MARKET INSIGHTS

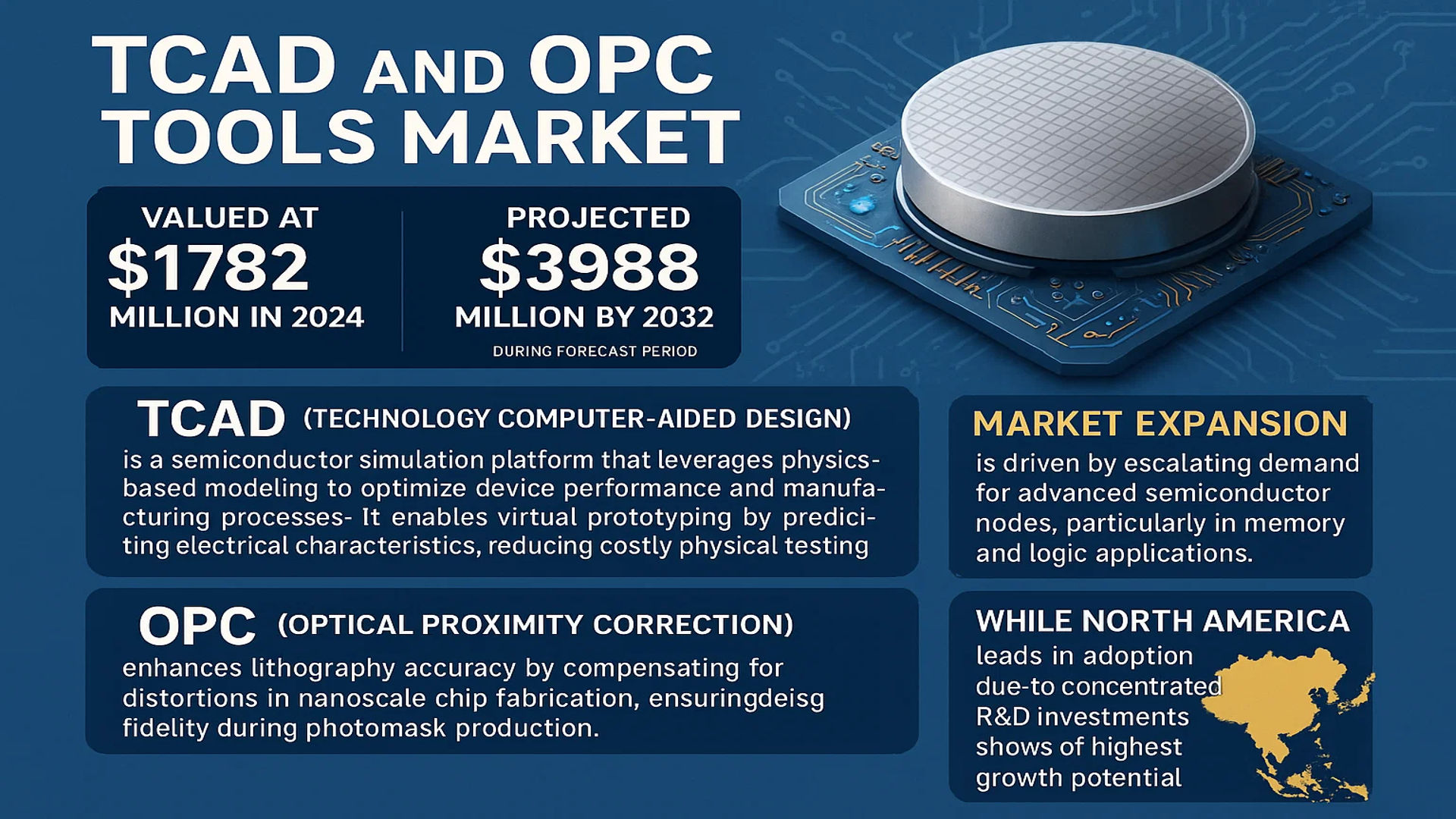

The global TCAD and OPC Tools Market was valued at 1782 million in 2024 and is projected to reach US$ 3988 million by 2032, at a CAGR of 12.2% during the forecast period.

