MARKET INSIGHTS

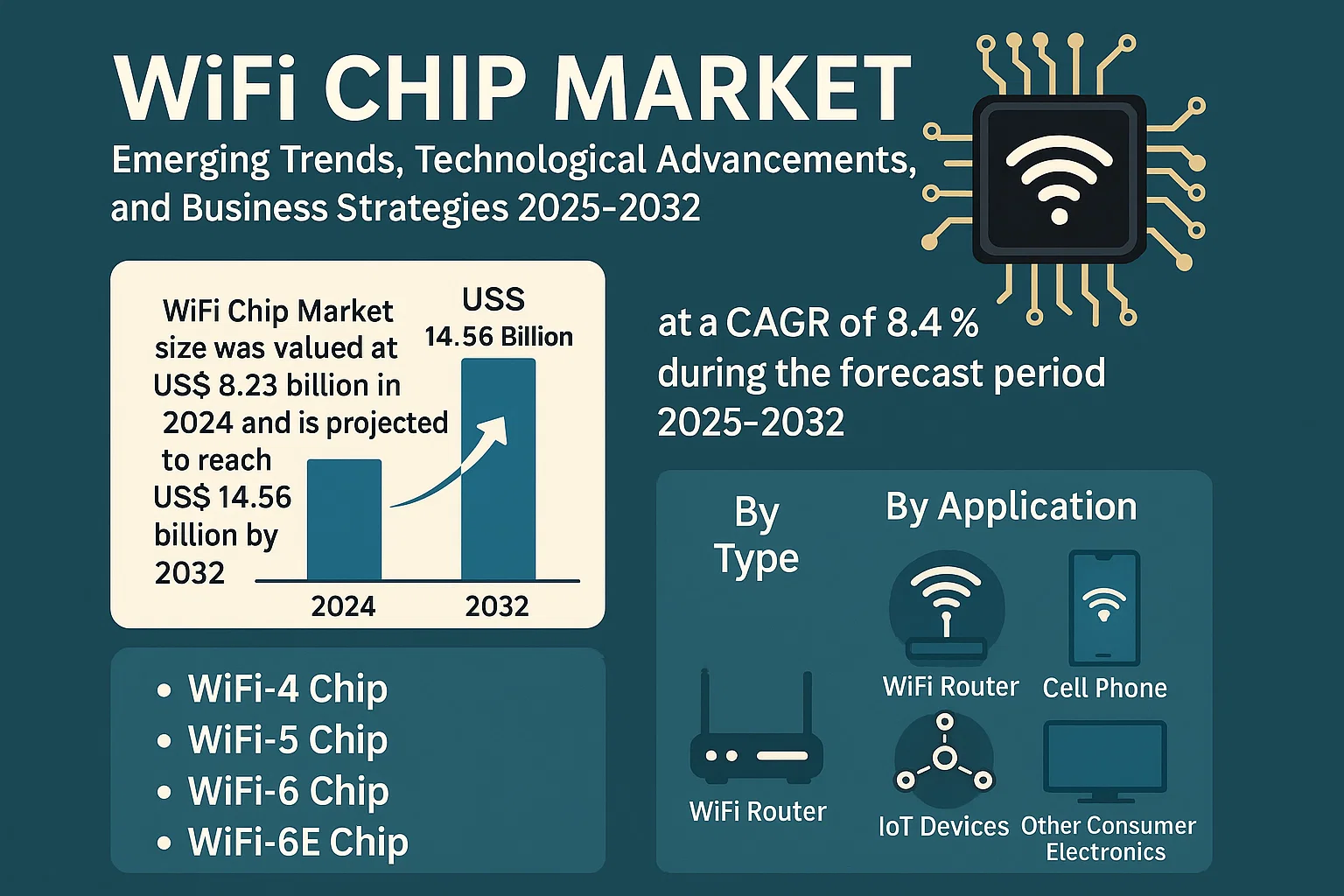

The global WiFi Chip Market size was valued at US$ 8.23 billion in 2024 and is projected to reach US$ 14.56 billion by 2032, at a CAGR of 8.4% during the forecast period 2025-2032. This growth aligns with the broader semiconductor industry, which was valued at USD 579 billion in 2022 and is expected to reach USD 790 billion by 2029.

