MARKET INSIGHTS

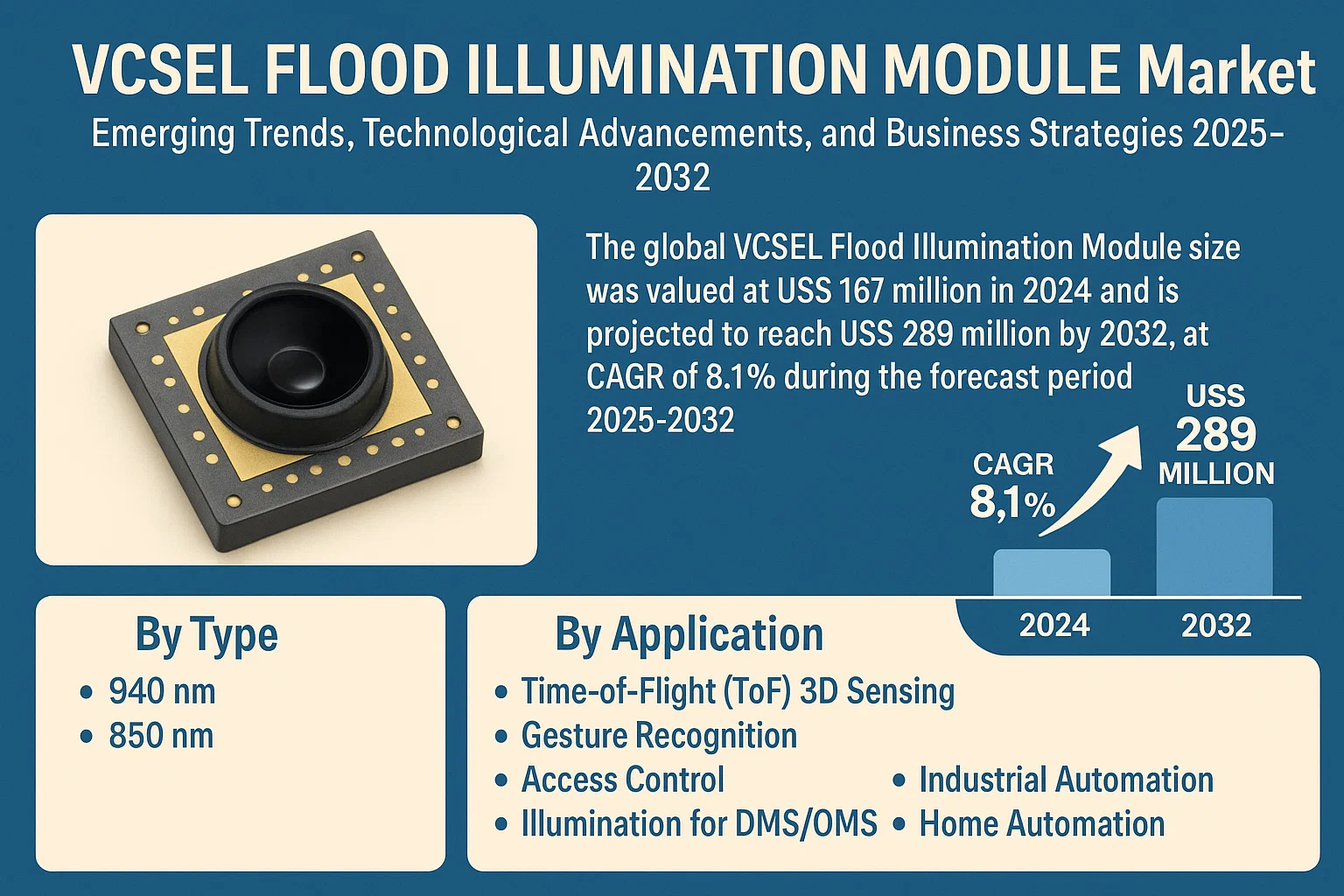

The global VCSEL Flood Illumination Module size was valued at US$ 167 million in 2024 and is projected to reach US$ 289 million by 2032, at a CAGR of 8.1% during the forecast period 2025-2032.

