MARKET INSIGHTS

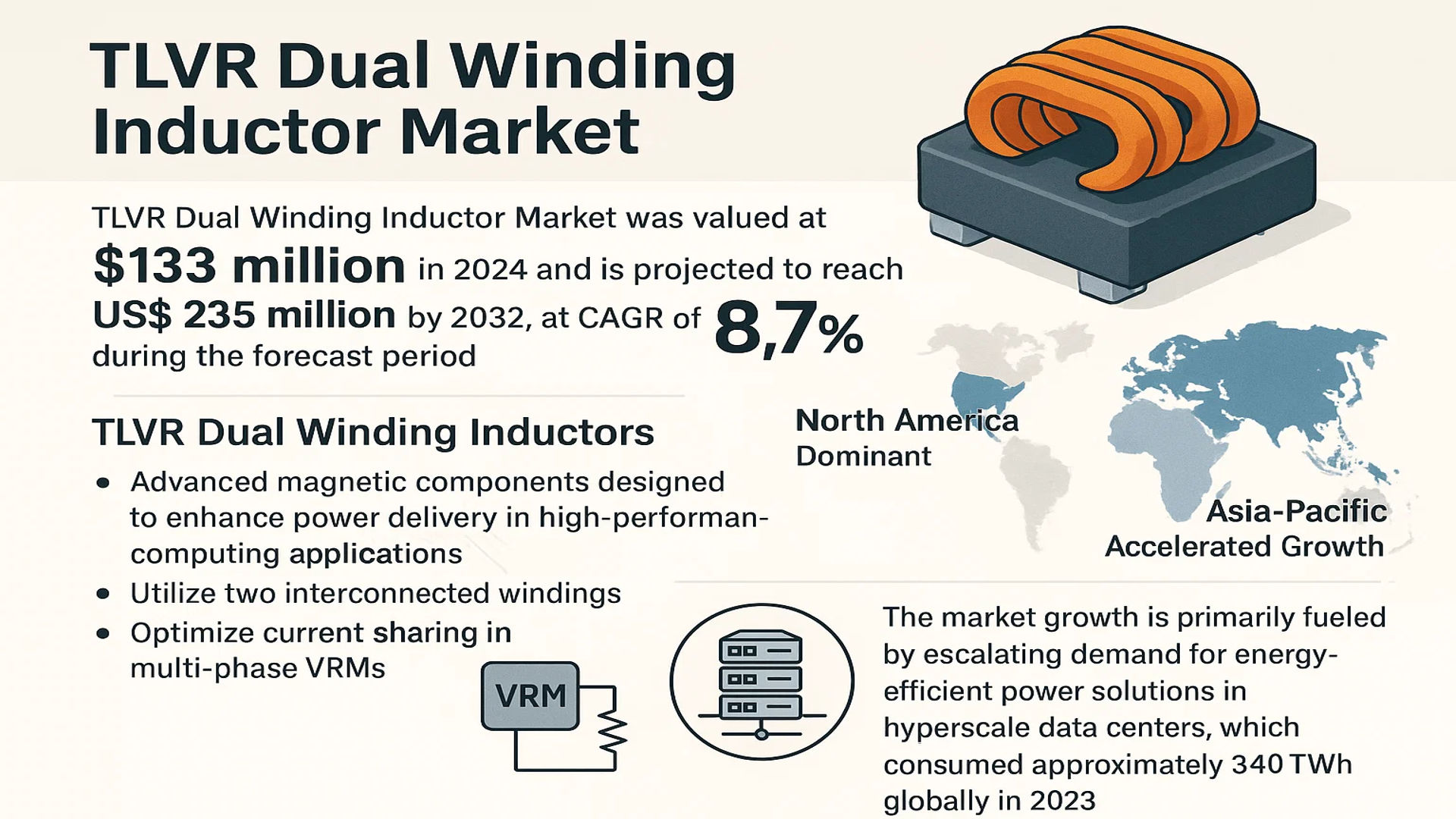

The global TLVR Dual Winding Inductor Market was valued at 133 million in 2024 and is projected to reach US$ 235 million by 2032, at a CAGR of 8.7% during the forecast period. While North America holds a dominant position due to its robust semiconductor industry, Asia-Pacific is witnessing accelerated growth, driven by increasing electronics manufacturing in China and South Korea.

