TC Wafer Temperature Measurement Systems Market Insights

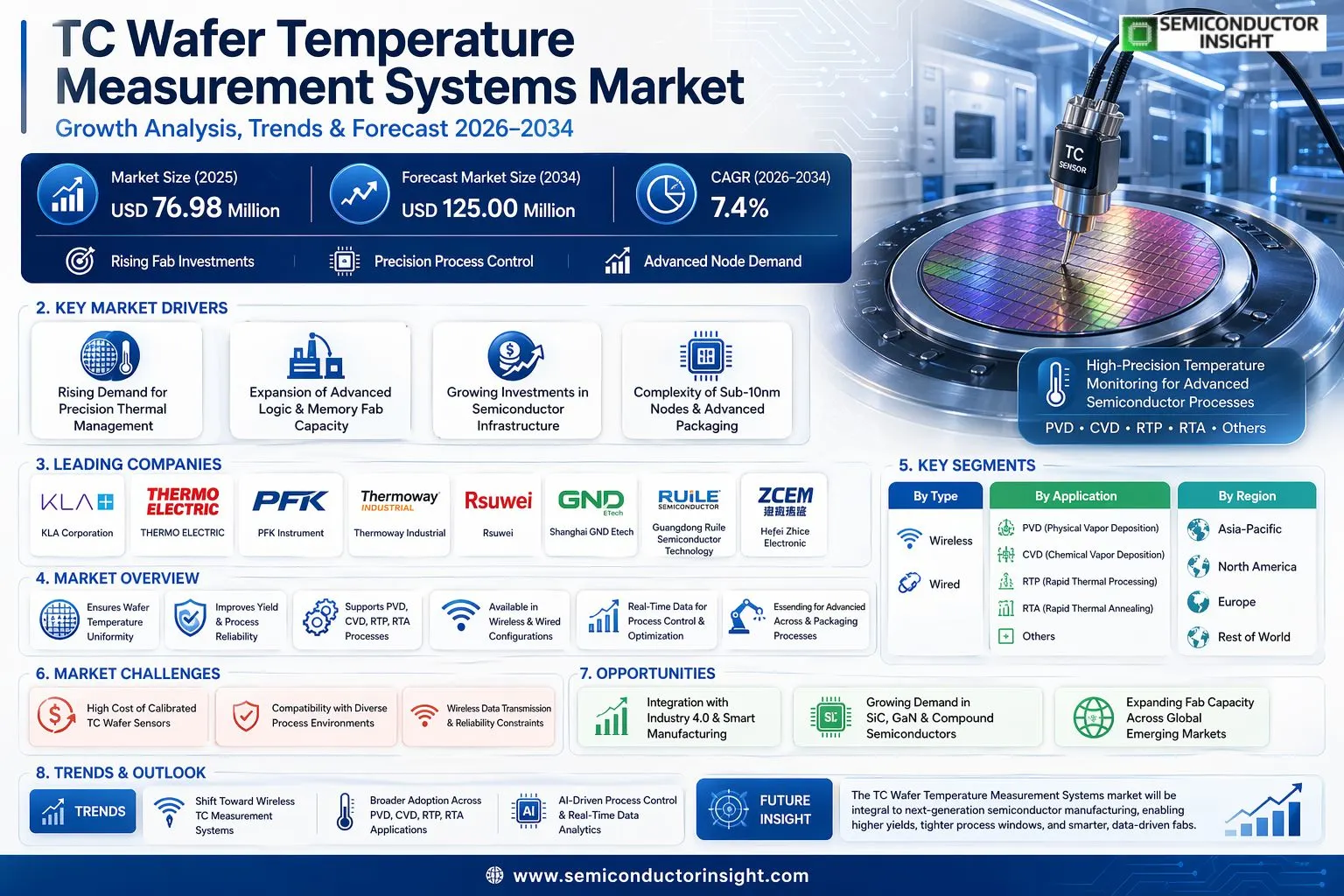

Global TC Wafer Temperature Measurement Systems market size was valued at USD 76.98 million in 2025. The market is projected to grow from USD 82.68 million in 2026 to USD 125 million by 2034, exhibiting a CAGR of 7.4% during the forecast period.