TCAD (Technology Computer-Aided Design) is a semiconductor simulation platform that leverages physics-based modeling to optimize device performance and manufacturing processes. It enables virtual prototyping by predicting electrical characteristics, reducing costly physical testing cycles. OPC (Optical Proximity Correction) enhances lithography accuracy by compensating for distortions in nanoscale chip fabrication, ensuring design fidelity during photomask production.

Market expansion is driven by escalating demand for advanced semiconductor nodes, particularly in memory and logic applications. While North America leads in adoption due to concentrated R&D investments, Asia-Pacific shows the highest growth potential because of expanding foundry capacities. Key players like Synopsys and ASML dominate the competitive landscape, collectively holding over 60% market share as of 2024. Recent developments include AI-powered simulation enhancements and cloud-based deployment models, which are reducing computational bottlenecks for complex designs.

MARKET DYNAMICS

MARKET DRIVERS

Advancements in Semiconductor Miniaturization to Propel TCAD and OPC Adoption

The relentless push toward smaller semiconductor nodes below 7nm is creating unprecedented demand for TCAD and OPC tools. As foundries transition to advanced process technologies, the complexity of modeling quantum effects and lithography distortions increases exponentially. This has led to over 30% year-over-year growth in TCAD tool adoption among leading edge semiconductor manufacturers. The ability to simulate FinFET and GAA transistor behaviors before costly fabrication runs provides a critical competitive advantage in today’s market.

Growing Complexity of Multi-Patterning Techniques Driving OPC Innovation

Modern EUV lithography processes now routinely employ complex multi-patterning approaches to achieve sub-20nm feature sizes. This has created a pressing need for more sophisticated OPC solutions that can handle the intricate interactions between multiple mask layers. The number of correction iterations required has increased 5x compared to conventional single-patterning nodes, compelling foundries to upgrade their OPC toolchains. Leading semiconductor manufacturers are allocating 15-20% of their R&D budgets specifically for advanced OPC solutions to maintain yield rates above 90%.

Expansion of Memory and Logic Applications Boosting Market Growth

The proliferation of high-density memory technologies including 3D NAND and DRAM is creating substantial demand for specialized TCAD applications. Memory manufacturers require precise simulation of vertical charge trap layers and complex channel behaviors that differ markedly from traditional logic devices. Simultaneously, the AI accelerator market is driving innovation in TCAD for novel architectures like in-memory computing. This dual demand from both memory and logic sectors is projected to contribute over 40% of total market growth through the forecast period.

MARKET RESTRAINTS

High Implementation Costs Restricting SME Adoption

The substantial capital expenditure required for advanced TCAD and OPC solutions creates significant barriers to market expansion. Comprehensive toolchains often require multimillion-dollar investments in both software licenses and supporting HPC infrastructure. This pricing structure effectively limits adoption to large semiconductor corporations, with small and mid-sized design houses priced out of the market. Recent data suggests the total cost of ownership for a full-featured TCAD/OPC environment can exceed $5 million annually when including maintenance and compute costs.

Specialized Workforce Shortage Creating Implementation Bottlenecks

The semiconductor industry currently faces a critical shortage of engineers with expertise in both device physics and computational modeling. The specialized skills required to properly configure and interpret TCAD simulations are particularly scarce, with estimates suggesting a global deficit of over 15,000 qualified professionals. This skills gap is further exacerbated by the extended training periods required – typically 12-18 months for engineers to become proficient with advanced simulation tools. The resulting productivity losses and implementation delays are constraining market growth despite strong underlying demand.

MARKET CHALLENGES

Model Accuracy Limitations at Advanced Nodes

As semiconductor features approach atomic scales, traditional TCAD models struggle to accurately capture quantum mechanical effects and atomic-level variations. The discrepancy between simulated and actual device performance has grown to as much as 15-20% for cutting-edge 3nm nodes, eroding confidence in simulation results. This challenge is particularly acute for emerging materials like 2D semiconductors and oxide channels that lack established modeling parameters. The industry urgently needs next-generation quantum-aware TCAD solutions to maintain simulation relevance.

