MARKET INSIGHTS

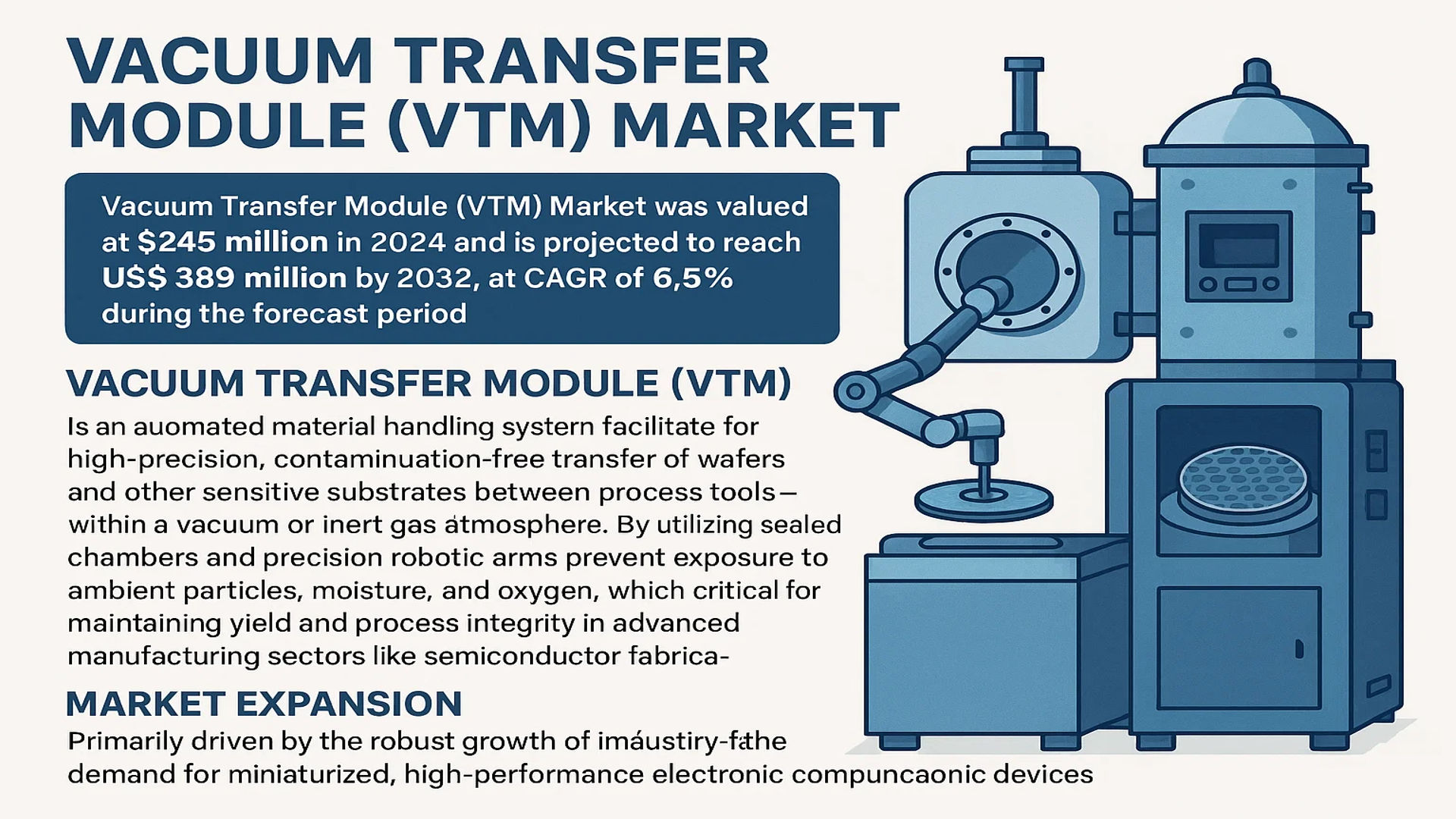

The global Vacuum Transfer Module (VTM) Market was valued at 245 million in 2024 and is projected to reach US$ 389 million by 2032, at a CAGR of 6.5% during the forecast period.

A Vacuum Transfer Module (VTM) is an automated material handling system designed for high-cleanliness environments. These systems facilitate the high-precision, contamination-free transfer of wafers and other sensitive substrates between process tools—such as etchers and thin film deposition equipment—within a vacuum or inert gas atmosphere. By utilizing sealed chambers and precision robotic arms, VTMs prevent exposure to ambient particles, moisture, and oxygen, which is critical for maintaining yield and process integrity in advanced manufacturing sectors like semiconductor fabrication.

