28nm Wafer Foundry Market Insights

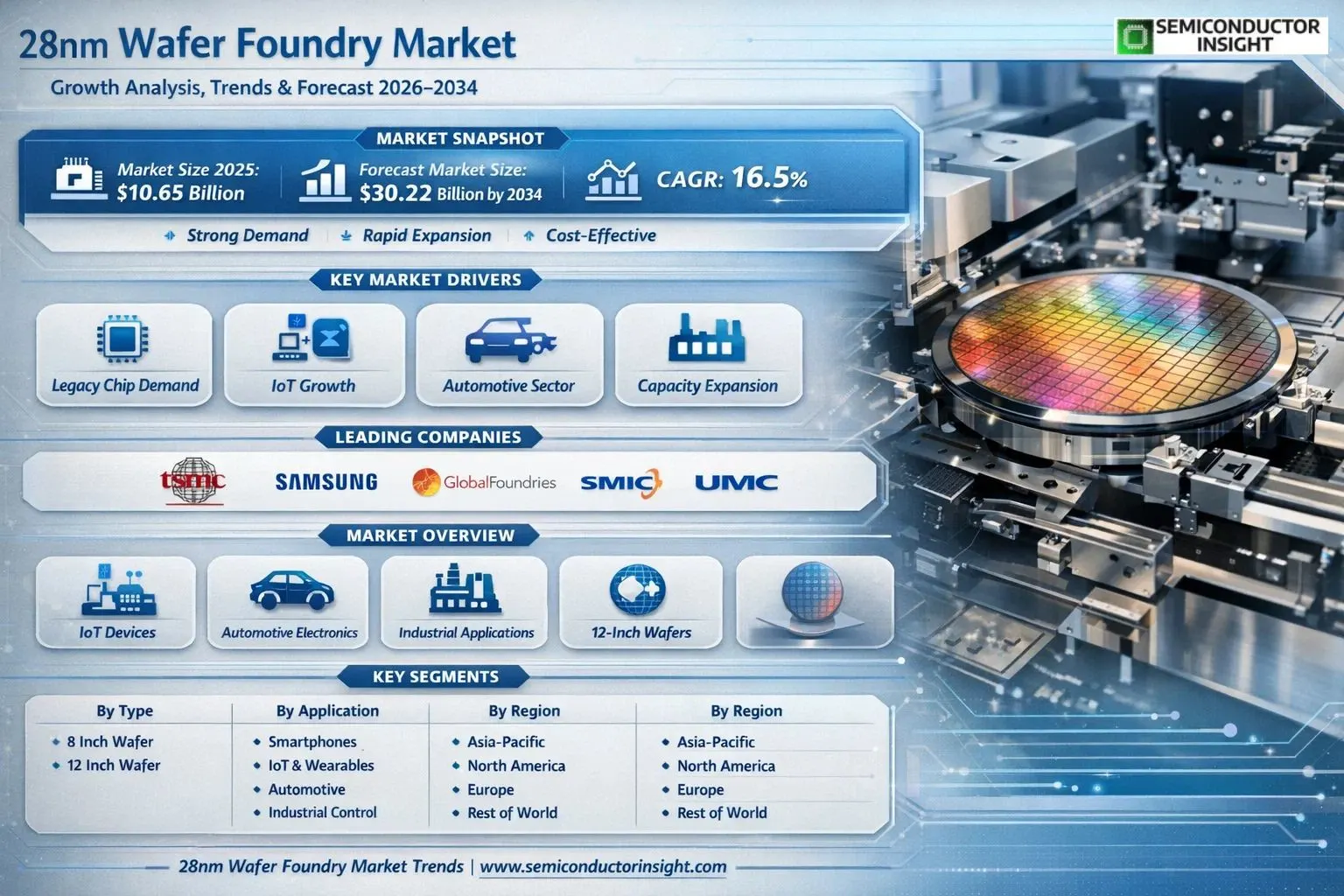

Global 28nm wafer foundry market size was valued at USD 10.65 billion in 2025. The market is projected to grow from USD 11.98 billion in 2026 to USD 30.22 billion by 2034, exhibiting a CAGR of 16.5% during the forecast period.

