MARKET INSIGHTS

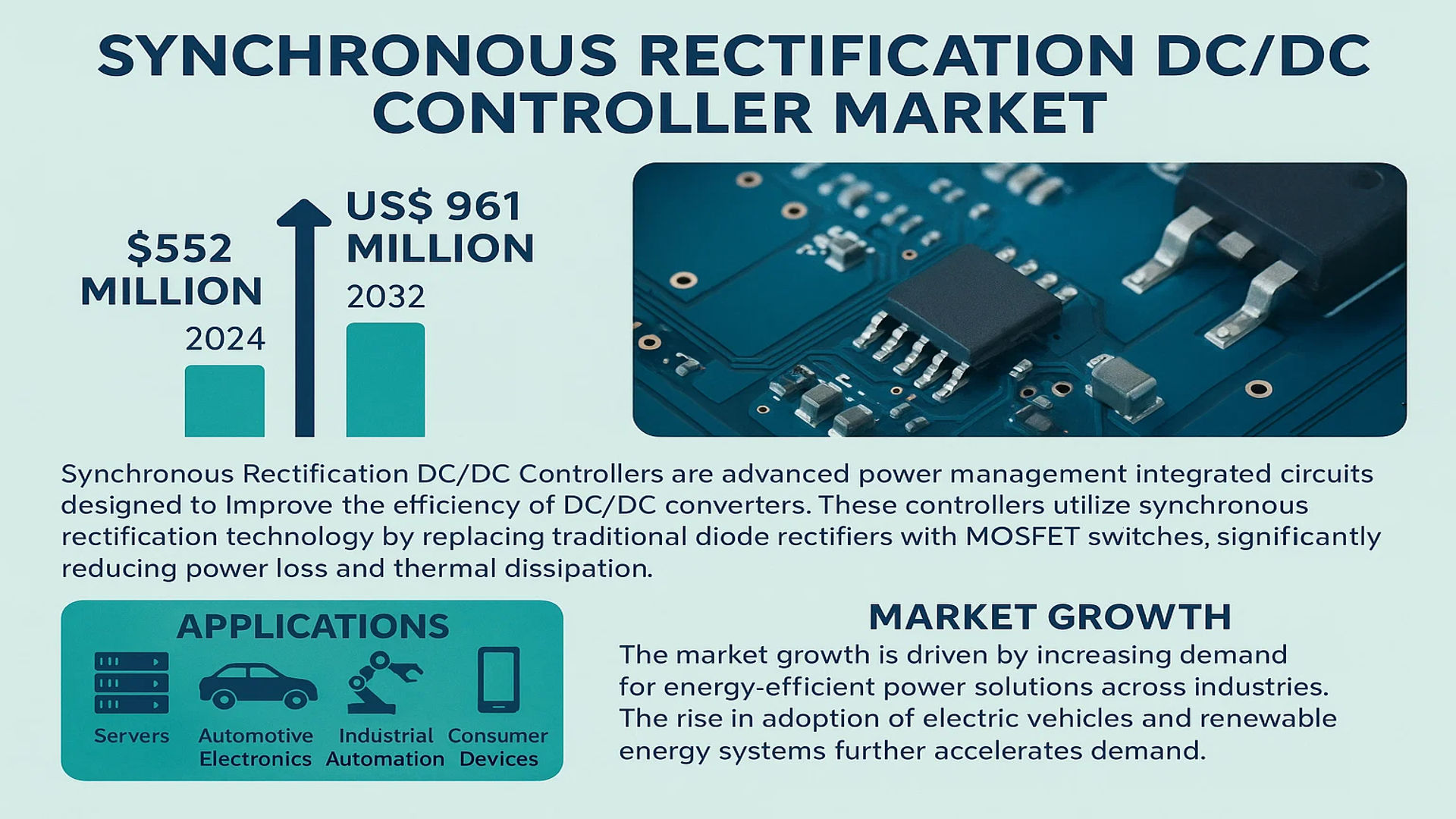

The global Synchronous Rectification DC/DC Controller Market was valued at 552 million in 2024 and is projected to reach US$ 961 million by 2032, at a CAGR of 9.0% during the forecast period.

