MARKET INSIGHTS

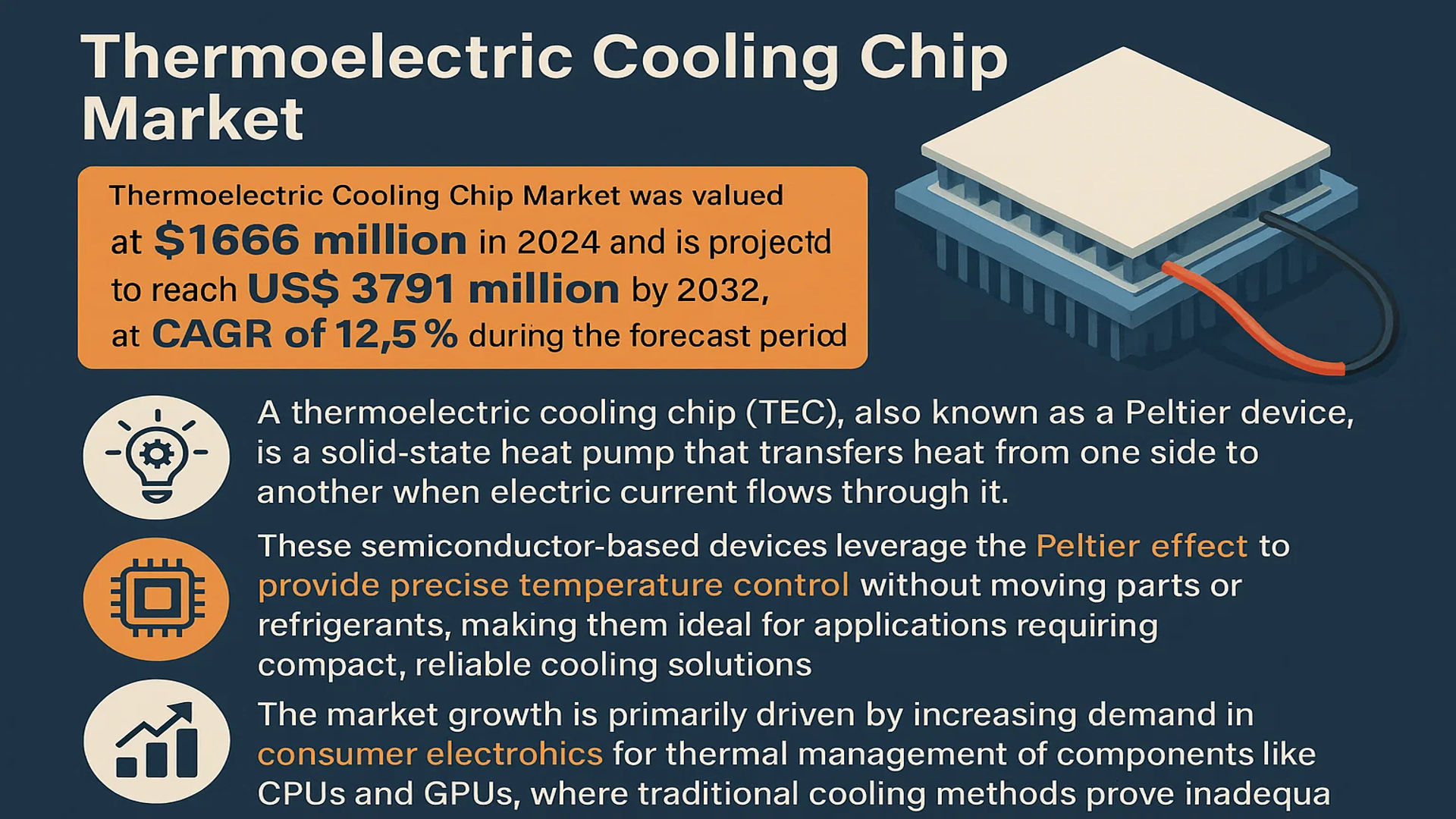

The global Thermoelectric Cooling Chip Market was valued at 1666 million in 2024 and is projected to reach US$ 3791 million by 2032, at a CAGR of 12.5% during the forecast period.

