MARKET INSIGHTS

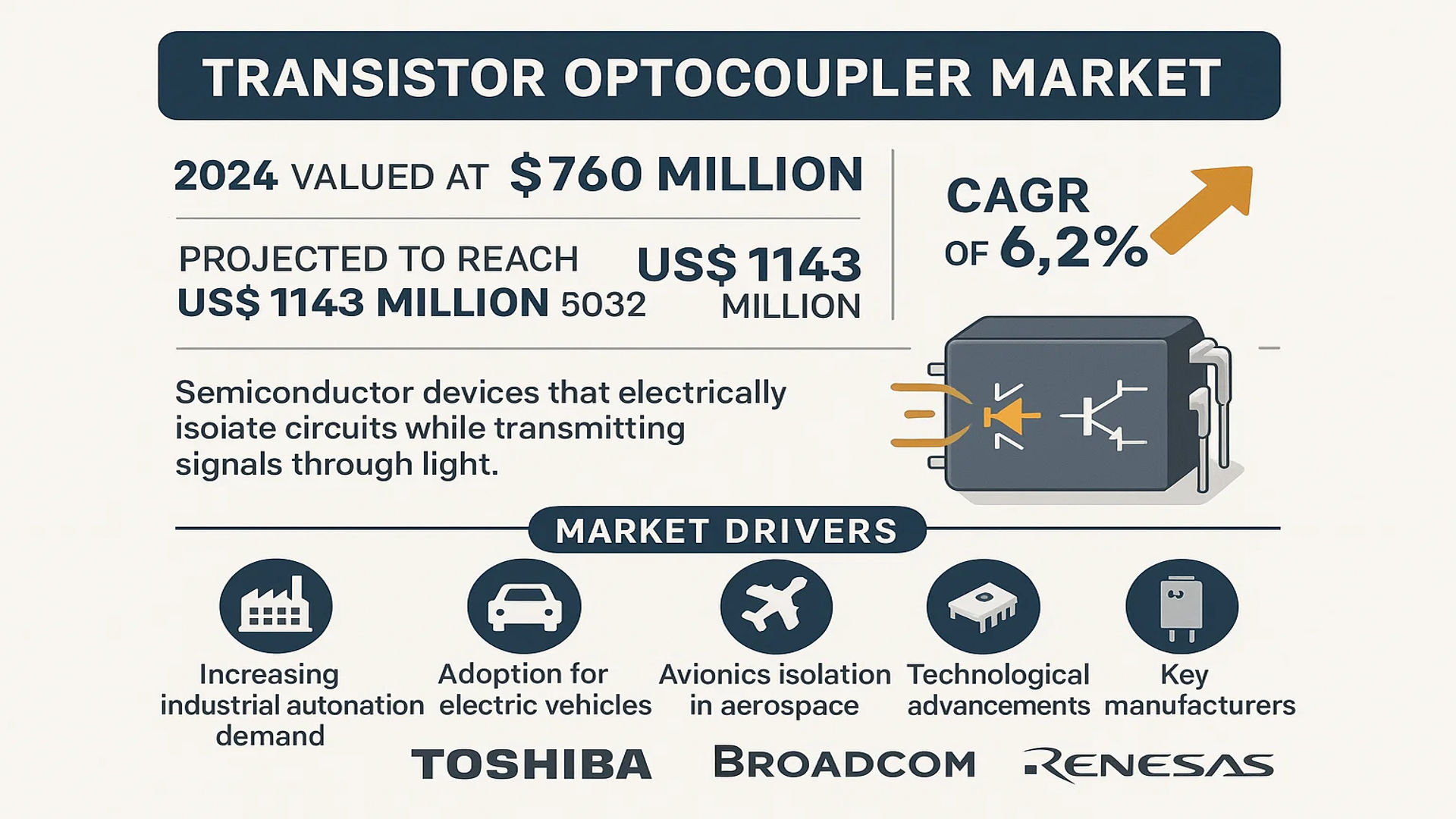

The global Transistor Optocoupler Market was valued at 760 million in 2024 and is projected to reach US$ 1143 million by 2032, at a CAGR of 6.2% during the forecast period.