A 28nm wafer foundry is a specialized semiconductor fabrication facility that produces integrated circuits using the 28-nanometer process technology. This node is a critical workhorse in the industry, serving as the sweet spot between cost-effective mature nodes and high-performance advanced nodes. It offers a significant advantage in power consumption, speed, and gate density over older technologies like 40nm, while remaining substantially more cost-effective to manufacture than cutting-edge sub-10nm processes. This makes it the technology of choice for a vast array of applications that require a balance of performance, power efficiency, and affordability.

The market is experiencing robust growth driven by several key factors, including sustained demand for legacy chips in automotive and industrial applications, the massive expansion of the Internet of Things (IoT) ecosystem, and global initiatives to bolster semiconductor supply chain resilience. Furthermore, the insatiable demand for connectivity and edge computing devices is contributing significantly to market expansion. Strategic moves by leading foundries are also expected to fuel growth. For instance, in 2023, TSMC, Samsung, and UMC all announced capacity expansions for their 28nm/22nm specialty processes to address the ongoing supply-demand imbalance. Taiwan Semiconductor Manufacturing Company (TSMC), Samsung Foundry, GlobalFoundries, Semiconductor Manufacturing International Corporation (SMIC), and United Microelectronics Corporation (UMC) are the dominant key players that operate in this concentrated market.

MARKET DRIVERS

Cost-Effective Mature Node Demand

28nm Wafer Foundry Market is propelled by sustained demand for cost-efficient semiconductor production in applications like power management ICs and automotive electronics. With production costs approximately 30-40% lower than 16nm nodes, foundries such as TSMC and GlobalFoundries report steady wafer orders exceeding 1.5 million units monthly for 28nm processes in 2023.

Expansion in IoT and Legacy Applications

Growth in IoT devices and industrial controls further drives the market, where 28nm offers optimal balance of performance and power efficiency. Market projections indicate a CAGR of 5.2% through 2028, fueled by over 25% of global IoT chips fabricated at this node due to reliable yield rates above 95%.

➤ Increased automotive adoption, with 28nm accounting for 40% of ADAS wafers, underscores resilience amid node transitions.

Strategic investments in capacity expansions by leading foundries ensure supply chain stability, positioning the 28nm wafer foundry segment as a cornerstone for mature technology ecosystems.

MARKET CHALLENGES

Supply Chain Disruptions

28nm Wafer Foundry Market faces hurdles from geopolitical tensions and raw material shortages, impacting wafer fabrication timelines. In 2023, delays affected up to 15% of production runs, prompting foundries to diversify suppliers amid rising equipment costs.

Other Challenges

Intensifying competition from advanced nodes like 7nm erodes market share, with 28nm volumes declining 8% year-over-year as clients migrate to higher-performance alternatives for data centers.

Capacity Allocation Pressures

Foundries prioritize newer processes, leading to 28nm backlogs that extend lead times to 20 weeks and inflate pricing by 10-12% in high-demand quarters.

MARKET RESTRAINTS

Shift to Advanced Nodes

A primary restraint on 28nm Wafer Foundry Market is the industry-wide migration toward sub-10nm technologies, reducing allocation for 28nm to under 20% of total foundry capacity by 2024. This shift prioritizes AI and high-performance computing demands over mature nodes.

Elevated R&D costs for maintaining 28nm yields, coupled with environmental regulations on chemical usage, constrain expansion. Foundries face compliance expenses rising 15% annually, limiting new fab investments.

Market saturation in consumer electronics further caps growth, as 28nm’s performance ceiling fails to meet evolving 5G and edge AI specifications, projecting stagnation at $8-10 billion through 2027.

MARKET OPPORTUNITIES

Automotive and Power Electronics Boom

28nm Wafer Foundry Market holds promise in electric vehicles and renewable energy sectors, where robust, cost-effective chips are essential. EV power management demand could boost 28nm wafers by 25% by 2028, leveraging radiation-hardened variants.

Emerging markets in Asia-Pacific offer untapped potential, with India and Southeast Asia ramping local production to cut import reliance, potentially adding 300,000 wafers annually.

Hybrid node strategies combining 28nm with specialty features like embedded memory open doors for customized solutions, enhancing market resilience against advanced node dominance.

28nm Wafer Foundry Market Trends

Demand Surge in IoT and Automotive Applications

28nm Wafer Foundry Market continues to exhibit robust demand driven by its position as a cost-effective bridge between mature and advanced semiconductor processes. Offering superior performance in power consumption, speed, and gate density compared to older nodes like 40nm, while maintaining lower costs than 14nm or 7nm technologies, the 28nm process remains vital for high-volume applications. Key sectors such as Internet of Things (IoT) devices and automotive electronics are primary contributors, with IoT requiring reliable, power-efficient chips for sensors and connectivity, and automotive electronics demanding robust solutions for advanced driver-assistance systems (ADAS) and infotainment.

