MARKET INSIGHTS

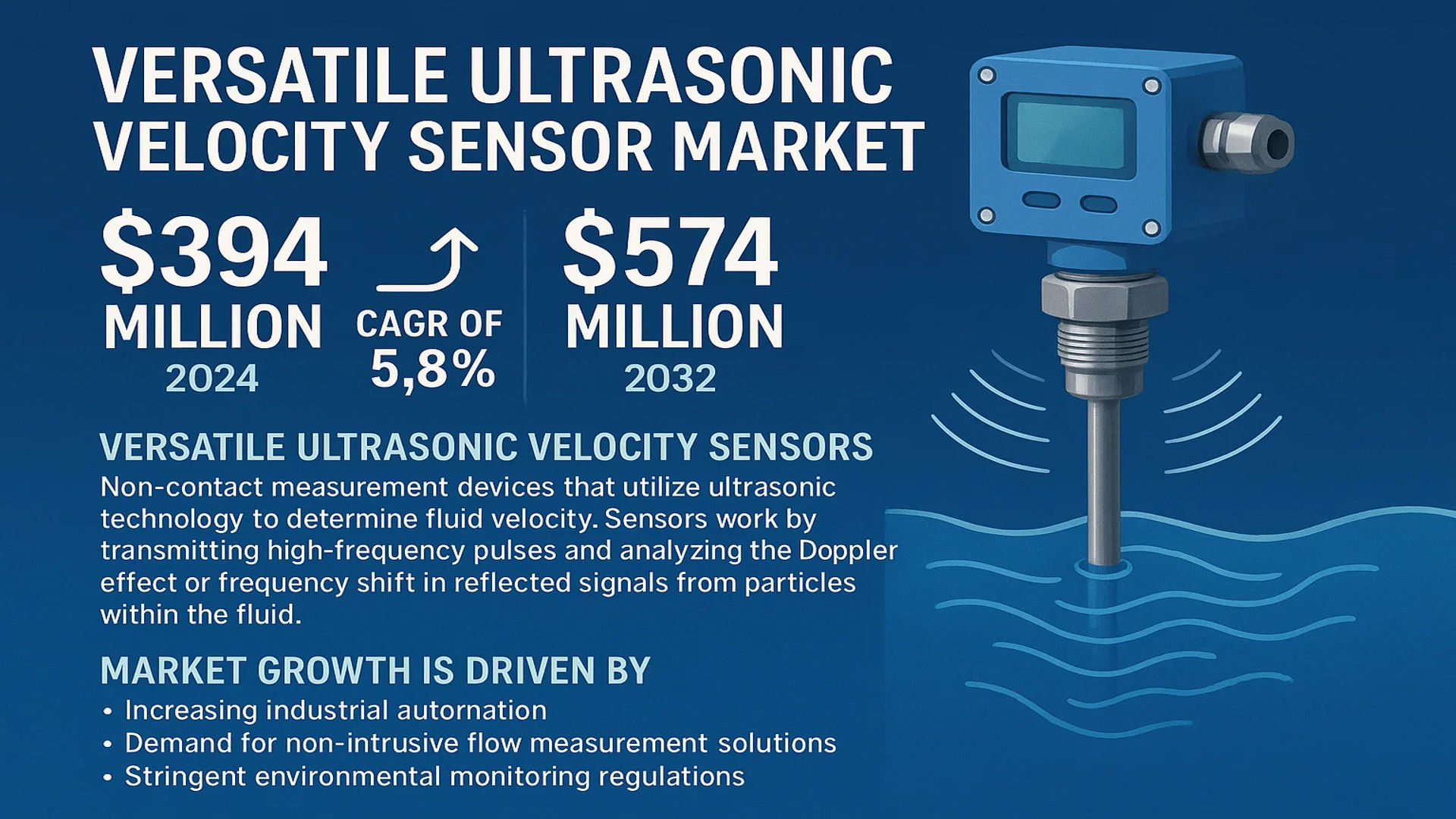

The global Versatile Ultrasonic Velocity Sensor Market was valued at 394 million in 2024 and is projected to reach US$ 574 million by 2032, at a CAGR of 5.8% during the forecast period.