A TC Wafer Temperature Measurement System is a specialized instrument designed to precisely monitor and record the temperature of semiconductor wafers throughout the fabrication process. Its primary function is to ensure thermal stability across critical process steps, including Physical Vapor Deposition (PVD), Chemical Vapor Deposition (CVD), Rapid Thermal Processing (RTP), and Rapid Thermal Annealing (RTA), thereby safeguarding the structural integrity, yield, and electrical performance of the finished semiconductor device. These systems are available in both wired and wireless configurations, with the wireless segment gaining increasing traction in advanced fab environments due to its non-contact measurement capability and compatibility with automated wafer handling systems.

The market is witnessing sustained growth driven by the accelerating global demand for semiconductors, the proliferation of advanced node chipmaking, and increasingly stringent process control requirements at leading-edge fabs. Furthermore, the expansion of semiconductor manufacturing capacity across Asia, North America, and Europe , supported by government-backed initiatives such as the U.S. CHIPS and Science Act and the European Chips Act , is generating substantial demand for precision thermal metrology solutions. Key manufacturers operating in this market include KLA Corporation, THERMO ELECTRIC, PFK Instrument, Thermoway Industrial, Rsuwei, Shanghai GND Etech, Guangdong Ruile Semiconductor Technology, and Hefei Zhice Electronic, among others, collectively shaping a competitive and innovation-driven landscape.

MARKET DRIVERS

Expanding Semiconductor Fabrication Demand Propelling Adoption of Wafer Temperature Measurement Technologies

Global semiconductor industry continues to experience robust capital investment in advanced fabrication facilities, creating strong demand for precision thermal monitoring equipment. TC wafer temperature measurement systems have become indispensable in modern fabs, particularly as device geometries shrink below 5nm and thermal uniformity across the wafer surface becomes a critical process control parameter. As leading chipmakers accelerate construction of next-generation fabs across Asia, North America, and Europe, procurement of advanced in-situ temperature measurement solutions is rising in tandem, directly supporting market expansion.

Increasing Process Complexity in Advanced Node Manufacturing Driving Precision Thermal Control Requirements

As semiconductor process nodes advance, the thermal budget management during deposition, annealing, and etch processes has grown significantly more stringent. TC wafer temperature measurement systems provide engineers with real-time, spatially resolved thermal data that enables tighter closed-loop control of rapid thermal processing (RTP) and chemical vapor deposition (CVD) equipment. The transition to gate-all-around (GAA) transistor architectures and 3D NAND structures further intensifies the need for highly accurate thermocouple-based wafer sensors capable of resolving temperature gradients at the sub-millimeter scale, making these systems a technically non-negotiable component of leading-edge process development.

➤ Government-backed semiconductor self-sufficiency initiatives in the United States, European Union, South Korea, Japan, and China are collectively driving hundreds of billions in new fab investments through 2030, establishing a sustained multi-year demand pipeline for TC wafer temperature measurement systems and allied process control instrumentation.

Beyond logic and memory, the proliferation of compound semiconductor manufacturing for power electronics, RF devices, and photonics applications is opening additional addressable markets. Substrates such as silicon carbide (SiC) and gallium nitride (GaN) introduce unique thermal property challenges that require specialized TC wafer sensor configurations compared to conventional silicon processes. This diversification of end-use substrates is broadening the total addressable market for TC wafer temperature measurement system vendors and encouraging continuous product innovation across the competitive landscape.

MARKET CHALLENGES

High Cost of Ownership and Calibration Complexity Limiting Widespread Deployment Across Smaller Fabs

Despite their technical advantages, TC wafer temperature measurement systems present considerable cost-of-ownership challenges, particularly for small and mid-size semiconductor manufacturers operating on tighter capital budgets. Instrumented wafers used as temperature sensors are consumable items subject to degradation over repeated thermal cycles, necessitating periodic recalibration and replacement. The associated metrology infrastructure, including data acquisition hardware and process integration software, adds further to the total investment. For fabs prioritizing cost reduction over process optimization granularity, these economic barriers can delay or defer adoption decisions, constraining the pace of market penetration.