A thermoelectric cooling chip (TEC), also known as a Peltier device, is a solid-state heat pump that transfers heat from one side to another when electric current flows through it. These semiconductor-based devices leverage the Peltier effect to provide precise temperature control without moving parts or refrigerants, making them ideal for applications requiring compact, reliable cooling solutions.

The market growth is primarily driven by increasing demand in consumer electronics for thermal management of components like CPUs and GPUs, where traditional cooling methods prove inadequate. However, the medical sector presents significant opportunities as TECs enable precise temperature control in diagnostic equipment and laboratory devices. Leading manufacturers including Laird Thermal Systems and Ferrotec are investing in advanced materials to improve energy efficiency, addressing one of the key challenges in wider TEC adoption.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Energy-Efficient Cooling Solutions Driving Market Growth

The global push toward energy efficiency across industries is significantly boosting the thermoelectric cooling chip market. With increasing energy costs and sustainability regulations, industries are actively seeking alternatives to traditional compressor-based cooling systems. Thermoelectric coolers (TECs) offer 25-30% higher energy efficiency in targeted cooling applications compared to conventional methods, making them ideal for precision temperature control. The consumer electronics sector alone accounts for over 35% of TEC adoption, driven by the need to cool processors in smartphones, gaming consoles, and wearable devices without moving parts or refrigerants.

Expanding Medical Applications Creating New Growth Avenues

Medical applications are emerging as a key growth sector with thermoelectric chips being widely adopted in portable medical devices, laboratory equipment, and diagnostic systems. The ability to maintain precise temperature ranges (±0.1°C) makes TECs indispensable for PCR machines, blood analyzers, and vaccine storage units. The medical segment is projected to grow at 14.2% CAGR through 2032, accelerated by post-pandemic healthcare infrastructure expansion. Recent developments include compact TE cooling modules for wearable health monitors that require silent, vibration-free operation – a capability unmatched by mechanical systems.

➤ The global telemedicine market, expected to reach $380 billion by 2030, will further drive demand for portable medical devices employing thermoelectric cooling technology.

Automotive Industry Electrification Fueling Adoption

Vehicle electrification represents perhaps the most transformative driver for thermoelectric technologies. With electric vehicles requiring sophisticated thermal management for batteries and onboard electronics, automakers are integrating TE modules at an unprecedented rate. Leading EV manufacturers currently allocate 12-15% of thermal budget to solid-state cooling solutions. The trend extends beyond passenger vehicles – commercial truck operators are adopting TE-based refrigerated transport systems that offer superior reliability over mechanical units in continuous operation scenarios.

MARKET RESTRAINTS

High Production Costs Limiting Widespread Adoption

Despite their advantages, thermoelectric cooling chips face significant adoption barriers due to manufacturing complexities. The specialized bismuth telluride semiconductor materials used in most commercial TECs can cost 3-5 times more than conventional cooling components. Material scarcity further compounds this challenge – tellurium remains a relatively rare byproduct of copper refining, with annual global production unable to meet projected demand. These cost factors currently restrict TEC implementation to high-value applications where performance benefits outweigh economic considerations.

Performance Limitations in High-Capacity Applications

Thermoelectric cooling fundamentally faces thermodynamic constraints that limit its effectiveness in large-scale applications. While excelling in precise, small-scale cooling scenarios, TECs become increasingly inefficient when required to manage heat loads above 500W. This makes them unsuitable for industrial cooling or building climate control without extensive (and costly) module arrays. The coefficient of performance (COP) for thermoelectric systems rarely exceeds 0.6 in practical applications – significantly lower than vapor-compression systems that typically achieve COPs between 2.0-4.0.

