MARKET INSIGHTS

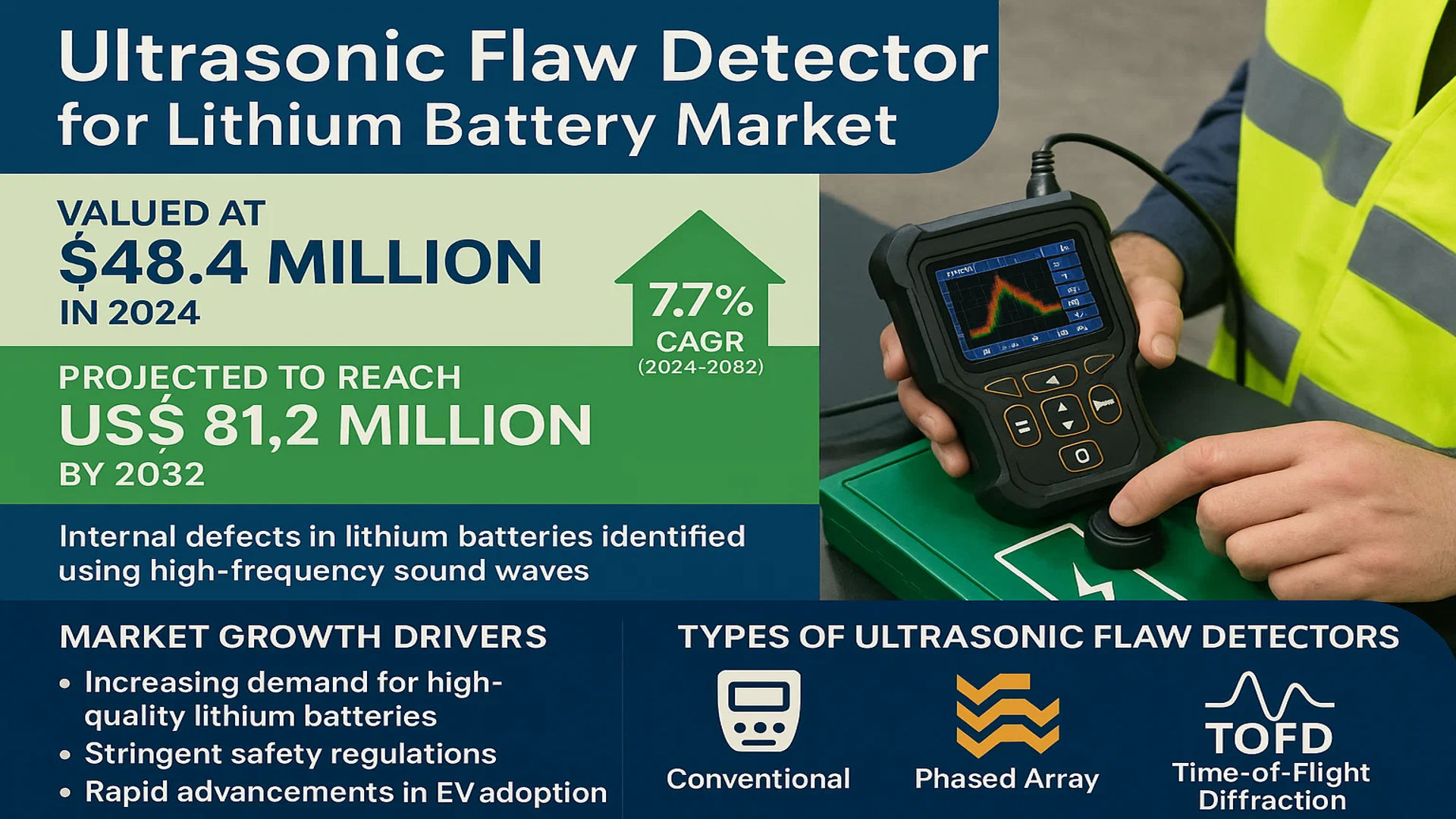

The global Ultrasonic Flaw Detector for Lithium Battery Market was valued at 48.4 million in 2024 and is projected to reach US$ 81.2 million by 2032, at a CAGR of 7.7% during the forecast period.

