Vehicle control units market Insights

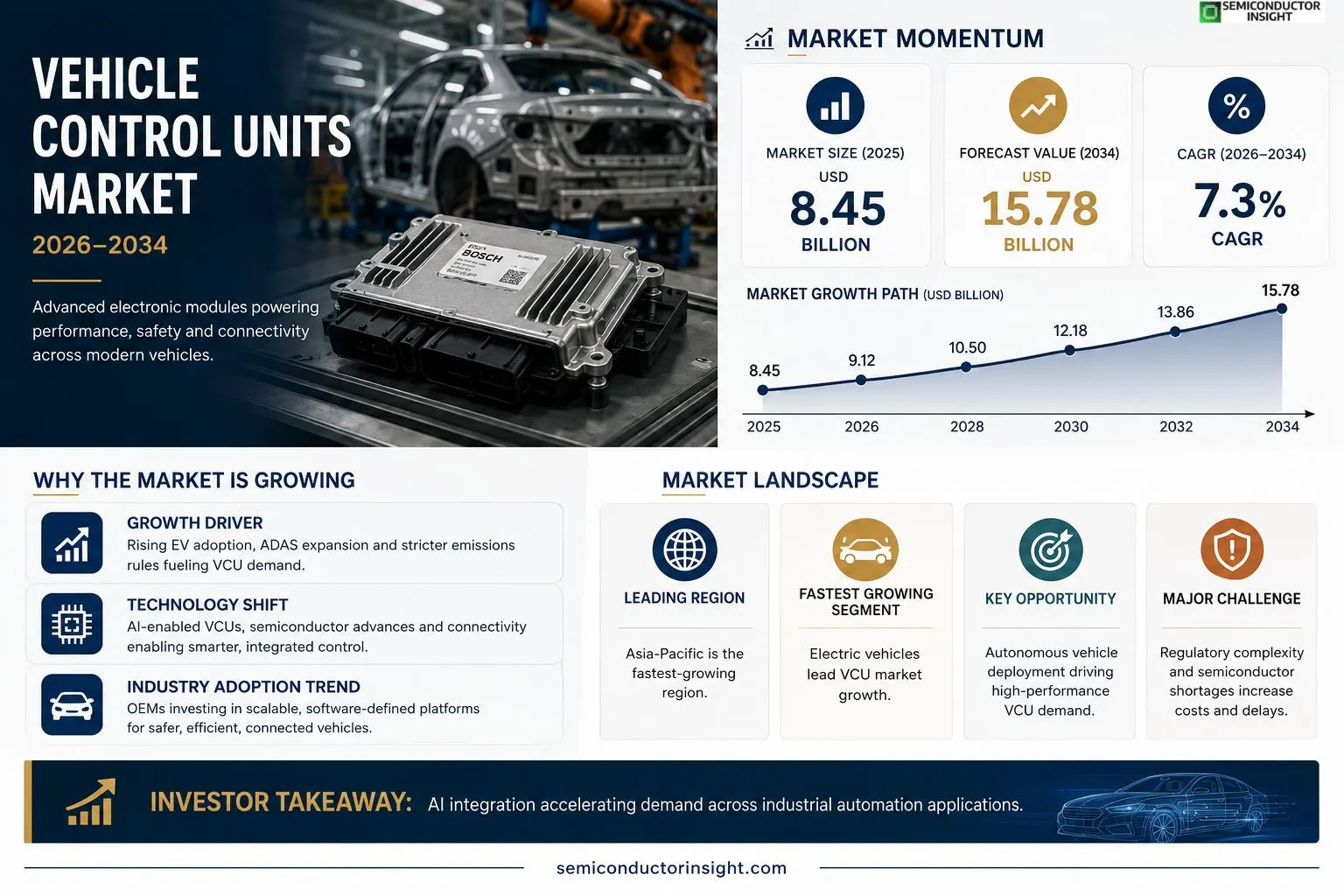

Vehicle control units market size was valued at USD 8.45 billion in 2025. The market is projected to grow from USD 9.12 billion in 2026 to USD 15.78 billion by 2034, exhibiting a CAGR of 7.3% during the forecast period.