TLVR (Transient Voltage Reduction) Dual Winding Inductors are advanced magnetic components designed to enhance power delivery in high-performance computing applications. These inductors utilize two interconnected windings to improve transient response, minimize voltage droop, and optimize current sharing in multi-phase voltage regulator modules (VRMs). Their unique architecture allows for faster load transitions while reducing electromagnetic interference, making them ideal for data centers, AI servers, and high-end GPUs where power efficiency and stability are critical.

The market growth is primarily fueled by escalating demand for energy-efficient power solutions in hyperscale data centers, which consumed approximately 340 TWh globally in 2023. Furthermore, advancements in 5G infrastructure and edge computing are creating new deployment opportunities. Major players like TDK and Infineon are investing in miniaturized inductor designs to cater to space-constrained applications, while emerging manufacturers in China are gaining traction through cost-competitive offerings. The 70-100nH inductance segment currently leads market share due to its widespread adoption in server power supplies.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for High-Performance Computing to Accelerate TLVR Inductor Adoption

The global surge in high-performance computing (HPC) applications is a primary driver for the TLVR dual winding inductor market. With artificial intelligence, machine learning, and big data analytics requiring increasingly powerful processing capabilities, modern CPUs and GPUs demand sophisticated power regulation. TLVR inductors significantly reduce voltage ripple and improve transient response in multi-phase power delivery networks—critical for maintaining stability in processors consuming over 300 watts. The data center sector alone is projected to consume over 400 terawatt-hours annually by 2025, necessitating more efficient power solutions. This technological imperative positions TLVR inductors as essential components in next-generation computing architectures.

Energy Efficiency Regulations Propel Market Growth

Stringent global energy efficiency standards are compelling electronics manufacturers to adopt advanced power conversion technologies. TLVR dual winding inductors achieve up to 94% power conversion efficiency in voltage regulator modules—a 3-5% improvement over conventional designs. This performance enhancement directly translates to reduced energy consumption in data centers, where power usage effectiveness (PUE) has become a critical operational metric. Regulatory initiatives like the EU’s EcoDesign Directive and ENERGY STAR certifications for servers create strong market pull for these high-efficiency components. The potential energy savings across millions of deployed servers present a compelling value proposition for TLVR inductor implementation.

Miniaturization Trend in Electronics Drives Component Innovation

Continued miniaturization of electronic devices creates demand for compact power solutions that don’t compromise performance. TLVR dual winding inductors occupy 30-40% less board space than traditional multi-inductor configurations while delivering superior electrical characteristics. This space-saving advantage proves particularly valuable in densely packed server motherboards and high-end graphics cards where component real estate is at a premium. The trend toward smaller form factors in enterprise computing equipment, coupled with the push for higher power densities exceeding 100W per square inch, positions TLVR technology as an optimal solution for modern power architecture designs.

MARKET RESTRAINTS

Complex Manufacturing Process Limits Supply Capacity

The specialized manufacturing requirements for TLVR dual winding inductors creates substantial production challenges. Precise alignment of multiple windings within tight tolerances demands advanced winding equipment and skilled technicians. Current manufacturing yields for these components hover around 80-85%, significantly lower than conventional inductor production rates. This constrained supply situation becomes particularly problematic during periods of strong market demand, leading to extended lead times exceeding 20 weeks across the industry. The specialized materials and processes required further exacerbate supply chain vulnerabilities, with limited qualified suppliers for the ultra-thin laminates and cores these components utilize.

High Development Costs Create Barrier to Entry

Substantial upfront engineering investment represents a significant market restraint for TLVR inductor adoption. Designing these components into power delivery networks requires specialized simulation tools and measurement equipment that can cost over $500,000. Additionally, the iterative tuning process often necessitates multiple prototype cycles before achieving optimal performance, adding both time and expense to development projects. Many small and medium-sized electronics manufacturers lack the resources to bear these development costs, limiting market penetration to higher-margin applications where the performance benefits justify the elevated engineering expenditures.

Thermal Management Challenges in High-Current Applications

Thermal performance constraints emerge as a significant technical restraint as power demands continue escalating. While TLVR inductors offer superior electrical characteristics, their compact dual-winding configuration presents heat dissipation challenges at current levels above 50 amps. Excessive temperatures negatively impact reliability and can reduce component lifespan by up to 30% in continuous high-load operation. These thermal limitations become particularly problematic in emerging applications such as AI accelerator cards and high-performance computing clusters where sustained peak power delivery is required. Innovative cooling solutions add cost and complexity, partially offsetting the technology’s inherent advantages.