Transistor optocouplers are semiconductor devices that electrically isolate circuits while transmitting signals through light. These components feature a light-emitting diode (LED) optically coupled with a phototransistor, providing high isolation voltage and stable performance in high-temperature environments. They serve critical functions in preventing voltage spikes, reducing noise interference, and enabling safe signal transmission between circuits with different ground potentials.

The market growth is driven by increasing industrial automation demand, particularly in manufacturing and process control applications. While the automotive sector shows strong adoption for electric vehicle systems, the aerospace industry requires optocouplers for avionics isolation. Furthermore, technological advancements in miniaturization and energy efficiency continue to expand application possibilities. Key manufacturers including Toshiba, Broadcom, and Renesas are investing in enhanced product lines to meet evolving industry requirements.

MARKET DYNAMICS

MARKET DRIVERS

Expansion of Industrial Automation to Accelerate Demand for Optocouplers

The global industrial automation market is projected to grow significantly, driven by Industry 4.0 adoption and smart factory initiatives. Transistor optocouplers play a critical role in protecting sensitive control systems from voltage surges and electrical noise in these environments. Their ability to provide galvanic isolation while enabling signal transmission makes them indispensable components in PLCs, motor drives, and power supplies. The increasing automation of manufacturing processes across automotive, food processing, and pharmaceutical sectors is creating sustained demand for high-reliability isolation components.

Growing Electric Vehicle Production to Fuel Market Expansion

The electric vehicle market is experiencing exponential growth, with production volumes expected to triple by 2030. Transistor optocouplers are extensively used in EV charging stations, battery management systems, and power conversion units. Their ability to operate reliably in high-temperature environments while maintaining electrical isolation positions them as critical components in automotive electrification. Recent advances in wide-bandgap semiconductor technologies are further driving the adoption of optocouplers that can handle higher voltages and switching frequencies required in next-generation EVs.

Increased Focus on Power Efficiency to Drive Innovation

Global energy efficiency initiatives are pushing manufacturers to develop optocouplers with lower power consumption and improved thermal performance. The power electronics market’s shift towards higher efficiency standards such as 80 PLUS Titanium certification is creating demand for optocouplers with enhanced current transfer ratio and reduced forward current requirements. Recent product launches feature optocouplers with power dissipation as low as 50mW while maintaining isolation voltages exceeding 5kV, making them ideal for renewable energy applications and smart grid infrastructure.

MARKET RESTRAINTS

Competition from Alternative Isolation Technologies to Limit Growth Potential

While transistor optocouplers dominate many isolation applications, emerging technologies like capacitive and magnetic isolators are gaining market share in certain segments. These alternatives offer advantages in speed, size, and integration capability that make them attractive for space-constrained applications. The development of silicon-based isolation products with higher data rates and lower power consumption presents a formidable challenge to traditional optocoupler solutions, particularly in communications and high-speed digital applications.

Supply Chain Disruptions to Impact Market Stability

The semiconductor industry continues to face material shortages and production capacity constraints that affect optocoupler availability. Lead times for certain optocoupler variants have extended significantly due to high demand across multiple industries. These supply chain challenges are compounded by geopolitical factors affecting the availability of key raw materials, creating inventory management challenges for manufacturers and end-users alike.

Thermal Management Challenges in High-Density Applications

As electronic systems become more compact and power-dense, thermal performance has emerged as a critical design consideration. Optocouplers must maintain reliability while operating in increasingly demanding thermal environments. The industry faces challenges in developing solutions that balance isolation voltage requirements with thermal dissipation characteristics, particularly in automotive and industrial applications where ambient temperatures can exceed 125°C.