Versatile ultrasonic velocity sensors are non-contact measurement devices that utilize ultrasonic technology to determine fluid velocity. These sensors work by transmitting high-frequency ultrasonic pulses and analyzing the Doppler effect or frequency shift in reflected signals from particles within the fluid. They provide real-time flow measurements with temperature and pressure compensation, making them ideal for applications requiring precise fluid dynamics monitoring.

The market growth is driven by increasing industrial automation, demand for non-intrusive flow measurement solutions, and stringent environmental monitoring regulations. The industrial sector dominates application demand due to widespread use in process control and fluid management systems. Key manufacturers like Bosch, Siemens, and Honeywell are investing in advanced sensor technologies to enhance measurement accuracy and reliability. The Doppler-type segment currently leads market share due to its versatility across different fluid types and operating conditions.

MARKET DYNAMICS

MARKET DRIVERS

Accelerated Industrial Automation to Fuel Demand for Ultrasonic Velocity Sensors

The global push towards industrial automation is significantly driving the adoption of versatile ultrasonic velocity sensors. These sensors play a critical role in modern manufacturing environments by enabling non-contact measurement of fluid velocities in pipelines, automotive assembly lines, and chemical processing plants. The industrial automation market has shown robust growth with automation spending increasing by over 12% annually since 2020. Ultrasonic sensors, with their ability to operate in harsh environments and measure without physical contact, have become indispensable components in smart factories implementing Industry 4.0 principles.

Growing Environmental Monitoring Requirements Boost Market Expansion

Stringent environmental regulations across multiple industries are creating substantial demand for accurate flow measurement solutions. Versatile ultrasonic velocity sensors are increasingly deployed for monitoring water treatment processes, air flow in HVAC systems, and industrial emissions. The environmental sensor market is projected to grow at approximately 7% CAGR through 2030, with ultrasonic technology gaining significant share due to its reliability and maintenance-free operation. Municipal water systems globally are upgrading to ultrasonic-based monitoring to comply with stricter environmental standards and reduce water loss through leakage detection.

Advancements in Doppler Technology Enhance Adoption Rates

Recent technological improvements in Doppler-type ultrasonic sensors are expanding their application scope. Modern sensors now offer measurement accuracy within ±0.5% of reading, even in challenging fluid conditions with low particle concentrations. The Doppler segment currently accounts for nearly 65% of the ultrasonic velocity sensor market, with adoption growing rapidly in sectors requiring precise flow measurements. These sensors are proving particularly valuable in pharmaceutical manufacturing where they enable non-invasive monitoring of critical processes without risk of contamination.

MARKET RESTRAINTS

High Initial Costs Limit Adoption in Price-Sensitive Markets

While ultrasonic velocity sensors offer numerous advantages, their relatively high cost compared to traditional mechanical flow meters remains a significant market barrier. The average price point for industrial-grade ultrasonic sensors is approximately 30-50% higher than conventional alternatives. This pricing disparity is particularly challenging in developing economies where budget constraints often dictate purchasing decisions. The initial investment includes not only the sensor hardware but also specialized installation and calibration services, creating additional financial hurdles for smaller operations.

Technical Limitations in Certain Applications Constrain Market Growth

Ultrasonic velocity sensors face performance limitations in specific operating conditions that restrict their universal adoption. In applications involving highly aerated liquids or fluids with extreme viscosity variations, measurement accuracy can deteriorate significantly. These technical challenges are particularly apparent in food processing and wastewater treatment scenarios where fluid properties vary widely. Additionally, the sensors require minimum pipe diameters and straight run lengths for optimal performance, which may not always be feasible in retrofit applications.

Integration Challenges with Legacy Systems Create Adoption Barriers

The transition from traditional measurement systems to ultrasonic solutions often encounters compatibility issues with existing industrial control architectures. Many facilities face substantial costs and operational disruptions when upgrading their monitoring infrastructure to accommodate modern ultrasonic sensors. These integration challenges are compounded by the shortage of skilled technicians capable of configuring and maintaining sophisticated ultrasonic measurement systems. In certain industries with established practices, resistance to adopting new technologies further slows market penetration.