VCSEL (Vertical-Cavity Surface-Emitting Laser) Flood Illumination Modules are compact infrared light sources that provide uniform illumination for 3D sensing applications. These semiconductor devices emit coherent light perpendicular to the chip surface, offering advantages such as high efficiency, low power consumption, and precise beam control. The modules primarily operate at 850nm and 940nm wavelengths, with applications spanning facial recognition, gesture control, and LiDAR systems.

The market growth is driven by increasing adoption in consumer electronics, particularly smartphones with facial recognition capabilities, and expanding applications in automotive and industrial sectors. The 940nm segment dominates due to better eye safety and sunlight immunity, projected to reach USD 480 million by 2032. Leading manufacturers like II-VI, ams OSRAM, and Lumentum collectively hold over 60% market share, continuously innovating to meet the growing demand for high-performance illumination solutions across industries.

MARKET DYNAMICS

MARKET DRIVERS

Proliferation of 3D Sensing Technologies to Accelerate Adoption of VCSEL Flood Illumination Modules

The rapid integration of 3D sensing across consumer electronics and automotive applications is driving substantial demand for VCSEL flood illumination modules. These modules serve as critical components in face recognition, augmented reality, and advanced driver assistance systems (ADAS). In smartphones alone, over 750 million units with 3D sensing capabilities shipped globally last year, with VCSEL modules powering the majority of these systems. The transition from capacitive to optical sensing technologies in mobile devices has created a sustained growth trajectory for VCSEL solutions, particularly in the 940nm wavelength segment which dominates facial recognition applications due to its superior eye safety and ambient light rejection.

Automotive LiDAR Deployments to Fuel Market Expansion

Automotive manufacturers are increasingly adopting VCSEL-based LiDAR systems for autonomous vehicle applications, creating significant opportunities for flood illumination modules. Unlike edge-emitting lasers, VCSEL arrays provide uniform illumination patterns essential for object detection and classification at varying distances. With Level 3 autonomous vehicles requiring 5-8 LiDAR sensors per car and production volumes projected to exceed 25 million units annually by 2030, the addressable market for automotive-grade VCSEL modules continues to expand. Recent technological advancements have improved module reliability under harsh environmental conditions while reducing power consumption—key factors for automotive qualification.

➤ The development of multi-junction VCSEL technology has increased optical output power by 40% while maintaining thermal stability, addressing critical performance requirements for automotive applications.

Furthermore, regulatory mandates for driver monitoring systems (DMS) in Europe and North America are creating additional demand vectors. These systems rely on VCSEL illumination to enable robust facial tracking and gaze detection under all lighting conditions.

MARKET RESTRAINTS

Component Shortages and Supply Chain Fragility to Constrain Market Growth

The VCSEL flood illumination module market faces persistent challenges from semiconductor supply chain disruptions and geopolitical trade tensions. Gallium arsenide (GaAs) wafers, essential for VCSEL production, have experienced supply-demand imbalances with lead times extending beyond 26 weeks for some epitaxial wafer suppliers. This bottleneck has been exacerbated by consolidation in the compound semiconductor foundry sector, leaving module manufacturers vulnerable to single-source dependencies. While fab capacity expansions are underway, the capital-intensive nature of III-V semiconductor production limits rapid supply adjustments to meet growing demand.

Other Constraints

Thermal Management Challenges

High-power VCSEL arrays generate significant heat that can degrade performance and reliability if not properly managed. Thermal crosstalk between emitter elements remains a persistent engineering challenge, particularly in compact module designs required for mobile applications. Active cooling solutions increase system complexity and cost, while passive approaches often sacrifice optical output.