Synchronous Rectification DC/DC Controllers are advanced power management integrated circuits designed to improve the efficiency of DC/DC converters. These controllers utilize synchronous rectification technology by replacing traditional diode rectifiers with MOSFET switches, significantly reducing power loss and thermal dissipation. The technology finds extensive applications in servers, automotive electronics, industrial automation, and consumer devices where high energy efficiency and compact power solutions are critical.

The market growth is driven by increasing demand for energy-efficient power solutions across industries. The rise in adoption of electric vehicles and renewable energy systems further accelerates demand. Key players like Texas Instruments, Infineon, and STMicroelectronics dominate the market, collectively holding over 45% revenue share as of 2024. Recent technological advancements include the development of controllers supporting wide input voltage ranges (below 10V to above 30V) to cater to diverse application needs.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Energy-Efficient Power Solutions in Electronics to Fuel Market Growth

The global push toward energy-efficient electronic devices is driving significant demand for synchronous rectification DC/DC controllers. With consumer electronics, industrial equipment, and electric vehicles increasingly requiring higher power conversion efficiency, these controllers have become critical components. Recent efficiency standards mandate power supplies to achieve over 90% conversion rates, positioning synchronous rectification as the preferred technology due to its ability to minimize switching losses. In 2024, the market for DC/DC converters in consumer electronics alone is projected to exceed $15 billion globally, with synchronous rectification solutions capturing a dominant share.

Expansion of 5G Infrastructure and Data Centers Creates Strong Demand

Massive investments in 5G networks and hyperscale data centers are creating unprecedented demand for high-efficiency power management solutions. Synchronous rectification DC/DC controllers are particularly favored for telecom infrastructure due to their ability to handle high current densities while minimizing thermal dissipation. The global 5G infrastructure market is expected to grow at 35% CAGR through 2030, with each base station requiring multiple DC/DC power conversion stages. Similarly, data center operators increasingly specify synchronous rectification solutions to meet stringent power usage effectiveness (PUE) targets below 1.3.

➤ The average hyperscale data center now contains over 10,000 DC/DC converter modules, creating significant demand for high-efficiency synchronous rectification controllers.

Automotive Electrification Trend Accelerates Adoption

The rapid transition to electric vehicles is creating new high-volume applications for synchronous rectification technology. Modern EV power architectures require multiple DC/DC conversion stages for battery management, onboard charging, and auxiliary systems. With automotive OEMs demanding converter efficiencies above 95% to maximize driving range, synchronous rectification has become the industry standard. The automotive DC/DC converter market is projected to reach $12 billion by 2028, with synchronous controllers capturing over 60% of this market.

MARKET CHALLENGES

Complex Design and Validation Processes Increase Time-to-Market

While synchronous rectification offers clear efficiency benefits, the technology presents significant design challenges. Implementing optimal control algorithms for synchronous MOSFET switching requires specialized expertise in power electronics. Each new design typically requires extensive validation testing under various load conditions to ensure stability and prevent catastrophic failures. The average development cycle for a new synchronous rectification controller design now exceeds 18 months, creating barriers for smaller players in the market.

Thermal Management Requirements in High-Density Applications

The industry’s push toward higher power densities creates thermal challenges for synchronous rectification implementations. While these controllers significantly reduce conduction losses compared to diode-based solutions, the remaining thermal load in compact form factors requires careful management. Many applications now demand junction temperatures below 125°C to ensure reliability, necessitating advanced packaging solutions that can add 20-30% to component costs.

