MARKET INSIGHTS

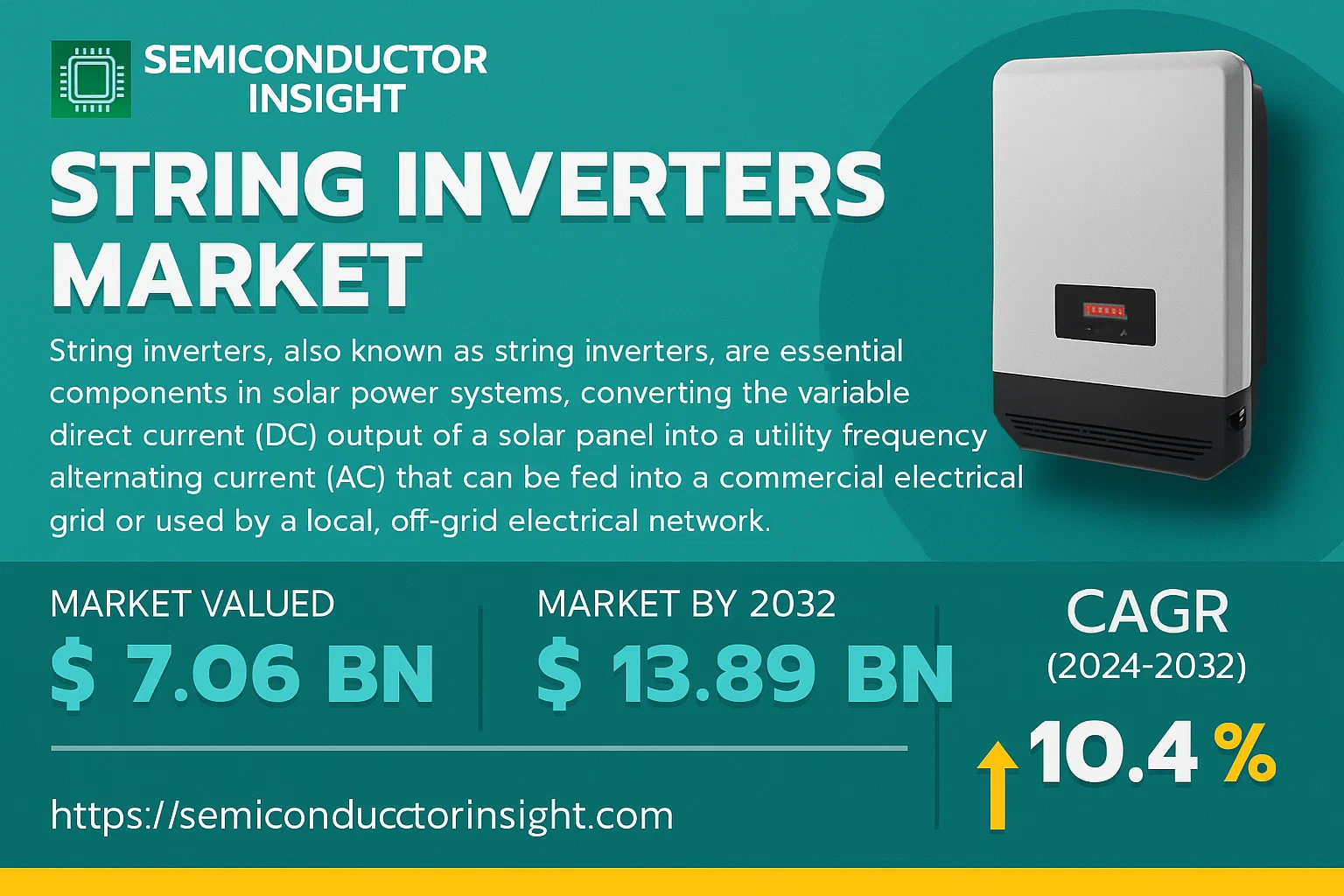

Global String Inverters Market was valued at USD 7.06 billion in 2024 and is projected to reach USD 13.89 billion by 2032, exhibiting a CAGR of 10.4% during the forecast period.

