MARKET INSIGHTS

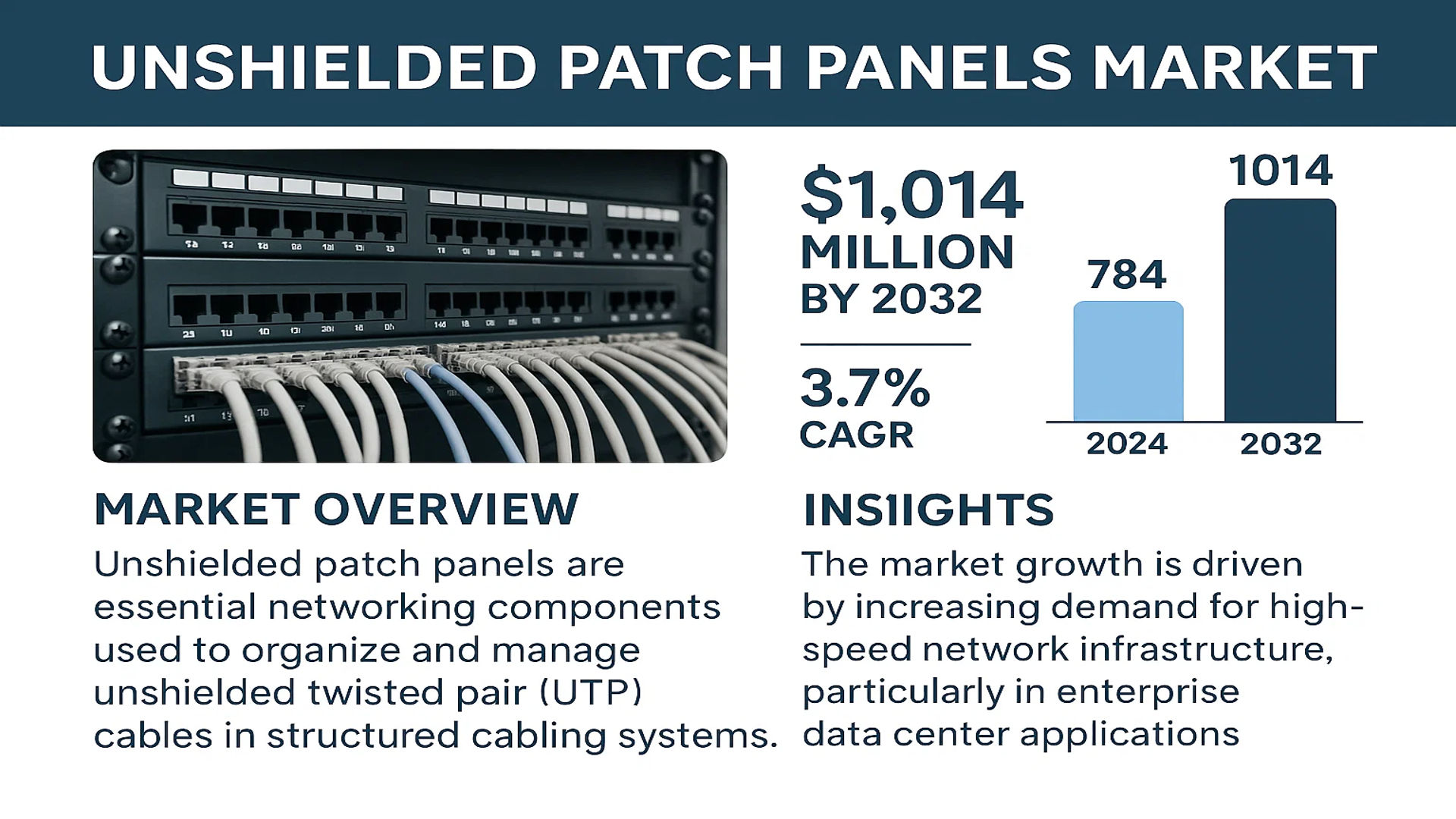

The global Unshielded Patch Panels Market was valued at 784 million in 2024 and is projected to reach US$ 1014 million by 2032, at a CAGR of 3.7% during the forecast period.

