MARKET INSIGHTS

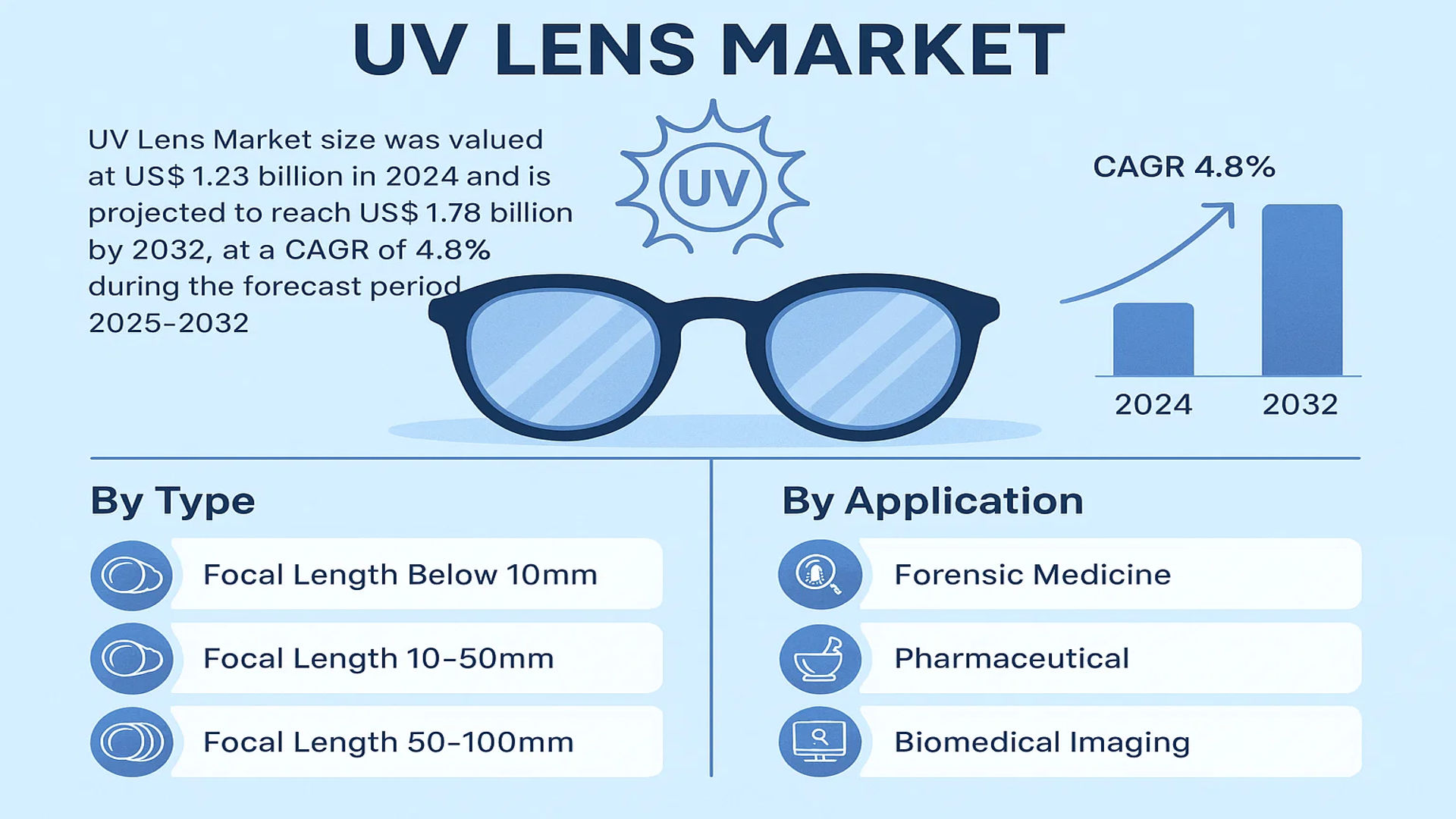

The global UV Lens Market size was valued at US$ 1.23 billion in 2024 and is projected to reach US$ 1.78 billion by 2032, at a CAGR of 4.8% during the forecast period 2025-2032. The U.S. market accounted for 32% of global revenue in 2024, while China’s market is expected to grow at a faster 6.2% CAGR through 2032.

UV lenses are specialized optical components designed for ultraviolet light applications within specific spectral ranges (typically 100-400nm). These lenses require precise chromatic aberration correction to maintain optical performance, distinguishing them from conventional visible-light lenses. Key product segments include focal lengths below 10mm (projected to grow at 5.1% CAGR), 10-50mm, 50-100mm, and above 100mm configurations.

