MARKET INSIGHTS

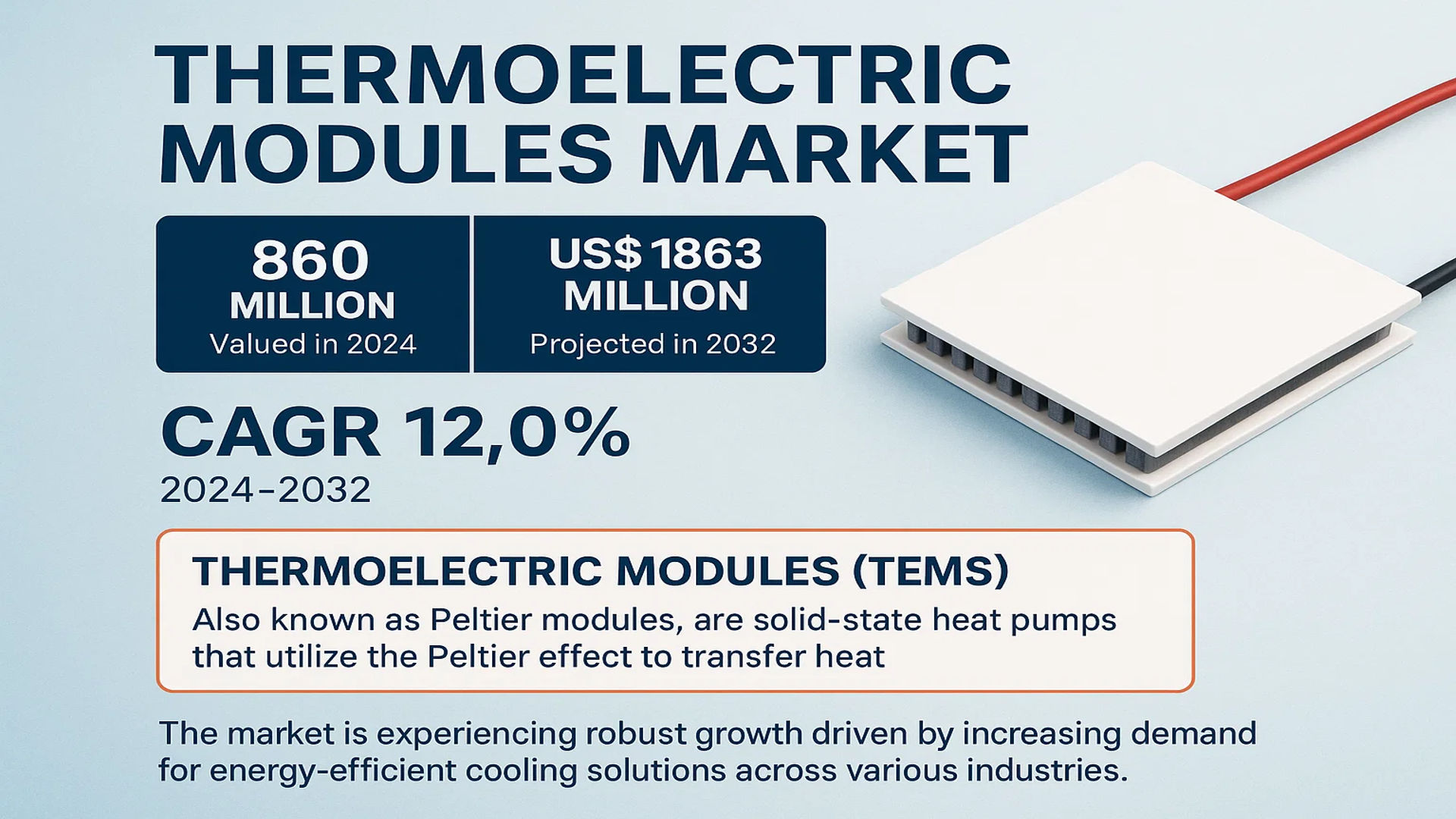

The global Thermoelectric Modules Market was valued at 860 million in 2024 and is projected to reach US$ 1863 million by 2032, at a CAGR of 12.0% during the forecast period.