Other Challenges

Integration with Legacy Process Equipment

A significant portion of installed semiconductor manufacturing equipment globally was designed prior to the widespread adoption of advanced in-situ thermal metrology. Retrofitting TC wafer temperature measurement capabilities into legacy rapid thermal processors, furnaces, and CVD tools can require substantial engineering effort and may introduce process disturbances during qualification. The lack of standardized communication interfaces between measurement systems and legacy tool controllers further complicates integration, often requiring customized software development that extends deployment timelines and increases implementation costs for end users.

Data Management and Process Integration Complexity

TC wafer temperature measurement systems generate high-density, spatially distributed thermal datasets that must be accurately synchronized with process timestamps and equipment sensor logs to yield actionable process control insights. Managing and interpreting this data within existing manufacturing execution system (MES) and advanced process control (APC) frameworks presents a non-trivial integration challenge. As fabs increase their reliance on AI-driven process optimization, ensuring the accuracy, completeness, and latency of thermal measurement data streams becomes both a technical and organizational challenge that demands dedicated resources and expertise.

MARKET RESTRAINTS

Competition from Alternative Thermal Metrology Technologies Constraining Market Share Growth

TC wafer temperature measurement systems operate within a competitive metrology landscape that includes non-contact alternatives such as optical pyrometry, emissivity-corrected infrared thermometry, and acoustic thermometry. In certain high-volume production environments, non-contact methods offer advantages including zero risk of wafer contamination, compatibility with sealed process chambers, and elimination of consumable sensor costs. As pyrometric and infrared technologies continue to improve in accuracy and repeatability, particularly for reflective metallic wafer surfaces, they exert competitive pressure on thermocouple-based approaches. Vendors in TC Wafer Temperature Measurement Systems Market must continuously articulate and demonstrate performance advantages to defend market position against these alternative modalities.

Geopolitical and Supply Chain Uncertainties Creating Near-Term Market Volatility

Global semiconductor equipment industry, including suppliers of TC wafer temperature measurement systems, is subject to evolving export control regulations, trade restrictions, and supply chain disruptions that introduce near-term demand uncertainty. Restrictions on equipment exports to certain geographies can limit market access for system vendors, while concentration of critical raw material supply chains creates procurement risks. Additionally, the cyclical nature of semiconductor capital expenditure means that fab investment programs can be delayed or scaled back during industry downturns, directly impacting order volumes for precision process metrology equipment. These structural and geopolitical restraints require market participants to maintain flexible business models and geographically diversified customer bases to sustain revenue stability.

MARKET OPPORTUNITIES

Integration of AI and Machine Learning with TC Wafer Temperature Measurement Systems Unlocking Advanced Process Optimization Capabilities

The convergence of high-density thermal measurement data from TC wafer temperature measurement systems with AI-powered analytics platforms represents a compelling growth opportunity for technology vendors and system integrators. By applying machine learning models to spatially resolved wafer temperature profiles, fabs can identify systematic thermal non-uniformities, predict equipment maintenance needs before yield-impacting events occur, and accelerate process recipe development. Forward-looking vendors that embed intelligent data processing capabilities directly into their TC wafer measurement platforms , or that offer open APIs enabling seamless integration with third-party APC and AI solutions , are well positioned to capture premium value and deepen customer relationships in a market increasingly focused on digital transformation of fab operations.

Expansion into Emerging Power Semiconductor and Photovoltaic Manufacturing Segments Offering New Revenue Streams

Beyond traditional silicon logic and memory applications, TC wafer temperature measurement systems are finding growing relevance in the manufacturing of power semiconductors, solar photovoltaic cells, and advanced packaging processes. The accelerating global transition to electric vehicles and renewable energy infrastructure is driving unprecedented capacity expansion in SiC and GaN power device fabrication, where precise thermal process control directly determines device performance and yield. Similarly, the heterogeneous integration trend in advanced packaging , encompassing wafer-level fan-out, 2.5D interposers, and chiplet-based assemblies , introduces new thermal management challenges during bonding and molding processes that TC wafer measurement systems are uniquely suited to address. These emerging application segments collectively represent a material incremental opportunity for market participants to diversify revenue beyond established logic and memory fab customers.

