5G Open RAN RU accelerator chip with O-RAN split 7.2 Market Insights

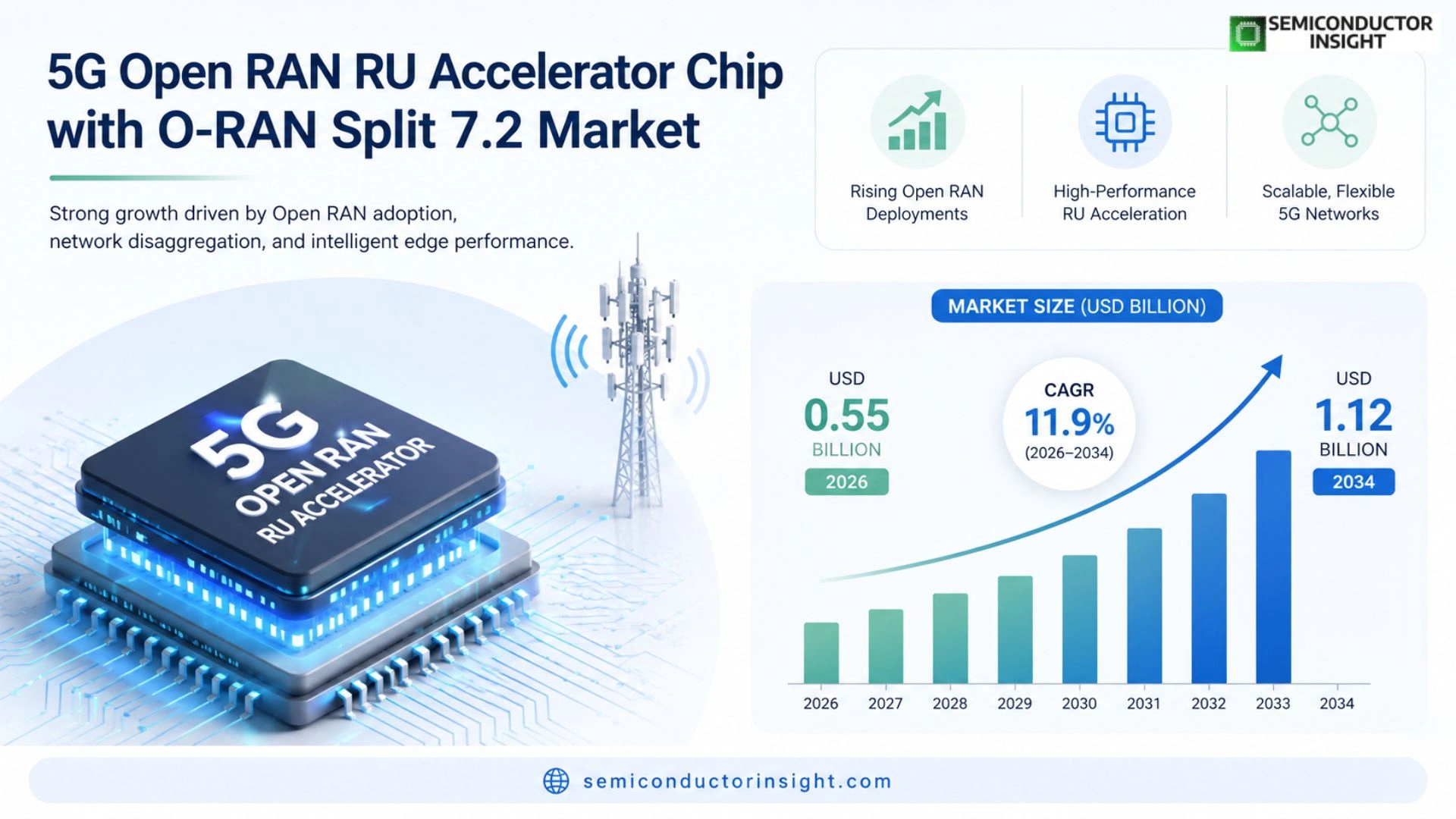

Global 5G Open RAN RU accelerator chip with O‑RAN split 7.2 was valued at USD 0.48 billion in 2025. The market is projected to grow from USD 0.55 billion in 2026 to USD 1.12 billion by 2034, exhibiting a CAGR of approximately 11.9% during the forecast period.