Thermoelectric modules (TEMs), also known as Peltier modules, are solid-state heat pumps that utilize the Peltier effect to transfer heat. These semiconductor-based devices are composed of numerous thermocouples connected electrically in series and thermally in parallel. When a low-voltage DC current is applied, heat is pumped from one side of the module to the other, creating a temperature differential. This allows a single module to provide both precise cooling and heating by simply reversing the current polarity, making them invaluable for applications requiring accurate temperature control without moving parts.

The market is experiencing robust growth driven by increasing demand for energy-efficient cooling solutions across various industries. The consumer electronics segment, which holds the largest application share at over 30%, is a primary growth driver due to the miniaturization of components and the need for thermal management in compact devices. Furthermore, advancements in automotive applications, particularly in seat conditioning and electronic enclosure cooling, are contributing significantly to market expansion. Geographically, China dominates the market with a 28% share, followed by North America at 23%, reflecting strong regional manufacturing and technological adoption. Key players like Ferrotec and II-VI Marlow, which collectively hold a significant market share, continue to innovate, further propelling the industry forward.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Energy-Efficient Cooling Solutions in Consumer Electronics to Drive Market Growth

The global thermoelectric modules market is experiencing robust growth driven by increasing demand for energy-efficient and compact cooling solutions across consumer electronics. Thermoelectric modules offer precise temperature control, silent operation, and reliability, making them ideal for applications such as portable refrigerators, laser diodes, and medical equipment. The consumer electronics segment, which accounts for over 35% of the market share, continues to expand with the proliferation of smartphones, gaming consoles, and wearable devices requiring thermal management. Innovations in miniaturization and efficiency are further accelerating adoption, with manufacturers developing modules that achieve cooling capacities exceeding 200 watts while maintaining compact form factors. The shift towards eco-friendly refrigeration technologies, coupled with stringent energy efficiency regulations in regions like Europe and North America, is pushing industries to adopt solid-state cooling solutions, thereby fueling market expansion.

Expansion in Automotive and Telecommunications Sectors to Boost Market Penetration

Thermoelectric modules are gaining significant traction in the automotive and telecommunications industries due to their ability to provide reliable thermal management in challenging environments. In the automotive sector, these modules are increasingly used in seat climate control systems, battery thermal management for electric vehicles, and electronic control unit cooling. The global electric vehicle market, projected to grow at a compound annual growth rate of over 20%, presents substantial opportunities for thermoelectric module manufacturers. Similarly, the telecommunications industry relies on these modules for cooling high-power laser diodes and base station equipment, where maintaining optimal operating temperatures is critical for performance and longevity. The 5G infrastructure rollout worldwide is further driving demand, with estimates suggesting that over 70% of new base station installations will incorporate advanced thermal management solutions by 2026.

Advancements in Medical Technology and Laboratory Equipment to Stimulate Demand

The medical and laboratory equipment sector represents a growing application area for thermoelectric modules, particularly in precision temperature control devices. These modules are essential components in DNA cyclers, blood analyzers, laboratory refrigerators, and medical imaging equipment where temperature stability within ±0.1°C is often required. The global medical device market, valued at approximately 500 billion dollars, continues to expand with increasing healthcare expenditure and technological advancements. Thermoelectric modules enable compact, vibration-free cooling solutions that are crucial for sensitive medical instruments. Recent developments in point-of-care diagnostics and portable medical devices have further increased the demand for small-form-factor thermoelectric coolers that can operate reliably in diverse environmental conditions.

➤ For instance, recent innovations in multi-stage thermoelectric modules have enabled cooling temperature differences exceeding 70°C, making them suitable for specialized medical and industrial applications requiring extreme temperature differentials.