MARKET OPPORTUNITIES

Expansion of 5G Infrastructure to Create New Application Areas

The global rollout of 5G networks presents significant opportunities for high-speed optocoupler solutions. These components are finding applications in base station power supplies, RF amplifiers, and signal conditioning circuits where electrical isolation is critical. The requirement for robust isolation solutions that can operate at millimeter-wave frequencies while maintaining signal integrity is driving innovation in optocoupler design and packaging technologies.

Rise of Smart Grid Technology to Drive Demand

Modernization of power distribution infrastructure is creating demand for optocouplers in smart meters, protective relays, and grid monitoring equipment. The ability to provide reliable isolation in harsh electrical environments makes optocouplers well-suited for these applications. With smart grid investments expected to grow substantially, manufacturers have opportunities to develop specialized product lines with enhanced surge immunity and long-term reliability characteristics.

Medical Electronics Growth to Open New Markets

The expansion of medical diagnostic and therapeutic equipment presents opportunities for high-reliability optocouplers. Applications in patient monitoring, imaging systems, and surgical equipment require components that meet stringent safety standards while providing noise immunity in sensitive measurement circuits. The development of medical-grade optocouplers with enhanced isolation and lower leakage currents positions the industry to benefit from healthcare technology advancements.

MARKET CHALLENGES

Miniaturization Demands to Pressure Design Capabilities

The ongoing trend toward smaller electronic components presents significant design challenges for optocoupler manufacturers. Maintaining isolation performance while reducing package sizes requires innovative material solutions and manufacturing processes. The industry must balance the need for compact designs with the fundamental physics of optoelectronic isolation, particularly for high-voltage applications where creepage and clearance requirements become increasingly difficult to meet in smaller packages.

Regulatory Compliance Complexity to Increase Development Costs

Evolving international safety standards for electrical isolation components require ongoing investment in product certification. The need to comply with multiple regional regulations while maintaining cost competitiveness creates pressure on profit margins. New requirements for environmental compliance and material restrictions add additional layers of complexity to product development cycles.

Product Commoditization to Intensify Price Competition

The market for standard optocouplers faces increasing price pressure as multiple manufacturers offer similar products. This commoditization makes differentiation challenging and requires companies to invest in specialized high-performance variants or integrated solutions to maintain profitability. The ability to develop unique value propositions through customized solutions or application-specific designs will be critical for long-term success in the increasingly competitive isolation components market.

TRANSISTOR OPTOCOUPLER MARKET TRENDS

Industrial Automation Surge Driving Market Growth

The global transistor optocoupler market is experiencing substantial growth, fueled by the rising demand for industrial automation across manufacturing, automotive, and energy sectors. These components play a critical role in safeguarding sensitive electronic circuits from high-voltage surges and electrical noise, making them indispensable in automated systems. Industry 4.0 adoption and smart factory initiatives have further accelerated demand, as optocouplers ensure reliable signal isolation in complex control systems. The industrial segment accounted for over 45% of the market share in 2024, reflecting their widespread use in Programmable Logic Controllers (PLCs), motor drives, and power supplies. Furthermore, stringent safety regulations in hazardous environments continue to push manufacturers to integrate optocoupler solutions into their designs.

Other Trends

Electric Vehicle (EV) Revolution

The rapid expansion of the electric vehicle market has created significant opportunities for transistor optocouplers, particularly in battery management systems (BMS) and charging infrastructure. With EV sales projected to surpass 45 million units annually by 2032, the need for high-reliability isolation components continues to grow. Optocouplers are crucial for voltage level shifting between low-voltage control circuits and high-voltage battery packs, ensuring both safety and performance. Emerging fast-charging technologies (above 350 kW) particularly benefit from robust isolation solutions, driving innovation in high-temperature, high-speed optocoupler designs.