MARKET CHALLENGES

Material Cost Volatility Impacts Profit Margins

The TLVR inductor market faces significant challenges from fluctuating raw material costs. These components rely heavily on specialty alloys and high-grade ferrite materials, whose prices have shown annual volatility exceeding 15% in recent years. The nickel-iron and cobalt-based magnetic materials essential for high-frequency performance are particularly susceptible to geopolitical supply chain disruptions and trade policy changes. This cost instability creates margin pressure throughout the value chain, as manufacturers struggle to maintain pricing consistency while absorbing material cost fluctuations. The situation is further complicated by the inability to substitute materials without compromising the stringent performance requirements of TLVR applications.

Intellectual Property Barriers Slow Market Expansion

Dense patent landscapes surrounding TLVR technology present substantial market challenges. Core patents covering fundamental dual-winding architectures and control methodologies remain held by a handful of established players, creating barriers for new entrants. Licensing negotiations for these protected technologies often involve complex cross-licensing arrangements and royalty agreements that can delay product development cycles. The resulting limited competition in certain market segments maintains higher price points, slowing adoption in cost-sensitive applications. This intellectual property landscape also discourages some manufacturers from investing in TLVR solutions due to concerns about future litigation risks and technology access limitations.

Technical Support Requirements Strain Resources

The sophisticated nature of TLVR inductor implementation creates substantial post-sales support challenges. These components often require customized tuning for each application, necessitating extensive field application engineering resources. Many manufacturers report that TLVR products demand 3-4 times more technical support hours compared to standard inductor lines. This heightened support burden strains profit margins, particularly as customers increasingly expect these services to be bundled into component pricing. The specialized knowledge required to properly implement TLVR solutions also limits the pool of qualified support personnel, creating bottlenecks in customer onboarding and problem resolution processes.

MARKET OPPORTUNITIES

Emerging AI Hardware Market Presents Growth Potential

The explosive growth in artificial intelligence hardware creates substantial opportunities for TLVR inductor expansion. Next-generation AI processors require unprecedented power delivery capabilities, with current demands exceeding 1000 amps in some high-end training accelerators. TLVR technology’s ability to maintain tight voltage regulation under these extreme loads positions it as an ideal solution for AI power architectures. Market projections indicate the AI hardware sector will grow at 25% annually through 2030, representing a significant greenfield opportunity for TLVR inductor suppliers. Recent design wins in leading AI server platforms validate the technology’s suitability for these demanding applications.

5G Infrastructure Buildout Drives New Applications

Global 5G network deployments are opening new application areas for TLVR inductor technology. The power delivery requirements of massive MIMO base stations and edge computing nodes demand the high-efficiency, fast-transient-response characteristics that TLVR designs provide. With over 5 million 5G base stations expected to be deployed by 2025, this infrastructure expansion represents a major growth vector. The technology’s ability to operate reliably in harsh environmental conditions also makes it well-suited for outdoor telecom equipment installations. Early adopters in the 5G sector report 20-30% improvements in power system efficiency compared to traditional inductor implementations.

Automotive Electrification Creates New Market Segments

The accelerating transition to electric and autonomous vehicles presents significant opportunities for TLVR inductor technology. Advanced driver assistance systems (ADAS) and autonomous computing platforms require robust power delivery solutions that can maintain stability under challenging automotive conditions. TLVR inductors’ superior performance in handling load transients makes them ideal for powering high-performance automotive computing systems. Additionally, emerging 48-volt mild hybrid architectures create new applications in vehicle power networks. The automotive sector’s stringent reliability requirements align well with TLVR technology’s robust design characteristics, though qualification processes remain lengthy and expensive.

TLVR DUAL WINDING INDUCTOR MARKET TRENDS

Increasing Demand for High-Performance Computing Drives Market Growth

The global TLVR (Trans-Inductor Voltage Regulator) Dual Winding Inductor market is experiencing robust growth, primarily fueled by the rising demand for efficient power delivery in high-performance computing (HPC) applications. These inductors, featuring two windings to optimize current distribution and minimize power losses, are critical for managing rapid load transitions in advanced CPUs, GPUs, and data center infrastructure. The market, valued at $133 million in 2024, is projected to expand at a compound annual growth rate (CAGR) of 8.7%, reaching $235 million by 2032. The increasing adoption of AI servers and faster data processing systems has amplified the need for TLVR inductors, as they significantly reduce voltage droop and enhance power efficiency in multi-phase voltage regulation.