MARKET OPPORTUNITIES

Emerging Smart City Infrastructure Offers Significant Growth Potential

The global smart city initiatives present a substantial opportunity for versatile ultrasonic velocity sensor manufacturers. Urban water management systems, intelligent transportation networks, and building automation all require advanced flow monitoring solutions. With smart city investments expected to exceed $2 trillion by 2025, ultrasonic sensors are positioned to play a crucial role in these infrastructure projects. Their ability to provide reliable, long-term measurement without maintenance makes them ideal for embedded applications in smart utility networks.

Expansion of Automotive Applications Creates New Market Space

The automotive industry’s shift toward electrification and advanced driver assistance systems (ADAS) is opening new application areas for ultrasonic sensors. Beyond traditional fluid measurement, these sensors are increasingly used for vehicle speed detection, parking assistance, and obstacle avoidance systems. The automotive ultrasonic sensor market is projected to grow at over 8% annually through 2030, with vehicle manufacturers incorporating more sensors per unit to meet safety and efficiency requirements. This expansion into automotive applications represents a significant diversification opportunity for sensor manufacturers.

Energy Sector Modernization Drives Demand for Advanced Monitoring Solutions

The global energy sector’s transition toward renewable sources and efficiency improvements is creating strong demand for precise flow measurement technologies. Ultrasonic velocity sensors are becoming essential components in solar thermal plants, geothermal systems, and hydrogen fuel infrastructure. The ability to measure diverse fluids accurately under varying pressure and temperature conditions makes them particularly valuable in these emerging energy applications. With renewable energy investments reaching record levels, sensor manufacturers have significant opportunities to develop specialized solutions for these growing markets.

MARKET CHALLENGES

Supply Chain Constraints Impact Sensor Manufacturing and Delivery

The global semiconductor shortage and supply chain disruptions continue to affect ultrasonic velocity sensor production. Critical components including transducers and signal processing chips face lead times extending up to 40 weeks in some cases. These constraints are particularly challenging for manufacturers serving time-sensitive industrial automation projects. The situation is compounded by rising raw material costs, with prices for specialized piezoelectric materials increasing by approximately 15-20% in recent years.

Intense Competition from Alternative Technologies Pressures Pricing

Ultrasonic velocity sensors face growing competition from emerging measurement technologies including laser Doppler velocimetry and advanced electromagnetic flow meters. These alternatives are achieving comparable accuracy in certain applications while often requiring less complex installation. The competitive landscape is driving price erosion in standard ultrasonic sensor products, putting pressure on manufacturer margins. This trend is particularly evident in the mid-range industrial market segment where cost sensitivity is high.

Standards and Certification Requirements Create Market Entry Barriers

The increasing complexity of industry certifications and regional compliance standards presents significant challenges for sensor manufacturers. Obtaining approvals for hazardous area installations (ATEX, IECEx), drinking water applications (NSF), and medical uses requires substantial investment in testing and documentation. These requirements disproportionately affect smaller manufacturers and new market entrants, potentially limiting innovation and competition in the sector. The certification process for a single sensor model in multiple regions can take 12-18 months and cost hundreds of thousands of dollars.

VERSATILE ULTRASONIC VELOCITY SENSOR MARKET TRENDS

Integration of AI and IoT Elevates Sensor Capabilities

The Versatile Ultrasonic Velocity Sensor Market is undergoing a significant transformation with the integration of Artificial Intelligence (AI) and Internet of Things (IoT) technologies. AI-enhanced signal processing improves the accuracy of flow velocity measurements by reducing interference and optimizing Doppler echo analysis. Meanwhile, IoT connectivity enables real-time monitoring and predictive maintenance in industrial applications such as wastewater management and HVAC systems. The growing adoption of Industry 4.0 has accelerated demand, with ultrasonic velocity sensors becoming essential for smart factory automation. The global market is projected to grow at a 5.8% CAGR through 2032, driven by these technological advancements.