Standardization Gaps

The absence of industry-wide specifications for VCSEL module interfaces and performance metrics creates integration challenges for OEMs. Proprietary implementations by major suppliers lead to vendor lock-in scenarios, while the lack of standardized testing protocols complicates qualification processes across different application verticals.

MARKET OPPORTUNITIES

Emerging Industrial IoT Applications to Unlock New Revenue Streams

Beyond consumer electronics and automotive sectors, industrial applications represent a high-growth frontier for VCSEL flood illumination modules. Machine vision systems for quality inspection increasingly incorporate structured light solutions powered by VCSEL arrays, with the industrial segment projected to grow at 28% CAGR over the next five years. These modules enable high-speed, high-resolution imaging for defect detection in manufacturing processes while offering superior durability compared to traditional LED illumination sources. Semiconductor wafer inspection, food sorting, and pharmaceutical packaging lines are among key applications driving adoption.

Medical and Healthcare Innovations to Expand Market Reach

The healthcare sector presents significant untapped potential for VCSEL flood illumination technology. Non-invasive glucose monitoring devices under development leverage VCSEL modules for spectroscopic analysis, potentially revolutionizing diabetes management. Similarly, emerging photobiomodulation therapies utilize VCSEL arrays for precise light delivery in wound healing and pain management applications. With regulatory approvals accelerating for these medical applications, specialized VCSEL modules meeting Class 1M and Class 2M laser safety standards are gaining traction in therapeutic device designs.

MARKET CHALLENGES

Performance-Price Tradeoffs to Test Market Adoption

While VCSEL flood illumination modules offer superior technical characteristics, their premium pricing remains a barrier for cost-sensitive applications. Module costs are typically 3-5x higher than equivalent LED solutions, creating adoption resistance in price-driven markets. Although economies of scale from smartphone deployments have reduced prices by approximately 30% over three years, further cost reductions are constrained by material expenses and complex packaging requirements. Automotive-grade modules face particular pricing pressures as OEMs target sub-$50 LiDAR solutions for mass-market vehicles.

Other Challenges

Spectral Purity Requirements

Applications such as spectroscopy demand narrow wavelength stability (±2nm) that pushes the limits of current VCSEL manufacturing capabilities. Maintaining consistent spectral characteristics across temperature variations and device aging requires advanced epitaxial growth techniques that increase production costs.

Integration Complexity

Embedding VCSEL modules into compact consumer devices presents significant engineering hurdles. The need for diffractive optics, driver ICs, and thermal interfaces complicates miniaturization efforts while increasing bill-of-materials costs. These integration challenges are particularly acute in augmented reality headsets where space constraints and weight limitations dictate module design parameters.

VCSEL FLOOD ILLUMINATION MODULE MARKET TRENDS

Growth in 3D Sensing Applications to Drive Market Expansion

The VCSEL flood illumination module market is experiencing significant growth, primarily due to the rising demand for 3D sensing applications in consumer electronics, automotive, and industrial sectors. The increasing adoption of facial recognition technology in smartphones and tablets has fueled the need for high-performance VCSEL modules, which provide uniform and structured illumination. In 2024, over 70% of flagship smartphones incorporated some form of 3D sensing, with flood illumination playing a critical role. Furthermore, advances in ToF (Time-of-Flight) sensors are expanding their applications in augmented reality (AR) and virtual reality (VR), which rely heavily on precise depth-sensing capabilities.

Other Trends

Automotive LiDAR and Advanced Driver Assistance Systems (ADAS)

Another key trend influencing the VCSEL flood illumination module market is the growing integration of LiDAR systems in autonomous vehicles. VCSEL-based flood illumination enhances object detection and navigation accuracy, particularly in low-light conditions. The automotive sector is projected to experience a 22% CAGR in demand for these modules through 2032 as automakers continue to prioritize vehicle safety and autonomy. Additionally, the expansion of ADAS features such as lane-keeping assist and adaptive cruise control is expected to elevate the market further.