Unshielded patch panels are essential networking components used to organize and manage unshielded twisted pair (UTP) cables in structured cabling systems. These panels facilitate efficient cable routing and connectivity in Ethernet networks without the need for additional electromagnetic interference (EMI) or radio frequency interference (RFI) protection. Commonly deployed in cost-sensitive environments, unshielded patch panels are widely used in enterprise IT networks, data centers, and telecommunications infrastructure where EMI/RFI risks are minimal.

The market growth is driven by increasing demand for high-speed network infrastructure, particularly in enterprise and data center applications. While North America currently holds the largest market share, Asia-Pacific is experiencing accelerated adoption due to rapid digital transformation initiatives. Key players like Cisco, Panduit, and CommScope dominate the competitive landscape, collectively accounting for approximately 35% of global revenue in 2024. Recent innovations include high-density designs supporting Cat6 and Cat6a cabling standards to accommodate growing bandwidth requirements.

MARKET DYNAMICS

MARKET DRIVERS

Expansion of Data Centers to Accelerate Adoption of Unshielded Patch Panels

The rapid growth of data centers worldwide is driving significant demand for unshielded patch panels due to their cost-effectiveness and compatibility with high-speed network architectures. With global data center IP traffic projected to grow at a compound annual growth rate exceeding 25% through 2030, network infrastructure investments continue rising to support cloud computing, edge computing, and hyperscale deployments. Unshielded patch panels serve as critical components in these environments, providing reliable cable management and connectivity for Cat5e, Cat6, and Cat6A UTP cabling systems. Major cloud service providers and enterprises increasingly favor these solutions for their standardization benefits and ease of installation in controlled EMI environments.

Growing Enterprise Network Upgrades to Support Market Growth

The ongoing digital transformation across industries is prompting enterprises to upgrade their network infrastructures, creating sustained demand for unshielded patch panel solutions. With businesses investing heavily in smart office technologies, IoT deployments, and unified communications platforms, structured cabling systems require scalable and affordable connectivity solutions. Unshielded patch panels deliver optimal performance for typical enterprise environments where electromagnetic interference remains minimal, offering a price advantage of 20-30% compared to shielded alternatives. The enterprise IT segment accounts for approximately 35% of total patch panel deployments, with particular strength in North American and European markets where commercial building retrofits are occurring at scale.

Advancements in Passive Network Infrastructure Driving Innovation

Manufacturers continue developing enhanced unshielded patch panel designs featuring tool-less termination, improved cable management, and higher port density to meet evolving market needs. Recent product innovations include panels with integrated cable organizers supporting 10GbE and emerging 25GbE standards, as well as modular designs enabling seamless upgrades. The competitive landscape features strong R&D investment from leading vendors, with multiple patents filed annually for improved contact designs and mounting systems. These technological improvements enhance reliability while maintaining the fundamental cost advantages of unshielded solutions in appropriate applications.

MARKET RESTRAINTS

Performance Limitations in High-Interference Environments Restrict Applications

While unshielded patch panels deliver excellent performance in typical office and data center settings, their effectiveness diminishes significantly in environments with substantial electromagnetic interference. Industrial facilities, healthcare imaging centers, and transportation hubs frequently require shielded solutions to maintain signal integrity, limiting the addressable market for unshielded alternatives. Testing indicates that unshielded connectivity solutions experience up to 30% greater signal degradation in high-EMI conditions compared to shielded designs, potentially causing network performance issues that outweigh their cost advantages in sensitive applications.

Increasing Fiber Optic Adoption Poses Competitive Threat

The growing deployment of fiber optic networks represents a structural challenge for copper-based unshielded patch panel solutions. Data centers and enterprises implementing high-speed backbone networks increasingly favor fiber connectivity, particularly for distances exceeding 50 meters or bandwidth requirements above 10Gbps. While copper-based unshielded solutions maintain strong positions in horizontal cabling applications, the fiber optic cable market is projected to grow at nearly double the rate of copper connectivity solutions through the forecast period. This technology shift prompts manufacturers to develop hybrid solutions that combine unshielded copper connectivity with fiber optic capabilities.