Other Trends

Expanding Industrial Automation Demand

Increasing automation across manufacturing, oil & gas, and chemical processing sectors is fueling the need for non-contact flow measurement solutions. Ultrasonic velocity sensors offer advantages like minimal maintenance and compatibility with corrosive fluids, making them preferable over traditional mechanical flowmeters. The Doppler-type segment, which dominates over 42% of the market, sees particularly strong adoption in pipeline monitoring due to its ability to track suspended particles in liquids without direct flow interruption.

Environmental Monitoring Applications Surge

Regulatory pressures for water conservation and emission control are driving ultrasonic sensor deployment in environmental monitoring systems globally. These sensors provide critical flow data for river discharge measurements, wastewater treatment efficiency tracking, and air velocity monitoring in stack emissions. In China, government mandates for industrial pollution control have triggered 12% year-over-year growth in sensor installations at environmental compliance facilities. The frequency difference type sensors are gaining traction in these applications due to their high precision in clean fluid measurements.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation Drives Competition in Ultrasonic Velocity Sensor Market

The global versatile ultrasonic velocity sensor market exhibits a moderately consolidated competitive structure, dominated by established electronics giants and specialized sensor manufacturers. Bosch leads the market with approximately 18% revenue share in 2024, leveraging its expertise in automotive applications and industrial sensing solutions. The company’s recent release of the FCH-series ultrasonic sensors with enhanced Doppler processing capabilities has strengthened its market position.

SICK AG and Honeywell follow closely, collectively accounting for around 25% of the market. These companies benefit from their strong distribution networks and customization capabilities for industrial applications. SICK’s focus on environmental monitoring solutions and Honeywell’s aerospace-grade sensors have created distinct competitive advantages in their respective niches.

The market also features several strategic partnerships aimed at technology integration. Siemens recently collaborated with semiconductor leader Infineon to develop next-generation ultrasonic velocity sensors with embedded AI capabilities for predictive maintenance applications. Such collaborations are reshaping competitive dynamics and accelerating product innovation cycles.

Meanwhile, Asian manufacturers like Sony Semiconductor and Nippon-seiki are gaining traction through cost-competitive offerings, particularly in the consumer electronics and automotive sectors. Their growth strategies emphasize miniaturization and power efficiency – critical factors for battery-operated devices.

List of Key Versatile Ultrasonic Velocity Sensor Manufacturers

- Robert Bosch GmbH (Germany)

- SICK AG (Germany)

- Texas Instruments Inc. (U.S.)

- STMicroelectronics (Switzerland)

- Infineon Technologies (Germany)

- Honeywell International Inc. (U.S.)

- Sony Semiconductor Solutions Corporation (Japan)

- Siemens AG (Germany)

- Nippon-seiki Co., Ltd. (Japan)

- TE Connectivity (Switzerland)

Segment Analysis:

By Type

Doppler Type Segment Leads Due to High Accuracy in Flow Measurement

The market is segmented based on type into:

- Doppler Type

- Subtypes: Single-Beam, Dual-Beam, and Multi-Beam

- Frequency Difference Type

- Subtypes: Transit-Time, Phase-Shift, and others

- Others

By Application

Industrial Segment Dominates Due to Widespread Use in Process Automation

The market is segmented based on application into:

- Industrial

- Subtypes: Oil & Gas, Chemical, Water Treatment, and others

- Security

- Subtypes: Surveillance, Intrusion Detection, and others

- Environmental Monitoring

- Others

By Technology

Non-invasive Technology Gains Traction Due to Better Reliability

The market is segmented based on technology into:

- Non-invasive

- Invasive

- Hybrid

By End User

Manufacturing Sector Holds Major Share Due to Industrial Automation Adoption

The market is segmented based on end user into:

- Manufacturing

- Oil & Gas

- Utilities

- Government & Defense

- Others

Regional Analysis: Versatile Ultrasonic Velocity Sensor Market

Asia-Pacific

Asia-Pacific dominates the global Versatile Ultrasonic Velocity Sensor market, accounting for the largest revenue share in 2024. China leads the region due to its expanding industrial automation sector and investments in smart manufacturing under initiatives like Made in China 2025. The country’s focus on environmental monitoring and water management solutions further drives demand for ultrasonic sensors. India shows rapid adoption, particularly in wastewater treatment plants and process industries, supported by government infrastructure projects. Japan and South Korea contribute significantly with their advanced robotics and automation sectors. While cost sensitivity limits premium sensor adoption in some areas, technological advancements and regional manufacturing growth position Asia-Pacific for continued leadership.