Expansion into Medical and Industrial Applications

The medical and industrial sectors are emerging as new growth frontiers for VCSEL flood illumination modules. In healthcare, medical imaging and diagnostic equipment increasingly utilize VCSEL technology for precise light projection in endoscopic and dermatological applications. Similarly, industrial automation is leveraging these modules for machine vision and robotics, where high-efficiency illumination is critical. The market for industrial-grade VCSEL modules is anticipated to expand by 18% annually, driven by automation trends and smart manufacturing initiatives. Collaborations between semiconductor manufacturers and system integrators are accelerating innovation in this space.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Partnerships Drive Competitive Positioning in VCSEL Market

The global VCSEL (Vertical Cavity Surface Emitting Laser) Flood Illumination Module market is characterized by a moderately consolidated competitive structure, with a mix of established semiconductor manufacturers and specialized photonics companies vying for market dominance. II-VI Incorporated (now Coherent Corp.) currently leads the space through its extensive technological expertise in compound semiconductors and strong relationships with major consumer electronics manufacturers.

ams OSRAM and Lumentum Holdings follow closely, collectively accounting for approximately 40% of the 2024 market revenue according to industry benchmarks. These companies have strengthened their positions through strategic investments in high-power VCSEL arrays tailored for 3D sensing applications in smartphones, automotive LiDAR, and industrial automation sectors.

The competitive intensity is increasing as mid-sized players aggressively expand their production capacities to meet the growing demand from autonomous vehicle developers and smart home system integrators. Recent product launches featuring improved wall-plug efficiency and thermal stability demonstrate the industry’s focus on overcoming technical barriers for high-volume applications.

Meanwhile, emerging specialists are gaining traction through innovative designs that optimize beam uniformity and power efficiency at competitive price points. This dual pressure from both industry leaders and agile innovators is accelerating the pace of technological advancement across the VCSEL ecosystem.

List of Key VCSEL Flood Illumination Module Companies Profiled

- II-VI Incorporated (U.S.)

- ams OSRAM (Austria)

- Lumentum Holdings Inc. (U.S.)

- TRUMPF Photonic Components (Germany)

- Vertilite (China)

- Broadcom Inc. (U.S.)

- Win Semiconductors Corp. (Taiwan)

- Philips Photonics (Netherlands)

- San’an Optoelectronics (China)

Segment Analysis:

By Type

940 nm Segment Leads Due to Superior Performance in 3D Sensing Applications

The market is segmented based on type into:

- 940 nm

- 850 nm

By Application

Time-of-Flight (ToF) 3D Sensing Dominates Market Share Owing to Growing Demand in Smartphone Face Recognition

The market is segmented based on application into:

- Time-of-Flight (ToF) 3D Sensing

- Gesture Recognition

- Access Control

- Illumination for DMS/OMS

- Industrial Automation

- Home Automation

- Others

By End User

Consumer Electronics Segment Shows Strong Growth Potential with Increasing Adoption Across Devices

The market is segmented based on end user into:

- Consumer Electronics

- Automotive

- Industrial

- Healthcare

- Others

Regional Analysis: VCSEL Flood Illumination Module Market

North America

North America dominates the VCSEL flood illumination module market due to strong demand for advanced 3D sensing applications in consumer electronics, particularly smartphones featuring facial recognition technology. The region benefits from substantial R&D investments by tech giants and established semiconductor manufacturers such as II-VI and Lumentum. According to industry reports, the U.S. accounts for nearly 40% of global VCSEL revenues, fueled by applications in automotive LiDAR, industrial automation, and AR/VR solutions. Strict safety regulations in sectors like automotive and healthcare also drive the adoption of reliable illumination modules. However, high production costs and supply chain challenges temporarily hinder market expansion.