MARKET RESTRAINTS

Component Supply Chain Volatility Impacts Production Stability

The synchronous rectification DC/DC controller market remains vulnerable to semiconductor supply chain disruptions. These devices require specialized high-voltage MOSFETs and precision analog components that have experienced allocation periods exceeding 52 weeks during recent chip shortages. Lead times for certain power management ICs have increased by 300% compared to pre-pandemic levels, forcing OEMs to maintain excessive inventory buffers that strain working capital.

Price Sensitivity in Consumer Applications Limits Premium Features Adoption

While industrial and automotive segments readily adopt advanced synchronous rectification solutions, consumer electronics manufacturers remain highly price-sensitive. In cost-driven markets like smartphone chargers and LCD TV power supplies, manufacturers often opt for simpler diode-based designs despite their lower efficiency. This creates a bifurcated market where premium features like digital programmability and adaptive dead-time control only penetrate about 30% of the total available market.

MARKET OPPORTUNITIES

Emerging GaN and SiC Power Device Integration Opens New Design Possibilities

The advent of wide-bandgap semiconductor technologies presents significant opportunities for synchronous rectification controller vendors. Gallium nitride (GaN) and silicon carbide (SiC) power devices enable switching frequencies above 1MHz with minimal losses, creating demand for specialized controller ICs. The GaN power device market is projected to grow at 56% CAGR through 2030, with synchronous rectification controllers representing a key enabling technology. Leading vendors are already introducing controllers specifically optimized for these next-generation power switches.

Industrial IoT Adoption Drives Demand for Smart Power Management

The proliferation of industrial IoT devices is creating demand for intelligent synchronous rectification solutions with digital monitoring capabilities. Modern industrial automation systems require power converters that can communicate operational parameters and health status via industrial protocols. This has led to the development of PMBus-compliant synchronous controllers that can report efficiency metrics, temperature data, and fault conditions. The market for digitally-controlled power converters in industrial applications is expected to triple by 2028.

SYNCHRONOUS RECTIFICATION DC/DC CONTROLLER MARKET TRENDS

Growth in High-Efficiency Power Solutions Drives Market Expansion

The synchronous rectification DC/DC controller market has witnessed significant growth due to the rising demand for high-efficiency power conversion solutions across industries. As energy efficiency regulations tighten globally, the adoption of these controllers in applications such as servers, telecom infrastructure, and automotive electronics has surged. The shift toward GaN (Gallium Nitride) and SiC (Silicon Carbide) semiconductors has further fueled market growth, with these materials enabling higher switching frequencies and better thermal management. Additionally, the global push for renewable energy integration has amplified the need for efficient power management systems, particularly in solar inverters and energy storage solutions.

Other Trends

Integration in Electric Vehicles (EVs) and Hybrid Systems

The automotive industry’s rapid transition to electric and hybrid vehicles has positioned synchronous rectification DC/DC controllers as a critical component in on-board chargers (OBCs) and battery management systems (BMS). The push for lightweight, compact, and highly efficient power circuits in EVs aligns perfectly with the advantages of these controllers, which minimize energy loss and heat dissipation. Furthermore, advancements in 800V battery architectures have accelerated demand for controllers that can handle higher voltage ranges while maintaining efficiency, a key factor expected to sustain long-term market growth.

Rise of Data Centers and 5G Infrastructure

The exponential growth of cloud computing and 5G networks has necessitated the deployment of advanced power management solutions in data centers and telecommunications infrastructure. Synchronous rectification DC/DC controllers play a vital role in reducing power losses in server power supplies, contributing to lower operational costs and improved energy efficiency. With data centers consuming nearly 1-2% of global electricity, the adoption of these controllers is a crucial step toward achieving sustainability targets. Moreover, the rollout of 5G small-cell networks demands compact and efficient power modules, further driving the need for high-performance DC/DC conversion solutions.