WiFi chips are semiconductor devices that enable wireless connectivity by implementing IEEE 802.11 standards. These integrated circuits (ICs) process radio frequency signals to establish network connections, supporting various WiFi generations including WiFi-4, WiFi-5, WiFi-6, and the emerging WiFi-6E. Key components include RF transceivers, baseband processors, and MAC controllers.

Market expansion is driven by increasing IoT adoption, with 29 billion connected devices projected by 2030, and rising demand for high-speed connectivity in smartphones and routers. The segment is also benefiting from technological advancements like WiFi 7 development, with major players including Qualcomm, Broadcom, and MediaTek leading innovation. While the analog IC segment grows steadily at 6% CAGR, WiFi chips show stronger momentum due to their critical role in modern wireless infrastructure.

MARKET DYNAMICS

MARKET DRIVERS

Proliferation of IoT Devices to Accelerate WiFi Chip Demand

The exponential growth of Internet of Things (IoT) applications is creating unprecedented demand for WiFi chips across multiple industries. With over 15 billion active IoT devices currently deployed globally and projections indicating this number will surpass 29 billion by 2030, WiFi chips are becoming fundamental components in smart infrastructure. These chips enable seamless connectivity in applications ranging from industrial automation to consumer wearables, driving manufacturers to develop more energy-efficient and high-performance solutions. For instance, the industrial IoT sector alone is expected to account for nearly 30% of all WiFi chip shipments by 2026, demonstrating the technology’s critical role in Industry 4.0 transformations.

WiFi 6/6E Standard Adoption to Fuel Market Expansion

The transition to WiFi 6 and WiFi 6E standards represents one of the most significant drivers for the WiFi chip market. These next-generation technologies offer substantial improvements in speed, capacity, and latency compared to previous standards. WiFi 6 provides up to 4x faster speeds than WiFi 5 in dense environments, while WiFi 6E unlocks additional spectrum in the 6 GHz band. Many leading smartphone manufacturers have already integrated WiFi 6E chips in their flagship devices, with over 350 million WiFi 6E chipsets expected to ship in 2024 alone. This rapid adoption is pushing major chip manufacturers to increase production capacity while driving down per-unit costs through economies of scale.

Remote Work Infrastructure Investments to Sustain Market Growth

The global shift toward hybrid work models continues to stimulate demand for advanced networking equipment, including WiFi chips. Enterprises are upgrading their network infrastructure to support bandwidth-intensive applications, with the enterprise WiFi market projected to grow at 10% CAGR through 2030. Furthermore, the consumer segment is witnessing increased demand for high-performance routers and mesh systems capable of supporting multiple streaming and videoconferencing sessions simultaneously. This sustained demand from both corporate and residential sectors is creating a robust growth trajectory for WiFi chip manufacturers.

MARKET CHALLENGES

Complex Supply Chain Constraints Impacting Production Timelines

The global semiconductor shortage has created significant production bottlenecks for WiFi chip manufacturers. Lead times for certain components have extended to 52 weeks or more, disrupting normal manufacturing cycles. While the situation has improved from its peak in 2021-22, the industry still faces intermittent shortages of specific materials like silicon wafers and specialty chemicals. These supply chain disruptions have forced many manufacturers to maintain higher inventory levels, increasing working capital requirements by an average of 20-25%. Smaller players in particular struggle with these challenges as they lack the purchasing power of larger corporations to secure favorable supplier agreements.

Other Challenges

Design Complexity

Developing WiFi chips that support multiple standards while maintaining power efficiency requires increasingly sophisticated engineering. Each new WiFi generation introduces complex features like orthogonal frequency-division multiple access (OFDMA) and multi-user MIMO, exponentially increasing design validation requirements. This complexity has led to extended product development cycles and higher R&D expenditures across the industry.

Security Vulnerabilities

As WiFi becomes more pervasive, security concerns continue to escalate. Recent vulnerabilities discovered in various WiFi standards have prompted manufacturers to implement more robust security protocols, adding to development costs and potentially delaying product time-to-market. The need for ongoing firmware updates and security patches creates additional challenges for manufacturers and end-users alike.