String inverters, also known as string inverters, are essential components in solar power systems, converting the variable direct current (DC) output of a solar panel into a utility frequency alternating current (AC) that can be fed into a commercial electrical grid or used by a local, off-grid electrical network. The market is experiencing robust growth due to several factors, including the global push towards renewable energy adoption, supportive government policies and incentives, and declining costs of solar photovoltaic (PV) modules. The increasing demand for energy efficiency and the growing installation of solar power plants, particularly in the residential and commercial sectors, are also significant contributors. Additionally, technological advancements in inverter technology, such as the integration of smart grid capabilities and the rise of hybrid inverters, are creating new opportunities.

MARKET DRIVERS

Accelerating Global Expansion of Utility-Scale Solar

The string inverter market is primarily driven by the robust growth in utility-scale solar installations worldwide. Government mandates for renewable energy and declining costs of photovoltaic modules are fueling project pipelines. String inverters offer a cost-effective and scalable solution for large-scale solar farms, making them the preferred choice for many developers. Their modularity allows for easier maintenance and potential upgrades compared to central inverter systems.

Rising Demand in the Commercial & Industrial (C&I) Segment

The commercial and industrial sector represents a significant growth area. Businesses are increasingly investing in on-site solar to reduce electricity costs and meet sustainability goals. String inverters are well-suited for the varied roof spaces and energy demands of C&I facilities. Their design efficiently manages different string configurations and shading scenarios, which is common in such installations.

➤ Technological Advancements Enhancing Performance

Continuous innovation is a key driver. Modern string inverters now incorporate advanced features like built-in monitoring, higher efficiency ratings exceeding 99%, and improved grid-support functions. The integration of technologies such as arc-fault circuit interruption and rapid shutdown capabilities enhances safety and compliance with stringent regulations, boosting their adoption.

MARKET CHALLENGES

Intense Competition from Alternative Technologies

The string inverter market faces significant competition from microinverters and DC-optimizer systems, particularly in the residential segment. These alternatives offer advantages in scenarios with shading or complex roof designs by performing Maximum Power Point Tracking (MPPT) at the individual panel level. This competition pressures string inverter manufacturers to continuously innovate and justify their value proposition.

Other Challenges

Supply Chain Constraints and Price Volatility

The industry is susceptible to disruptions in the global supply chain for critical electronic components, such as semiconductors and magnetics. These constraints can lead to production delays and increased costs, which may be passed on to end-users and potentially slow down market growth.

Grid Integration and Compliance Hurdles

As solar penetration increases, grid interconnection requirements become more complex. String inverters must comply with evolving grid codes concerning voltage regulation, frequency response, and anti-islanding. Ensuring compatibility and certification across different regions requires significant R&D investment from manufacturers.

MARKET RESTRAINTS

Price Erosion and High Competitive Pressure

A major restraint for the string inverter market is the persistent price pressure due to intense competition among a large number of global and regional manufacturers. This environment leads to thin profit margins, which can limit investment in research and development. The market is highly sensitive to pricing, and cost leadership becomes a critical factor for survival and growth.

Technical Limitations in Complex Installations

While versatile, string inverters can be less efficient than microinverters in installations where shading or panel orientation is not uniform. The performance of an entire string is limited by its weakest-performing panel. This inherent technical characteristic can restrain their adoption in the residential market, where rooftop conditions are often suboptimal.

MARKET OPPORTUNITIES

Expansion into Emerging Economies

Significant growth opportunities exist in emerging markets across Asia-Pacific, Latin America, and Africa. Rapid urbanization, growing energy demand, and supportive government policies are driving solar adoption. String inverters, with their proven reliability and cost-effectiveness, are well-positioned to capture a large share of these new markets, particularly for utility and C&I projects.