Vehicle control units are sophisticated electronic modules that coordinate power‑train functions, battery management, braking systems and driver‑assist features within modern automobiles. These units integrate microcontrollers, sensors and software algorithms to ensure optimal performance, safety and energy efficiency across conventional and electric vehicles.The market is experiencing rapid growth due to several factors, including rising adoption of electric vehicles, increased investment in advanced driver‑assistance systems (ADAS), and stringent emissions regulations worldwide.

Furthermore, advancements in semiconductor technology and connectivity are driving demand for more capable VCUs.

Initiatives by key players such as Bosch, which recently launched an AI‑enabled VCU platform , Continental’s partnership with Tesla for next‑generation powertrain integration, and Denso’s expansion of its VCU portfolio are expected to further accelerate market expansion.

MARKET DRIVERS

Increasing Adoption of Advanced Driver Assistance Systems

The Vehicle control units market is being propelled by the rapid integration of Advanced Driver Assistance Systems (ADAS) across new vehicle models. In 2024, approximately 95 million vehicles were produced worldwide, and an estimated 75 % of them were equipped with at least one ADAS feature, creating a sizable demand for reliable control units that manage sensor fusion and real‑time decision making.

Electrification and Connectivity Growth

Electrified powertrains and high‑speed vehicle‑to‑infrastructure communication require sophisticated VCUs to orchestrate battery management, motor control, and over‑the‑air updates. Forecasts suggest that electric vehicle sales will exceed 30 % of total new car registrations by 2027, directly expanding the addressable market for integrated control solutions.

➤ “Control unit scalability will define the next generation of autonomous platforms, driving a compound annual growth rate above 10 % through 2032.”

Combined, these trends elevate the strategic importance of Vehicle control units market, compelling OEMs to invest in modular architectures that can support both safety‑critical functions and future software‑defined capabilities.

MARKET CHALLENGES

Regulatory Complexity

Regulators across North America, Europe, and Asia present divergent functional safety and cybersecurity requirements, forcing manufacturers to certify each VCU variant for multiple standards such as ISO 26262 and UNECE R155. This fragmented compliance landscape drives up validation costs and extends product launch timelines.

Other Challenges

Supply Chain Constraints

The semiconductor shortage that began in 2020 continues to affect the availability of microcontrollers and power‑management ICs essential for VCUs. Limited wafer allocations and longer lead times compel OEMs to adopt risk‑mitigation strategies, including dual‑source agreements and inventory buffering.

MARKET RESTRAINTS

High Development Costs

Designing VCU platforms that meet stringent safety, emissions, and over‑the‑air update criteria demands extensive R&D investment. Development budgets for a single next‑generation control unit can exceed $50 million, creating a financial barrier for smaller suppliers and limiting market entry to well‑capitalized players.

MARKET OPPORTUNITIES

Autonomous Vehicle Deployment

As Level 3 and Level 4 autonomous driving prototypes transition to commercial fleets, the need for high‑performance, redundant VCUs escalates. Companies that can deliver safety‑rated, fail‑operational control units integrated with AI acceleration are positioned to capture a growing share of Vehicle control units market, especially in emerging mobility‑as‑a‑service (MaaS) ecosystems.

Vehicle control units market Trends

Electrification Accelerates VCU Adoption

Modern vehicles rely on sophisticated electronic modules that coordinate power‑train functions, battery management, braking, and driver‑assist features. As electric vehicle penetration rises worldwide, the demand for highly integrated control units grows in parallel. Manufacturers are replacing legacy mechanical systems with compact, software‑driven solutions that can manage higher voltage architectures and support fast‑charging strategies. The shift also encourages tighter integration with thermal‑management and energy‑recovery subsystems, elevating overall vehicle efficiency while meeting stricter emissions standards. These dynamics position Vehicle control units market as a focal point for automotive OEMs seeking to balance performance, safety, and regulatory compliance.