TC Wafer Temperature Measurement Systems Market Trends

Rising Semiconductor Manufacturing Complexity Driving Demand for Precision Temperature Measurement

TC Wafer Temperature Measurement Systems Market is experiencing a notable shift driven by the increasing complexity of semiconductor manufacturing processes. As wafer fabrication technologies advance toward smaller nodes and more intricate device architectures, maintaining precise thermal control during production has become a critical operational requirement. TC Wafer Temperature Measurement Systems, which ensure temperature stability throughout the semiconductor manufacturing process, are increasingly positioned as indispensable tools for guaranteeing wafer quality and end-product performance. Manufacturers operating across PVD, CVD, RTP, and RTA processes are placing greater emphasis on real-time temperature monitoring to reduce defect rates and improve yield consistency.

Other Trends

Shift Toward Wireless TC Wafer Temperature Measurement Solutions

One of the most prominent trends reshaping TC Wafer Temperature Measurement Systems Market is the growing adoption of wireless measurement configurations. Wireless systems offer enhanced flexibility in fab environments where conventional wired setups may introduce installation constraints or risk signal interference. As semiconductor fabs modernize their equipment infrastructure, wireless TC wafer systems are gaining traction for their ability to integrate more seamlessly into automated production lines. This trend is particularly evident in advanced logic and memory chip manufacturing facilities in Asia and North America, where operational efficiency and data accuracy are paramount.

Expanding Application Scope Across Process Technologies

The application landscape for TC Wafer Temperature Measurement Systems is broadening beyond traditional thermal processing steps. While RTP and RTA applications have historically represented core use cases, growing utilization in CVD and PVD processes reflects a wider recognition of temperature management’s role in film deposition quality and uniformity. Semiconductor manufacturers across North America, Europe, and Asia , particularly in China, South Korea, Japan, and Southeast Asia , are investing in upgraded thermal measurement capabilities to support next-generation device production requirements.

Competitive Landscape and Regional Manufacturing Dynamics Influencing Market Trajectory

TC Wafer Temperature Measurement Systems Market is characterized by the presence of established global players such as KLA Corporation and THERMO ELECTRIC alongside specialized regional manufacturers including Shanghai GND Etech, Guangdong Ruile Semiconductor Technology, and Hefei Zhice Electronic. This competitive mix is intensifying innovation activity, particularly in sensor accuracy, system miniaturization, and compatibility with advanced process chambers. Asia, led by China and South Korea, continues to emerge as both a significant consumer and an expanding production hub for these systems. Meanwhile, North American and European markets remain driven by demand from leading-edge semiconductor fabs prioritizing high-precision thermal control across increasingly complex manufacturing workflows.

COMPETITIVE LANDSCAPE

Key Industry Players

TC Wafer Temperature Measurement Systems Market: Competitive Dynamics and Leading Manufacturers Shaping Global Semiconductor Metrology Ecosystem

Global TC Wafer Temperature Measurement Systems market is characterized by a moderately consolidated competitive landscape, with KLA Corporation standing out as the dominant force owing to its extensive semiconductor metrology portfolio, deep integration with leading chip manufacturers, and robust R&D capabilities. KLA’s established presence across North America, Europe, and Asia-Pacific gives it a significant first-mover advantage, particularly in high-precision applications such as RTP (Rapid Thermal Processing) and CVD (Chemical Vapor Deposition). The top five global players collectively commanded a substantial share of the market’s approximately US$ 76.98 million valuation in 2025, underscoring the concentration of technology expertise and manufacturing capacity among a select group of established firms. Competition in this market is primarily driven by product accuracy, thermal calibration reliability, wireless versus wired technology differentiation, and the ability to integrate seamlessly into existing semiconductor fabrication environments.

