Market Insights

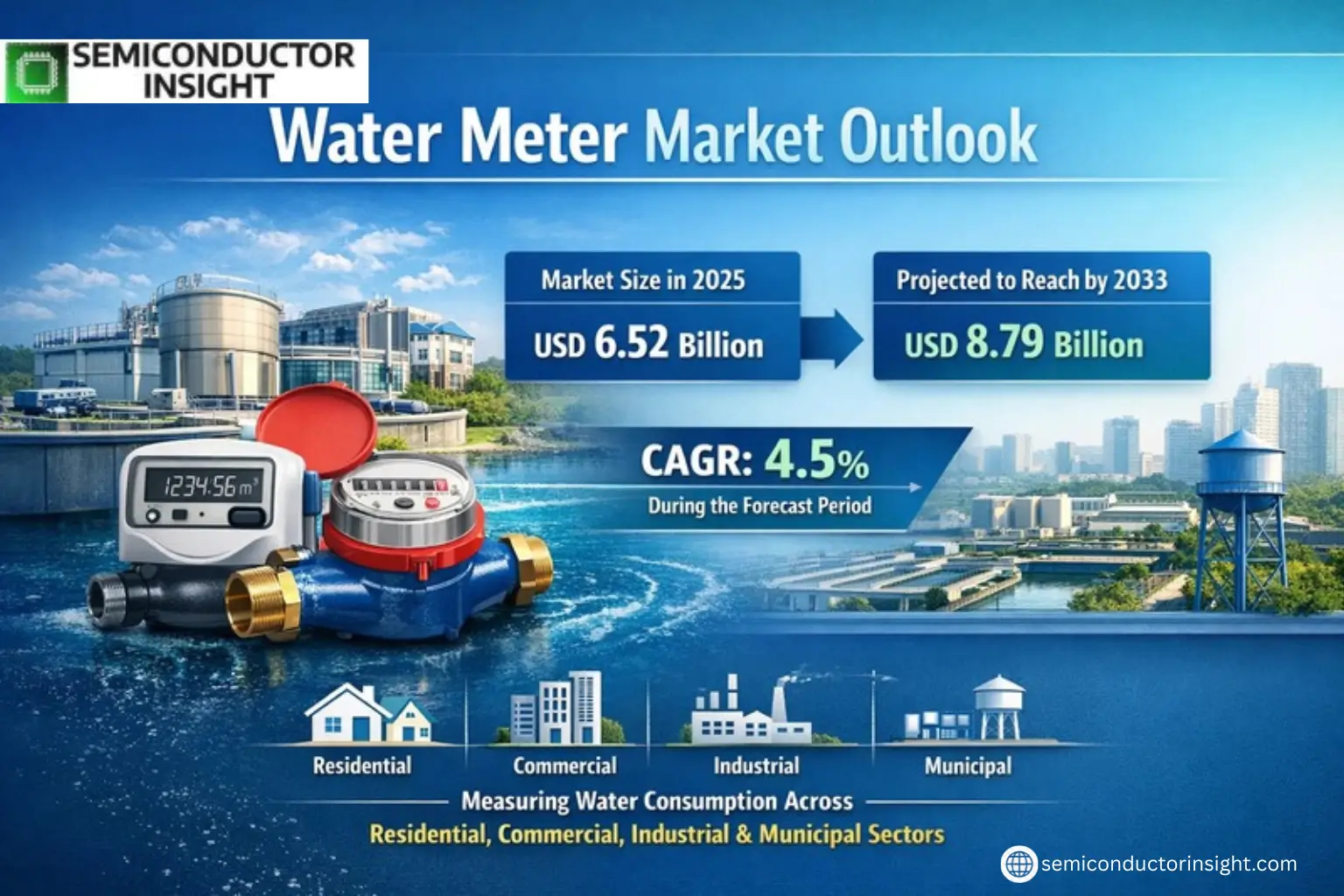

Global Water Meter Market size was valued at USD 6.52 billion in 2025. The market is projected to grow from USD 6.52 billion in 2025 to USD 8.79 billion by 2033, exhibiting a CAGR of 4.5% during the forecast period.

Water meters are devices used to measure the volume of water consumed by residential, commercial, industrial, and municipal users. These meters play a critical role in water management, enabling accurate billing and efficient resource allocation. The two primary types of water meters include mechanical water meters and smart water meters, with the latter gaining significant traction due to advancements in IoT and automation technologies.