Computational Scaling Issues with Advanced OPC

The computational demands of modern OPC algorithms are growing exponentially with each process node. Full-chip mask correction for a contemporary 5nm design can require over 10 million CPU core-hours, creating unsustainable infrastructure costs. The situation is further complicated by the transition to curvilinear mask patterns which increase computational complexity by an order of magnitude. Without breakthroughs in algorithmic efficiency or specialized hardware acceleration, the time and cost of OPC processing threatens to become a limiting factor for semiconductor scaling.

MARKET OPPORTUNITIES

Cloud-Based Solutions Opening New Markets

The emergence of cloud-optimized TCAD and OPC solutions is creating significant expansion opportunities. By reducing upfront capital requirements and providing elastic compute scaling, cloud deployments make these tools accessible to mid-sized semiconductor companies. Early adopters report 30-40% cost reductions compared to on-premise implementations while maintaining equivalent performance. This shift is particularly compelling for fabless design firms and academic researchers who previously lacked access to enterprise-grade simulation tools.

AI-Enhanced Tools Driving Productivity Gains

The integration of machine learning techniques into TCAD and OPC workflows is creating transformative efficiency improvements. Neural network acceleration of iterative OPC corrections has demonstrated runtime reductions of 50-70% while maintaining comparable accuracy. Similarly, AI-powered parameter extraction in TCAD can reduce simulation setup times from weeks to hours. These productivity gains are making simulation-driven design methodologies practical for mainstream semiconductor development rather than being limited to specialized applications.

Emerging Materials Creating New Simulation Requirements

The semiconductor industry’s exploration of novel materials like GaN, SiC, and 2D semiconductors represents a substantial growth vector for TCAD providers. Each new material system requires specialized physical models and parameter libraries, creating opportunities for vendors offering comprehensive material-specific solutions. The power electronics market alone is projected to drive over $200 million in specialized TCAD revenue by 2028 as these technologies transition from research to volume production.

TCAD AND OPC TOOLS MARKET TRENDS

Adoption of Advanced Semiconductor Nodes to Drive Market Growth

The increasing demand for high-performance semiconductor devices has propelled the adoption of TCAD and OPC tools, particularly for nodes below 7nm. Leading foundries and integrated device manufacturers (IDMs) are leveraging these tools to optimize lithography and process simulation, ensuring higher accuracy in manufacturing advanced chips. The global TCAD and OPC tools market is projected to grow at a CAGR of 12.2% from 2024 to 2032, reflecting the industry’s shift toward sub-5nm and sub-3nm technologies. Furthermore, the integration of machine learning algorithms into TCAD and OPC solutions has enhanced pattern correction capabilities, reducing mask design iterations by up to 30% in some cases.

Other Trends

Rise of AI-Driven Simulation Tools

Artificial intelligence is transforming TCAD and OPC workflows by enabling predictive modeling and automated corrections. AI-based simulation tools are now capable of learning from historical process data to optimize device performance and yield, significantly reducing time-to-market. The growing complexity of 3D NAND and FinFET architectures has further necessitated the use of intelligent TCAD tools, which can model multi-physics interactions with high precision. Meanwhile, OPC enhancements now incorporate deep learning to predict and compensate for lithography-induced distortions in real-time.

Strategic Collaborations Fueling Innovation

The semiconductor industry is witnessing a surge in partnerships between TCAD/OPC tool vendors, foundries, and research institutions. These collaborations aim to accelerate the development of next-generation solutions tailored for emerging memory and logic applications. Recent agreements have focused on improving EUV lithography modeling and multi-patterning techniques critical for leading-edge nodes. Additionally, China’s aggressive investments in domestic semiconductor R&D are driving regional market expansion, with local players like Suzhou Peifeng Tunan Semiconductor gaining traction in the Asia-Pacific TCAD segment.

COMPETITIVE LANDSCAPE

Key Industry Players

Semiconductor Simulation Leaders Accelerate Innovation to Meet Advanced Node Demands

The global TCAD and OPC tools market exhibits a moderately consolidated structure with established players dominating the revenue share while emerging regional players make strategic inroads. Synopsys maintains market leadership with an estimated 28% revenue share in 2024, leveraging its comprehensive Sentaurus TCAD platform and Proteus OPC solution that support emerging technologies like Gate-All-Around (GAA) transistors. The company’s recent acquisition of Silicon Frontline Technology further enhanced its 3D TCAD modeling capabilities for advanced packaging applications.