Furthermore, increasing investments in healthcare infrastructure across emerging economies and the growing adoption of automated laboratory equipment are expected to drive sustained growth in this segment over the forecast period.

MARKET CHALLENGES

High Initial Costs and Limited Energy Efficiency Compared to Traditional Systems to Challenge Market Adoption

Despite the growing adoption of thermoelectric modules, the market faces significant challenges related to cost competitiveness and energy efficiency. Thermoelectric cooling systems typically have higher initial costs compared to conventional vapor-compression refrigeration systems, particularly for high-capacity applications. The coefficient of performance (COP) of thermoelectric modules generally ranges between 0.3 and 0.7, which is lower than traditional systems that can achieve COP values exceeding 3.0. This efficiency gap becomes more pronounced in large-scale cooling applications, making it difficult for thermoelectric technology to compete in price-sensitive markets. The manufacturing process involving rare earth materials and specialized semiconductor compounds also contributes to higher production costs, which are ultimately passed on to end-users.

Other Challenges

Technical Limitations in Heat Dissipation

Thermoelectric modules face inherent limitations in heat dissipation capacity, especially when dealing with high heat loads. The maximum temperature difference achievable is constrained by material properties, and heat sink design becomes critical for optimal performance. In applications requiring heat removal exceeding 300 watts, traditional cooling methods often remain more practical and cost-effective.

Material and Manufacturing Constraints

The production of high-performance thermoelectric materials involves complex manufacturing processes and specialized equipment. Bismuth telluride, the most commonly used material, presents supply chain challenges and price volatility. Additionally, achieving consistent quality and performance across production batches requires stringent quality control measures, adding to manufacturing complexity and cost.

MARKET RESTRAINTS

Technical Complexities in High-Temperature Applications to Restrict Market Expansion

While thermoelectric modules offer numerous advantages, their application in high-temperature environments presents significant technical challenges that restrain market growth. The performance of thermoelectric materials degrades at elevated temperatures, limiting their use in industrial processes and automotive applications where ambient temperatures can exceed 85°C. The maximum operating temperature for conventional bismuth telluride modules is typically around 150°C, beyond which material properties deteriorate rapidly. This temperature limitation restricts their application in sectors such as metallurgy, power generation, and high-temperature manufacturing processes where cooling requirements often involve much higher temperature differentials.

Additionally, the reliability of thermoelectric modules in harsh environments remains a concern. Thermal cycling-induced stress can lead to performance degradation and eventual failure, particularly in applications experiencing frequent temperature fluctuations. The development of advanced materials capable of withstanding higher temperatures while maintaining satisfactory thermoelectric properties continues to be an area of ongoing research, but commercial implementation remains limited.

MARKET OPPORTUNITIES

Emerging Applications in Renewable Energy and Waste Heat Recovery to Create New Growth Avenues

The thermoelectric modules market is poised for significant expansion through emerging applications in renewable energy systems and waste heat recovery. Thermoelectric generators (TEGs) that convert waste heat directly into electricity are gaining attention across various industries, particularly in automotive exhaust systems, industrial processes, and solar thermal applications. The global waste heat recovery market, projected to exceed 90 billion dollars by 2030, presents substantial opportunities for thermoelectric technology adoption. Recent advancements in materials science have improved conversion efficiencies to levels exceeding 8%, making TEGs increasingly viable for commercial applications.

Additionally, the integration of thermoelectric modules in solar thermal systems and geothermal energy applications is creating new market segments. These systems can enhance overall energy efficiency by converting excess heat into usable electricity, particularly in distributed energy generation scenarios. The growing focus on sustainable energy solutions and carbon emission reduction targets worldwide is driving increased investment and research in thermoelectric power generation technologies.

Furthermore, developments in IoT and edge computing are opening new opportunities for thermoelectric modules in powering remote sensors and low-power electronic devices. The ability to generate electricity from temperature differences makes thermoelectric generators ideal for applications where battery replacement is impractical or where continuous power is required from environmental heat sources.