Ultrasonic flaw detectors are advanced non-destructive testing (NDT) devices designed to identify internal defects in lithium batteries, which are critical for ensuring performance and safety. These devices utilize high-frequency sound waves to detect anomalies such as cracks, voids, and delamination within battery cells, which are common in applications like electric vehicles (EVs), energy storage systems, and consumer electronics. The three primary types of ultrasonic flaw detectors include conventional instruments, phased array detectors, and time-of-flight diffraction (TOFD) detectors, each offering unique advantages in precision and efficiency.

The market growth is driven by increasing demand for high-quality lithium batteries, stringent safety regulations, and rapid advancements in EV adoption. Furthermore, key industry players such as Baker Hughes, Olympus, and Sonatest are expanding their product portfolios and technological capabilities to meet rising market demands. Asia-Pacific, particularly China, dominates the market due to its robust lithium battery manufacturing sector, while North America and Europe are witnessing accelerated growth due to stringent regulatory standards.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for EV Battery Safety to Fuel Market Expansion

The global shift toward electric vehicles is creating unprecedented demand for ultrasonic flaw detection in lithium-ion battery manufacturing. With EV production projected to grow at over 20% annually through 2030, manufacturers are prioritizing battery quality control to prevent thermal runaway incidents. Ultrasonic testing provides critical non-destructive evaluation of electrode layers, welds, and internal structures – detecting micrometer-scale defects that could compromise battery performance and safety. This technology helps producers meet stringent automotive quality standards while reducing warranty claims.

Government Regulations on Battery Safety Standards Accelerating Adoption

Stringent new regulations worldwide are mandating comprehensive battery testing protocols. Regulatory bodies in North America, Europe, and Asia have introduced safety certifications requiring non-destructive testing methods throughout battery production. The UNECE R100 standard for EV batteries, for instance, specifically recommends ultrasonic inspection for detecting internal anomalies. Such regulations create binding requirements that directly increase market demand for advanced flaw detection systems. Manufacturers investing in ultrasonic testing equipment can demonstrate compliance while minimizing recall risks.

Technological Advancements Enhancing Detection Capabilities

Recent innovations in ultrasonic phased array and time-of-flight diffraction (TOFD) technologies now enable detection of sub-millimeter defects previously undetectable. Modern systems incorporate AI-powered analysis algorithms achieving over 98% defect recognition accuracy, a significant improvement from conventional methods. New portable systems also allow in-line inspection without slowing production throughput. These technological advancements make ultrasonic testing increasingly valuable for battery manufacturers seeking to improve quality without sacrificing efficiency.

MARKET RESTRAINTS

High Initial Investment Costs Limiting SME Adoption

Advanced ultrasonic flaw detection systems represent a significant capital expenditure, with industrial-grade equipment often exceeding $50,000 per unit. This creates a substantial barrier for small and medium-sized battery manufacturers who may lack the financial resources to implement comprehensive testing programs. While the long-term ROI justifies the expense through reduced scrap and warranty costs, the upfront investment requirements prevent many operations from upgrading their quality control infrastructure in the short term.

Operational Complexity Requiring Specialized Training

Effective ultrasonic testing requires certified technicians with specialized training in both equipment operation and defect interpretation. The industry faces a shortage of qualified personnel as testing demands outpace workforce development. Even automated systems require highly trained staff to configure, calibrate, and validate results. This skills gap hinders market expansion, with many manufacturers delaying equipment purchases until they can secure or develop the necessary technical expertise.