MARKET OPPORTUNITIES

Emerging Materials Science Creating New Possibilities

Breakthroughs in semiconductor materials present the most promising opportunity for market expansion. Researchers have demonstrated ZT values exceeding 2.0 in experimental skutterudite and half-Heusler compounds – nearly double the performance of traditional bismuth telluride. Commercialization of these materials could revolutionize the industry by enabling thermoelectric systems to compete in broader applications. Several startups have already secured Series B funding to scale production of next-generation TE materials, with pilot plants expected within three years.

5G Infrastructure Expansion Driving Demand

The global rollout of 5G networks is creating substantial demand for thermal management solutions in base stations and edge computing nodes. Thermoelectric coolers are uniquely suited for these applications due to their compact size, directional cooling capability, and reliability in outdoor environments. Network equipment providers are projected to increase TEC adoption by 18% annually through 2030 as they address the thermal challenges of high-frequency mmWave technologies. This represents a largely untapped market segment that could account for 22-25% of industry revenue by the decade’s end.

MARKET CHALLENGES

Supply Chain Vulnerabilities Impacting Market Stability

The thermoelectric cooling industry faces significant supply chain risks due to concentrated material sourcing. Over 85% of bismuth production originates from just four countries, creating potential bottlenecks during geopolitical disruptions. Recent trade restrictions have already caused price volatility in tellurium markets, with costs fluctuating by as much as 40% within single quarters. Manufacturers are struggling to maintain stable pricing structures, forcing some to implement restrictive order minimums or extended lead times for customers.

Technical Challenges

Thermal Stress Management

Repeated thermal cycling creates mechanical stresses at semiconductor junctions that can reduce module lifespan. While newer designs have improved durability, field data shows average TE systems still experience 15-20% performance degradation after five years of continuous operation – a concern for mission-critical applications.

Standardization Issues

The absence of universal performance metrics complicates procurement decisions across industries. Unlike traditional cooling systems rated by BTU/hour or tons of refrigeration, TE modules currently lack standardized rating methodologies, creating confusion in specification processes.

THERMOELECTRIC COOLING CHIP MARKET TRENDS

Advancements in Solid-State Cooling Technology Fuel Market Expansion

The thermoelectric cooling chip market is experiencing robust growth due to significant advancements in solid-state cooling solutions. Unlike traditional compressor-based systems, thermoelectric modules offer precise temperature control, compact size, and silent operation, making them ideal for applications in medical devices, automotive systems, and high-performance electronics. The market is projected to grow from $1.66 billion in 2024 to $3.79 billion by 2032, driven by a CAGR of 12.5%. Recent innovations in semiconductor materials, such as bismuth telluride-based alloys, have improved energy efficiency by 15-20%, enhancing adoption in miniaturized electronic devices.

Other Trends

Rising Demand for Energy-Efficient Cooling Solutions

Environmental regulations and energy conservation initiatives are pushing industries toward sustainable cooling alternatives. Thermoelectric cooling chips consume up to 30% less energy than conventional refrigeration systems in specific applications, making them a preferred choice for data centers and electric vehicles. The automotive sector alone accounts for nearly 18% of the global demand, with TECs being widely used in battery thermal management systems for EVs. This trend is further supported by government incentives promoting green technologies.

Expansion in Consumer Electronics and Healthcare Sectors

The proliferation of IoT devices and portable medical equipment has amplified the need for reliable, compact cooling solutions. Single-stage TECs dominate the market with a 60% revenue share in 2024, favored for their cost-effectiveness in consumer electronics like gaming consoles and smartphones. Meanwhile, multi-stage TECs are gaining traction in medical applications, particularly in PCR machines and portable diagnostic devices, where precise temperature stability is critical. The healthcare segment is expected to grow at 14.3% CAGR, outpacing other verticals due to increased R&D in biomedical instrumentation.

COMPETITIVE LANDSCAPE

Key Industry Players

Thermoelectric Cooling Chip Manufacturers Expand Capacities to Meet Rising Demand

The global thermoelectric cooling chip (TEC) market features a dynamic competitive landscape with both established multinational players and emerging regional manufacturers. Ferrotec Corporation leads the market with its extensive portfolio spanning single-stage and multi-stage TEC modules, catering to consumer electronics, automotive, and industrial applications. The company’s strong supply chain integration and technological prowess enable it to maintain a dominant position across North America and Asia-Pacific.