The market is experiencing steady growth driven by factors such as increasing urbanization, rising demand for efficient water management systems, and government initiatives promoting smart city projects. Additionally, the shift toward smart water meters which offer real-time monitoring and leak detection is accelerating adoption across regions. Key players like Sensus, Badger Meter, Itron, Honeywell, and Ningbo Water Meter dominate the market, collectively holding a 39% share. Asia-Pacific leads globally with a 53% market share due to rapid infrastructure development, followed by Europe (22%) and North America (17%).

MARKET DRIVERS

Global Water Scarcity Concerns

The increasing water scarcity across regions is driving demand for water meter installations. Governments worldwide are implementing strict water conservation policies, with metering being a key component. Urbanization and population growth are further accelerating adoption, as utilities seek to monitor usage patterns effectively.

Smart Meter Infrastructure Investments

Utilities are investing heavily in smart water meter technology to reduce non-revenue water losses. Advanced metering infrastructure (AMI) deployments grew by approximately 12% globally last year, with digital solutions offering real-time consumption monitoring and leak detection capabilities.

Regulatory mandates for water conservation in commercial buildings and industrial sectors are creating sustained demand for accurate metering solutions across all consumer segments.

MARKET CHALLENGES

High Infrastructure Upgrade Costs

The transition to advanced water metering systems requires significant capital expenditure. Many municipal utilities face budget constraints, delaying large-scale deployments. Cost recovery periods often exceed 5-7 years, creating hesitation among cash-strapped water authorities.

Other Challenges

Data Management Complexities

Modern water meter networks generate vast data volumes, requiring sophisticated analytics platforms. Utilities lacking IT infrastructure struggle with data processing, limiting the effectiveness of smart meter investments.

MARKET RESTRAINTS

Slow Replacement Cycles

Traditional mechanical water meters have lifespans exceeding 10-15 years, creating natural adoption barriers for new technologies. Utilities often postpone upgrades until end-of-life, slowing market turnover despite technological advancements.

MARKET OPPORTUNITIES

IoT-enabled Metering Solutions

Integration of IoT technology in water meter systems presents significant growth potential. Wireless connectivity allows utilities to implement usage-based pricing models and predictive maintenance, potentially reducing operational costs by up to 30%. Emerging markets represent particularly strong opportunities as they leapfrog directly to smart metering solutions.

Water Meter Market Trends

Smart Meter Adoption Driving Market Growth

Global Water Meter Market is experiencing steady growth, projected to reach USD 8.78 billion by 2033 with a 4.5% CAGR. Smart water meters currently dominate the product segment with 71% market share due to their accuracy and real-time monitoring capabilities. Asia-Pacific leads regional adoption, accounting for 53% of global demand, driven by rapid urbanization and infrastructure development in emerging economies.

Other Trends

Residential Sector Dominance

Residential applications hold 78% market share as governments worldwide implement stricter water conservation policies. The commercial sector is also seeing increased adoption, particularly in water-intensive industries seeking to optimize resource management through advanced metering solutions.

Market Consolidation and Competitive Landscape

The top five manufacturers control 39% of the global Water Meter Market, with Sensus, Badger Meter, and Itron leading the sector. Product innovation remains key as companies integrate IoT capabilities into smart meters. Recent mergers and acquisitions are reshaping competitive dynamics, particularly in North America and European markets.

Regulatory Push for Water Conservation

Municipal regulations mandating water metering in urban areas are accelerating market growth. Europe shows particularly strong adoption due to the EU Water Framework Directive, while drought-prone regions like the Middle East are investing heavily in metering infrastructure to manage scarce water resources more effectively.

Future Outlook and Challenges

While the Water Meter Market shows promising growth, challenges include high initial costs of smart meters and varying regional adoption rates. Emerging markets with aging infrastructure present significant opportunities, particularly for companies offering cost-effective hybrid solutions combining mechanical and smart metering technologies.

COMPETITIVE LANDSCAPE

Key Industry Players

Smart Metering Adoption Reshapes Water Utility Infrastructure

Global Water Meter Market is dominated by established players like Sensus (Xylem), Badger Meter, and Itron, which collectively hold nearly 40% market share. These companies lead through advanced smart metering solutions and strategic acquisitions. The competitive landscape reflects increasing R&D investments in IoT-enabled meters, with Asia-Pacific emerging as both a manufacturing hub and largest consumer market. Honeywell and Neptune Technology Group maintain strong positions in North America through municipal contracts, while European leaders Kamstrup and Diehl focus on energy-efficient designs.