Integration with Energy Storage Systems (ESS)

The rising demand for solar-plus-storage systems presents a major opportunity. The development of hybrid inverters and AC-coupled solutions that seamlessly integrate string inverters with batteries is a key growth area. This allows consumers and businesses to maximize self-consumption of solar energy, provide backup power, and participate in energy management services.

Advancements in Digitalization and Smart Features

There is a growing opportunity to leverage data analytics and the Internet of Things (IoT). Smart string inverters with advanced monitoring and predictive maintenance capabilities can provide valuable insights into system performance. This can lead to new service-based revenue models for manufacturers and installers, such as performance guarantees and operational maintenance contracts.

String Inverters Market Trends

Robust Market Expansion Fueled by Global Renewable Energy Push

The global String Inverters market is experiencing a significant growth trajectory, driven by the worldwide acceleration of solar photovoltaic (PV) installations. The market, valued at $7,061 million in 2024, is projected to surge to $13,890 million by 2032, representing a steady Compound Annual Growth Rate (CAGR) of 10.4% during the forecast period. This robust expansion is primarily attributed to supportive government policies for renewable energy, declining costs of solar panels, and increasing electricity demand, particularly in the residential sector. The technological maturity, reliability, and cost-effectiveness of string inverters compared to other inverter types continue to make them the preferred choice for a wide range of solar applications.

Other Trends

Dominance of the Asia-Pacific Region

Geographically, the market is dominated by the Asia-Pacific region, with China alone accounting for a substantial 69% share of the global market. This dominance is supported by massive domestic solar deployment targets, a strong manufacturing base, and competitive pricing. Europe and North America follow as the next largest regional markets, with growth driven by ambitious decarbonization goals and incentives for residential and commercial solar power generation. Emerging economies in Southeast Asia, South America, and the Middle East are also expected to present significant growth opportunities in the coming years.

Consolidation Among Leading Manufacturers

The competitive landscape is characterized by a high level of concentration, with the top five players—HUAWEI, Sungrow, SMA, GOODWE, and FIMER—collectively holding approximately 62% of the market share. This concentration drives intense competition focused on technological innovation, product efficiency, reliability, and global service networks. Key competitive strategies include the development of smart inverters with advanced grid-support functions, expansion into new geographical markets, and strategic partnerships to enhance product portfolios and market reach.

Segmentation Highlights and Future Outlook

In terms of product segmentation, 30-40KW string inverters constitute the largest segment, capturing over 27% of the market share, favored for their versatility in commercial and small utility-scale applications. On the application front, the Household Use segment is the largest, accounting for over 44% of the market, underscoring the critical role of residential solar in the global energy transition. Looking ahead, the market faces trends such as the integration of energy storage systems with hybrid inverters, the rise of digitalization and IoT for remote monitoring, and the need for products that ensure grid stability. However, challenges including supply chain volatility, price pressure, and evolving grid codes will require continuous adaptation from industry participants.

COMPETITIVE LANDSCAPE

Key Industry Players

String Inverter Market Dominated by Global Giants with Strong Regional Concentration

The global string inverter market is characterized by a high degree of concentration, with the top five players accounting for approximately 62% of the market share. HUAWEI leads the market, leveraging its strong brand recognition, extensive R&D capabilities, and a comprehensive product portfolio that caters to residential, commercial, and utility-scale applications. The Chinese market is the largest globally, holding about 69% of the market share, which provides a significant home-field advantage for domestic leaders like HUAWEI, Sungrow, and SINENG. This concentration is driven by economies of scale, technological innovation, and strong supply chain integration, creating significant barriers to entry for new competitors. Market leaders compete intensely on technological features such as efficiency, reliability, smart grid compatibility, and after-sales service.