Miniaturization and High-Speed Communication Demands

The trend toward compact, energy-efficient devices continues to shape optocoupler development, with manufacturers introducing space-saving packages that maintain high isolation voltage ratings. While conventional optocouplers typically operate below 10 Mbps, recent advancements have pushed data rates beyond 50 Mbps to accommodate modern industrial communication protocols like EtherCAT and PROFINET. However, this performance improvement comes with thermal management challenges, prompting research into new semiconductor materials and packaging techniques. The increasing integration of optocouplers with additional protection features (such as built-in overvoltage clamps) reflects the industry’s focus on delivering complete isolation solutions.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Invest in Innovation to Secure Competitive Edge

The global transistor optocoupler market demonstrates a moderately consolidated structure, dominated by established semiconductor manufacturers with strong technological capabilities. Broadcom Inc. currently leads the market with an estimated revenue share of 18.2% in 2024, owing to its comprehensive optocoupler portfolio spanning industrial, automotive, and aerospace applications. The company’s recent acquisition of IoT-focused optoelectronics firms has further strengthened its position.

Vishay Intertechnology and Toshiba follow closely, collectively accounting for nearly 25% of global sales. Their competitive advantage stems from decades of expertise in optoelectronic components and strategic manufacturing footprint across Asia. Both companies have been actively expanding production capacities, particularly for high-temperature tolerant optocouplers used in automotive electrification systems.

The market also features dynamic mid-sized players like Littelfuse and Renesas Electronics, who are gaining traction through specialization. Littelfuse’s 2023 launch of ultra-compact automotive-grade optocouplers has helped it capture emerging EV opportunities, while Renesas continues to integrate optocouplers with its microcontroller solutions for industrial automation.

Meanwhile, Texas Instruments and Infineon Technologies are reshaping competition through vertical integration. By combining optocouplers with power management ICs, these firms offer system-level solutions that reduce component count for end-users. Their R&D investments in GaN-based optocouplers indicate a strategic focus on next-gen isolation technologies.

List of Key Transistor Optocoupler Manufacturers Profiled

- Broadcom Inc. (U.S.)

- Vishay Intertechnology (U.S.)

- Toshiba Electronic Devices & Storage Corporation (Japan)

- Littelfuse, Inc. (U.S.)

- Renesas Electronics Corporation (Japan)

- Texas Instruments Incorporated (U.S.)

- Infineon Technologies AG (Germany)

- OMEGA Engineering (U.S.)

- ISOCOM Components Ltd (UK)

- Skyworks Solutions, Inc. (U.S.)

- On Semiconductor Corporation (U.S.)

- Fairchild Semiconductor (U.S.)

- Lite-On Technology Corporation (Taiwan)

Segment Analysis:

By Type

DC Input Optocouplers Dominate the Market Due to High Demand in Industrial Automation

The market is segmented based on type into:

- DC Input

- AC Input

By Application

Industrial Automation Leads Market Adoption Due to Critical Isolation Requirements

The market is segmented based on application into:

- Aerospace

- Industrial Automation

- Automotive Electronics

- Consumer Electronics

- Others

By Voltage Range

Medium Voltage Segment Shows Strong Growth in Power Management Applications

The market is segmented by isolation voltage range into:

- Low Voltage (up to 1kV)

- Medium Voltage (1kV – 5kV)

- High Voltage (above 5kV)

By Packaging Type

DIP Packaging Remains Preferred Choice for General Industrial Applications

The market is segmented by packaging format into:

- Dual In-line Package (DIP)

- Surface Mount Devices (SMD)

- Others

Regional Analysis: Transistor Optocoupler Market

Asia-Pacific

The Asia-Pacific region dominates the global transistor optocoupler market, accounting for over 45% of revenue share as of 2024. This leadership position stems from robust electronics manufacturing ecosystems in China, Japan, and South Korea, coupled with increasing industrialization across India and Southeast Asia. The region benefits from high-volume production of consumer electronics, industrial automation systems, and automotive components – all key application areas for optocouplers. China’s semiconductor industry growth, supported by government initiatives like the “Made in China 2025” policy, continues to drive demand for isolation components. However, intense price competition among regional manufacturers presents both opportunities and challenges for market players.