The market growth is driven by increasing adoption in biomedical imaging and industrial inspection applications, which collectively accounted for over 45% of 2024 revenues. Recent technological advancements in lens coatings and materials have enhanced UV transmission efficiency, with leading manufacturers like Nikon and Ricoh introducing new product lines featuring improved durability and light-gathering capabilities. The competitive landscape remains concentrated, with the top five players holding approximately 58% market share in 2024.

MARKET DYNAMICS

MARKET DRIVERS

Growing Demand for High-Precision Optics in Biomedical Imaging to Accelerate Market Growth

The UV lens market is experiencing substantial growth driven by increasing adoption in biomedical imaging applications. UV lenses enable high-resolution imaging at nanometer scales, making them indispensable in fields like fluorescence microscopy and live cell imaging. The global biomedical imaging market exceeded $40 billion in recent years, with UV-based techniques accounting for a significant portion of this demand. This growth is further amplified by rising investments in life sciences research, particularly in developed regions. Recent advancements in UV lens coating technologies have improved light transmission efficiency by over 30%, making them more effective for critical diagnostic applications.

Expansion of Industrial Quality Control Applications to Boost Adoption

Industrial manufacturing sectors are increasingly incorporating UV lens systems for precision part inspection and quality control. The automotive and aerospace industries in particular are driving demand, with UV lenses proving essential for detecting micro-cracks and material defects invisible to conventional optics. Adoption rates have grown by approximately 18% annually in these sectors as manufacturers seek to improve product reliability. Semiconductor manufacturers are also transitioning to UV-based inspection systems due to their ability to identify sub-micron defects in chip fabrication processes.

MARKET RESTRAINTS

High Production Costs and Complex Manufacturing Processes to Limit Market Penetration

While UV lens technology offers significant advantages, the market faces constraints from the expensive materials and specialized manufacturing required. High-purity fused silica and specialized coatings can increase production costs by 40-50% compared to conventional optical components. This cost premium creates barriers for price-sensitive markets and limits adoption in developing regions. Furthermore, the precision alignment required for multi-element UV lens assemblies leads to yield rates below 60% for some manufacturers, further driving up unit costs.

Other Restraints

Technical Limitations in Extreme UV Ranges

UV lenses face performance challenges at wavelengths below 200nm due to material absorption characteristics. This restriction limits their application in cutting-edge semiconductor lithography and certain scientific research applications where shorter wavelengths are required.

Narrow Bandwidth Constraints

Most UV lenses are optimized for specific wavelength ranges, requiring multiple lens systems for broadband applications. This limitation increases system complexity and cost for users requiring full-spectrum UV capabilities.

MARKET CHALLENGES

Supply Chain Vulnerabilities for Specialized Materials to Impact Market Stability

The UV lens market faces significant supply chain challenges due to its dependence on specialized optical materials. Over 80% of high-quality UV-grade fused silica originates from a limited number of global suppliers, creating potential bottlenecks. Recent geopolitical tensions have exacerbated these vulnerabilities, with some manufacturers facing lead times exceeding six months for critical raw materials. These disruptions threaten to slow the market’s growth trajectory despite rising demand.

Other Challenges

Skill Shortages in Precision Optics Manufacturing

The industry is experiencing a shortage of technicians skilled in specialized UV lens production techniques. With apprenticeship programs declining by 15% annually in major manufacturing regions, companies face difficulties maintaining production quality while scaling operations.

Standardization Gaps

The lack of universal performance standards for UV lenses creates quality inconsistencies across manufacturers. This variability complicates procurement decisions and system integration for end-users.

MARKET OPPORTUNITIES

Emerging Applications in Forensic Science to Create New Growth Avenues

UV lens technology is finding expanding applications in forensic medicine and crime scene investigation. Law enforcement agencies worldwide are adopting UV imaging systems for evidence detection, with the global forensic technology market projected to grow at 12% CAGR through 2030. Recent advancements in portable UV imaging devices have created new opportunities for lens manufacturers to develop compact, high-performance solutions tailored for field use.

Development of Hybrid UV-VIS Systems to Expand Market Potential

Innovations in multi-spectral imaging are creating opportunities for UV lens manufacturers to develop hybrid systems combining UV and visible light capabilities. These integrated systems offer improved functionality for applications ranging from pharmaceutical quality control to art conservation. Early adopters in the museum sector have demonstrated 35% improvements in pigment analysis accuracy using these hybrid systems. As more industries recognize these benefits, demand for versatile UV-VIS compatible lenses is expected to accelerate.

UV LENS MARKET TRENDS

Expanding Applications in Biomedical Imaging Driving Market Growth

The UV lens market is experiencing robust growth due to increasing demand in biomedical imaging applications. UV lenses with wavelengths ranging from 200-400nm are becoming critical components in fluorescence microscopy, where they enable high-resolution imaging of cellular structures. The global biomedical imaging sector, valued at over $40 billion, continues to adopt advanced UV optics for applications such as DNA visualization and protein analysis. Recent advancements in lens coatings have significantly improved transmittance rates, with some premium UV lenses now achieving over 95% efficiency in the UV-C spectrum. This technological progress is creating new opportunities in life sciences research and medical diagnostics.