Beyond the dominant players, the market includes a range of significant niche and regional competitors that have carved out specific segments. European companies like SMA (Germany) and Fronius (Austria) hold strong positions, particularly in the premium residential and commercial markets, where brand reputation for quality and advanced technology commands customer loyalty. Similarly, companies such as GOODWE and GROWATT have gained substantial traction in the global residential sector. Other players like KSTAR, TBEA, and KACO focus on specific power ranges or regional markets, offering specialized solutions for industrial applications or emerging markets. The competitive dynamics are further influenced by ongoing technological shifts, including the integration of storage and smart energy management features, which all players are actively developing to maintain relevance.

List of Key String Inverters Companies Profiled

- HUAWEI

- Sungrow Power Supply Co., Ltd

- SMA

- GOODWE

- SINENG

- ATEC GROUP

- KSTAR

- CPS

- GROWATT

- TBEA

- FIMER

- Fronius

- KELONG

- SAJ

- KACO

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

30-40KW String Inverters are the leading segment, favored for their ideal balance between power output and versatility, making them suitable for a wide range of commercial and larger residential installations. Their dominance is driven by the sweet spot they occupy in terms of efficiency, cost-effectiveness, and ease of integration with standard solar panel configurations. Smaller units are primarily for residential use, while larger capacities cater to utility-scale projects with demanding power requirements. |

| By Application |

|

Household Use is the leading application segment, propelled by the global push for residential solar adoption, government incentives for homeowners, and rising electricity costs. This segment’s growth is further accelerated by the increasing availability of financing options and consumer awareness of renewable energy benefits. The Industrial and Commercial segment is also significant, driven by corporate sustainability goals and the economic advantages of on-site power generation for businesses. |

| By End User |

|

Residential Consumers constitute the leading end-user segment, driven by individual homeowners seeking energy independence and reduced utility bills. The demand from this group is characterized by a preference for reliable, user-friendly inverters with strong warranty support. Commercial & Industrial Entities represent a highly valuable market, demanding robust and scalable solutions to meet their larger energy loads and operational reliability requirements, often involving sophisticated energy management features. |

| By Grid Connectivity |

|

On-Grid Systems are the predominant choice, as most solar installations are designed to feed excess power back into the utility grid, offering financial returns through net metering. The robust infrastructure and favorable policies in many regions strongly favor on-grid connectivity. However, Hybrid Systems are gaining significant traction, as they offer the security of battery backup during grid outages while still maintaining the economic benefits of grid connection, appealing to both residential and commercial users seeking energy resilience. |

| By Technology Focus |

|

Standard String Inverters remain the volume leader due to their proven reliability and cost-efficiency for unshaded, uniform rooftop installations. Nevertheless, MLPE-Optimized Inverters, designed to work with module-level power electronics, are seeing rapid adoption in residential markets where shading or complex roof designs are common, as they maximize energy harvest. The market is also evolving towards Smart Inverters that offer advanced grid-support functions, which are becoming increasingly important for maintaining grid stability as solar penetration grows. |

Regional Analysis: String Inverters Market

The market is characterized by high maturity in countries like China and Australia, where favorable government subsidies, renewable purchase obligations, and streamlined grid-connection processes have been in place for years. These policies create a stable, long-term environment that encourages investment in solar projects utilizing string inverters. In emerging markets such as Vietnam and Thailand, new incentive schemes are rapidly accelerating adoption.

Asia-Pacific is the global hub for string inverter manufacturing, with China hosting several of the world’s largest producers. This concentration leads to significant economies of scale, reducing production costs and fostering intense competition. A deeply integrated local supply chain for electronic components ensures fast production times and resilience against global disruptions, solidifying the region’s cost leadership.

Manufacturers in the region are at the forefront of developing advanced features for string inverters, including higher efficiency ratings, enhanced grid-support functions, and integrated smart monitoring capabilities. A vast range of products is available to suit diverse applications, from low-cost options for utility-scale projects to premium, feature-rich models for the commercial and residential segments demanding high reliability.