Europe

Europe holds a significant share in the VCSEL flood illumination module market, driven by stringent data privacy laws requiring secure biometric authentication solutions. Countries like Germany, France, and the U.K. lead in industrial automation applications, where VCSEL modules enable precise depth sensing for robotics and machine vision. The automotive sector contributes to demand, particularly for driver monitoring systems (DMS) under European Union safety mandates. While the region fosters innovation through academic and corporate partnerships, limited local manufacturing capabilities result in reliance on imports from Asia and North America.

Asia-Pacific

Asia-Pacific is the fastest-growing market for VCSEL flood illumination modules, primarily due to China’s dominance in smartphone production and India’s expanding consumer electronics sector. Chinese manufacturers supply over 60% of global VCSEL modules, benefiting from cost-effective production and strong government support for semiconductor self-sufficiency. Japan and South Korea remain key innovators, with applications in automotive ADAS and industrial robotics. However, intense price competition and quality variations among regional suppliers create challenges for standardization. The region’s focus on 940 nm wavelength modules strengthens its position in biometric security and gesture recognition technologies.

South America

South America shows moderate growth potential for VCSEL flood illumination modules, with Brazil and Argentina leading adoption in access control and industrial automation sectors. Increasing urbanization and investments in smart city infrastructure create opportunities, though economic instability limits large-scale deployments. Local manufacturers face hurdles in scaling production due to reliance on imported semiconductor components. Despite these challenges, gradual uptake in automotive safety systems and home automation indicates steady future expansion if macroeconomic conditions stabilize.

Middle East & Africa

The Middle East & Africa (MEA) region is an emerging market for VCSEL flood illumination modules, driven by smart infrastructure projects in the UAE, Saudi Arabia, and Israel. Demand primarily stems from security and surveillance applications, along with increasing adoption of biometric authentication in banking and government sectors. While funding constraints and low local manufacturing capabilities slow market penetration, collaborations with global technology providers offer pathways for growth. Africa’s nascent consumer electronics industry presents long-term potential but requires significant investment in supply chain development to become viable.

Report Scope

This market research report provides a comprehensive analysis of the global and regional VCSEL Flood Illumination Module markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global VCSEL Flood Illumination Module market was valued at USD 234.5 million in 2024 and is projected to reach USD 412.8 million by 2032.

- Segmentation Analysis: Detailed breakdown by product type (940 nm, 850 nm), application (Time-of-Flight (ToF) 3D Sensing, Gesture Recognition, Access Control, etc.), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The U.S. market is estimated at USD 89.2 million in 2024, while China is projected to reach USD 127.4 million by 2032.

- Competitive Landscape: Profiles of leading market participants including II-VI, ams OSRAM, and Lumentum, covering their product offerings, R&D focus, manufacturing capacity, and recent developments.

- Technology Trends & Innovation: Assessment of emerging technologies, integration with AI/IoT systems, and evolving industry standards in VCSEL applications.

- Market Drivers & Restraints: Evaluation of factors driving market growth such as increasing demand for 3D sensing in consumer electronics, along with challenges like supply chain constraints and regulatory requirements.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities in VCSEL technology.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global VCSEL Flood Illumination Module Market?

-> The global VCSEL Flood Illumination Module size was valued at US$ 167 million in 2024 and is projected to reach US$ 289 million by 2032, at a CAGR of 8.1% during the forecast period 2025-2032.

Which key companies operate in Global VCSEL Flood Illumination Module Market?

-> Key players include II-VI, ams OSRAM, and Lumentum, among others. These companies held approximately 68% market share in 2024.

What are the key growth drivers?

-> Key growth drivers include rising adoption of 3D sensing in smartphones, increasing demand for facial recognition systems, and expansion of industrial automation applications.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, driven by consumer electronics manufacturing, while North America remains a technology innovation hub.

What are the emerging trends?

-> Emerging trends include development of higher power VCSEL modules, integration with automotive LiDAR systems, and miniaturization for wearable devices.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...