Market Insights

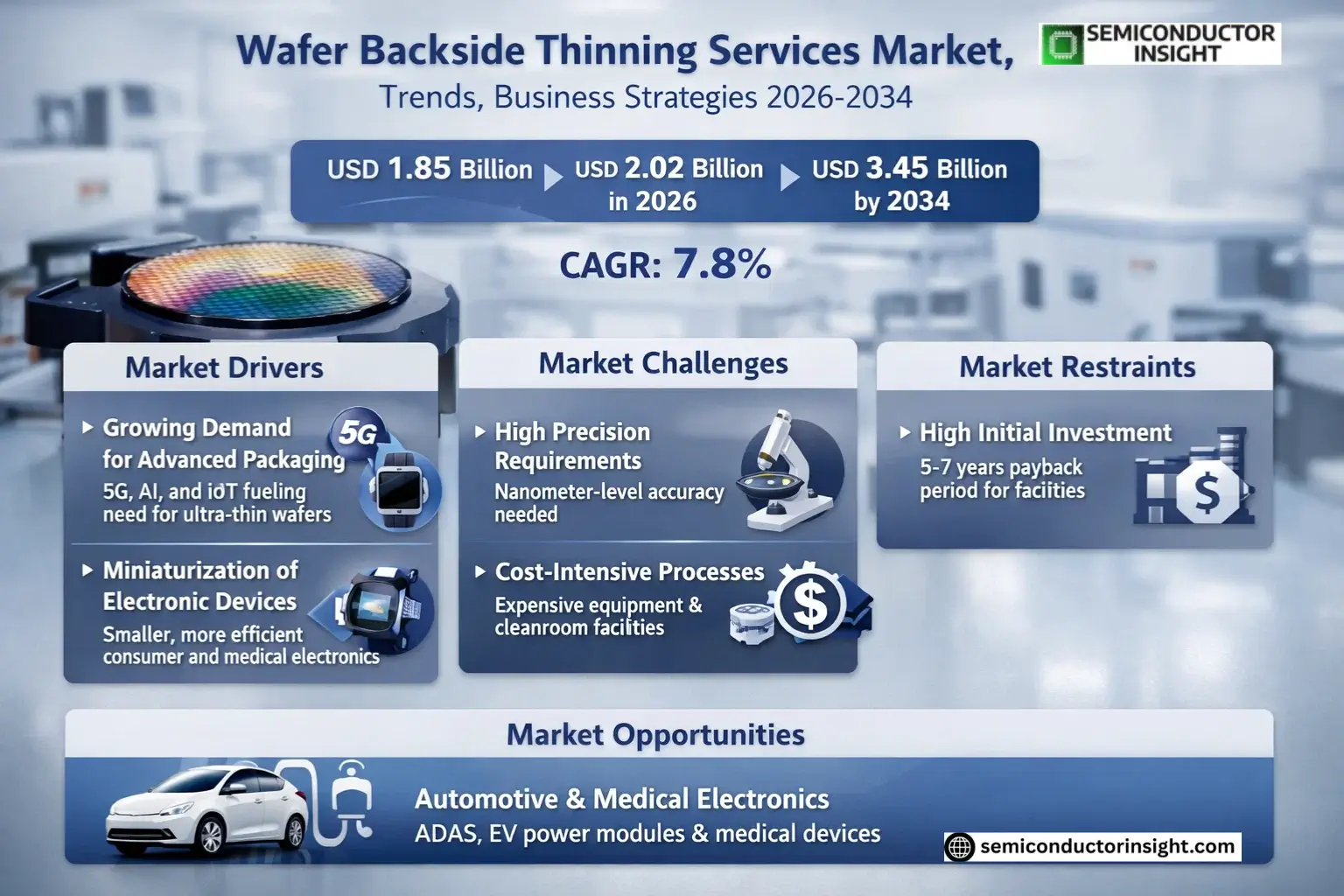

Global Wafer Backside Thinning Services Market size was valued at USD 1.85 billion in 2025. The market is projected to grow from USD 2.02 billion in 2026 to USD 3.45 billion by 2034, exhibiting a CAGR of 7.8% during the forecast period.

Wafer backside thinning services involve precision processes such as grinding and etching to reduce the thickness of semiconductor wafers, enhancing performance and enabling advanced packaging solutions. These services are critical for applications in consumer electronics, automotive electronics, and data centers, where thinner wafers improve thermal management and device integration.

The market is driven by increasing demand for compact and high-performance semiconductor devices, alongside advancements in wafer-level packaging technologies. Key players like DISCO Corporation and Silicon Valley Microelectronics are expanding their capabilities to meet rising industry requirements, further accelerating market growth.

MARKET DRIVERS

Growing Demand for Advanced Semiconductor Packaging

Wafer Backside Thinning Services Market is experiencing significant growth due to the rising demand for advanced semiconductor packaging solutions. As consumer electronics and IoT devices become more compact, manufacturers require ultra-thin wafers to enable higher-density chip integration. Global shift toward 5G technology and AI applications has further accelerated this demand.