MARKET OPPORTUNITIES

Emerging Markets Offer Significant Expansion Potential

Developing economies present substantial growth opportunities as telecommunications infrastructure investments accelerate across Asia, Latin America, and Africa. Government broadband initiatives and private sector network buildouts in these regions favor cost-effective unshielded solutions for initial deployments, particularly in commercial real estate and multi-tenant environments. Market analysis indicates that unshielded patch panel adoption in emerging markets could grow at 5-7% annually through 2032, outpacing mature markets. Manufacturers are establishing local production facilities and distribution partnerships to capitalize on this potential while adapting products to regional standards and installation practices.

Smart Building Deployments Create New Application Areas

The proliferation of smart building technologies is generating demand for structured cabling solutions that can support diverse low-voltage systems. Modern office buildings increasingly utilize unshielded patch panels not only for data networks but also for security systems, building automation controls, and audio-visual installations. This convergence creates opportunities for manufacturers to develop specialized panels featuring color-coded ports, enhanced labeling systems, and integrated power-over-Ethernet support. Market surveys suggest that nearly 40% of new commercial construction projects now incorporate dedicated cabling infrastructure for multiple smart building applications, with unshielded solutions preferred for their flexibility and affordability in these mixed-use deployments.

MARKET CHALLENGES

Supply Chain Volatility Impacts Component Availability

The unshielded patch panel market faces ongoing challenges from global supply chain disruptions affecting raw material availability and production schedules. Copper pricing fluctuations, polymer resin shortages, and semiconductor component delays have created unpredictable lead times for finished products. Industry reports indicate that average delivery times for standard patch panel configurations extended by 2-3 weeks during peak disruption periods, forcing some installers to substitute products or delay projects. Manufacturers are responding with dual-sourcing strategies and inventory buffering, but these measures increase operational costs that may eventually impact consumer pricing structures.

Other Challenges

Skilled Labor Shortages Affect Installation Quality

The growing complexity of structured cabling systems combined with workforce retirements has created installation challenges that can impact product performance. Proper termination and testing of unshielded cabling requires trained technicians, with certification programs struggling to keep pace with industry demand. Poorly installed systems may fail to achieve rated performance levels despite using quality components, potentially undermining confidence in unshielded solutions. Industry associations have responded with expanded training initiatives, but the skills gap remains a persistent challenge across multiple regions.

Regulatory Compliance Adds Design Complexity

Evolving international standards for network infrastructure components require continuous product testing and certification updates. New requirements covering materials flammability, environmental sustainability, and electromagnetic compatibility necessitate regular design revisions across product lines. Compliance with regional variations in telecommunications standards also complicates global product strategies, sometimes requiring separate SKUs for different markets. These regulatory pressures increase product development cycles and testing costs for manufacturers operating in the space.

UNSHIELDED PATCH PANELS MARKET TRENDS

Growing Demand for High-Speed Data Transmission Drives Market Expansion

The increasing need for high-speed data transmission in enterprise IT networks and data centers is propelling the adoption of unshielded patch panels globally. With the global market projected to reach US$ 1014 million by 2032, growing at a CAGR of 3.7%, organizations are investing in cost-effective cabling solutions that support high bandwidth requirements. Unshielded twisted pair (UTP) cables, combined with these panels, are widely used in environments where electromagnetic interference is minimal, such as office networks and small-scale data centers. The U.S. and China are key markets, with China expected to witness significant growth due to rapid digital infrastructure development.

Other Trends

Adoption of Rack-Mountable Panels in Data Centers

The rack-mountable panels segment is anticipated to grow substantially, driven by increasing data center deployments worldwide. These panels offer space efficiency and ease of maintenance, making them ideal for structured cabling in high-density server environments. Cloud service providers and enterprises leveraging hyperscale infrastructure are increasingly opting for unshielded patch panels due to their affordability and compatibility with existing UTP cabling standards. Telecommunications providers also prefer modular patch panels for their scalability in network expansion projects.