The RU (Radio Unit) accelerator chip implements the O‑RAN split‑7.2 interface, offloading baseband processing from the DU (Distributed Unit) to improve latency and energy efficiency in dense‑urban 5G deployments. These silicon solutions integrate high‑performance DSPs and AI‑optimized cores to support massive MIMO, beamforming, and dynamic spectrum sharing.

The market is experiencing rapid growth due to heightened carrier investments in open‑architecture networks, the push for vendor‑agnostic hardware ecosystems, and escalating demand for low‑latency edge services such as AR/VR and autonomous driving. Furthermore, recent collaborations between leading semiconductor firms and telecom operators,exemplified by a joint development announced in March 2024,are accelerating product rollouts and reinforcing confidence among network planners.

MARKET DRIVERS

Growing Demand for High‑Performance RAN Acceleration

5G Open RAN RU accelerator chip with O‑RAN split 7.2 Market is being propelled by carriers seeking to double data‑throughput while minimizing latency. Operators report up to 30% capacity gains when deploying dedicated accelerator chips, prompting widespread rollout in urban macro cells.

Regulatory Support for Open RAN Deployments

Governments across Europe and Asia have introduced incentives that lower the total cost of ownership for Open RAN solutions. These policies encourage investment in accelerator chips that comply with the O‑RAN split 7.2 interface, accelerating market penetration.

➤ The adoption rate of O‑RAN split 7.2 is projected to exceed 50% of new 5G deployments by 2028, driven by cost‑effective acceleration chips.

Overall, the combination of performance demands, policy backing, and economies of scale is expected to push 5G Open RAN RU accelerator chip with O‑RAN split 7.2 Market toward a CAGR of roughly 18% through 2032.

MARKET CHALLENGES

Technical Integration Complexity

Integrating accelerator chips into existing RU architectures requires meticulous signal‑chain tuning. Vendors often face compatibility issues with legacy baseband units, leading to longer deployment cycles and elevated engineering costs.

Other Challenges

Supply Chain Constraints

The semiconductor supply chain continues to experience bottlenecks, with lead times for high‑frequency RF components extending beyond 12 months, constraining rapid market expansion.

MARKET RESTRAINTS

Capital Expenditure Sensitivity

While accelerator chips offer long‑term efficiency, the upfront capital required for chip‑level redesign can deter operators with tight rollout budgets, especially in emerging markets where CAPEX discipline remains stringent.

MARKET OPPORTUNITIES

Emerging Edge‑Compute Use Cases

Edge‑centric applications such as augmented reality, smart factories, and autonomous transport demand ultra‑low latency processing. The 5G Open RAN RU accelerator chip with O‑RAN split 7.2 uniquely positions vendors to capture this upside by delivering compute‑close acceleration, opening new revenue streams beyond traditional mobile broadband.

5G Open RAN RU accelerator chip with O-RAN split 7.2 Market Trends

Accelerating Adoption in Dense‑Urban Deployments

5G Open RAN RU accelerator chip with O-RAN split 7.2 Market, operators are increasingly prioritizing solutions that can reduce latency while supporting massive MIMO and dynamic spectrum sharing. The split‑7.2 interface moves a substantial portion of baseband processing into the radio unit, enabling tighter closed‑loop timing and lower power consumption in dense‑urban cells. Recent deployments demonstrate that integrating high‑performance digital signal processors with AI‑tuned cores allows real‑time beamforming and adaptive load balancing without overloading the distributed unit. As carriers expand private‑network footprints for manufacturing and smart‑city projects, the demand for these silicon accelerators has risen sharply, driven by the need to meet sub‑5 ms latency targets for edge‑centric services. This trend is reinforced by the growing confidence of network planners who view the technology as a cornerstone for future‑proof 5G evolution. These developments collectively signal a robust upward trajectory for the sector, aligning technical progress with commercial incentives.