Other Trends

Advanced Driver‑Assistance Integration

Advanced driver‑assistance systems (ADAS) increasingly depend on real‑time data processing and sensor fusion. Vehicle control units now embed high‑performance microcontrollers capable of executing AI‑based algorithms for lane‑keeping, adaptive cruise control, and automated emergency braking. This convergence reduces wiring complexity and improves response latency, which is critical for safety‑critical functions. Leading suppliers such as Bosch and Continental are expanding their VCU portfolios with AI‑enabled platforms that can be over‑the‑air updated, ensuring that vehicles remain compliant with evolving software standards throughout their lifecycle.

Semiconductor & Connectivity Advances

The ongoing transition to next‑generation semiconductor technologies, including silicon carbide (SiC) and gallium nitride (GaN), is reshaping the architecture of vehicle control units. These materials provide higher power density and lower thermal losses, enabling more compact designs that support both conventional and electric powertrains. Simultaneously, the rise of vehicle‑to‑everything (V2X) communication mandates that VCUs incorporate robust connectivity stacks, allowing seamless interaction with cloud services, traffic infrastructure, and other road users. By embedding secure communication protocols and over‑the‑air update capabilities, manufacturers can future‑proof their platforms while delivering new functionalities without physical recalls.

COMPETITIVE LANDSCAPEKey Industry Players

Vehicle control units market Competitive Overview

Vehicle control units (VCU) market is dominated by a handful of electronics and automotive suppliers that combine deep semiconductor expertise with automotive system integration. Bosch remains the de‑facto market leader, leveraging its extensive sensor portfolio and AI‑enabled VCU platform to capture a large share of both ICE and EV segments. Continental follows closely, especially after its strategic partnership with Tesla that accelerates next‑generation powertrain integration. Denso’s expanding VCU suite and ZF Friedrichshafen’s focus on drivetrain electrification further cement the top‑tier structure, where scale, R&D intensity, and OEM relationships define competitive advantage. These incumbents benefit from economies of scale, allowing them to invest in advanced silicon and software stacks that meet stringent safety and emissions standards across major automotive markets.Beyond the core leaders, a vibrant cohort of niche and specialist players intensifies competition by targeting specific functions or vehicle segments. Valeo and Aptiv concentrate on ADAS‑linked VCU solutions, while NXP Semiconductors and Infineon Technologies supply high‑performance microcontrollers and power management ICs that underpin VCU architectures. Magna International and Hyundai Mobis offer system‑level integration services, and Renesas Electronics and Texas Instruments provide cost‑effective MCU families for entry‑level models. Foxconn (Hon Hai) is rapidly scaling its automotive electronics footprint, Mitsubishi Electric supplies robust power modules for commercial vehicles, and TE Connectivity delivers critical connectivity components. This diversified ecosystem ensures continual innovation and pricing pressure across the market.

List of Key Vehicle Control Units Companies Profiled

- Bosch

- Continental

- Denso

- ZF Friedrichshafen

- Valeo

- NXP Semiconductors

- Infineon Technologies

- Aptiv

- Magna International

- Hyundai Mobis

- Renesas Electronics

- Texas Instruments

- Foxconn (Hon Hai)

- Mitsubishi Electric

- TE Connectivity

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Powertrain VCUs are central to vehicle performance, providing precise control over engine and motor functions.

|

| By Application |

|

Electric Vehicles drive innovation in VCU design, demanding higher computational power and energy‑aware algorithms.

|

| By End User |

|

OEMs prioritize integration flexibility and scalability in VCU platforms.

|

| By Architecture |

|

Hybrid Architecture is gaining traction for its balance of performance and redundancy.

|

| By Connectivity |

|

Automotive Ethernet is reshaping VCU communication strategies.

|

Regional Analysis: North America

United States

The integration of artificial intelligence (AI) and machine learning (ML) into VCUs is enabling more intelligent and autonomous driving capabilities. This includes features such as adaptive cruise control, lane keeping assist, and automated emergency braking. The development of high-performance processors and communication protocols is crucial for handling the increasing computational demands of modern VCUs.

Stringent environmental regulations, particularly those related to emissions, are driving innovation in VCU technology. Safety regulations also play a significant role, requiring VCUs to incorporate advanced safety features and ensure reliable performance. The evolving regulatory landscape necessitates continuous adaptation and compliance by VCU manufacturers.