Laird Thermal Systems and TE Technology have solidified their market positions through continuous innovation in high-performance cooling solutions. In 2024, these companies collectively accounted for approximately 28% of global TEC revenue, demonstrating their technological leadership in precision temperature control applications for medical devices and telecommunications equipment.

Market competition intensifies as Chinese manufacturers like Guangdong Fuxin Technology and Zhejiang Advanced Thermoelectric Technology expand their production capacities. With cost-competitive offerings and improving product quality, these players are increasingly winning contracts in price-sensitive markets, particularly in the automotive and consumer electronics segments where thermal management requirements continue to grow.

Recent strategic moves include Coherent Corp’s acquisition of specialty thermoelectric materials suppliers to vertically integrate its supply chain, while KELK has partnered with automotive OEMs to develop next-generation battery cooling solutions for electric vehicles. Such developments indicate the market’s evolution toward application-specific solutions rather than standard off-the-shelf products.

List of Key Thermoelectric Cooling Chip Manufacturers

- Ferrotec Corporation (Japan)

- Laird Thermal Systems (U.S.)

- TE Technology, Inc. (U.S.)

- Coherent Corp (U.S.)

- TEC Microsystems GmbH (Germany)

- Guangdong Fuxin Technology (China)

- Thermonamic Electronics (China)

- KELK Ltd. (Japan)

- Zhejiang Advanced Thermoelectric Technology (China)

- Z-MAX Co. Ltd. (South Korea)

- Kryotherm (Russia)

- Kyocera Corporation (Japan)

Segment Analysis:

By Type

Single-Stage TEC Segment Leads Thermoelectric Cooling Chip Market Due to Compact Design and Cost Efficiency

The market is segmented based on type into:

- Single-Stage TEC

- Multi-Stage TEC

- Other

By Application

Consumer Electronics Segment Dominates Owing to Increased Demand for Compact Cooling Solutions

The market is segmented based on application into:

- Consumer Electronics

- Communications

- Medical

- Automobile

- Industry

- Aerospace and Defense

- Other

By Power Range

Low Power Modules Hold Significant Share in Thermoelectric Cooling Market

The market is segmented based on power range into:

- Low Power (Below 20W)

- Medium Power (20W-100W)

- High Power (Above 100W)

By Material Type

Bismuth Telluride-Based Materials Dominate Due to High Conversion Efficiency

The market is segmented based on material type into:

- Bismuth Telluride (Bi2Te3)

- Lead Telluride (PbTe)

- Silicon-Germanium (SiGe)

- Other Materials

Regional Analysis: Thermoelectric Cooling Chip Market

Asia-Pacific

Asia-Pacific dominates the global thermoelectric cooling chip (TEC) market, accounting for over 40% of global demand, driven by China’s robust electronics manufacturing ecosystem. China’s semiconductor industry, valued at $150 billion in 2024, heavily relies on TECs for thermal management in consumer electronics, 5G infrastructure, and automotive applications. Japan leads in high-efficiency multi-stage TEC production, with key players like Kyocera Corporation and KELK catering to precision cooling needs in medical and aerospace sectors. India shows rapid adoption in telecom base stations and electric vehicle battery cooling, though local manufacturing remains limited. The region benefits from cost-competitive supply chains and government initiatives like Japan’s “Moonshot R&D Program” supporting next-gen TEC development.

North America

The North American market, valued at approximately $480 million in 2024, thrives on technological advancements and defense sector demand. The U.S. accounts for 85% of regional consumption, with companies like Laird Thermal Systems and TE Technology supplying TECs for military communications, laser systems, and electric vehicle inverters. Stringent FDA standards accelerate medical TEC adoption, particularly in portable diagnostic devices. However, reliance on Asian imports for mass-produced single-stage TECs presents supply chain vulnerabilities, prompting initiatives like the “CHIPS and Science Act” to strengthen domestic semiconductor infrastructure.