Enterprise IT Network Modernization Spurs Demand

The shift toward hybrid work models and digital transformation initiatives is accelerating the modernization of enterprise IT networks. Businesses require reliable, high-performance cabling solutions to support bandwidth-intensive applications such as VoIP, video conferencing, and cloud computing. Unshielded patch panels are preferred in office environments where EMI shielding is unnecessary, offering cost savings of up to 30% compared to shielded alternatives. Furthermore, advancements in Cat 6A and Cat 7 UTP cables enhance transmission speeds, reinforcing the demand for compatible patch panel solutions.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Network Solution Providers Drive Market Growth Through Product Innovation

The global unshielded patch panels market is characterized by intense competition with a mix of established multinational corporations and specialist networking solution providers. Cisco Systems, Inc. dominates the market share with its comprehensive portfolio of networking infrastructure solutions. The company leverages its strong brand presence across enterprise and data center segments, particularly in North America and Europe. In 2024, Cisco account for approximately 18% of the global unshielded patch panel revenue, demonstrating its leadership in the structured cabling ecosystem.

CommScope and Panduit Corporation follow closely as key competitors, each holding significant market positions through their specialized cabling solutions. Panduit’s robust distribution network and CommScope’s recent acquisitions in the connectivity space have strengthened their market positions. These companies collectively account for nearly 30% of market revenue, emphasizing the semi-consolidated nature of the industry.

Medium-sized players like Leviton and Siemon continue to gain traction through product differentiation and regional market expertise. Leviton’s focus on high-density patch panel solutions and Siemon’s emphasis on modular designs have proved successful in capturing niche applications. Meanwhile, emerging competitors are entering the market through competitive pricing strategies and innovative form factors, particularly in Asia-Pacific markets.

The competitive environment continues to evolve as companies invest in R&D for next-generation patch panel solutions. Recent developments include the integration of smart monitoring capabilities and enhanced cable management features, which are becoming critical differentiators in enterprise IT deployments.

List of Key Unshielded Patch Panel Manufacturers

- Cisco Systems, Inc. (U.S.)

- CommScope (U.S.)

- Panduit Corporation (U.S.)

- Leviton (U.S.)

- Siemon (U.S.)

- Belden Inc. (U.S.)

- Hubbell Incorporated (U.S.)

- Netgear (U.S.)

- Vertiv (U.S.)

- Amphenol Corporation (U.S.)

- TE Connectivity (Switzerland)

- Schneider Electric (France)

- Rittal (Germany)

- Eaton (Ireland)

- Broadcom Inc. (U.S.)

Segment Analysis:

By Type

Rack-Mountable Panels Lead the Market Due to Their High Scalability in Data Center Applications

The market is segmented based on type into:

- Rack-Mountable Panels

- Subtypes: 1U, 2U, and larger configurations

- Modular Panels

- Subtypes: Angled and flat designs

- Feed-Through Panels

- Wall-Mount Panels

- Others

By Application

Data Centers Drive Market Growth Due to Expanding Cloud Infrastructure Demands

The market is segmented based on application into:

- Data Centers

- Enterprise IT Networks

- Telecommunications

- Government IT Networks

- Others

By Port Configuration

24-Port and 48-Port Configurations Remain Industry Standards for Network Density

The market is segmented based on port configuration into:

- 12-Port

- 24-Port

- 48-Port

- 96-Port

- Others

By Cable Category

Cat6 and Cat6a Panels See Strong Adoption for High-Speed Network Infrastructure

The market is segmented based on supported cable category into:

- Cat5e

- Cat6

- Cat6a

- Cat7

- Others

Regional Analysis: Unshielded Patch Panels Market

Asia-Pacific

The Asia-Pacific region dominates the unshielded patch panels market, driven by rapid digital transformation and expanding IT infrastructure. Countries such as China, India, and Japan are leading contributors due to their booming telecommunications and data center industries. In China, government initiatives like Digital China 2025 are accelerating demand for structured cabling solutions. Meanwhile, India’s growing adoption of cloud services and enterprise networking solutions is fueling the market. Cost efficiency remains a key factor, making unshielded variants popular, though rising awareness of EMI risks is gradually encouraging hybrid deployments.