THERMOELECTRIC MODULES MARKET TRENDS

Miniaturization and Efficiency Gains Drive Adoption in Consumer Electronics

The relentless push towards smaller, more powerful electronic devices has created unprecedented demand for compact thermal management solutions, positioning thermoelectric modules (TEMs) as a critical enabling technology. Unlike traditional compressor-based cooling systems, TEMs offer solid-state reliability, precise temperature control, and scalability down to millimeter-scale dimensions. This has proven particularly valuable for high-performance computing applications, where maintaining junction temperatures within strict parameters directly impacts processor longevity and performance. The global consumer electronics segment, which accounted for over 35% of TEM applications in 2024, continues to drive innovation in module design and materials science. Recent developments in bismuth telluride-based semiconductors have achieved coefficient of performance (COP) improvements exceeding 15% compared to previous generations, making TEMs increasingly viable for mainstream applications beyond niche cooling requirements.

Other Trends

Energy Harvesting Applications Gain Traction

While thermoelectric modules have traditionally been employed for active cooling, their ability to convert waste heat into usable electrical energy is emerging as a significant growth vector. Industrial applications leveraging this capability grew at approximately 18% annually between 2022-2024, particularly in automotive exhaust heat recovery and industrial process monitoring. The scalability of TEM systems allows for deployment in scenarios ranging from microwatt energy harvesting for wireless sensors to kilowatt-scale systems for manufacturing facilities. This dual-function capability—both cooling and power generation—provides unique value propositions that conventional thermal management technologies cannot match, especially in remote or energy-constrained environments where operational efficiency is paramount.

Medical and Scientific Applications Demand Higher Precision

The medical and laboratory equipment sector represents one of the most technically demanding segments for thermoelectric modules, requiring temperature stability within ±0.1°C for sensitive diagnostic equipment and storage applications. This precision requirement has driven manufacturers to develop multi-stage TEM configurations capable of achieving temperature differentials exceeding 70°C, enabling portable medical devices that maintain reagent integrity in ambient temperatures up to 40°C. The pharmaceutical cold chain logistics market, valued at over $15 billion globally, increasingly incorporates TEM-based portable containers for temperature-sensitive vaccine transport, particularly in last-mile delivery scenarios where traditional cooling methods prove impractical. Furthermore, the integration of advanced temperature control algorithms with TEM systems has enabled adaptive thermal management that responds to changing environmental conditions in real-time, a critical capability for field-deployable medical equipment.

Automotive Electrification Creates New Thermal Challenges

The rapid transition to electric vehicles (EVs) has generated substantial new demand for thermal management solutions that address unique challenges in battery systems, power electronics, and passenger comfort. TEMs are increasingly deployed in battery thermal management systems (BTMS) where maintaining optimal temperature ranges (typically 15-35°C) significantly impacts battery life, safety, and performance. With global EV production exceeding 10 million units annually, the addressable market for automotive-grade TEMs has expanded dramatically. Recent innovations include integrated thermoelectric systems that provide both heating and cooling functions using the same hardware, reducing complexity and weight compared to conventional HVAC systems. This capability proves particularly valuable in extreme climates where both cabin heating and battery cooling may be required simultaneously, presenting thermal management challenges that conventional systems struggle to address efficiently.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Companies Focus on Technological Innovation and Global Expansion

The global thermoelectric modules market exhibits a semi-consolidated structure, characterized by the presence of established multinational corporations, specialized mid-sized enterprises, and emerging regional players. Ferrotec and II-VI Marlow collectively command a significant portion of the market, holding approximately 40% of the global revenue share as of 2024. Their dominance stems from extensive product portfolios, robust R&D capabilities, and strong distribution networks across key regions including Asia-Pacific, North America, and Europe.