Market expansion is primarily driven by the robust growth of the global semiconductor industry and increasing demand for miniaturized, high-performance electronic devices. The transition to larger wafer sizes, particularly the adoption of 300mm technology, necessitates advanced automation and contamination control, further propelling VTM demand. However, the market faces challenges such as high initial costs and technical complexity. Key players, including CYMECHS Inc, Ninebell, and RORZE, are focusing on innovation and strategic collaborations to enhance system reliability and throughput, thereby supporting sustained market growth.

MARKET DYNAMICS

MARKET DRIVERS

Expansion of Semiconductor Manufacturing to Drive Vacuum Transfer Module Adoption

The global semiconductor industry continues to experience robust growth, with manufacturing capacity expansions creating substantial demand for vacuum transfer modules. Semiconductor fabrication facilities require increasingly sophisticated material handling systems to maintain yield rates exceeding 90% in advanced processes. Vacuum transfer modules enable contamination-free transfer of wafers between process chambers, which is critical for nodes below 10nm where even microscopic particles can cause device failures. The transition to larger wafer sizes, particularly the growing adoption of 300mm manufacturing lines, necessitates higher precision transfer systems capable of handling delicate substrates without damage. With semiconductor capital expenditure projected to maintain double-digit growth rates in key manufacturing regions, the demand for reliable vacuum transfer solutions is expected to increase correspondingly.

Advancements in Thin Film Deposition Technologies to Boost Market Growth

Technological innovations in deposition equipment are creating new opportunities for vacuum transfer module integration. Modern deposition systems increasingly incorporate multiple process chambers connected through centralized transfer modules, enabling complex multilayer structures without breaking vacuum. This configuration significantly reduces processing time and improves film quality by eliminating atmospheric exposure between deposition steps. The growing adoption of atomic layer deposition (ALD) and molecular beam epitaxy (MBE) techniques, which require ultra-high vacuum conditions below 10⁻⁹ torr, particularly benefits from integrated vacuum transfer systems. These advanced deposition methods are essential for manufacturing next-generation semiconductor devices, optical coatings, and quantum computing components, driving demand for precision vacuum handling solutions.

Furthermore, the increasing automation of fabrication processes requires seamless integration between different equipment types. Vacuum transfer modules serve as critical interfaces between etchers, deposition systems, and metrology tools, enabling fully automated production lines. This integration reduces human intervention, minimizes contamination risks, and improves overall equipment effectiveness. The trend toward smart manufacturing and Industry 4.0 practices in semiconductor facilities is accelerating the adoption of automated material handling systems with real-time monitoring and predictive maintenance capabilities.

MARKET RESTRAINTS

High Capital Investment Requirements to Limit Market Penetration

The substantial capital expenditure required for vacuum transfer module implementation presents a significant barrier to market expansion. Advanced VTM systems incorporating precision robotics, ultra-high vacuum components, and sophisticated control systems typically represent a considerable portion of overall equipment costs in semiconductor fabrication facilities. This financial barrier is particularly challenging for smaller manufacturers and research institutions operating with constrained budgets. The total cost of ownership extends beyond initial purchase prices to include installation, validation, maintenance, and potential facility modifications to accommodate these systems.

Additionally, the specialized nature of vacuum transfer technology requires significant investment in research and development to maintain competitiveness. Manufacturers must continuously innovate to meet evolving industry requirements for higher throughput, improved reliability, and compatibility with emerging process technologies. These R&D expenditures, combined with the costs associated with obtaining necessary certifications and complying with industry standards, contribute to the overall financial barriers facing both suppliers and end-users in this market segment.

MARKET OPPORTUNITIES

Emerging Applications in Photovoltaics and Display Manufacturing to Create New Growth Avenues

The expansion of vacuum-based processing into new application areas presents significant growth opportunities for vacuum transfer module manufacturers. The photovoltaic industry increasingly adopts vacuum deposition techniques for producing high-efficiency solar cells, particularly in the thin-film and perovskite solar cell segments. These manufacturing processes require controlled environments to prevent contamination and ensure consistent product quality. Similarly, the display manufacturing sector utilizes vacuum transfer systems for organic light-emitting diode (OLED) production, where even minimal oxygen or moisture exposure can degrade device performance.