Beyond the market leader, several niche yet strategically significant players are actively shaping the competitive contours of the TC Wafer Temperature Measurement Systems space. Companies such as THERMO ELECTRIC and PFK Instrument have carved out specialized positions by delivering tailored thermocouple-based measurement solutions for specific process applications including PVD (Physical Vapor Deposition) and RTA (Rapid Thermal Annealing). Meanwhile, Asia-based manufacturers including Shanghai GND Etech, Guangdong Ruile Semiconductor Technology, and Hefei Zhice Electronic are rapidly gaining traction, leveraging cost-competitive manufacturing, proximity to semiconductor fabs in China and Southeast Asia, and growing domestic demand for advanced wafer process control tools. As the market is projected to reach US$ 125 million by 2034 at a CAGR of 7.4%, competitive intensity is expected to increase, with players investing in wireless TC wafer platforms and next-generation sensor technologies to differentiate their offerings and capture emerging growth opportunities across global semiconductor manufacturing hubs.

List of Key TC Wafer Temperature Measurement Systems Companies Profiled

- KLA Corporation

- THERMO ELECTRIC

- PFK Instrument

- Thermoway Industrial

- Rsuwei

- Shanghai GND Etech

- Guangdong Ruile Semiconductor Technology

- Hefei Zhice Electronic

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Wireless TC Wafer Temperature Measurement Systems represent the leading and fastest-growing product type in the market, driven by the increasing complexity of semiconductor fabrication environments that demand flexible, non-intrusive monitoring solutions.

|

| By Application |

|

CVD (Chemical Vapor Deposition) emerges as the dominant application segment for TC Wafer Temperature Measurement Systems, owing to the critical role that precise thermal management plays in ensuring uniform thin-film deposition across wafer surfaces.

|

| By End User |

|

Foundries constitute the leading end-user segment for TC Wafer Temperature Measurement Systems, as the rapid expansion of contract chip manufacturing to meet global semiconductor demand necessitates rigorous process control at every stage of wafer fabrication.

|

| By Wafer Size |

|

300mm Wafer Systems represent the leading segment by wafer size, reflecting the industry-wide migration toward larger wafer formats that deliver superior economies of scale and higher die output per fabrication run.

|

| By Thermocouple Configuration |

|

Multi-Point TC Wafer Systems lead this segment as semiconductor manufacturers increasingly prioritize comprehensive across-wafer temperature uniformity mapping to address the thermal non-uniformity challenges inherent in modern high-throughput process equipment.

|

Regional Analysis: TC Wafer Temperature Measurement Systems Market

Asia-Pacific continues to witness an unprecedented wave of semiconductor fabrication plant expansions, particularly in Taiwan, South Korea, and mainland China. These large-scale investments directly translate into heightened demand for TC wafer temperature measurement systems, as each new fab line requires precision thermal monitoring tools to ensure process consistency, yield optimization, and equipment qualification across diverse wafer processing stages.

National semiconductor strategies across Asia-Pacific , including China’s domestic chip programs, South Korea’s K-Semiconductor Belt initiative, and Japan’s semiconductor revitalization plans , are channeling significant public funding into advanced manufacturing infrastructure. This policy-driven momentum is accelerating the adoption of high-precision process control equipment, including TC wafer temperature measurement systems, across both established and emerging regional fab operators.

The progressive shift toward advanced and sub-advanced technology nodes in Asia-Pacific fabs demands increasingly stringent thermal uniformity and temperature measurement precision during wafer processing. TC wafer temperature measurement systems play a critical role in enabling the tight process windows required at these nodes, making them indispensable tools as regional manufacturers push the boundaries of miniaturization and device performance.

Asia-Pacific is witnessing a maturing local supplier ecosystem for semiconductor process control equipment, including TC wafer temperature measurement systems. Regional manufacturers in Japan, South Korea, and China are investing in enhancing measurement accuracy, system durability, and process integration capabilities. This growing domestic supply base is reducing dependence on imported solutions while driving competitive innovation in product performance and cost-effectiveness across the region.