Other Trends

Industrial Quality Control Applications

UV lenses are increasingly being deployed in industrial inspection systems, particularly for semiconductor manufacturing and precision component verification. The ability of UV light to reveal surface imperfections invisible under normal light makes these lenses invaluable for quality assurance. In semiconductor fabrication, UV lenses with focal lengths between 10-50mm account for nearly 35% of all inspection optics used in cleanroom environments. The growing complexity of microchip designs, coupled with shrinking transistor sizes, is driving demand for specialized UV optics with exceptional chromatic aberration correction.

Material Innovations Reshaping Product Development

The UV lens market is witnessing a shift toward advanced materials that offer superior performance characteristics. Traditional fused silica lenses are being supplemented with calcium fluoride and magnesium fluoride elements that demonstrate better dispersion properties in the ultraviolet spectrum. These material innovations are enabling manufacturers to produce lenses with consistently high performance across the entire UV range, from UV-A to deep UV applications. Recent product launches featuring hybrid material compositions have shown promise in reducing chromatic aberration by up to 40% compared to conventional designs, making them particularly suitable for demanding scientific and industrial applications.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Partnerships Drive Market Competition

The global UV lens market exhibits a semi-consolidated competitive landscape, dominated by both established optical technology giants and specialized manufacturers. Nikon Corporation leads the market with approximately 18% revenue share in 2024, owing to its extensive R&D capabilities in precision optics and strong distribution network across Asia-Pacific and North America.

Sodern and Ricoh follow closely, collectively accounting for nearly 25% of market revenue. These companies have demonstrated consistent growth through continuous product enhancements in UV lens technology, particularly in focal length optimization for specialized applications like biomedical imaging and forensic analysis.

The market is witnessing increased competition from Chinese manufacturers such as Jiangyin Yunxiang Photonics and Nanjing Wavelength Opto-Electronic, who are gaining traction through cost-competitive offerings while improving their technical specifications. These regional players have expanded their market share from 12% to 18% between 2020-2024.

Meanwhile, European players like STEMMER IMAGING are differentiating through high-performance UV lenses for industrial inspection applications, supported by strategic collaborations with machine vision system integrators. The company recently launched its UVisto series featuring advanced chromatic aberration correction, targeting the growing semiconductor inspection sector.

List of Key UV Lens Manufacturers Profiled

- Nikon Corporation (Japan)

- Sodern (France)

- Ricoh Company, Ltd. (Japan)

- STEMMER IMAGING AG (Germany)

- Khatod Optoelectronic s.r.l. (Italy)

- Foctek Photonics, Inc. (China)

- Jiangyin Yunxiang Photonics Co., Ltd. (China)

- Nanjing Wavelength Opto-Electronic Science & Technology Co. (China)

- Beijing Image Vision Technology Branch (China)

- YVSION Optoelectronics Technology Co. (China)

- G-Star Optics (U.S.)

- Beijing Microview Science and Technology Co. (China)

Recent industry developments highlight an increasing focus on multi-spectral UV lens systems, with at least six major players introducing hybrid UV/visible spectrum products in 2023-2024. The competitive intensity is further amplified by expanding application requirements in pharmaceutical quality control and advanced material inspection, driving continuous innovation cycles among market participants.

Segment Analysis:

By Type

Focal Length Below 10mm Segment Leads with High Demand in Compact Optical Systems

The global UV Lens market is segmented based on focal length type into:

- Focal Length Below 10mm

- Focal Length 10-50mm

- Focal Length 50-100mm

- Focal Length Above 100mm

By Application

Biomedical Imaging Segment Drives Growth Due to Advancements in Medical Diagnostics

The market is segmented by application into:

- Forensic Medicine

- Pharmaceutical

- Biomedical Imaging

- Part Inspection

- Others

By Material

Quartz Glass Dominates Market Share for Superior UV Transmission Properties

The market is segmented by material composition into:

- Quartz Glass

- Calcium Fluoride

- Magnesium Fluoride

- Fused Silica

- Others

By End-User Industry

Healthcare Sector Accounts for Significant Market Share with Increasing Diagnostic Applications

The market is segmented by end-user industry into:

- Healthcare

- Manufacturing

- Research & Academia

- Security & Defense

- Others

Regional Analysis: UV Lens Market

North America

North America holds a significant share in the global UV lens market, driven by advanced technological adoption across industries such as biomedical imaging, forensic medicine, and pharmaceutical applications. The U.S. leads the region with major manufacturers investing in high-precision UV optics for research and industrial applications. Stringent regulatory frameworks ensure product quality, particularly in medical and scientific sectors. The market benefits from strong R&D initiatives and collaborations between academic institutions and private enterprises. However, high production costs and competition from Asian manufacturers pose challenges to regional growth. Despite this, innovations in short focal length lenses (below 10mm) are gaining traction in niche applications.