Advanced packaging technologies represent another promising opportunity, particularly for 2.5D and 3D integration schemes requiring multiple processing steps under controlled environments. The development of heterogeneous integration approaches, which combine different semiconductor materials and technologies within single packages, necessitates sophisticated material handling solutions capable of maintaining process integrity throughout complex manufacturing sequences. These emerging applications demonstrate the potential for vacuum transfer technology expansion beyond traditional semiconductor manufacturing into adjacent high-tech industries.

MARKET CHALLENGES

Technical Complexity and Reliability Requirements to Challenge Market Participants

Vacuum transfer modules must operate with exceptional reliability in demanding production environments, presenting significant engineering challenges. These systems must maintain ultra-high vacuum integrity while performing thousands of transfer cycles without failure. The precision robotics required for wafer handling must operate with micron-level accuracy while minimizing particle generation and maintaining stable performance over extended periods. Achieving these performance benchmarks requires sophisticated engineering solutions and extensive testing, particularly for systems designed for high-volume manufacturing applications.

Other Challenges

Integration Compatibility

Ensuring seamless integration with diverse equipment platforms from multiple manufacturers presents ongoing challenges. The lack of standardized interfaces often requires custom engineering solutions for each installation, increasing implementation complexity and costs. Compatibility issues can arise from differences in software protocols, mechanical interfaces, and vacuum requirements between equipment from different suppliers.

Maintenance and Service Requirements

The specialized nature of vacuum technology necessitates highly trained maintenance personnel and specialized tools for servicing and repair. The limited availability of qualified technicians, particularly in emerging manufacturing regions, can impact equipment uptime and overall productivity. Additionally, the need for regular preventive maintenance and potential spare part availability issues can affect total cost of ownership and operational efficiency.

VACUUM TRANSFER MODULE (VTM) MARKET TRENDS

Rising Demand for Advanced Semiconductor Fabrication to Drive Market Growth

The global Vacuum Transfer Module (VTM) market is experiencing robust growth, primarily fueled by the relentless expansion of the semiconductor industry. As chip manufacturers push towards smaller process nodes, such as the 3nm and upcoming 2nm technologies, the requirement for pristine, contamination-free wafer handling becomes non-negotiable. VTMs are critical in this ecosystem, ensuring wafers are transferred between process tools—like etchers and thin film deposition equipment—without exposure to ambient air, which can introduce defects and compromise yield. This trend is underscored by the global market’s valuation of $245 million in 2024, with projections indicating a climb to $389 million by 2032, representing a steady compound annual growth rate (CAGR) of 6.5%. This growth is intrinsically linked to the capital expenditure cycles of major foundries, where investments in new fabrication facilities equipped with the latest automation directly correlate with increased VTM procurement.

Other Trends

Expansion into Emerging Applications Beyond Traditional Semiconductors

While the semiconductor sector remains the dominant force, VTM technology is finding lucrative new applications in adjacent high-tech manufacturing fields. The display industry, particularly for OLED and micro-LED production, requires similarly stringent contamination controls during the transfer of large, fragile glass substrates. Furthermore, the burgeoning fields of photonics and advanced packaging, including 2.5D and 3D integrated circuits (ICs), are creating fresh demand streams. These applications often involve handling delicate interposers and chiplets that are highly susceptible to particulate and moisture damage, making the hermetic sealing and precision robotics of VTMs indispensable. This diversification is a key strategic focus for leading manufacturers, mitigating reliance on the sometimes-volatile semiconductor capital equipment cycle.

Technological Innovation and Automation Integration

Technological innovation is a paramount trend, with manufacturers relentlessly focusing on enhancing VTM performance metrics. Key development areas include increasing transfer speed to improve overall equipment effectiveness (OEE), enhancing positioning accuracy to sub-micron levels for next-generation nodes, and integrating sophisticated real-time particle monitoring systems. There is a significant push towards the adoption of Artificial Intelligence (AI) and machine learning for predictive maintenance, which can analyze vibration data from robotic arms to forecast failures before they occur, minimizing unplanned downtime. Additionally, the industry is moving towards greater standardization and modular designs to reduce integration complexity and cost for equipment manufacturers. This wave of innovation is crucial for supporting the high-volume manufacturing requirements of modern fabs and is a primary differentiator among the top market players.