Other Trends

Advancements in Data Center Power Architecture

As data centers transition to higher power densities and energy-efficient designs, the demand for TLVR Dual Winding Inductors continues to rise. These components play a vital role in ensuring stable power delivery for next-generation storage systems and AI-driven computing platforms. The 70-100 nH inductance range segment is particularly gaining traction, catering to the high-power distribution requirements of modern data centers. Furthermore, emerging technologies such as 5G and edge computing are reinforcing the need for compact, high-efficiency inductors that can operate in demanding environments with minimal thermal dissipation.

Expansion of AI and Semiconductor Applications

The rapid proliferation of artificial intelligence and machine learning applications has accelerated semiconductor innovation, necessitating advanced power management solutions. TLVR Dual Winding Inductors are increasingly incorporated into AI server designs to optimize transient response and improve overall system efficiency. Leading manufacturers like TDK, Eaton, and Infineon are focusing on R&D initiatives to develop inductors with lower core losses and higher saturation currents. Moreover, the intensified competition among semiconductor giants to enhance GPU performance is contributing to the market’s expansion, as TLVR inductors provide a crucial balance between power efficiency and thermal management in high-speed computing applications.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation and Strategic Expansion Drive Market Competition

The global TLVR (Trans-Inductor Voltage Regulator) Dual Winding Inductor market features a competitive yet fragmented landscape with major electronic component manufacturers and specialized inductor producers vying for market share. TDK Corporation leads the segment through its comprehensive product portfolio and strong R&D capabilities in advanced magnetics. The company holds approximately 18% market share in 2024, driven by its technological expertise in high-efficiency power solutions for data centers and AI applications.

Infineon Technologies and Eaton Corporation follow closely, collectively accounting for around 25% of the global market. Their growth stems from vertical integration strategies and partnerships with major computing hardware manufacturers. Infineon’s recent acquisition of a specialized magnetic components manufacturer in 2023 significantly enhanced its TLVR inductor capabilities, while Eaton continues to expand its production capacity in Asia to meet growing demand.

Mid-sized players like Abracon LLC and Bourns Inc. are gaining traction through niche product innovations and customized solutions for specific applications. Abracon’s recent launch of a high-current, low-profile TLVR inductor series has positioned it strongly in the AI server market segment, which is expected to grow at over 10% CAGR through 2032.

The Asian market sees fierce competition among regional specialists such as Sunlord Electronics and Tai-Tech Advanced Electronics, who benefit from local supply chain advantages and cost competitiveness. These companies are increasingly targeting export markets while expanding their technology portfolios to compete with global leaders.

List of Key TLVR Dual Winding Inductor Manufacturers

- TDK Corporation (Japan)

- Eaton Corporation (Ireland)

- Abracon LLC (U.S.)

- Infineon Technologies (Germany)

- Pulse Electronics (YAGEO Group) (U.S.)

- Bourns Inc. (U.S.)

- ITG Electronics (Taiwan)

- Superworld Electronics (China)

- Sunlord Electronics (China)

- Microgate Technology (Taiwan)

- Tai-Tech Advanced Electronics (Taiwan)

- POCO (China)

- SK Electronics (South Korea)

Segment Analysis:

By Inductance Range (nH)

70-100 nH Segment Leads Due to High Adoption in AI Servers and Data Centers

The market is segmented based on inductance range into:

- 70-100 nH

- 100-170 nH

- 170-220 nH

- Others

By Application

Data Center Segment Dominates Due to Growing Demand for Power-Efficient Computing Solutions

The market is segmented based on application into:

- AI Server

- Data Center

- Storage System

- Others

By Core Material

Ferrite Core Leads the Market Due to its High Magnetic Permeability and Cost-Effectiveness

The market is segmented based on core material into:

- Ferrite Core

- Iron Powder Core

- Molded Core

- Others

By End-User Industry

High-Performance Computing Leads Due to Demand for Power-Efficient VRM Solutions

The market is segmented based on end-user industry into:

- High-Performance Computing (HPC)

- Telecommunications

- Automotive Electronics

- Consumer Electronics

- Others

Regional Analysis: TLVR Dual Winding Inductor Market

Asia-Pacific

The Asia-Pacific region leads the global TLVR dual winding inductor market, driven by robust demand from high-performance computing applications. China and Japan are the dominant players, accounting for over 40% of regional market share, thanks to their strong semiconductor and electronics manufacturing ecosystems. The rapid expansion of data centers—particularly in China, India, and Southeast Asia—fuels demand for efficient power regulation components. Companies like TDK, Infineon, and Sunlord are actively expanding production capacities to meet growing needs, while cost-competitive local manufacturers are gaining traction in mid-range applications. Recent government investments in AI infrastructure and 5G further accelerate adoption.