North America

North America represents a technologically advanced market for transistor optocouplers, with stringent quality standards and a focus on high-reliability applications. The United States leads regional demand, particularly in aerospace, defense, and medical equipment sectors where component durability is critical. Recent investments in renewable energy infrastructure and electric vehicle production have created new growth avenues. The presence of major semiconductor companies and R&D centers fosters innovation in optocoupler technology, with emphasis on miniaturization and enhanced thermal performance to meet evolving industry requirements.

Europe

Europe maintains a strong position in the transistor optocoupler market, characterized by advanced industrial automation adoption and strict electromagnetic compatibility regulations. Germany remains the largest national market, driven by its thriving automotive and industrial control sectors. The region shows growing preference for energy-efficient optocouplers that comply with EU environmental directives. While growth remains steady, European manufacturers face cost pressures from Asian competitors, leading to increased focus on specialized high-value optocoupler solutions for niche applications in medical and aerospace industries.

South America

The South American transistor optocoupler market exhibits moderate growth, with Brazil and Argentina as primary consumption centers. Industrial expansion and upgrading of manufacturing capabilities are gradually increasing demand, though adoption rates lag behind more developed regions. Economic instability and currency fluctuations sometimes disrupt supply chains and component availability. Nonetheless, the automotive sector’s recovery and increasing penetration of automation technologies present opportunities for market expansion, particularly for cost-competitive optocoupler solutions.

Middle East & Africa

This emerging region shows potential for transistor optocoupler adoption, though market development remains uneven. Infrastructure projects and industrial diversification efforts in GCC countries drive demand for industrial automation components. South Africa serves as a regional hub for electronics manufacturing, while North African nations are gradually developing their industrial bases. The market faces challenges including limited local production capabilities and reliance on imports, but growing investments in smart city projects and renewable energy systems indicate promising long-term prospects.

Report Scope

This market research report provides a comprehensive analysis of the Global Transistor Optocoupler Market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market was valued at USD 760 million in 2024 and is projected to reach USD 1143 million by 2032, growing at a CAGR of 6.2%.

- Segmentation Analysis: Detailed breakdown by product type (DC Input, AC Input), application (Aerospace, Industrial, Automobile, Others), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, with Asia-Pacific accounting for over 40% market share in 2024.

- Competitive Landscape: Profiles of leading market participants including Broadcom, Toshiba, Renesas, and Infineon Technologies, covering their product portfolios, R&D investments, and recent strategic developments.

- Technology Trends & Innovation: Assessment of emerging technologies in optocoupler design, miniaturization trends, and integration with IoT applications in industrial automation.

- Market Drivers & Restraints: Evaluation of factors including industrial automation growth, EV adoption, and 5G infrastructure development versus challenges like semiconductor shortages and pricing pressures.

- Stakeholder Analysis: Strategic insights for component manufacturers, system integrators, and investors regarding supply chain optimization and emerging opportunities in high-voltage applications.

The research employs a rigorous methodology combining primary interviews with industry leaders and analysis of verified market data from regulatory filings, trade associations, and financial reports to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Transistor Optocoupler Market?

->Transistor Optocoupler Market was valued at 760 million in 2024 and is projected to reach US$ 1143 million by 2032, at a CAGR of 6.2% during the forecast period.

Which key companies operate in Global Transistor Optocoupler Market?

-> Key players include Broadcom, Toshiba, Renesas, Infineon Technologies, ON Semiconductor, and Vishay, among others.

What are the key growth drivers?

-> Key growth drivers include industrial automation adoption, EV production growth, and 5G infrastructure deployment.

Which region dominates the market?

-> Asia-Pacific holds the largest market share, driven by electronics manufacturing in China, Japan, and South Korea.

What are the emerging trends?

-> Emerging trends include high-speed optocouplers for 5G, automotive-grade components for EVs, and miniaturized packages.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...