MARKET RESTRAINTS

Market Saturation in Consumer Electronics to Limit Growth Potential

While WiFi chip adoption continues to grow, certain segments are approaching saturation points that may constrain future expansion. The smartphone market, which accounts for approximately 35% of all WiFi chip consumption, is showing signs of maturity with declining replacement rates. Similarly, tablets and laptops have reached high penetration levels in developed markets, with annual growth rates slowing to low single digits. This saturation forces chip manufacturers to increasingly rely on premium features and next-generation standards to maintain growth, rather than simply benefiting from expanding unit volumes.

Regulatory Hurdles in Spectrum Allocation to Restrict Innovation Cycles

The introduction of new WiFi standards frequently requires regulatory approval for additional spectrum allocation. The fragmented nature of global telecommunications regulations creates complex challenges for chip manufacturers who must develop region-specific products. For example, while WiFi 6E has been approved in many countries, several major markets still restrict 6 GHz access, forcing manufacturers to produce separate product variants. These regulatory delays can postpone market adoption of new technologies by 12-18 months in some regions, hindering the industry’s ability to realize the full potential of technological advancements.

MARKET OPPORTUNITIES

Emerging WiFi 7 Standard to Create New Revenue Streams

The anticipated commercialization of WiFi 7 technology presents significant market opportunities for forward-looking manufacturers. Early WiFi 7 chipsets demonstrate theoretical speeds exceeding 40 Gbps and will support new applications in augmented reality and industrial automation. While formal certification is expected in 2024, prototype implementations already show 2-3x performance improvements over WiFi 6E in controlled environments. Industry analysts predict that WiFi 7 could account for 15% of all WiFi chip revenue by 2026 as high-end routers and enterprise networks begin adopting the standard. The transition window between WiFi 6/6E and WiFi 7 is expected to create a multi-year upgrade cycle across multiple device categories.

Specialized Industrial Applications to Drive Premium Pricing

The increasing digitization of manufacturing processes is creating demand for industrial-grade WiFi chips with enhanced reliability features. Unlike consumer applications, industrial environments require chips that can operate in extreme temperatures and high-electromagnetic interference conditions. These specialized applications command significantly higher ASPs (average selling prices) compared to standard consumer WiFi chips, with margins 30-40% above the industry average. Major industrial automation projects are expected to generate over $2 billion in WiFi chip revenue by 2027, presenting attractive growth opportunities for manufacturers who can meet stringent quality requirements.

Integration with 5G Networks to Enable New Use Cases

The convergence of WiFi and 5G technologies is creating synergistic opportunities across telecommunications infrastructure. Network operators are increasingly deploying converged solutions that automatically hand off connections between WiFi and cellular networks, requiring specialized chipsets that support both technologies. These hybrid solutions are particularly valuable in enterprise environments where they can reduce cellular network congestion while providing seamless connectivity. The market for converged connectivity chips is forecast to grow at 25% CAGR through 2030, representing one of the most dynamic segments within the broader WiFi chip market.

WIFI CHIP MARKET TRENDS

WiFi-6 and WiFi-6E Adoption Accelerates Market Growth

The global WiFi chip market is experiencing exponential growth, driven primarily by rapid adoption of WiFi-6 and WiFi-6E technologies across consumer and enterprise applications. These next-generation standards offer significantly higher data rates, improved network efficiency, and reduced latency compared to previous iterations. While WiFi-5 (802.11ac) still holds a substantial market share, industry data indicates that WiFi-6 chip shipments grew by over 300% year-over-year in 2023, demonstrating remarkable market traction. The emergence of WiFi-6E, which operates in the newly-opened 6GHz spectrum, is particularly noteworthy as it provides additional bandwidth for bandwidth-intensive applications such as 8K video streaming and AR/VR experiences. Furthermore, modern WiFi chips now integrate advanced features like multi-user MIMO and OFDMA, significantly enhancing performance in high-density environments.