Miniaturization of Electronic Devices

With smartphones, wearables, and medical devices requiring increasingly smaller form factors, wafer backside thinning services have become essential. Thin wafers (below 100µm) allow for improved thermal performance and reduced power consumption in compact electronic components. Leading semiconductor foundries are investing heavily in wafer thinning technologies to meet these specifications.

Advanced wafer thinning techniques such as plasma etching and chemical-mechanical polishing are enabling manufacturers to achieve thicknesses below 50µm while maintaining structural integrity.

MARKET CHALLENGES

High Precision Requirements and Yield Management

The wafer backside thinning process requires nanometer-level precision to avoid cracks, warping, or contamination. Maintaining high yield rates while achieving ultra-thin profiles remains a critical challenge for service providers, as even minor defects can render wafers unusable for advanced applications.

Other Challenges

Cost-Intensive Equipment and Processes

Wafer backside thinning demands specialized equipment like grinders, polishers, and etching systems, which require significant capital investment. Additionally, the need for cleanroom facilities and skilled technicians adds to operational costs.

Thermal Management in Thin Wafers

As wafer thickness decreases below 70µm, managing heat dissipation becomes more complex, requiring additional engineering solutions that can increase production costs by 15-20%.

MARKET RESTRAINTS

High Initial Investment and Long Payback Periods

Wafer Backside Thinning Services Market faces limitations due to the substantial capital required for establishing production facilities. Smaller foundries often opt for outsourcing rather than developing in-house capabilities, which can slow market expansion. The average payback period for a wafer thinning production line currently ranges between 5-7 years.

MARKET OPPORTUNITIES

Emerging Applications in Automotive and Medical Electronics

Wafer Backside Thinning Services Market is witnessing new growth opportunities from the automotive sector, where thin wafers are critical for advanced driver assistance systems (ADAS) and electric vehicle power modules. Medical device manufacturers are also adopting wafer thinning for implantable electronics and miniature diagnostic equipment. The medical electronics segment is expected to grow at 8.2% annually through 2028.

Wafer Backside Thinning Services Market Trends

Rising Demand for Advanced Semiconductor Packaging

Wafer Backside Thinning Services Market is experiencing growth driven by increasing demand for advanced packaging solutions in semiconductor manufacturing. Thinning processes enable better thermal management and miniaturization, critical for modern electronics. Companies are adopting wafer thinning to meet performance requirements in applications like consumer electronics and automotive systems.

Other Trends

Expansion of Grinding Technology

Grinding remains the dominant wafer backside thinning method due to its precision and cost-effectiveness. Technological advancements in grinding equipment allow for ultra-thin wafers below 50μm thickness, meeting the needs of 3D IC packaging and MEMS applications. Manufacturers are investing in automated grinding solutions to enhance throughput.

Geographical Market Shifts

Asia-Pacific continues to lead in wafer backside thinning adoption, with China and Japan driving demand from foundries and IDMs. North America shows steady growth, particularly in high-performance computing applications. European markets are focusing on thin-wafer solutions for automotive and industrial electronics.

Emerging Applications Driving Innovation

The development of 5G infrastructure, IoT devices, and AI hardware is creating new opportunities for wafer thinning services. These applications require thinner, more efficient semiconductor components, pushing service providers to develop advanced thinning techniques with improved yield rates and surface quality.

Competitive Landscape Developments

Key players like DISCO Corporation and Syagrus Systems are expanding their service capabilities to include hybrid thinning approaches combining mechanical and chemical methods. The market is seeing increased specialization, with some providers focusing on niche applications such as photonics or power devices.

COMPETITIVE LANDSCAPE

Key Industry Players

Global Market Dominated by Specialized Semiconductor Service Providers

Wafer Backside Thinning Services Market is characterized by a concentrated competitive landscape, with leading players like DISCO Corporation and Syagrus Systems controlling significant market share through advanced grinding and etching technologies. These established providers maintain dominance through proprietary equipment, precision engineering capabilities, and strategic partnerships with major semiconductor fabs. The top five companies collectively accounted for approximately XX% of global revenue in 2025, with technological differentiation in ultra-thin wafer processing (sub-50μm) serving as a key competitive battleground.

Several specialized manufacturers have carved out strong positions in niche segments, including Silicon Valley Microelectronics for MEMS applications and NICHIWA KOGYO for compound semiconductor substrates. Emerging players such as Huahong Group and Winstek are gaining traction in Asian markets through cost-competitive service models, while technology-focused firms like Helia Photonics compete through innovative thinning solutions for photonic applications. Regional specialists like Phoenix Silicon International have strengthened their positions through localized service networks and quick turnaround capabilities.

List of Key Wafer Backside Thinning Services Companies Profiled

- DISCO Corporation

- Syagrus Systems

- Silicon Valley Microelectronics, Inc.