North America

The North American market is characterized by high-value applications in oil & gas, aerospace, and smart city projects. Stringent regulations on emission monitoring and pipeline safety (e.g., U.S. DOT PHMSA standards) accelerate ultrasonic sensor deployment. The U.S. holds over 60% of the regional market share, with increasing R&D investments in non-contact measurement technologies. Canada’s mining and water resource sectors present key growth opportunities, while Mexico’s industrial expansion fuels demand. However, market maturity in certain sectors and competition from alternative technologies create moderate growth challenges.

Europe

Europe’s market thrives on strict industrial efficiency standards and sustainability mandates. Germany remains the largest consumer, driven by its automotive and manufacturing sectors implementing Industry 4.0 solutions. The EU’s focus on reducing industrial wastewater discharge (per Water Framework Directive) boosts environmental monitoring applications. France and the U.K. show strong adoption in security systems and building automation. Nordic countries lead in developing compact, low-power sensors for harsh environments. Though growth is steady, higher costs compared to Asian alternatives impact price-sensitive segments.

South America

Market growth in South America is tempered by economic fluctuations but shows potential in mining and agriculture applications. Brazil accounts for nearly half of regional demand, with ultrasonic sensors used in food processing and hydroelectric plants. Argentina’s oil extraction projects and Chile’s mining operations present niche opportunities. However, limited local manufacturing and reliance on imports hinder widespread adoption. Political instability and currency volatility further challenge market expansion, though gradual infrastructure improvements support long-term growth.

Middle East & Africa

The region exhibits emerging but uneven growth. Gulf nations (UAE, Saudi Arabia) drive demand through smart city projects and desalination plant expansions. Ultrasonic sensors see increasing use in oil pipeline monitoring and HVAC systems. Africa’s market remains underdeveloped but shows promise in water resource management, particularly in South Africa and Nigeria. Limited technical expertise and budget constraints slow adoption, though partnerships with global manufacturers are gradually improving market penetration in key sectors.

Report Scope

This market research report provides a comprehensive analysis of the Global Versatile Ultrasonic Velocity Sensor Market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market was valued at USD 394 million in 2024 and is projected to reach USD 574 million by 2032 at a CAGR of 5.8%.

- Segmentation Analysis: Detailed breakdown by product type (Doppler Type, Frequency Difference Type, Others), application (Industrial, Security, Environmental Monitoring, Others), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa. The U.S. and China are key growth markets.

- Competitive Landscape: Profiles of leading participants including Bosch, SICK, TI, STMicro, Infineon, Honeywell, Sony, Siemens, Nippon-seiki and TE Connectivity, covering their market share, product portfolios, and strategic developments.

- Technology Trends & Innovation: Assessment of ultrasonic measurement technologies, integration with IoT systems, and advancements in fluid dynamics sensing.

- Market Drivers & Restraints: Evaluation of factors including industrial automation growth, environmental monitoring needs, and technical challenges in sensor accuracy.

- Stakeholder Analysis: Strategic insights for sensor manufacturers, system integrators, and industrial end-users regarding market opportunities.

The report employs primary and secondary research methodologies, including expert interviews and analysis of verified market data, to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Versatile Ultrasonic Velocity Sensor Market?

->Versatile Ultrasonic Velocity Sensor Market was valued at 394 million in 2024 and is projected to reach US$ 574 million by 2032, at a CAGR of 5.8% during the forecast period.

Which key companies operate in this market?

-> Key players include Bosch, SICK, TI, STMicro, Infineon, Honeywell, Sony, Siemens, Nippon-seiki, and TE Connectivity.

What are the key growth drivers?

-> Growth is driven by industrial automation, environmental monitoring needs, and advancements in ultrasonic sensing technology.

Which region dominates the market?

-> Asia-Pacific shows the fastest growth, while North America and Europe remain significant markets.

What are the emerging trends?

-> Emerging trends include integration with Industry 4.0 systems, miniaturization of sensors, and development of multi-parameter sensing solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...