Other Trends

Internet of Things (IoT) Ecosystem Expansion

The proliferation of IoT devices continues to create substantial demand for cost-effective, low-power WiFi chips designed for smart home, industrial, and healthcare applications. Manufacturers are increasingly focusing on developing energy-efficient solutions with enhanced security protocols to cater to battery-powered IoT endpoints. Industry projections suggest that by 2027, over 40% of all WiFi chip shipments will be destined for IoT applications, reflecting the technology’s critical role in enabling ubiquitous connectivity. This trend is particularly evident in smart home devices, where WiFi-based solutions are overcoming traditional protocol fragmentation to become the preferred connectivity standard.

Integration with 5G Networks Driving Innovation

The convergence of WiFi and cellular technologies is reshaping the connectivity landscape, with modern WiFi chips increasingly supporting seamless handoffs between WiFi and 5G networks. This integration is particularly important for applications requiring uninterrupted connectivity, such as enterprise mobility solutions and public hotspots. Several industry leaders have introduced WiFi chips with enhanced coexistence algorithms that optimize performance in environments saturated with both WiFi and cellular signals. Furthermore, the development of WiFi 7 (802.11be) chipsets, anticipated to enter mass production in 2024, promises to deliver multi-gigabit speeds and ultra-low latency, potentially transforming how wireless networks are deployed across various sectors. These advancements are expected to support emerging use cases in industrial automation, telemedicine, and cloud gaming, further expanding the addressable market for WiFi chip manufacturers.

COMPETITIVE LANDSCAPE

Key Industry Players

WiFi Chip Manufacturers Focus on Innovation to Capture Market Share

The global WiFi chip market is highly competitive, featuring a mix of established semiconductor giants and emerging innovators. Qualcomm and Broadcom currently dominate the market landscape, collectively holding over 45% of the global revenue share in 2024. Their leadership stems from advanced WiFi-6/6E solutions and strong partnerships with smartphone manufacturers.

MediaTek has rapidly gained traction through cost-effective chipsets for mid-range devices, while Intel maintains a strong position in PC and enterprise networking segments. These companies are aggressively investing in next-generation WiFi 7 technology, scheduled for commercial deployment by 2025.

Emerging players like ASR Microelectronics and Espressif Systems are disrupting the market with specialized IoT solutions, capturing 12.3% of the total unit shipments in 2024. Their growth reflects the increasing demand for low-power, high-efficiency connectivity in smart home applications.

List of Key WiFi Chip Manufacturers Profiled

- Qualcomm Technologies, Inc. (U.S.)

- Broadcom Inc. (U.S.)

- Intel Corporation (U.S.)

- MediaTek Inc. (Taiwan)

- NXP Semiconductors N.V. (Netherlands)

- Texas Instruments Incorporated (U.S.)

- Infineon Technologies AG (Germany)

- ON Semiconductor Corp. (U.S.)

- Realtek Semiconductor Corp. (Taiwan)

- Triductor Technology Inc. (China)

- Espressif Systems (China)

Segment Analysis:

By Type

WiFi-6 Chip Segment Dominates Due to Increasing Demand for High-Speed Connectivity

The market is segmented based on type into:

- WiFi-4 Chip

- WiFi-5 Chip

- WiFi-6 Chip

- WiFi-6E Chip

By Application

Smartphones Lead the Market Owing to Ubiquitous Wireless Connectivity Needs

The market is segmented based on application into:

- WiFi Router

- Cell Phone

- IoT Devices

- Other Consumer Electronics

By End User

Consumer Electronics Sector Accounts for Largest Market Share

The market is segmented based on end user into:

- Consumer Electronics

- Enterprise

- Automotive

- Industrial

Regional Analysis: WiFi Chip Market

North America

North America dominates the WiFi chip market with advanced technological adoption and widespread 5G deployment. The U.S. accounts for the highest demand due to strong investments in smart infrastructure, including smart cities and IoT deployments. Companies like Qualcomm, Broadcom, and Intel lead innovation, focusing on WiFi 6E and future WiFi 7 standards to support high-speed connectivity. The region benefits from high disposable income, strong R&D investments, and escalating demand for low-latency wireless solutions in gaming, AR/VR, and enterprise applications. However, regulatory pressures around semiconductor supply chain security and trade restrictions pose challenges.