North America

North America represents a highly significant market for TC wafer temperature measurement systems, anchored by its established base of leading semiconductor equipment manufacturers, world-class research institutions, and a robust domestic chip fabrication industry that continues to receive transformative investment under recent industrial policy initiatives. The United States, in particular, is experiencing a notable resurgence in semiconductor manufacturing capacity, with multiple large-scale fab projects underway that are expected to substantially increase demand for precision process control tools, including TC wafer temperature measurement systems. The region also benefits from a deeply innovative technology development ecosystem, where close partnerships between equipment suppliers, semiconductor producers, and academic research centers accelerate the development of next-generation thermal measurement solutions. Canada contributes additional research and manufacturing capacity, further supporting the regional market’s breadth and resilience throughout the forecast period.

Europe

Europe occupies a strategically important position in Global TC wafer temperature measurement systems market, supported by a well-developed semiconductor equipment manufacturing base, particularly in Germany, the Netherlands, and France. The European Chips Act and related national semiconductor investment programs are catalyzing significant expansion of regional wafer fabrication capacity, which in turn is driving demand for high-precision thermal measurement tools across both legacy and advanced technology nodes. European semiconductor equipment manufacturers are widely recognized for their engineering precision and innovation, contributing meaningfully to Global advancement of TC wafer temperature measurement technology. The region’s emphasis on process reliability, environmental compliance, and energy-efficient manufacturing also shapes the functional requirements placed on temperature measurement systems deployed within European fab environments, distinguishing regional procurement priorities from other global markets.

South America

South America represents an emerging and gradually developing market for TC wafer temperature measurement systems, currently constrained by a relatively limited semiconductor manufacturing base compared to other global regions. Brazil leads regional activity, with nascent efforts to build domestic electronics manufacturing and semiconductor design capabilities that may, over time, generate incremental demand for precision process control equipment. While large-scale wafer fabrication investment remains limited across the region, growing interest in electronics production, automotive electronics, and industrial automation is laying the groundwork for longer-term market development. As regional economies prioritize technological diversification and digital infrastructure expansion, South America is expected to represent a modest but progressively relevant contributor to Global TC wafer temperature measurement systems market by the latter part of the forecast period.

Middle East & Africa

The Middle East and Africa region is at an early stage of development within TC Wafer Temperature Measurement Systems Market, with current demand primarily driven by technology adoption in research institutions, specialized electronics manufacturing facilities, and emerging industrial sectors. The Middle East, particularly through initiatives in the United Arab Emirates and Saudi Arabia, is investing in advanced technology infrastructure as part of broader economic diversification strategies, which includes exploratory engagement with semiconductor and electronics manufacturing capabilities. While large-scale fab operations remain absent from the region, the growing focus on digital transformation, smart manufacturing, and technology-driven economic development creates a foundational environment for future market participation. Over the 2026–2034 forecast period, the Middle East and Africa are expected to represent a nascent but increasingly watched frontier for TC wafer temperature measurement systems market stakeholders seeking long-term geographic diversification.

Report Scope

This market research report provides a comprehensive analysis of TC Wafer Temperature Measurement Systems Market, covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of TC Wafer Temperature Measurement Systems Market?

-> Global TC Wafer Temperature Measurement Systems Market was valued at USD 76.98 million in 2025 and is expected to reach USD 125 million by 2034, growing at a CAGR of 7.4% during the forecast period.

Which key companies operate in TC Wafer Temperature Measurement Systems Market?

-> Key players include KLA Corporation, THERMO ELECTRIC, PFK Instrument, Thermoway Industrial, Rsuwei, Shanghai GND Etech, Guangdong Ruile Semiconductor Technology, and Hefei Zhice Electronic, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for semiconductor manufacturing precision, increasing adoption of advanced wafer fabrication processes such as PVD, CVD, RTP, and RTA, and the need for stringent temperature stability to ensure wafer quality and product performance.

Which region dominates the market?

-> Asia is a dominant and fastest-growing region, driven by strong semiconductor manufacturing activity in China, Japan, South Korea, and Southeast Asia, while North America, particularly the U.S., remains a significant market contributor.

What are the emerging trends?

-> Emerging trends include wireless TC wafer temperature measurement systems, integration of IoT-enabled monitoring, miniaturization of sensor technologies, and increasing adoption of real-time temperature control solutions to meet the evolving demands of advanced semiconductor fabrication processes.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...