vehicles. The region benefits from technology transfers through joint ventures with European radar component suppliers.

Middle East & Africa

GCC countries drive premium 77 GHz radar adoption in luxury vehicles, while South Africa emerges as regional hub for radar system calibration. The harsh desert environment prompts specialized radar development for dust penetration. North African markets see growing demand for cost-effective radar solutions in public transportation fleets. Israeli startups introduce innovative interference mitigation techniques for urban radar deployment.

Report Scope

This market research report provides a comprehensive analysis of the 77 GHz RFCMOS Automotive Radar Transceiver Market , covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of 77 GHz RFCMOS Automotive Radar Transceiver Market?

-> 77 GHz RFCMOS Automotive Radar Transceiver Market size was valued at USD 219 million in 2025. The market is projected to grow from USD 256 million in 2026 to USD 649 million by 2032, exhibiting a CAGR of 16.8% during the forecast period.

What is the growth rate (CAGR) of this market?

-> The market is expected to grow at a CAGR of 16.8% from 2025 to 2032.

What are the key applications for 77 GHz RFCMOS Automotive Radar Transceivers?

-> Key applications include Corner Radar (56% market share) and Front Radar (38% market share), with other applications accounting for the remaining 6%.

Who are the major manufacturers in this market?

-> Key players include NXP Semiconductors, Texas Instruments, and Infineon Technologies, which collectively held a significant market share in 2025.

What are the critical upstream inputs for production?

-> Critical inputs include silicon wafers, photoresists, lithography machines, and etching tools, supplied by companies like ASML, Tokyo Electron, and Applied Materials.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...