MARKET CHALLENGES

Heterogeneous Battery Designs Complicating Standardization

The rapid evolution of battery formats presents significant challenges for flaw detection equipment manufacturers. Varying cell chemistries, form factors (prismatic, cylindrical, pouch), and internal architectures require customized testing protocols and transducer configurations. This lack of standardization forces vendors to continuously adapt their solutions while maintaining backward compatibility – driving up R&D costs and complicating customer implementations.

Competition from Alternative Testing Methods

While ultrasonic testing provides unique advantages, it faces competition from X-ray and thermal imaging technologies in certain applications. Some manufacturers employ a combination of methods to achieve comprehensive quality assurance, which can limit ultrasonic system deployments to specific testing phases rather than full production line integration.

MARKET OPPORTUNITIES

Emerging Solid-State Battery Production Creating New Application Potential

The anticipated commercialization of solid-state batteries presents significant growth opportunities. These next-generation power sources require even more precise manufacturing controls, with their multilayer ceramic structures being particularly well-suited to ultrasonic inspection. Equipment vendors developing specialized solutions for solid-state battery production can establish early leadership in what industry analysts project will become a multi-billion dollar market segment by 2030.

Expanding Aftermarket for Battery Testing Services

Beyond manufacturing applications, ultrasonic testing shows growing potential in battery health monitoring and maintenance. Fleet operators and energy storage facility managers increasingly require condition assessment tools to evaluate battery degradation. This creates opportunities for service providers offering portable inspection solutions throughout battery lifecycles – particularly in mission-critical applications like grid storage and commercial EV operations.

ULTRASONIC FLAW DETECTOR FOR LITHIUM BATTERY MARKET TRENDS

Rising Demand for Battery Safety in Electric Vehicles Drives Market Growth

The global ultrasonic flaw detector market for lithium batteries is experiencing significant growth, primarily driven by the rapid expansion of the electric vehicle (EV) industry. With lithium-ion batteries being highly sensitive to internal defects such as cracks, voids, and delamination, manufacturers are increasingly adopting non-destructive testing (NDT) solutions to ensure battery safety and performance. The global ultrasonic flaw detector market for lithium batteries was valued at $48.4 million in 2024 and is projected to reach $81.2 million by 2032, growing at a CAGR of 7.7%. The growing EV market, which is expected to account for over 30% of vehicle sales by 2030, further amplifies the necessity for advanced flaw detection technologies to prevent battery failures and thermal runaway incidents.

Other Trends

Technological Advancements in Phased Array Ultrasonic Testing (PAUT)

Recent innovations in Phased Array Ultrasonic Testing (PAUT) have significantly enhanced the accuracy and efficiency of flaw detection in lithium batteries. PAUT enables precise detection of internal defects without physical contact, reducing the risk of false positives and improving quality control. The PAUT segment is projected to grow at a CAGR of 8.2% from 2024 to 2032, outperforming conventional ultrasonic inspection methods. Companies are also integrating AI-powered defect recognition to enhance real-time data analysis, further improving detection rates and reducing inspection time by nearly 40% compared to traditional methods.

Expanding Applications in Energy Storage and Consumer Electronics

The demand for ultrasonic flaw detectors is not limited to the EV sector; the energy storage and consumer electronics industries also contribute significantly to market expansion. Energy storage batteries, critical for renewable energy integration, require stringent quality checks to prevent performance degradation. Similarly, consumer electronics manufacturers are adopting ultrasonic testing to ensure the reliability of high-capacity batteries used in smartphones, laptops, and wearables. Energy storage batteries accounted for over 25% of the market share in 2024, with consumer electronics expected to exhibit steady growth due to increasing consumer expectations for battery longevity and safety.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation and Strategic Partnerships Drive Market Competition

The global ultrasonic flaw detector market for lithium batteries features a mix of established players and emerging competitors striving to capitalize on the growing demand for non-destructive testing solutions. As lithium-ion batteries become critical components in electric vehicles (EVs), energy storage systems, and consumer electronics, the need for reliable flaw detection technologies continues to escalate. The market is moderately consolidated, with industry leaders leveraging their technological expertise and extensive distribution networks to maintain dominance.