North America

North America remains a high-value market, with the U.S. contributing the majority of demand due to its advanced data center infrastructure and leadership in AI server development. The presence of tech giants like Google, Amazon, and Microsoft drives innovation in power-efficient designs, favoring high-performance TLVR inductors. However, supply chain dependencies on Asian manufacturers and stricter import regulations pose challenges. Eaton and Bourns are key local suppliers, focusing on customized solutions for enterprise and hyperscale data centers. Regulatory standards for energy efficiency (e.g., ENERGY STAR for servers) further incentivize adoption.

Europe

Europe’s market growth is anchored by Germany, the U.K., and the Nordic countries, where data center investments align with sustainability goals. The region emphasizes energy-efficient components, creating opportunities for TLVR inductors in renewable-energy-powered facilities. Infineon and Pulse Electronics leverage local R&D to develop low-loss inductor variants. However, slower adoption in Eastern Europe due to fragmented infrastructure and cost sensitivity limits overall growth. EU directives on electronic waste reduction and energy efficiency standards (e.g., Ecodesign) will likely push broader market penetration.

South America

The market in South America is nascent but shows potential, particularly in Brazil and Argentina, where localized data center investments are increasing. Economic instability and reliance on imported components constrain growth, though partnerships with global manufacturers like YAGEO and Abracon aim to improve supply chain resilience. The lack of domestic production facilities remains a bottleneck, but gradual digital transformation in banking and telecommunications sectors could drive future demand.

Middle East & Africa

This region is in early stages of adoption, with the UAE, Saudi Arabia, and Israel leading due to data center expansions and smart city initiatives. High dependence on imports and limited technical expertise slow market maturation, but sovereign investments in AI and cloud infrastructure present long-term opportunities. Companies like Codaca and Superworld Electronics are exploring partnerships to cater to niche high-performance applications, though price sensitivity remains a hurdle for widespread adoption.

Report Scope

This market research report provides a comprehensive analysis of the global TLVR Dual Winding Inductor market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global TLVR Dual Winding Inductor market was valued at USD 133 million in 2024 and is projected to reach USD 235 million by 2032, growing at a CAGR of 8.7%.

- Segmentation Analysis: Detailed breakdown by inductance range (70-100nH, 100-170nH, 170-220nH, Others) and application (AI Server, Data Center, Storage System, Others) to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The U.S. and China are key markets with significant growth potential.

- Competitive Landscape: Profiles of leading market participants including TDK, Eaton, Infineon, Bourns, and Pulse Electronics (YAGEO), covering their product portfolios, market share, and strategic initiatives.

- Technology Trends & Innovation: Assessment of emerging inductor technologies, material advancements, and integration with high-performance computing systems.

- Market Drivers & Restraints: Evaluation of factors driving market growth including rising demand for AI servers and data centers, along with challenges such as supply chain constraints and material costs.

- Stakeholder Analysis: Strategic insights for component manufacturers, power solution providers, system integrators, and investors regarding market opportunities.

The research employs primary and secondary methodologies, including interviews with industry experts and analysis of verified market data, to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global TLVR Dual Winding Inductor Market?

-> TLVR Dual Winding Inductor Market was valued at 133 million in 2024 and is projected to reach US$ 235 million by 2032, at a CAGR of 8.7% during the forecast period.

Which key companies operate in Global TLVR Dual Winding Inductor Market?

-> Key players include TDK, Eaton, Abracon, Infineon, Pulse Electronics (YAGEO), Bourns, and ITG Electronics.

What are the key growth drivers?

-> Growth is driven by increasing demand for high-performance computing, AI server deployments, and data center expansion worldwide.

Which region dominates the market?

-> Asia-Pacific leads in market share, while North America shows strong growth due to advanced computing infrastructure.

What are the emerging trends?

-> Emerging trends include miniaturization of components, higher frequency operation, and integration with advanced power management solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...