Other Trends

Shift Toward 12-Inch Wafers

In 28nm Wafer Foundry Market, there is a noticeable transition from 8-inch to 12-inch wafers, enhancing production efficiency and yield rates. This shift supports higher throughput for applications like smartphones and industrial controls, where economies of scale are critical. Leading foundries prioritize 12-inch capacity expansions to meet escalating volumes in consumer and embedded systems.

Market Concentration with Top Players

28nm Wafer Foundry Market remains highly concentrated, dominated by TSMC, Samsung, GlobalFoundries, SMIC, and UMC. These players control significant shares through advanced manufacturing capabilities and strategic investments. TSMC and Samsung lead in technology refinements, while SMIC and UMC cater to regional demands, particularly in Asia. This oligopolistic structure fosters innovation in process optimization but also intensifies competition on pricing and delivery timelines.

Regional Dynamics Led by Asia-Pacific

Asia, especially China, Japan, South Korea, and Southeast Asia, drives 28nm Wafer Foundry Market growth due to proximity to major electronics manufacturing hubs and supportive government policies. North America and Europe follow with focused demand from automotive and industrial sectors, while emerging markets in South America and the Middle East & Africa show potential in IoT adoption. Overall, the market’s evolution reflects balanced expansion across smartphones, computers, automotive electronics, and industrial control applications, underscoring the 28nm node’s enduring relevance in diversified semiconductor ecosystems.

COMPETITIVE LANDSCAPE

Key Industry Players

28nm Wafer Foundry Market Leaders and Concentration

28nm Wafer Foundry Market exhibits a highly concentrated structure, dominated by a handful of leading pure-play foundries and integrated device manufacturers (IDMs) with dedicated foundry services. TSMC commands the largest market share, leveraging its mature 28nm process technology that balances cost efficiency with superior performance in power consumption, speed, and gate density. This node serves as a critical bridge between legacy processes like 40nm and advanced nodes such as 14nm or 7nm, driving demand across smartphones, IoT, automotive electronics, and industrial applications. The oligopolistic nature of the market, with top players controlling the majority of capacity, underscores high capital barriers and economies of scale in 8-inch and 12-inch wafer production.

Beyond the frontrunners, other significant players like Samsung Foundry, GlobalFoundries, SMIC, and UMC contribute substantial capacity and innovation in 28nm offerings, often customizing processes for specific end-markets such as computing and automotive. Niche foundries including Shanghai Huahong and PSMC focus on specialized 28nm solutions for analog, mixed-signal, and power management ICs, capturing segments underserved by volume leaders. This competitive dynamic fosters price stability amid growing demand, projected to expand from US$10,650 million in 2025 to US$30,220 million by 2034 at a 16.5% CAGR, while top five firms hold dominant revenue and sales shares.

List of Key 28nm Wafer Foundry Companies Profiled

- TSMC

- Samsung Foundry

- GlobalFoundries

- SMIC

- UMC

- Shanghai Huahong

- PSMC

- Vanguard International Semiconductor (VIS)

- Tower Semiconductor

- DB HiTek

- X-FAB

- Silterra Malaysia

- Grace Semiconductor Manufacturing (merged into HHGrace)

- United Microelectronics Corporation (UMC affiliate facilities)

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

12 Inch Wafer leads due to its advantages in high-volume production environments.

|

| By Application |

|

Smartphone application dominates as it leverages the cost-performance sweet spot of 28nm technology.

|

| By End User |

|

Consumer Electronics end users lead the adoption of 28nm foundry services.

|

| By Technology |

|

28nm HPC technology variant is prominent for its performance advantages.

|

| By Platform |

|

Handsets platform commands the forefront with its dynamic requirements.

|

Regional Analysis: 28nm Wafer Foundry Market

Asia-Pacific

Taiwan’s mature infrastructure anchors Asia-Pacific’s 28nm wafer foundry dominance, with facilities excelling in yield optimization and volume scaling. China’s emerging fabs complement this by prioritizing self-reliance, while South Korea focuses on specialized automotive-grade processes. These hubs benefit from proximity to end-markets, enabling rapid prototyping and customization in 28nm Wafer Foundry Market.