Olympus Corporation remains a frontrunner in ultrasonic testing solutions, holding a significant market share. The company’s advanced phased-array ultrasonic testing (PAUT) systems are widely adopted in battery manufacturing for their high-resolution imaging capabilities and efficiency in detecting minute defects.

Baker Hughes and Sonatest have also solidified their positions through continuous innovation in conventional ultrasonic flaw detectors. Their equipment’s ability to identify internal cracks, voids, and delamination in lithium battery electrodes without compromising structural integrity gives them a competitive edge.

Meanwhile, specialists like Zetec and Proceq are gaining traction by focusing on portable flaw detection solutions tailored for battery inspection. Their compact, user-friendly devices cater to manufacturers requiring on-site testing capabilities.

Asian players, particularly Hitachi Power Solutions and Ryoden Shonan Electronics Corporation, are expanding rapidly by developing cost-effective solutions for the region’s burgeoning battery production facilities. Their growing influence challenges traditional Western manufacturers’ market share.

List of Key Ultrasonic Flaw Detector Companies

- Olympus Corporation (Japan)

- Baker Hughes Company (U.S.)

- Sonatest Ltd. (UK)

- Zetec Inc. (U.S.)

- Proceq SA (Switzerland)

- Karldeutsch (Germany)

- Hitachi Power Solutions (Japan)

- Ryoden Shonan Electronics Corporation (Japan)

- Nova Instruments(NDT Systems) (Israel)

- Centurion NDT (U.S.)

Segment Analysis:

By Type

Phased Array Ultrasonic Flaw Detector Segment Gains Traction Due to Advanced Imaging Capabilities

The Ultrasonic Flaw Detector for Lithium Battery market is segmented based on type into:

- Conventional Ultrasonic Flaw Instruments

- Phased Array Ultrasonic Flaw Detector

- TOFD Ultrasonic Flaw Detector

- Others

By Application

Power Battery Segment Remains Dominant Owing to Stringent EV Battery Safety Requirements

The market is segmented based on application into:

- Power Battery

- Energy Storage Battery

- Consumer Electronics Battery

- Others

By End User

Battery Manufacturers Lead Adoption for Quality Control and Safety Assurance

The market is segmented based on end user into:

- Battery Manufacturers

- Research Institutions

- Quality Inspection Agencies

- Others

By Technology

Automated Inspection Solutions Gain Popularity for High-Volume Production Lines

The market is segmented based on technology into:

- Manual Inspection Systems

- Semi-Automated Systems

- Fully Automated Inspection Systems

Regional Analysis: Ultrasonic Flaw Detector for Lithium Battery Market

Asia-Pacific

The Asia-Pacific region leads the global ultrasonic flaw detector market for lithium batteries, driven by rapid EV adoption and extensive battery manufacturing in China, Japan, and South Korea. China, accounting for over 60% of global lithium-ion battery production, enforces stringent quality control measures that necessitate advanced non-destructive testing (NDT) solutions. Japan’s emphasis on precision manufacturing and South Korea’s thriving consumer electronics sector further propel demand. However, price sensitivity limits widespread adoption of high-end phased array systems, with most manufacturers preferring conventional ultrasonic instruments. The region also benefits from strong R&D investments in battery safety technologies.

North America

North America’s market growth stems from rigorous safety standards in the EV and aerospace sectors, where battery defects carry significant liability risks. The U.S. Department of Energy’s $200 million funding for battery manufacturing R&D under the Bipartisan Infrastructure Law indirectly supports NDT equipment adoption. Technological sophistication drives preference for automated phased array and TOFD systems, especially among tier-1 battery suppliers. Regulatory pressure from organizations like UL and NFPA regarding thermal runaway prevention has made ultrasonic testing integral to quality assurance protocols. The region shows increasing mergers between NDT providers and battery manufacturers to develop customized solutions.