Europe

Europe’s market growth, projected at 9.8% CAGR through 2032, centers on sustainability and industrial automation. Germany’s automotive sector utilizes TECs for battery thermal management in EVs, while France leads in aerospace applications through collaborations between Safran and TEC Microsystems GmbH. EU directives on energy-efficient cooling solutions drive R&D in bismuth telluride-based modules, though higher production costs limit price competitiveness against Asian alternatives. The Nordic countries are emerging as innovation hubs for IoT-integrated TECs in data center cooling applications.

Middle East & Africa

This nascent market is gaining traction through infrastructure development in Gulf Cooperation Council (GCC) countries. The UAE and Saudi Arabia deploy TECs in telecom tower cooling systems and thermal management for solar energy plants, leveraging partnerships with global suppliers like Ferrotec. Africa’s growth is constrained by limited technical expertise and infrastructure, though South Africa shows potential in medical refrigeration applications. The region’s harsh climates create unique opportunities for high-temperature resistant TEC solutions.

South America

Brazil dominates the regional market with applications in automotive and food preservation, supported by investments in semiconductor R&D centers. Argentina’s niche medical device industry utilizes imported multi-stage TECs. Economic instability and import dependency hinder widespread adoption, though local assembly initiatives by companies like Z-MAX Co. Ltd. aim to reduce lead times. The region’s focus on renewable energy systems could drive future TEC demand for power generation equipment cooling.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Thermoelectric Cooling Chip markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Thermoelectric Cooling Chip market was valued at USD 1,666 million in 2024 and is projected to reach USD 3,791 million by 2032, at a CAGR of 12.5%.

- Segmentation Analysis: Detailed breakdown by product type (Single-Stage TEC, Multi-Stage TEC, Others), application (Consumer Electronics, Communications, Medical, Automobile, Industry, Aerospace & Defense, Others), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America (U.S., Canada, Mexico), Europe (Germany, France, U.K., Italy, Russia), Asia-Pacific (China, Japan, South Korea, India), Latin America, and Middle East & Africa.

- Competitive Landscape: Profiles of 18 leading market participants including Coherent Corp, Ferrotec, Laird Thermal Systems, TE Technology, and Kyocera Corporation, with their market share, product portfolios, and strategic developments.

- Technology Trends: Assessment of semiconductor material innovations, miniaturization trends, and integration with IoT/AI systems for smart thermal management.

- Market Drivers & Restraints: Evaluation of factors including demand for energy-efficient cooling, growth in electronics miniaturization, and challenges related to material costs and efficiency limitations.

- Stakeholder Analysis: Strategic insights for semiconductor manufacturers, OEMs, system integrators, and investors regarding emerging opportunities in thermal management solutions.

The research methodology combines primary interviews with industry leaders and analysis of verified market data from regulatory bodies, trade associations, and financial reports to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Thermoelectric Cooling Chip Market?

-> Thermoelectric Cooling Chip Market was valued at 1666 million in 2024 and is projected to reach US$ 3791 million by 2032, at a CAGR of 12.5% during the forecast period.

Which key companies operate in Global Thermoelectric Cooling Chip Market?

-> Key players include Coherent Corp, Ferrotec, Laird Thermal Systems, TE Technology, Kyocera Corporation, Guangdong Fuxin Technology, and KELK, among others.

What are the key growth drivers?

-> Key growth drivers include increasing demand for compact cooling solutions in electronics, growth in medical device applications, and automotive thermal management requirements.

Which region dominates the market?

-> Asia-Pacific leads in market share due to electronics manufacturing concentration, while North America shows strong growth in medical and defense applications.

What are the emerging trends?

-> Emerging trends include development of high-efficiency thermoelectric materials, integration with 5G infrastructure, and adoption in electric vehicle battery cooling systems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...