The supply chain for VCUs is complex and interconnected. Disruptions in the supply chain, such as semiconductor shortages, can significantly impact VCU production and availability. Manufacturers are increasingly focusing on diversifying their supply chains and building strategic partnerships to mitigate these risks.

The VCU market is highly competitive, with a mix of established players and emerging companies vying for market share. Competition is primarily based on technological innovation, product performance, and cost-effectiveness. Consolidation within the industry is also observed, with mergers and acquisitions shaping the competitive landscape.

Europe

The European VCU market is characterized by a strong emphasis on sustainability and technological innovation. Driven by ambitious emissions targets and a growing electric vehicle segment, the demand for advanced VCUs is steadily increasing. Key trends in the European market include the development of highly integrated VCUs, the adoption of sophisticated diagnostic tools, and the focus on enhancing vehicle connectivity. Government incentives and regulations supporting the transition to electric mobility are further boosting the VCU market. Business strategies in Europe involve close collaboration with automotive OEMs and suppliers, as well as investments in R&D to meet evolving regulatory requirements. The European market is also witnessing a growing interest in cybersecurity solutions for VCUs, reflecting the increasing importance of protecting vehicle systems from cyber threats. The shift towards autonomous driving is creating new opportunities for advanced VCUs with enhanced capabilities.

Asia-Pacific

The Asia-Pacific region represents the largest and fastest-growing market for Vehicle Control Units ly. Driven by rapid industrialization, increasing automotive production, and a rising demand for modern vehicles, the VCU market in Asia-Pacific is witnessing significant expansion. China is the dominant player in this region, with a massive automotive market and a strong focus on domestic VCU production. Other key markets include Japan, South Korea, and India. Trends in the Asia-Pacific VCU market include the increasing adoption of electric vehicles and connected car technologies, the development of cost-effective VCUs for mass-market vehicles, and the growing emphasis on localization of VCU production. Business strategies in the Asia-Pacific market emphasize building strong relationships with local automotive manufacturers and leveraging cost advantages in manufacturing. The region is also witnessing a surge in investments in R&D for advanced VCU technologies.

South America

The South American VCU market is experiencing moderate growth, driven by increasing automotive sales and a growing demand for safety and convenience features. The market is characterized by a mix of established and emerging automotive manufacturers. Key trends include the adoption of cost-effective VCUs for entry-level vehicles and the increasing demand for advanced safety systems. Government regulations related to vehicle safety and emissions are also influencing the market. Business strategies in South America involve focusing on providing value-for-money VCUs and establishing strong distribution networks. The region is also witnessing a growing interest in aftermarket VCUs.

Middle East & Africa

The Middle East and Africa VCU market is characterized by growth potential, driven by increasing automotive sales and rising disposable incomes. The market is seeing a growing demand for vehicles with advanced features, including safety and connectivity technologies. Key trends include the adoption of VCUs for hybrid and electric vehicles and the increasing focus on cybersecurity. Government investments in infrastructure and automotive manufacturing are also contributing to market growth. Business strategies in this region involve focusing on building partnerships with local automotive manufacturers and providing customized VCU solutions. The market is relatively price-sensitive, with a strong demand for cost-effective VCUs.

Report Scope

This market research report provides a comprehensive analysis of the Vehicle control units market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real‑time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Vehicle control units market?

-> Vehicle control units market was valued at USD 8.45 billion in 2025 and is expected to reach USD 15.78 billion by 2034.

Which key companies operate in Vehicle control units market?

-> Key players include Bosch, Continental, Denso, among others.

What are the key growth drivers?

-> Key growth drivers include rising adoption of electric vehicles, increased investment in advanced driver‑assistance systems (ADAS), stringent emissions regulations, advancements in semiconductor technology and connectivity.

Which region dominates the market?

-> Asia‑Pacific is the fastest‑growing region, while Europe remains a dominant market.

What are the emerging trends?

-> Emerging trends include AI‑enabled VCU platforms, powertrain integration partnerships, and expanded VCU portfolios incorporating advanced connectivity.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...