Laird Thermal Systems and KELK Ltd. also maintain considerable market positions, particularly in the consumer electronics and automotive sectors. These companies leverage their expertise in precision temperature control and miniaturization technologies to cater to the evolving demands for energy-efficient cooling solutions. Their growth is further propelled by strategic partnerships with OEMs and continuous investments in expanding production capacities.

Meanwhile, Chinese manufacturers like Guangdong Fuxin Technology and Thermonamic Electronics are rapidly gaining traction, driven by cost-competitive offerings and strong domestic demand. These players are increasingly focusing on enhancing product quality and obtaining international certifications to penetrate Western markets. Their aggressive pricing strategies and scaling production capabilities are reshaping competitive dynamics, particularly in price-sensitive segments.

Established players are responding by accelerating innovation cycles and pursuing strategic acquisitions. For instance, CUI Devices recently expanded its thermoelectric cooler series for high-density applications, while Phononic secured additional funding to advance its solid-state cooling technology. Such developments indicate intensifying competition centered on product performance, reliability, and customization capabilities.

List of Key Thermoelectric Modules Companies Profiled

- Ferrotec (USA)

- II-VI Marlow (USA)

- Laird Thermal Systems (USA)

- KELK Ltd. (Canada)

- Z-MAX (Japan)

- RMT Ltd. (Russia)

- Guangdong Fuxin Technology (China)

- Thermion Company (USA)

- Crystal Ltd (China)

- CUI Devices (USA)

- Kryotherm Industries (Russia)

- Phononic (USA)

- Merit Technology Group (China)

- TE Technology (USA)

- KJLP electronics co., ltd (South Korea)

- Thermonamic Electronics (China)

Segment Analysis:

By Type

Single Stage Module Segment Dominates the Market Due to its Cost-Effectiveness and Widespread Use in Consumer Electronics

The market is segmented based on type into:

- Single Stage Module

- Multiple Modules

- Others (Micromodules, Etc.)

By Application

Consumer Electronics Segment Leads Due to High Demand for Compact Cooling Solutions in Portable Devices

The market is segmented based on application into:

- Consumer Electronics

- Communication

- Medical Experiment

- Automobile

- Industrial

- Aerospace & Defense

- Others

By End User

Electronics Manufacturing Segment Holds Significant Share Owing to Integration in Various Electronic Products

The market is segmented based on end user into:

- Electronics Manufacturers

- Automotive OEMs

- Medical Device Companies

- Research Institutions

- Aerospace & Defense Contractors

By Technology

Bismuth Telluride-Based Modules Lead the Market Due to Superior Thermoelectric Properties at Room Temperature

The market is segmented based on technology into:

- Bismuth Telluride (Bi2Te3)

- Lead Telluride (PbTe)

- Silicon-Germanium (SiGe)

- Skutterudites

- Others

Regional Analysis: Thermoelectric Modules Market

Asia-Pacific

The Asia-Pacific region is the dominant force in the global thermoelectric modules market, accounting for the largest market share of approximately 28% as of 2024. This leadership is primarily driven by China’s massive manufacturing ecosystem for consumer electronics and telecommunications equipment, which are the two largest application segments for these modules. The region benefits from robust production capabilities, significant investments in R&D, and a strong presence of key manufacturers like Guangdong Fuxin Technology. Furthermore, rapid industrialization, growing automotive production, and increasing adoption of energy-efficient cooling solutions in data centers across countries like Japan, South Korea, and India are propelling demand. Japan, in particular, holds a significant share of about 20% globally, supported by its advanced technological landscape and presence of major players. The region’s growth is further fueled by government initiatives promoting electronic manufacturing and a continuous shift towards miniaturization and precision temperature control in various industries.