Europe

Europe’s market thrives on its robust automotive electrification agenda and circular economy policies mandating battery health assessments for second-life applications. The EU Battery Regulation (2023) requires comprehensive defect monitoring throughout the battery lifecycle, creating sustained demand. Germany leads in adopting AI-integrated ultrasonic systems that correlate flaw patterns with predictive maintenance data. However, the high cost of advanced equipment constrains smaller manufacturers, creating a two-tier market. Collaborative projects like the European Battery Alliance foster innovation in NDT techniques tailored for next-gen solid-state batteries expected post-2025.

South America

The emerging lithium mining industry in Argentina and Chile drives baseline demand for ultrasonic testing in battery raw material processing. Brazil’s nascent EV market shows potential but lacks standardized testing frameworks. Most equipment imports originate from Chinese or European suppliers due to limited local NDT expertise. Economic instability and reliance on fossil fuels continue to hinder large-scale battery production investments. Nonetheless, regional governments are gradually implementing battery safety regulations aligned with UNECE standards, signaling future growth opportunities.

Middle East & Africa

The market remains embryonic, with ultrasonic flaw detection primarily used in oil & gas applications. Limited local battery production means most demand comes from imported battery quality verification at ports. The UAE and Saudi Arabia show increasing interest in energy storage systems, but adoption lags due to budget constraints and preference for proven thermal testing methods. South Africa’s automotive sector presents the most immediate opportunity as global OEMs establish EV assembly lines requiring compliance with international battery testing norms. Overall growth awaits broader renewable energy infrastructure development.

Report Scope

This market research report provides a comprehensive analysis of the Global Ultrasonic Flaw Detector for Lithium Battery Market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market was valued at USD 48.4 million in 2024 and is projected to reach USD 81.2 million by 2032, growing at a CAGR of 7.7%.

- Segmentation Analysis: Detailed breakdown by product type (Conventional Ultrasonic Flaw instruments, Phased Array Ultrasonic Flaw Detector, TOFD Ultrasonic Flaw Detector) and application (Power Battery, Energy Storage Battery, Consumer Electronics Battery, Others) to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The U.S. and China are key growth markets, with Asia-Pacific expected to dominate.

- Competitive Landscape: Profiles of leading market participants including Baker Hughes, Olympus, Sonatest, Sonotron NDT, and Karldeutsch, covering their product portfolios, market share, and strategic developments.

- Technology Trends & Innovation: Assessment of emerging NDT technologies, integration of AI for defect analysis, and advancements in ultrasonic testing methodologies for lithium battery inspection.

- Market Drivers & Restraints: Evaluation of factors such as growing EV adoption, battery safety regulations, and technological limitations in flaw detection accuracy.

- Stakeholder Analysis: Strategic insights for battery manufacturers, NDT equipment suppliers, quality assurance professionals, and investors in the lithium battery value chain.

The research employs a combination of primary interviews with industry experts and analysis of verified market data to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Ultrasonic Flaw Detector for Lithium Battery Market?

-> Ultrasonic Flaw Detector for Lithium Battery Market was valued at 48.4 million in 2024 and is projected to reach US$ 81.2 million by 2032, at a CAGR of 7.7% during the forecast period.

Which key companies operate in this market?

-> Major players include Baker Hughes, Olympus, Sonatest, Sonotron NDT, Karldeutsch, Proceq, and Zetec.

What are the key growth drivers?

-> Growth is driven by rising EV production, stringent battery safety standards, and increasing demand for reliable battery inspection technologies.

Which region dominates the market?

-> Asia-Pacific leads the market due to strong battery manufacturing presence, particularly in China, Japan, and South Korea.

What are the emerging technology trends?

-> Emerging trends include AI-powered defect recognition, portable handheld detectors, and integration with automated production lines.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...