Meanwhile, ASML and Siemens EDA have significantly expanded their market positions through vertical integration strategies. ASML’s Brion computational lithography solutions now account for nearly 18% of the OPC tools segment, benefiting from tighter integration with the company’s EUV lithography systems. Siemens strengthened its position through the 2023 acquisition of OneSpin Solutions, adding formal verification capabilities to complement its Simcenter TCAD offerings.

The competitive intensity is increasing as mid-tier players adopt specialized approaches. Silvaco has carved out a strong niche in TCAD for power semiconductor design, capturing over 12% of the analog/mixed-signal segment. Chinese contender Suzhou Peifeng Tunan Semiconductor demonstrated rapid growth with 40% year-over-year revenue increase in 2023, supported by government initiatives to boost domestic semiconductor IP development.

List of Key TCAD and OPC Tools Companies Profiled

- Synopsys, Inc. (U.S.)

- Siemens EDA (Germany)

- ASML Holding NV (Netherlands)

- Silvaco, Inc. (U.S.)

- Suzhou Peifeng Tunan Semiconductor Co., Ltd (China)

- Yuwei Optics (China)

- DJEL Corporation (Japan)

- GMPT Solutions (South Korea)

Market differentiation increasingly hinges on cloud-based deployment models and AI/ML integration. All major players now offer SaaS versions of their tools, with Siemens reporting that cloud-based licenses accounted for 32% of new TCAD tool deployments in 2023. The integration of machine learning for faster OPC convergence has become a key battleground, with Synopsys’ recent introduction of AI-driven pattern matching reducing OPC runtime by up to 40% compared to conventional methods.

Looking ahead, the competitive landscape will likely see further specialization as the industry bifurcates between providers focusing on cutting-edge nodes (sub-3nm) and those optimizing solutions for mature nodes (28nm and above). Strategic alliances between TCAD/OPC vendors and semiconductor manufacturers are expected to intensify, particularly in the development of application-specific simulation frameworks for emerging memory architectures and heterogeneous integration schemes.

Segment Analysis:

By Type

TCAD Tools Lead the Market Driven by Rising Demand for Semiconductor Process Simulation

The market is segmented based on type into:

- TCAD Tools

- Subtypes: Process Simulation, Device Simulation, and Others

- OPC Tools

- Subtypes: Rule-Based OPC, Model-Based OPC, and Others

By Application

Memory Segment Accounts for Major Share Due to High Demand for Advanced Memory Chip Design

The market is segmented based on application into:

- Memory

- Logic

- Others

By Region

Asia Pacific Captures Largest Market Share Owing to Strong Semiconductor Manufacturing Presence

The market is segmented based on region into:

- North America

- Asia Pacific

- Europe

- Rest of World

By End User

Foundries Represent Dominant Segment Given Intensive Use of TCAD/OPC in Chip Manufacturing

The market is segmented based on end user into:

- Foundries

- IDMs (Integrated Device Manufacturers)

- Fabless Semiconductor Companies

- Research Institutions

Regional Analysis: TCAD and OPC Tools Market

Asia-Pacific

The Asia-Pacific region dominates the global TCAD and OPC Tools market, driven primarily by China’s aggressive semiconductor expansion and substantial government investments in domestic chip manufacturing. With foundries like TSMC, Samsung, and SMIC accelerating process node development to 3nm and below, demand for advanced simulation and lithography correction tools has skyrocketed. China’s “Big Fund” semiconductor initiative has allocated over $50 billion to boost self-sufficiency, directly benefiting local TCAD providers like Suzhou Peifeng Tunan Semiconductor. Meanwhile, Japan and South Korea continue leveraging their legacy in semiconductor equipment manufacturing, with key players adopting hybrid solutions combining TCAD process modeling with EUV-compatible OPC tools.