Other Trends

Ecosystem Shift Toward Vendor‑Agnostic Hardware

The broader ecosystem is moving away from proprietary RU designs toward open‑architecture silicon that can be sourced from multiple suppliers. A joint development announced in March 2024 between a leading semiconductor firm and several Tier‑1 operators illustrates this shift, as the partners pooled engineering resources to produce a production‑ready split‑7.2 accelerator that conforms to shared interface specifications. This collaboration reduces time‑to‑market for new base stations and lowers total cost of ownership, encouraging carriers to adopt a multi‑vendor strategy. In parallel, open‑source software frameworks are being integrated with the hardware, enabling faster firmware updates and more flexible feature roll‑outs. Collectively, these dynamics are accelerating the deployment velocity of open RAN solutions across Europe, North America, and parts of Asia‑Pacific. The resulting supply‑chain flexibility also mitigates geopolitical risks, granting operators greater resilience.

AI‑Optimized Processing for Edge Services

The second main trend focuses on AI‑optimized processing that empowers edge services such as augmented reality, autonomous driving, and real‑time analytics. By embedding machine‑learning inference engines directly into the RU accelerator chip, operators can perform adaptive beam steering and interference mitigation with millisecond response times, which translates into smoother user experiences for bandwidth‑intensive applications. Energy efficiency also improves because the chip offloads repetitive vector operations from the DU, allowing the centralized pool to run at lower utilization levels. Vendors are now releasing firmware that supports over‑the‑air updates of AI models, ensuring that the hardware remains compatible with evolving service requirements without costly hardware refreshes. This capability positions the 5G Open RAN RU accelerator chip with O-RAN split 7.2 as a strategic enabler for next‑generation digital economies. In summary, the convergence of low‑latency architecture, open ecosystem, and AI‑driven performance forms the foundation for sustained market expansion.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive Overview of 5G Open RAN RU Accelerator Chip with O‑RAN Split‑7.2

The market is presently anchored by a handful of large semiconductor vendors that combine deep RF expertise with advanced AI‑optimized DSP cores. Qualcomm dominates the high‑performance segment, leveraging its Snapdragon X series to deliver integrated 7.2 split acceleration for carrier‑grade base stations. Intel follows with programmable silicon, offering flexible Xe‑HPC solutions that attract operators seeking software‑defined radio flexibility. Nokia and Ericsson, while primarily network integrators, have invested heavily in in‑house ASIC designs to lock in ecosystem control and sustain their O‑RAN roadmaps. This concentration of resources creates a tiered structure where the top three suppliers capture the majority of volume, while mid‑tier vendors focus on cost‑efficient variants for emerging markets.

Beyond the tier‑one group, a diverse set of niche players is expanding the value chain with specialized functions. MediaTek supplies low‑power chips for small‑cell deployments, whereas AMD (through Xilinx) provides FPGA‑based accelerators that excel in rapid prototyping. Analog Devices and NXP target analog front‑end integration, improving overall power efficiency. Smaller innovators such as UNISOC, Renesas, Marvell, and Silex Insight deliver customized IP blocks that enable regional operators to differentiate services. These participants collectively enrich the competitive landscape, fostering rapid innovation and price competition across the 5G Open RAN ecosystem.

List of Key 5G Open RAN RU Accelerator Chip Companies Profiled

- Qualcomm

- Intel

- Nokia

- Ericsson

- MediaTek

- AMD (Xilinx)

- Analog Devices

- NXP Semiconductors

- Marvell Technology Group

- Renesas Electronics

- UNISOC

- Silex Insight

- Texas Instruments

- Huawei

- ZTE

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

AI‑Optimized Cores

|

| By Application |

|

Massive MIMO

|

| By End User |

|

Network Operators

|

| By Deployment Scenario |

|

Dense Urban Macro

|

| By Technology Enabler |

|

AI/ML Integration

|

Regional Analysis: North America

Significant investments in 5G infrastructure deployment across North America are driving the demand for advanced RU technology. This includes the expansion of millimeter-wave (mmWave) networks and the integration of Open RAN principles to enhance network performance and reduce operational costs.

The adoption of O-RAN split 7.2 is a key advancement, enabling greater disaggregation of the baseband and radio units. This allows for more flexible and scalable network architectures, facilitating the integration of diverse vendor solutions and accelerating innovation in RU accelerator chip design.