Specialized manufacturers like Zenner and Sanchuan Wisdom Technology are gaining traction through cost-competitive ultrasonic meter solutions. Chinese players including Ningbo Water Meter and Hangzhou Seck Intelligent Technology account for over 25% of global production capacity, focusing on export markets. Emerging smart water management startups are disrupting traditional markets through AI-powered leakage detection systems, though infrastructure requirements limit their current market penetration.

List of Key Water Meter Companies Profiled

- Sensus (Xylem Inc.)

- Badger Meter

- Itron Inc.

- Honeywell International

- Ningbo Water Meter Co., Ltd.

- Neptune Technology Group

- Diehl Stiftung & Co. KG

- Kamstrup A/S

- Sanchuan Wisdom Technology Co., Ltd.

- Ningbo Donghai Group

- Zenner International GmbH

- Mueller Water Products

- Hangzhou Seck Intelligent Technology

- Suntront Tech Co., Ltd.

- Shenzhen Huaxu Science & Technology Development

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Smart Water Meter dominates due to:

|

| By Application |

|

Residential Sector shows strongest adoption because:

|

| By End User |

|

Public Utilities lead consumption due to:

|

| By Technology |

|

Ultrasonic Technology gains traction because:

|

| By Installation |

|

Replacement Units drive market growth through:

|

Regional Analysis: Global Water Meter Market

Asia-Pacific

China leads regionally with comprehensive smart meter deployment programs, particularly in urban areas. The government mandates contribute to steady market growth, with emphasis on IoT-enabled devices for efficient water resource monitoring and leak detection.

India’s market expansion stems from nationwide water conservation programs and AMR system adoption. Municipal corporations are prioritizing meter installations to address water distribution challenges in rapidly growing urban centers.

Japan maintains advanced water meter infrastructure with high smart meter penetration. The market focuses on precision measurement technologies and integration with broader smart utility networks.

Emerging ASEAN economies show increasing demand for basic water meters as rural water access improves. Governments are implementing universal metering policies to establish consumption patterns and reduce system losses.

North America

The North American Water Meter Market features high replacement demand and smart meter adoption. U.S. utilities are implementing large-scale meter modernization projects with focus on data analytics capabilities. Canadian municipalities emphasize leak detection and water conservation through advanced metering infrastructure. The region benefits from stringent water efficiency regulations and established market players offering innovative connected meter solutions.

Europe

European markets demonstrate mature adoption of smart water meters, driven by sustainability targets and water conservation directives. The EU’s water framework directive encourages meter deployment across member states. Western Europe leads in AMI implementation, while Eastern Europe shows growth potential with infrastructure upgrades. Several countries mandate universal water metering for all consumers.

Latin America

Latin America presents opportunities for Water Meter Market growth amid expanding urban water networks. Brazil and Mexico lead regional adoption through municipal water management initiatives. The market focuses on addressing non-revenue water challenges through improved metering. Basic meter demand remains strong, though smart meter pilot projects are increasing in major cities.

Middle East & Africa

The MEA region shows varying water meter adoption levels across countries. GCC nations invest heavily in smart water infrastructure, integrating meters with city-wide resource management systems. African markets face infrastructure challenges but demonstrate potential with development initiatives focusing on universal water access and metered supply.

Report Scope

This market research report provides a comprehensive analysis of the Water Meter Market, covering the forecast period 2025–2033. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of water meters in enabling efficient water management across industries such as residential, commercial, industrial, and municipal.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of smart water metering solutions, IoT applications, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for manufacturers, suppliers, distributors, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Water Meter Market?

-> Water Meter Market size was valued at USD 6.52 billion in 2025. The market is projected to grow from USD 6.52 billion in 2025 to USD 8.79 billion by 2033, exhibiting a CAGR of 4.5% during the forecast period.

Which key companies operate in Water Meter Market?

-> Key players include Sensus, Badger Meter, Itron, Honeywell, Ningbo Water Meter, Neptune Technology Group, Diehl Stiftung, Kamstrup, Sanchuan Wisdom Technology, and Ningbo Donghai Group, among others. The top five players hold a combined market share of about 39%.

What is the largest product segment?

-> Smart Water Meter is the largest segment, accounting for 71% of the market share.

Which region dominates the Water Meter Market?

-> Asia-Pacific is the largest market with 53% share, followed by Europe (22%) and North America (17%).

What is the leading application segment?

-> Residential applications dominate with 78% market share.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...