The string inverter market caters to a wide spectrum of applications, from massive desert solar plants to complex commercial rooftops and dense urban residential installations. This diversity has driven the development of inverters specifically engineered to perform reliably in the region’s varied and often harsh climates, including high temperatures, humidity, and coastal conditions, ensuring longevity and consistent energy harvest.

North America

The North American string inverter market is distinguished by a strong focus on technological sophistication, reliability, and strict compliance with grid codes. The United States represents the largest market, driven by the Investment Tax Credit (ITC) and a growing number of state-level renewable portfolio standards. The market demand is bifurcated between large-scale utility projects, which favor high-power string inverters for their balance of cost and performance, and a robust residential sector that values advanced monitoring and safety features. Canada’s market, while smaller, is growing steadily, supported by federal carbon pricing policies and provincial incentives. A key dynamic is the high consumer and installer expectation for product quality, long warranties, and robust customer support, influencing the competitive landscape towards established, reputable brands.

Europe

Europe presents a mature and highly competitive market for string inverters, characterized by a strong push for energy self-sufficiency and decarbonization. Germany, Spain, the Netherlands, and Italy are key markets, with growth fueled by the EU’s Green Deal and national subsidies for residential and commercial solar installations. The region exhibits a strong preference for high-efficiency, durable inverters with advanced grid-management capabilities to support the dense and complex European power grid. The market is also seeing a significant trend towards hybridization, with growing demand for string inverters compatible with battery storage systems. Competition is intense among European, Chinese, and other international manufacturers, focusing on innovation, reliability, and compliance with stringent regional safety and grid standards.

South America

The South American string inverter market is an emerging arena with significant growth potential, primarily driven by Brazil and Chile. Brazil’s market is expanding rapidly due to a burgeoning distributed generation segment, supported by net metering regulations and rising electricity costs, which makes solar investments highly attractive for residential and commercial users. Chile’s market is propelled by its abundant solar resources and a strong focus on large-scale mining operations and utility projects seeking cost-effective energy solutions. While the market is price-sensitive, there is a growing appreciation for quality and reliability. The primary challenges include economic volatility and underdeveloped grid infrastructure in some areas, which influences the requirements for string inverters with robust grid-support functions.

Middle East & Africa

The Middle East and Africa region is experiencing rapid growth in the string inverters market, largely driven by massive utility-scale solar tenders in the Gulf Cooperation Council (GCC) countries, particularly Saudi Arabia and the UAE. These projects demand highly reliable, high-capacity string inverters capable of operating efficiently in extreme desert conditions. In contrast, Sub-Saharan Africa’s market is developing, focused more on smaller commercial and industrial applications and mini-grids, where the simplicity and cost-effectiveness of string inverters are key advantages. A major dynamic across the region is the need for products that can withstand harsh environmental conditions, including high temperatures, dust, and sandstorms. The market is also characterized by a mix of international suppliers and a growing presence of cost-competitive Chinese manufacturers.

Report Scope

This market research report provides a comprehensive analysis of the String Inverters Market , covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of String Inverters Market?

-> Global String Inverters Market was valued at USD 7061 million in 2024 and is projected to reach USD 13890 million by 2032, exhibiting a CAGR of 10.4% during the forecast period.

Which key companies operate in String Inverters Market?

-> Key players include HUAWEI, Sungrow Power Supply Co., Ltd, SMA, GOODWE, FIMER, and SINENG, among others. The top five players hold a combined market share of approximately 62%.

What are the key growth drivers?

-> Key growth drivers include increasing adoption of solar energy, government incentives for renewable power, and advancements in inverter technology.

Which region dominates the market?

-> China is the largest market, with a share of about 69%, followed by Europe and North America.

What are the emerging trends?

-> Emerging trends include the dominance of the 30-40KW product segment and the growing application in Household Use, which holds over 44% market share.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...