Europe

Europe is a significant market driven by strict data privacy laws (GDPR) and smart home adoption. Countries like Germany, the U.K., and France lead in industrial IoT and automotive WiFi integration, accelerating demand for high-performance WiFi chips. The EU’s focus on digital sovereignty has led to partnerships with local semiconductor manufacturers like Infineon and NXP, reducing reliance on foreign chip suppliers. WiFi 6 adoption is growing, particularly in enterprise solutions. However, geopolitical tensions and energy crises have impacted supply chains, leading to cautious market expansion.

Asia-Pacific

The fastest-growing region, driven by China, Japan, and India, Asia-Pacific dominates manufacturing and consumption of WiFi chips. China’s tech giants (Huawei, Xiaomi) are vertically integrating semiconductor production, with MediaTek and Realtek leading market share. Affordable smartphones and massive IoT deployments in India and Southeast Asia fuel demand for cost-effective WiFi 4 and WiFi 5 chips. Meanwhile, Japan and South Korea focus on high-end chips for robotics and automotive use cases. Supply chain disruptions and U.S.-China trade tensions remain key challenges, but local semiconductor policies (e.g., India’s PLI scheme) aim to boost self-sufficiency.

South America

South America shows gradual growth, primarily in Brazil and Argentina, driven by expanding telecom infrastructure and consumer electronics. Low 5G penetration restricts demand for advanced WiFi 6/6E chips, with most demand centered on WiFi 4 and WiFi 5 for budget devices. Economic instability and currency fluctuations hinder large-scale investments, though rising smartphone adoption in rural areas provides opportunities. Local players struggle to compete with dominant global suppliers, limiting market consolidation.

Middle East & Africa

An emerging market with substantial long-term potential, the region prioritizes smart city initiatives (e.g., UAE’s Dubai 2040 Plan). WiFi chip demand is concentrated in GCC countries like Saudi Arabia and the UAE, where high-income consumers drive premium device sales. However, Africa’s growth lags due to limited digital infrastructure, though mobile-first economies (Nigeria, Kenya) present opportunities for low-cost WiFi solutions. Supply chain fragmentation and geopolitical risks slow adoption, but public-private partnerships aim to bridge connectivity gaps.

Report Scope

This market research report provides a comprehensive analysis of the global and regional WiFi Chip markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type (WiFi-4, WiFi-5, WiFi-6, WiFi-6E), application (WiFi Router, Cell Phone, IoT), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with country-level analysis.

- Competitive Landscape: Profiles of leading participants including Broadcom, Qualcomm, Intel, MediaTek, NXP, and their product strategies, R&D focus, and market positioning.

- Technology Trends: Assessment of emerging WiFi standards (WiFi 7), AI/ML integration in chipsets, power efficiency improvements, and 5G-WiFi convergence technologies.

- Market Drivers & Restraints: Evaluation of factors including IoT expansion, smart home adoption, and 5G proliferation versus supply chain challenges and geopolitical factors.

- Stakeholder Analysis: Strategic insights for semiconductor manufacturers, OEMs, investors, and policymakers regarding market opportunities and challenges.

Research methodology combines primary interviews with industry leaders, analysis of financial reports, and validation through multiple verified data sources to ensure accuracy.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global WiFi Chip Market?

-> WiFi Chip Market size was valued at US$ 8.23 billion in 2024 and is projected to reach US$ 14.56 billion by 2032, at a CAGR of 8.4% during the forecast period 2025-2032.

Which key companies operate in Global WiFi Chip Market?

-> Key players include Broadcom, Qualcomm, Intel, MediaTek, NXP, Texas Instruments, Infineon, and Realtek, collectively holding over 75% market share.

What are the key growth drivers?

-> Primary growth drivers include 5G network expansion, smart home device adoption, IoT proliferation, and increasing demand for WiFi-6/6E compatible devices.

Which region dominates the market?

-> Asia-Pacific accounts for 42% of global demand, driven by electronics manufacturing in China, South Korea, and Taiwan, while North America leads in technology adoption.

What are the emerging trends?

-> Emerging trends include WiFi-7 development, AI-powered chipsets, ultra-low power designs for IoT, and integrated 5G-WiFi solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...