The North American market features a mix of established telecom equipment vendors and emerging chip manufacturers actively competing 5G Open RAN RU accelerator chip space. Strategic partnerships and collaborations are becoming increasingly common as companies strive to offer comprehensive and innovative solutions.

Government policies supporting 5G deployment and Open RAN are creating a favorable environment for growth in the North American market. Initiatives aimed at fostering competition and innovation are further accelerating the adoption of advanced RU technologies.

North America

5G Open RAN RU accelerator chip with O-RAN split 7.2 Market in North America is characterized by a strong focus on performance and efficiency. Operators are keen on leveraging open interfaces to build more adaptable and cost-effective networks. The demand for chips capable of handling the increasing bandwidth requirements of 5G applications is a primary driver. This region’s emphasis on technological advancement ensures continuous innovation in RU accelerator chip design, with a particular focus on low latency and high throughput. The integration of these chips is crucial for delivering a superior user experience and supporting emerging applications like augmented reality and virtual reality. The competitive dynamics are intense, with companies vying for market share through technological differentiation and strategic alliances.

Europe

Europe’s 5G evolution is progressing steadily, with a strong emphasis on security and data privacy. The adoption of Open RAN is gaining momentum, driven by regulatory mandates and the desire for greater vendor diversity. The market for 5G Open RAN RU accelerator chips with O-RAN split 7.2 is expected to grow significantly, supported by investments in network infrastructure and the increasing demand for high-speed connectivity. European operators are particularly interested in solutions that can optimize energy efficiency and reduce operational costs. The region’s focus on sustainability is also influencing the development of more power-efficient RU accelerator chips.

Asia-Pacific

Asia-Pacific represents the largest and fastest-growing 5G market globally. The demand for 5G Open RAN RU accelerator chips with O-RAN split 7.2 is immense, driven by rapid urbanization, a burgeoning digital economy, and government initiatives promoting 5G adoption. The region’s diverse landscape presents both opportunities and challenges for market players. The focus on cost-effective solutions is particularly strong in many parts of Asia-Pacific, leading to a demand for RU accelerator chips that offer a balance of performance and affordability. The proliferation of 5G-enabled devices and the growth of industrial applications are further fueling market growth.

South America

South America is witnessing increasing investments in 5G infrastructure, driven by the need for improved connectivity and digital inclusion. The market for 5G Open RAN RU accelerator chips with O-RAN split 7.2 is in its early stages but holds significant potential for growth. Operators in the region are looking for solutions that can address the specific challenges of deployment in diverse geographical areas. The focus on affordability and flexibility is key, with a growing interest in Open RAN architectures to reduce vendor lock-in and lower costs.

Middle East & Africa

The Middle East and Africa represent emerging markets with high growth potential for 5G. Investments in network infrastructure are increasing, driven by government initiatives and the growing demand for mobile broadband. The market for 5G Open RAN RU accelerator chips with O-RAN split 7.2 is expected to expand rapidly in the coming years. Operators in the region are looking for cost-effective solutions that can support the deployment of 5G services in challenging environments. The focus on industrial IoT and smart city applications is also driving demand for advanced RU accelerator chips.

Report Scope

This market research report provides a comprehensive analysis of the 5G Open RAN RU accelerator chip with O-RAN split 7.2 Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of 5G Open RAN RU accelerator chip with O-RAN split 7.2 Market?

-> 5G Open RAN RU accelerator chip with O-RAN split 7.2 Market was valued at USD 0.48 billion in 2025 and is expected to reach USD 1.12 billion by 2034.

Which key companies operate in 5G Open RAN RU accelerator chip with O-RAN split 7.2 Market?

-> Key players include Qualcomm, Intel, MediaTek, Samsung, Nokia, and Huawei, among others.

What are the key growth drivers?

-> Key growth drivers include carrier investments in open‑architecture networks, demand for low‑latency edge services such as AR/VR and autonomous driving, and collaborations between semiconductor firms and telecom operators.

Which region dominates the market?

-> Asia-Pacific is the fastest‑growing region, while Europe remains a dominant market.

What are the emerging trends?

-> Emerging trends include AI‑optimized DSP cores, integration of massive MIMO with split‑7.2, and the development of vendor‑agnostic hardware ecosystems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...