North America

North America represents the second-largest market for thermoelectric modules, holding a share of about 23%. This region is characterized by high technological adoption and stringent performance requirements across its key industries. The United States is the major contributor, driven by strong demand from the aerospace and defense sectors for reliable thermal management in avionics and surveillance systems, as well as from the medical industry for precise temperature control in diagnostic and laboratory equipment. The presence of leading manufacturers such as II-VI Marlow and Laird Thermal Systems fosters innovation and caters to the need for high-reliability modules. Additionally, the growing focus on energy efficiency and the development of electric vehicles, which utilize thermoelectric modules for battery thermal management and cabin climate control, are creating new growth avenues. The market is mature but continues to evolve with advancements in material science and increasing applications in renewable energy systems.

Europe

Europe holds a significant position in the global thermoelectric modules market, driven by a strong industrial base and a high emphasis on research and innovation. The automotive industry is a major consumer, particularly in Germany, where modules are used in advanced driver-assistance systems (ADAS), infotainment units, and seat climate control. Strict regulations on vehicle emissions and a push towards electric mobility are further incentivizing the adoption of efficient thermal solutions. The region also has a well-established medical device sector, which relies on thermoelectric technology for applications requiring stable and precise temperature environments. Furthermore, initiatives related to energy efficiency and sustainability, supported by EU policies, are encouraging the use of solid-state heat pumps in various industrial processes. While the market is advanced, competition from Asian manufacturers and cost pressures remain challenges that European companies address through focus on high-value, customized solutions.

South America

The thermoelectric modules market in South America is emerging and is characterized by gradual growth, primarily influenced by the industrial and automotive sectors in countries like Brazil and Argentina. The region’s economic volatility and infrastructure limitations have historically restrained widespread adoption. However, increasing industrialization and the modernization of manufacturing facilities are creating opportunities for these modules in process control and equipment cooling. The automotive industry, though smaller than in other regions, presents potential for growth as vehicle production incorporates more electronic components requiring thermal management. The market is cost-sensitive, which often leads to a preference for standard, single-stage modules. While the adoption of advanced multi-stage or micro-modules is slower, long-term prospects are tied to economic stabilization and increased investment in technological upgrades across key industries.

Middle East & Africa

The market for thermoelectric modules in the Middle East & Africa is nascent but shows potential for future development. Growth is primarily driven by infrastructure development, particularly in the Gulf Cooperation Council (GCC) countries like the UAE and Saudi Arabia, where investments in telecommunications, data centers, and oil & gas instrumentation are creating demand for reliable cooling solutions. The extreme climatic conditions in the region also necessitate robust thermal management for outdoor electronic equipment. However, the market faces challenges such as limited local manufacturing, reliance on imports, and a focus on cost-effective solutions over high-performance alternatives. In Africa, economic constraints and underdeveloped industrial sectors slow market penetration, though specific applications in medical storage and telecommunications base stations offer niche opportunities. Overall, the market is expected to grow gradually, aligned with broader economic diversification and technological adoption trends in the region.

Report Scope

This market research report provides a comprehensive analysis of the global Thermoelectric Modules market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Thermoelectric Modules Market?

-> Thermoelectric Modules Market was valued at 860 million in 2024 and is projected to reach US$ 1863 million by 2032, at a CAGR of 12.0% during the forecast period.

Which key companies operate in Global Thermoelectric Modules Market?

-> Key players include Ferrotec, II-VI Marlow, KELK Ltd., Laird Thermal Systems, and Guangdong Fuxin Technology, among others. The top three companies hold approximately 40% of the global market share.

What are the key growth drivers?

-> Key growth drivers include increasing demand for precise temperature control in consumer electronics, growing adoption in automotive applications, and advancements in medical and laboratory equipment requiring reliable cooling solutions.

Which region dominates the market?

-> China is the largest market with approximately 28% share, followed by North America (23%) and Japan (20%). Asia-Pacific demonstrates the fastest growth rate due to expanding electronics manufacturing and industrial base.

What are the emerging trends?

-> Emerging trends include development of high-efficiency thermoelectric materials, integration with IoT for smart temperature management, miniaturization of modules for portable devices, and growing application in renewable energy systems for waste heat recovery.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...