Continuous refinements in 28nm high-k metal gate and FinFET-like structures boost power efficiency, vital for edge computing and 5G infrastructure. Regional R&D consortia drive strain engineering for enhanced mobility, keeping Asia-Pacific ahead in balancing performance and affordability within the 28nm wafer foundry ecosystem.

Integrated vendor networks from silicon to assembly mitigate disruptions, a key strength in 28nm Wafer Foundry Market. Local sourcing of chemicals and equipment reduces lead times, while diversified logistics strategies enhance reliability for global clients reliant on Asia-Pacific production.

Heavy capital inflows fund fab modernizations and greenfield projects tailored to 28nm demands. Public-private partnerships accelerate talent development, positioning the region for long-term leadership in mature node foundry services amid shifting business strategies through 2034.

North America

North America plays a pivotal role in 28nm Wafer Foundry Market through innovation-driven design and strategic partnerships, despite limited domestic fabrication. Leading fabless firms collaborate with overseas partners for 28nm production, focusing on high-margin applications like AI accelerators and defense systems. Recent policy shifts encourage onshoring via subsidies, spurring investments in advanced packaging tied to 28nm cores. The region’s strength lies in IP development and system-level integration, fostering demand for reliable wafer supply. Challenges include higher costs and talent shortages, but growing ecosystems in the Southwest bolster resilience. North America influences global trends by prioritizing customized 28nm solutions for next-gen computing, shaping business strategies toward diversified sourcing by 2034.

Europe

Europe advances steadily in 28nm Wafer Foundry Market, leveraging automotive and industrial sectors for mature node adoption. Specialized foundries emphasize radiation-hardened and low-power 28nm processes for ADAS, medical devices, and renewable energy controls. Collaborative research initiatives across member states enhance yield improvements and EUV readiness for extensions. While dependent on Asian capacity, Europe builds strategic reserves and local assembly to counter supply vulnerabilities. Regulatory focus on sustainability drives eco-friendly fab designs, aligning with green wafer production goals. This region’s analytical approach ensures niche leadership in safety-critical applications, with evolving partnerships strengthening its position in the 28nm wafer foundry landscape through 2034.

South America

South America remains an emerging player in 28nm Wafer Foundry Market, with nascent infrastructure limiting scale but showing potential in consumer electronics assembly. Brazil leads regional efforts through tech parks and incentives attracting outsourcing for back-end processes linked to 28nm wafers. Proximity to growing Latin markets supports IoT and agrotech deployments requiring cost-optimized 28nm chips. Skill-building programs bridge gaps, while imports from Asia meet current needs. Economic stabilization and trade agreements pave the way for incremental fab investments, positioning South America for gradual integration into global 28nm supply chains with business strategies emphasizing affordability and localization by 2034.

Middle East & Africa

The Middle East & Africa region is nascent in 28nm Wafer Foundry Market, focusing on oil-to-tech diversification. Gulf states invest in semiconductor hubs for sovereign capabilities, targeting 28nm for smart cities and defense electronics. Africa’s telecom growth fuels demand for affordable wafers, spurring assembly facilities. Partnerships with established foundries provide technology transfer, building local expertise. Infrastructure challenges persist, but energy abundance supports power-intensive fabs. Strategic visions prioritize 28nm as an entry node, fostering ecosystems for long-term self-sufficiency amid regional trends toward digital transformation through 2034.

Report Scope

This market research report provides a comprehensive analysis of the 28nm Wafer Foundry Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of 28nm Wafer Foundry Market?

-> Global 28nm Wafer Foundry market was valued at USD 10,650 million in 2025 and is expected to reach USD 30,220 million by 2034 at a CAGR of 16.5%.

Which key companies operate in 28nm Wafer Foundry Market?

-> Key players include TSMC, Samsung, GlobalFoundries, SMIC, UMC, Shanghai Huahong, and PSMC, among others.

What are the key growth drivers?

-> Key growth drivers include lower costs compared to advanced processes like 14nm and 7nm, improved performance over older nodes such as 40nm in power consumption, speed, and gate density.

Which region dominates the market?

-> Asia dominates the market, driven by major players in China, Taiwan, Japan, and South Korea.

What are the emerging trends?

-> Emerging trends include strong demand from smartphones, IoT, automotive electronics, and industrial control applications, with focus on 8-inch and 12-inch wafers.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...