North America

North America remains the innovation hub for TCAD and OPC technologies, housing industry leaders like Synopsys and Silvaco. The CHIPS and Science Act’s $52 billion funding has revitalized domestic semiconductor R&D, with major fabs under construction by Intel and TSMC requiring cutting-edge design verification tools. The region shows particular strength in physics-based TCAD solutions for novel architectures like GAAFETs, while OPC innovation focuses on machine learning approaches to handle EUV lithography complexities. Strict export controls on advanced EDA tools to China have paradoxically strengthened North American vendors’ competitive positioning in allied markets.

Europe

Europe’s market emphasizes precision TCAD solutions for automotive and industrial semiconductor applications, with Siemens EDA and ASML driving OPC advancements for mature nodes. The EU Chips Act’s €43 billion investment targets increasing Europe’s global semiconductor market share to 20% by 2030, creating opportunities for specialized TCAD tools in power electronics and MEMS. German research institutes like Fraunhofer lead in developing open-source TCAD platforms, while Dutch firms concentrate on computational lithography enhancements to support ASML’s EUV ecosystem. However, the region lags in cutting-edge logic process support compared to US and Asian competitors.

Middle East & Africa

The MEA region presents nascent growth potential, with Israel emerging as a surprising hotspot for TCAD startups focusing on photonics and quantum computing applications. While semiconductor manufacturing infrastructure remains limited, governments are investing in design capabilities – Saudi Arabia’s NEOM project includes plans for an analog semiconductor hub. South Africa’s growing fabless design industry drives basic TCAD adoption, though the market struggles with limited access to advanced OPC tools due to export restrictions and lack of local foundry partnerships.

South America

South America’s TCAD and OPC tools market remains underdeveloped, primarily serving academic and research institutions with basic process simulation needs. Brazil leads in local TCAD adoption through universities developing semiconductor R&D capabilities, while Argentina shows increasing demand for power device modeling tools. The lack of domestic semiconductor manufacturing and reliance on imported EDA solutions constrains market growth, though recent trade agreements may facilitate greater access to mid-range TCAD products from European vendors.

Report Scope

This market research report provides a comprehensive analysis of the Global TCAD and OPC Tools market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the semiconductor design and manufacturing industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, including the market value of USD 1,782 million in 2024 projected to reach USD 3,988 million by 2032 at a CAGR of 12.2%.

- Segmentation Analysis: Detailed breakdown by product type (TCAD Tools and OPC Tools), application (Memory, Logic, Others), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with country-level analysis for major markets including the US, China, Germany, Japan, and others.

- Competitive Landscape: Profiles of leading market participants including Synopsys, Silvaco, ASML, Siemens, and others, covering their product portfolios, market share, and strategic initiatives.

- Technology Trends & Innovation: Assessment of emerging semiconductor design technologies, integration of AI in TCAD/OPC tools, and advancements in photolithography correction techniques.

- Market Drivers & Restraints: Evaluation of factors such as growing semiconductor industry, miniaturization of chips, and challenges like high development costs and technical complexity.

- Stakeholder Analysis: Strategic insights for semiconductor manufacturers, EDA tool providers, foundries, investors, and policymakers regarding market opportunities.

The research methodology combines primary interviews with industry experts and secondary data from verified sources to ensure accuracy and reliability of market insights.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global TCAD and OPC Tools Market?

->TCAD and OPC Tools Market was valued at 1782 million in 2024 and is projected to reach US$ 3988 million by 2032, at a CAGR of 12.2% during the forecast period.

Which key companies operate in Global TCAD and OPC Tools Market?

-> Key players include Synopsys, Silvaco, ASML, Siemens, GMPT, DJEL, Suzhou Peifeng Tunan Semiconductor, and Yuwei Optics.

What are the key growth drivers?

-> Key growth drivers include increasing semiconductor complexity, demand for advanced nodes, and rising adoption of AI in chip design.

Which region dominates the market?

-> Asia-Pacific leads in market share due to semiconductor manufacturing growth, while North America dominates in tool development.

What are the emerging trends?

-> Emerging trends include cloud-based TCAD solutions, machine learning-enhanced OPC, and integration with 3D IC design tools.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...