Demand for Miniaturization and High-Density Power Designs

Manufacturers are increasingly focused on developing synchronous rectification DC/DC controllers with smaller footprints while maintaining high power density, responding to the demand for miniaturized electronic devices. The proliferation of IoT devices, wearables, and portable medical equipment has led to the integration of these controllers in space-constrained applications. Innovations in packaging technologies, such as wafer-level packaging (WLP) and chip-scale modules, have enabled manufacturers to deliver compact yet efficient solutions, reinforcing the market’s upward trajectory.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Semiconductor Giants and Emerging Brands Compete for Market Share in High-Efficiency Power Conversion Solutions

The global synchronous rectification DC/DC controller market features a dynamic competitive environment where established semiconductor manufacturers compete with specialized power IC developers. Texas Instruments and Infineon Technologies currently dominate the landscape, collectively accounting for over 30% of the 2024 market share due to their comprehensive product portfolios and strong distribution networks across North America and Europe.

STMicroelectronics and ON Semiconductor maintain significant positions in the market through continuous innovation in energy-efficient solutions. These companies have recently launched new controller families optimized for automotive and industrial applications, responding to growing demand for higher power density and thermal performance.

Asian manufacturers including Renesas Electronics and ROHM Semiconductor are gaining traction through cost-competitive solutions tailored for consumer electronics. Their ability to deliver highly integrated controllers at competitive price points has enabled strong penetration in the APAC region, particularly in China’s booming electronics manufacturing sector.

Meanwhile, specialized players like Richtek Technology and Hangzhou Silan Microelectronics are carving out niche positions through application-specific designs. These companies focus on delivering customized solutions for fast-charging applications and server power supplies, leveraging their technical expertise in high-frequency switching topologies.

List of Key Synchronous Rectification DC/DC Controller Manufacturers

- Texas Instruments (U.S.)

- Infineon Technologies (Germany)

- STMicroelectronics (Switzerland)

- ON Semiconductor (U.S.)

- Renesas Electronics (Japan)

- ROHM Semiconductor (Japan)

- NXP Semiconductors (Netherlands)

- Diodes Incorporated (U.S.)

- Richtek Technology (Taiwan)

- Hangzhou Silan Microelectronics (China)

Segment Analysis:

By Type

Minimum Voltage: Below 10 V Segment Leads Due to High Adoption in Low-Power Applications

The market is segmented based on type into:

- Minimum Voltage: Below 10 V

- Subtypes: Buck Converters, Boost Converters, Buck-Boost Converters

- Minimum Voltage: Above or Equal to 10 V

- Subtypes: Step-Down Converters, Step-Up Converters, Isolated Converters

By Application

Consumer Electronics Charger Segment Dominates Owing to Rising Demand for Portable Devices

The market is segmented based on application into:

- Car Charger

- Consumer Electronics Charger

- Industrial Power Supply

- Other

By End User

Electronics Manufacturing Sector Accounts for Significant Market Share

The market is segmented based on end user into:

- Electronics Manufacturers

- Automotive Industry

- Telecommunications Providers

- Industrial Equipment Manufacturers

Regional Analysis: Synchronous Rectification DC/DC Controller Market

Asia-Pacific

The Asia-Pacific region dominates the global synchronous rectification DC/DC controller market, accounting for the largest revenue share in 2024. This leadership position stems from China’s robust semiconductor manufacturing ecosystem and Japan’s and South Korea’s technological advancements in power electronics. The region benefits from strong demand across consumer electronics, automotive electrification, and 5G infrastructure deployment. China’s 14th Five-Year Plan emphasizes semiconductor self-sufficiency, driving local production of power management ICs. However, recent global chip shortages have exposed supply chain vulnerabilities, prompting both regional players and multinationals to diversify manufacturing bases across Southeast Asia. The Minimum Voltage: Below 10V segment sees particularly high adoption in portable devices, while industrial applications favor higher voltage controllers. Key challenges include price competition and the need for continuous innovation to meet evolving efficiency standards.