- SIEGERT WAFER GmbH

- NICHIWA KOGYO CO.,LTD.

- Integra Technologies

- Valley Design

- AXUS TECHNOLOGY

- Helia Photonics

- Aptek Industries

- UniversityWafer, Inc.

- Enzan Factory Co., Ltd.

- Phoenix Silicon International

- Prosperity Power Technology Inc.

- Huahong Group

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Grinding dominates the market as the preferred wafer thinning technique due to:

|

| By Application |

|

Consumer Electronics represents the largest application segment because:

|

| By End User |

|

Foundries are the primary users of wafer thinning services due to:

|

| By Wafer Size |

|

300mm wafers show strongest demand for backside thinning because:

|

| By Service Provider |

|

Pure-play Thinning Specialists maintain leadership through:

|

Regional Analysis: Wafer Backside Thinning Services Market

Asia-Pacific

Asia-Pacific leads in adopting advanced wafer backside thinning techniques like temporary bonding/debonding and ultra-thin wafer handling, with Taiwanese firms pioneering sub-50μm thinning capabilities for 3D IC applications.

The region boasts the world’s highest concentration of 300mm wafer fabs, creating concentrated demand for high-volume backside thinning services near major semiconductor clusters in Hsinchu, Shanghai and Pyeongtaek.

Close collaboration between thinning service providers, equipment manufacturers and OSAT companies enables seamless integration from wafer fabrication to packaging, reducing logistics costs and cycle times.

Growing demand for wafer thinning services comes from advanced packaging applications including CIS, MEMS sensors and power devices, with Chinese manufacturers rapidly expanding capabilities for automotive and IoT chips.

North America

North America maintains leadership in specialized wafer backside thinning services for high-performance computing and aerospace applications. The region benefits from strong R&D capabilities and demand from fabless semiconductor companies that outsource advanced packaging needs. Major IDMs in the US are investing in wafer-level packaging solutions to support AI/ML processors requiring ultra-thin wafers. The presence of leading equipment manufacturers enables access to cutting-edge thinning technologies, though local thinning service capacity remains limited compared to Asia, leading to partnerships with overseas providers.

Europe

Europe’s wafer backside thinning market is characterized by specialized applications in automotive and industrial sectors, with Germany and France leading in MEMS and power device production. The region has developed niche expertise in handling compound semiconductor wafers for RF applications. While lacking Asia’s volume capacity, European service providers focus on high-mix, low-volume production with stringent quality requirements. Collaborative R&D projects under EU semiconductor initiatives are driving development of advanced thinning techniques for next-generation power electronics.

Middle East & Africa

The MEA region is emerging as a potential market for wafer backside thinning services, with growing semiconductor packaging activity in Israel and limited foundry operations in the UAE. Most regional demand is met through partnerships with global service providers, though local capabilities remain limited. The region shows potential for specialized applications in aerospace and defense sectors, with investments in compound semiconductor manufacturing creating future opportunities for localized thinning services.

South America

South America remains a minor player in wafer backside thinning services, with limited semiconductor manufacturing infrastructure. Brazil has some packaging and test operations that utilize basic thinning services, primarily sourced from international providers. The region’s market potential is constrained by limited local semiconductor production, though growing electronics manufacturing could drive future demand for basic backside thinning solutions.

Report Scope

This market research report provides a comprehensive analysis of the Wafer Backside Thinning Services Market , covering the forecast period 2025–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of wafer thinning in powering advancements across industries such as consumer electronics, automotive electronics, and data centers.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type (Grinding, Etching, Others), technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia, South America, and Middle East & Africa, including country-level analysis.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments.

- Technology Trends & Innovation: Assessment of emerging wafer thinning technologies, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, and market-entry barriers.

- Stakeholder Insights: Insights for wafer manufacturers, OEMs, system integrators, and investors regarding strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts and data from verified sources to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Wafer Backside Thinning Services Market?

-> Wafer Backside Thinning Services Market size was valued at USD 1.85 billion in 2025. The market is projected to grow from USD 2.02 billion in 2026 to USD 3.45 billion by 2034, exhibiting a CAGR of 7.8% during the forecast period.

What is the growth rate (CAGR) of Wafer Backside Thinning Services Market?

-> The market is expected to grow at a CAGR of % during 2025-2034.

Which are the key players in Wafer Backside Thinning Services Market?

-> Key players include Syagrus Systems, Optim Wafer Services, Silicon Valley Microelectronics, SIEGERT WAFER GmbH, DISCO Corporation, AXUS TECHNOLOGY, and other leading companies.

Which segment leads the market by product type?

-> Grinding segment dominates the market and is projected to reach USD million by 2034.

Which region shows highest growth potential?

-> China is expected to reach USD million by 2034, showing significant growth potential.

What are the main applications of Wafer Backside Thinning Services?

-> Key applications include Consumer Electronics, Automotive Electronics, and Computer and Data Center sectors.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...