Geographic Shift and Supply Chain Considerations

A notable geographic shift is underway, significantly influencing the VTM market landscape. While the United States remains a technological leader and a substantial market, the Asia-Pacific region, particularly China, is demonstrating explosive growth. This is a direct consequence of massive government and private investments aimed at achieving semiconductor self-sufficiency and expanding domestic manufacturing capacity. Such concentrated regional growth presents both opportunities and challenges, including potential supply chain bottlenecks for critical components and intensified competition among global and local suppliers. Navigating these geographic dynamics, including trade policies and local content requirements, has become an essential aspect of strategic planning for all companies operating within this market.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Focus on Technological Innovation and Strategic Expansion to Maintain Market Position

The global Vacuum Transfer Module (VTM) market exhibits a semi-consolidated competitive structure, characterized by the presence of both established multinational corporations and emerging specialized manufacturers. This dynamic landscape is driven by intense R&D investment and strategic partnerships aimed at capturing larger market shares in the rapidly evolving semiconductor and high-precision manufacturing sectors. While the market remains accessible to new entrants due to ongoing technological innovations, leading players maintain dominance through extensive product portfolios and robust global distribution networks.

CYMECHS Inc. and RORZE Corporation are recognized as pivotal players in the VTM market, primarily due to their advanced technological capabilities and significant market penetration across key regions including Asia and North America. These companies have established strong reputations for reliability and precision in vacuum transfer solutions, catering extensively to the semiconductor fabrication industry. Their continuous innovation in robotic automation and vacuum technology enables them to address the increasingly complex requirements of next-generation manufacturing processes.

Meanwhile, Ninebell and SIASUN Robot & Automation Co., Ltd. have demonstrated remarkable growth, leveraging their expertise in automation and robotics to secure substantial market shares. Their expansion strategies often include tailored solutions for specific applications such as etching and thin film deposition, allowing them to effectively compete with larger incumbents. These companies benefit from strong regional support, particularly in the Asian market where semiconductor manufacturing investments are accelerating.

Additionally, several specialized manufacturers including Wuxi Fortrend Engineering and Suzhou Honghu Semiconductor Technology are strengthening their market presence through focused innovations and strategic collaborations. These players often target niche segments within the VTM market, offering customized solutions that address unique customer requirements. Their agility and customer-centric approaches enable them to compete effectively despite the presence of larger competitors.

The competitive environment is further intensified by ongoing technological advancements and increasing demand for higher precision and efficiency in material handling. Companies are increasingly investing in R&D to develop next-generation VTMs with enhanced capabilities such as higher throughput, improved contamination control, and greater compatibility with diverse manufacturing equipment. This focus on innovation is crucial for maintaining competitive advantage as customer expectations continue to evolve.

List of Key Vacuum Transfer Module (VTM) Companies Profiled

- CYMECHS Inc. (South Korea)

- Ninebell (South Korea)

- RORZE Corporation (Japan)

- Alemnis AG (Switzerland)

- Suzhou Honghu Semiconductor Technology Co., Ltd. (China)

- Shanghai Mountain Automation Technology Co., Ltd. (China)

- Sihemicro (China)

- Wuxi Fortrend Engineering Co., Ltd. (China)

- SIASUN Robot & Automation Co., Ltd. (China)

- Shanghai Hirokawa Co., Ltd. (China)

- Shanghai Super Electronics Technology Co., Ltd. (China)

Segment Analysis:

By Type

300mm VTM Segment Dominates the Market Due to High Adoption in Advanced Semiconductor Fabrication

The market is segmented based on type into:

- 200mm VTM

- 300mm VTM

- Others

By Application

Thin Film Deposition Equipment Segment Leads Due to Critical Role in Semiconductor Manufacturing Processes

The market is segmented based on application into:

- Etcher

- Thin Film Deposition Equipment

- Others

By End-User Industry

Semiconductor Manufacturing Segment Holds Largest Share Due to Extensive Use in Wafer Fabrication Facilities

The market is segmented based on end-user industry into:

- Semiconductor Manufacturing

- Flat Panel Display Production

- Solar Cell Manufacturing

- Research and Development Facilities

- Others

By Technology

Atmospheric-to-Vacuum Transfer Segment Leads Owing to its Critical Function in Multi-Chamber Systems

The market is segmented based on technology into:

- Atmospheric-to-Vacuum Transfer

- Vacuum-to-Vacuum Transfer

- Loadlock Systems

- Others

Regional Analysis: Vacuum Transfer Module (VTM) Market

Asia-Pacific

The Asia-Pacific region is the undisputed leader in the global VTM market, driven by its dominant semiconductor manufacturing ecosystem. Countries like Taiwan, South Korea, and China are at the forefront, housing the world’s most advanced semiconductor fabrication plants (fabs). This concentration of high-volume production, particularly for leading-edge nodes below 10nm, creates immense demand for precision automation equipment like VTMs. The region’s growth is fueled by massive government and private investments in expanding fab capacity, such as initiatives under China’s “Made in China 2025” policy and significant corporate spending by giants like TSMC and Samsung. While cost competitiveness remains a key driver, there is a parallel and accelerating push toward developing and adopting more sophisticated, high-throughput VTMs to support next-generation chip production, including those for artificial intelligence and high-performance computing applications.

North America

The North American market is characterized by high-value, innovation-driven demand, primarily from the United States. The market is propelled by the reshoring and onshoring of semiconductor manufacturing, heavily supported by legislation like the CHIPS and Science Act, which allocates over $52 billion in incentives and R&D funding. This strategic push aims to bolster domestic supply chain security and reduce reliance on foreign foundries. Consequently, demand is strongest for advanced VTMs compatible with the latest process technologies being developed by Intel and other IDMs (Integrated Device Manufacturers) and for equipment used in compound semiconductor and MEMS fabrication. The focus is on systems offering superior reliability, minimal downtime, and seamless integration with other tools in highly automated fab lines.

Europe

Europe’s VTM market is a hub for specialized, high-mix manufacturing. The region has a strong presence in power semiconductors, sensors, MEMS, and photonics, which often involves smaller batch sizes and a diverse range of substrates compared to high-volume logic or memory fabs. This creates a distinct demand profile for VTMs that offer flexibility, high precision, and compatibility with a variety of process tools beyond just etching and deposition. European equipment manufacturers and research institutes, such as those within the Imec ecosystem, are also key drivers of innovation, often requiring custom or highly adaptable VTM solutions for R&D and pilot production lines. The market is further supported by EU initiatives aimed at strengthening its strategic autonomy in key technology areas.

South America

The VTM market in South America is in a nascent stage of development. The region’s semiconductor industry is limited, with most manufacturing focused on assembly, testing, and packaging rather than front-end wafer fabrication. This results in minimal demand for high-end VTMs. Any existing demand is typically met through imports for specific niche applications, maintenance of older equipment, or small-scale R&D facilities. Economic volatility and a lack of large-scale, coordinated national semiconductor strategies have historically hindered the development of a significant local market for such advanced capital equipment.

Middle East & Africa

Similar to South America, the Middle East & Africa region represents an emerging and highly limited market for VTMs. While some nations, particularly in the Gulf Cooperation Council (GCC), are making substantial investments in technology diversification and building technology hubs, these efforts are currently focused on downstream industries and software. The establishment of a significant semiconductor fabrication base requiring VTMs is a long-term ambition rather than a current reality. Any market activity is confined to very specific research projects or highly specialized industrial applications, with demand being met entirely through international suppliers.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Vacuum Transfer Module (VTM) markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Vacuum Transfer Module (VTM) Market?

-> Vacuum Transfer Module (VTM) Market was valued at 245 million in 2024 and is projected to reach US$ 389 million by 2032, at a CAGR of 6.5% during the forecast period.

Which key companies operate in Global Vacuum Transfer Module (VTM) Market?

-> Key players include CYMECHS Inc, Ninebell, RORZE, Alemnis, Suzhou Honghu Semiconductor Technology, Shanghai Mountain, Sihemicro, Wuxi Fortrend Engineering, SIASUN Robot & Automation Co., Ltd, Shanghai Hirokawa, and Shanghai Super Electronics Technology, among others.

What are the key growth drivers?

-> Key growth drivers include increasing semiconductor manufacturing complexity, demand for contamination-free wafer handling, expansion of 300mm fabrication facilities, and the global push for advanced chip production capabilities.

Which region dominates the market?

-> Asia-Pacific dominates the market, driven by substantial semiconductor manufacturing investments in China, Taiwan, South Korea, and Japan, while North America shows significant growth due to recent semiconductor fabrication expansion initiatives.

What are the emerging trends?

-> Emerging trends include integration of AI for predictive maintenance, development of multi-chamber VTMs for cluster tools, increased adoption of 300mm systems, and enhanced robotics for higher throughput and precision.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...