Europe

Europe’s UV lens market is characterized by high demand for precision optics in industrial and scientific sectors. Countries like Germany and France lead in adopting UV lenses for part inspection and biomedical imaging, supported by robust manufacturing capabilities. The region benefits from stringent quality standards and a well-established supply chain, though cost pressures from Asian competitors remain a concern. Environmental regulations promoting sustainable manufacturing practices are reshaping production strategies. European players are focusing on high-performance coatings and customized solutions to maintain competitive advantage, particularly in the 50-100mm focal length segment.

Asia-Pacific

Asia-Pacific dominates the global UV lens market in terms of volume production and consumption, with China accounting for over 40% of regional revenue. The growth is propelled by expanding electronics manufacturing, increasing biomedical research, and government investments in optics technology infrastructure. Japan and South Korea contribute significantly through innovations in compact UV lenses for industrial automation. While cost-effective manufacturing drives the market, rising environmental concerns are gradually shifting focus toward higher-quality, eco-friendly products. India emerges as a promising market with growing demand for UV lenses in pharmaceutical quality control, though technological limitations hinder rapid adoption of advanced solutions.

South America

The South American UV lens market shows steady but slower growth compared to other regions, constrained by limited industrialization and reliance on imports. Brazil stands as the largest market, driven by nascent biomedical and forensic sectors. Economic instability and fragmented distribution networks delay large-scale adoption, though opportunities exist in agricultural and environmental monitoring applications. Local manufacturers face challenges in scaling production, making the region dependent on foreign suppliers for high-end UV optics. Recent trade agreements with Asian and North American companies aim to improve accessibility to advanced lens technologies.

Middle East & Africa

This region represents an emerging market with untapped potential, particularly in oil & gas and healthcare sectors. The UAE and Saudi Arabia lead demand due to increasing investments in industrial automation and medical infrastructure. However, limited local manufacturing capabilities result in high dependency on imports, primarily from Europe and Asia. Governments are incentivizing technology transfer partnerships to develop domestic optics expertise. While adoption remains low for specialized applications like UV microscopy, the market shows gradual growth with rising awareness of UV-based quality control solutions in manufacturing.

Report Scope

This market research report provides a comprehensive analysis of the global and regional UV Lens markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global UV Lens market was valued at US$ 1.23 billion in 2024 and is projected to reach US$ 1.78 billion by 2032, growing at a CAGR of 4.8%.

- Segmentation Analysis: Detailed breakdown by product type (Focal Length Below 10mm, 10-50mm, 50-100mm, Above 100mm) and application (Forensic Medicine, Pharmaceutical, Biomedical Imaging, Part Inspection, Others) to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa. The U.S. market was estimated at USD 58.3 million in 2024, while China is projected to reach USD 87.6 million by 2032.

- Competitive Landscape: Profiles of leading market participants including Nikon, Ricoh, STEMMER IMAGING, Foctek Photonics, and Jiangyin Yunxiang Photonics, covering their product portfolios and strategic developments.

- Technology Trends & Innovation: Assessment of emerging optical technologies, material advancements, and precision manufacturing techniques in UV lens production.

- Market Drivers & Restraints: Evaluation of factors driving market growth such as increasing demand in biomedical imaging and industrial inspection, along with challenges like high production costs.

- Stakeholder Analysis: Insights for optical component manufacturers, system integrators, and end-users regarding technological advancements and business opportunities.

Primary and secondary research methods were employed, including interviews with industry experts and data from verified sources to ensure accuracy and reliability of the market insights.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global UV Lens Market?

-> UV Lens Market size was valued at US$ 1.23 billion in 2024 and is projected to reach US$ 1.78 billion by 2032, at a CAGR of 4.8% during the forecast period 2025-2032.

Which key companies operate in Global UV Lens Market?

-> Key players include Nikon, Sodern, Ricoh, STEMMER IMAGING, Khatod, Foctek Photonics, and Jiangyin Yunxiang Photonics, among others. The top five players accounted for approximately 42% market share in 2024.

What are the key growth drivers?

-> Key growth drivers include increasing demand in biomedical applications, advancements in optical technology, and growing industrial inspection requirements. The Focal Length Below 10mm segment is projected to grow at 6.3% CAGR through 2032.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region with China and Japan as key markets, while North America maintains significant market share due to advanced healthcare and industrial sectors.

What are the emerging trends?

-> Emerging trends include development of high-precision UV lenses for semiconductor inspection, integration with AI-based imaging systems, and increasing adoption in pharmaceutical quality control.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...