North America

North America represents the second-largest market, characterized by high-value applications in data centers, electric vehicles, and aerospace systems. The U.S. market benefits from strong R&D investments by industry leaders like Texas Instruments and Onsemi, particularly in gallium nitride (GaN) and silicon carbide (SiC) compatible controllers. Recent initiatives like the CHIPS and Science Act aim to strengthen domestic semiconductor production, which could reshape supply chains for power management ICs. Automotive applications are gaining momentum with the transition to 48V architectures in EVs. However, the market faces pressure from geopolitical trade tensions and the need to balance performance enhancements with cost constraints in consumer applications.

Europe

Europe maintains a strong position in the synchronous rectification DC/DC controller market, driven by stringent energy efficiency regulations and leadership in industrial automation. German and French manufacturers prioritize high-reliability solutions for automotive and industrial applications, with Infineon and STMicroelectronics playing pivotal roles. The EU’s Green Deal initiatives accelerate demand for energy-efficient power conversion solutions across sectors. A notable trend is the integration of digital control features for smart power management in Industry 4.0 applications. Challenges include navigating complex compliance requirements and competition from Asian suppliers in cost-sensitive market segments.

South America

The South American market shows moderate growth, primarily servicing consumer electronics and renewable energy applications. Brazil leads regional demand, though economic volatility constrains market expansion. Local assembly of electronic products creates opportunities for DC/DC controller adoption, particularly in battery-powered devices and solar power systems. However, the market remains price-sensitive, favoring basic controller designs over premium solutions. Infrastructure limitations and fluctuating import policies create supply chain uncertainties, prompting some manufacturers to establish local partnerships for better market access.

Middle East & Africa

This emerging market demonstrates potential in telecommunications infrastructure and oil/gas applications, though adoption remains limited by underdeveloped electronics manufacturing. The UAE and Saudi Arabia show the strongest growth, driven by smart city initiatives and diversification from oil economies. 5G deployments and renewable energy projects create demand for efficient power conversion solutions. However, the market relies heavily on imports, with limited local technical expertise for advanced controller implementations. Long-term growth depends on infrastructure development and stabilization of regional supply chains.

Report Scope

This market research report provides a comprehensive analysis of the Global Synchronous Rectification DC/DC Controller market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type (Minimum Voltage: Below 10 V and Above or Equal to 10 V), application (Car Charger, Consumer Electronics Charger, Industrial Power Supply, Others), and end-user industries.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis.

- Competitive Landscape: Profiles of leading market participants, including their product portfolios, R&D investments, manufacturing capabilities, and strategic initiatives such as mergers and acquisitions.

- Technology Trends & Innovation: Assessment of advancements in synchronous rectification technology, integration with AI/IoT, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving growth, such as increasing demand for energy-efficient power solutions, alongside challenges like supply chain disruptions and regulatory complexities.

- Stakeholder Analysis: Strategic insights for semiconductor manufacturers, OEMs, system integrators, and investors to capitalize on emerging opportunities.

The report employs a robust research methodology, combining primary interviews with industry experts and validated secondary data sources to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Synchronous Rectification DC/DC Controller Market?

-> Synchronous Rectification DC/DC Controller Market was valued at 552 million in 2024 and is projected to reach US$ 961 million by 2032, at a CAGR of 9.0% during the forecast period..

Which key companies operate in Global Synchronous Rectification DC/DC Controller Market?

-> Key players include STMicroelectronics, Renesas, Infineon, Texas Instruments, NXP, Onsemi, ROHM, Diodes, ABLIC, and Nexperia, among others.

What are the key growth drivers?

-> Growth is driven by rising demand for energy-efficient power solutions, expansion of 5G infrastructure, and increasing adoption in automotive and industrial applications.

Which region dominates the market?

-> Asia-Pacific leads the market due to strong manufacturing hubs in China and Japan, while North America remains a key innovator in semiconductor technologies.

What are the emerging trends?

-> Emerging trends include integration of GaN/SiC technologies, miniaturization of power modules, and AI-driven power management solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...