North America

As a mature market, North America emphasizes advanced networking solutions within existing infrastructure. The U.S. accounts for the majority of regional demand, supported by large-scale data center expansion and enterprise IT upgrades. Compliance with stringent industry standards like TIA-568 ensures high-quality deployments, while demand for modular and rack-mountable panels is rising among hyperscale data centers. Canada, though smaller in volume, is witnessing steady growth from smart city projects and 5G rollouts. Innovation and scalability are prioritized over cost, distinguishing this market from Asia-Pacific.

Europe

Europe’s emphasis on sustainability and energy-efficient IT infrastructure shapes its unshielded patch panels market. Germany and the U.K. lead in adoption, particularly in enterprise IT networks and colocation facilities. While shielded panels dominate EMI-sensitive environments, unshielded variants remain popular for cost-sensitive applications in SMBs and government IT networks. The EU’s Green Deal indirectly influences the market by promoting cable management solutions that reduce e-waste. Local manufacturers like Rittal and Siemon are investing in modular designs to cater to evolving space constraints in urban data centers.

South America

The South American market is emerging, with Brazil and Argentina representing key demand hubs. Limited IT budget allocations constrain adoption of advanced solutions, but rising investments in broadband infrastructure present opportunities. Telecom operators and educational institutions primarily deploy unshielded patch panels due to their affordability, though inconsistent regulatory oversight and economic volatility hinder large-scale projects. Vendors focus on partnerships with local distributors to navigate the fragmented supply chain.

Middle East & Africa

This region shows niche but growing demand, led by the UAE, Saudi Arabia, and South Africa. Mega-projects like NEOM and expanding data center footprints drive uptake in the Gulf nations, while Africa relies on unshielded panels for basic IT network setups. Challenges include underdeveloped cabling standards and reliance on imports, though local manufacturing initiatives in the UAE aim to reduce costs. Long-term growth is tied to urbanization and digitalization trends across the region.

Report Scope

This market research report provides a comprehensive analysis of the Global Unshielded Patch Panels Market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market was valued at USD 784 million in 2024 and is projected to reach USD 1014 million by 2032, growing at a CAGR of 3.7%.

- Segmentation Analysis: Detailed breakdown by product type (Rack-Mountable Panels, Modular Panels, Feed-Through Panels, Others) and application (Telecommunications, Data Centers, Enterprise IT Networks, Government IT Networks, Others) to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with country-level analysis for key markets including U.S., China, Germany, and Japan.

- Competitive Landscape: Profiles of 16 leading market participants including Cisco, Netgear, Panduit, Leviton, Vertiv, Siemon, Belden, CommScope, Hubbell, and Amphenol, covering their market share, product portfolios, and strategic developments.

- Technology Trends & Innovation: Assessment of evolving cabling standards, integration with next-gen networks, and compatibility with emerging data transmission technologies.

- Market Drivers & Restraints: Evaluation of factors including data center expansion, enterprise network upgrades, and 5G deployment versus challenges from shielded alternatives and fiber optic adoption.

- Stakeholder Analysis: Strategic insights for network equipment manufacturers, IT infrastructure providers, system integrators, and investors regarding market opportunities.

This report combines primary research (industry expert interviews) with secondary research (verified market data) to deliver accurate, actionable intelligence for strategic decision-making.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Unshielded Patch Panels Market?

-> Unshielded Patch Panels Market was valued at 784 million in 2024 and is projected to reach US$ 1014 million by 2032, at a CAGR of 3.7% during the forecast period.

Which key companies operate in Global Unshielded Patch Panels Market?

-> Major players include Cisco, Netgear, Panduit, Leviton, Vertiv, Siemon, Belden, CommScope, Hubbell, and Amphenol, with the top five companies holding significant market share.

What are the key growth drivers?

-> Growth is driven by increasing data center deployments, enterprise network expansions, and cost-effective UTP cable adoption in non-EMI environments.

Which region dominates the market?

-> North America currently leads in market share, while Asia-Pacific is experiencing the fastest growth due to digital infrastructure development.

What are the emerging trends?

-> Emerging trends include high-density panel designs, tool-less installation features, and integration with intelligent network management systems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...