MARKET INSIGHTS

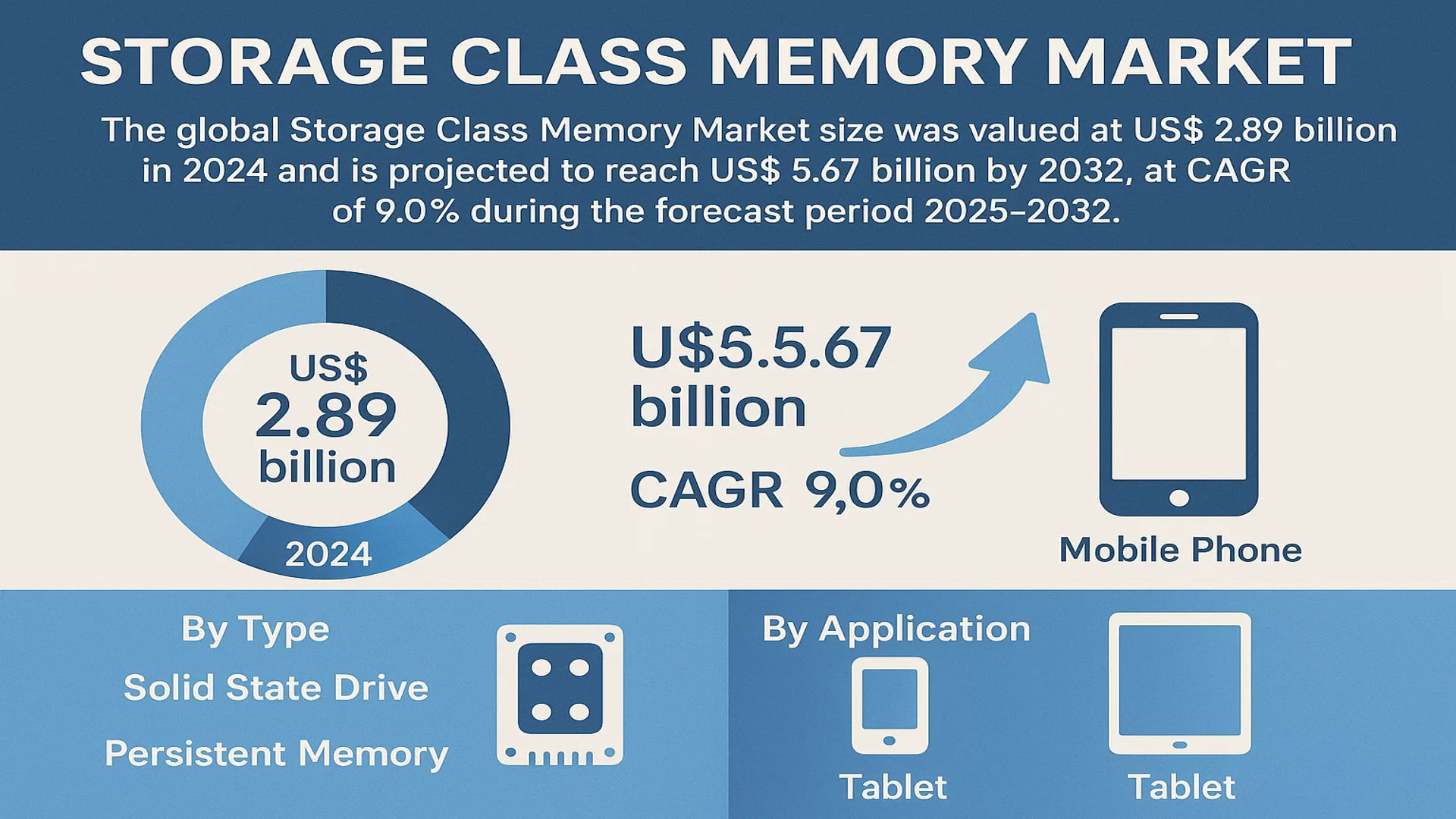

The global Storage Class Memory Market size was valued at US$ 2.89 billion in 2024 and is projected to reach US$ 5.67 billion by 2032, at a CAGR of 9.0% during the forecast period 2025-2032.

Storage Class Memory (SCM) represents a breakthrough technology that bridges the gap between traditional memory and storage solutions. It combines the high-speed performance of DRAM with the non-volatile persistence of flash storage, enabling faster data access while maintaining energy efficiency. Major SCM types include 3D XPoint, ReRAM, and MRAM, with applications spanning enterprise storage systems, high-performance computing, and consumer electronics.

The market growth is driven by increasing demand for low-latency storage solutions in data centers, the proliferation of AI/ML workloads, and the need for energy-efficient memory architectures. While North America currently leads adoption (contributing over 40% of 2024 revenues), Asia-Pacific is emerging as the fastest-growing region due to semiconductor manufacturing expansion. Key players like Intel and Micron have accelerated product development, with Intel’s Optane technology demonstrating significant performance gains in enterprise applications.

MARKET DYNAMICS

MARKET DRIVERS

Growing Demand for High-Performance Computing to Accelerate SCM Adoption

The exponential growth in data-intensive applications across industries is driving unprecedented demand for high-performance storage solutions. Storage Class Memory (SCM) bridges the gap between traditional DRAM and NAND flash, offering latency close to DRAM while providing persistence at scale. With enterprises increasingly adopting AI, machine learning, and real-time analytics, SCM’s ability to reduce data bottlenecks is becoming critical. The technology’s sub-microsecond latency and high endurance make it ideal for workloads requiring rapid data access. Emerging use cases in financial services for high-frequency trading and healthcare for genomic sequencing are creating significant market traction. As computational requirements grow more demanding, SCM’s performance advantages position it as a key enabler of next-generation computing architectures.

Enterprise Digital Transformation Initiatives Fueling Market Expansion

Major corporations worldwide are investing heavily in digital infrastructure modernization, with storage performance being a critical focus area. SCM solutions are gaining traction as enterprises seek to optimize database performance, accelerate transaction processing, and improve application responsiveness. The technology’s ability to serve as either high-performance storage or expanded memory provides deployment flexibility that aligns perfectly with hybrid cloud strategies. Industries with mission-critical data requirements – including telecommunications, defense, and autonomous vehicle development – are increasingly incorporating SCM into their technology roadmaps. This enterprise adoption is expected to drive significant market growth as organizations prioritize infrastructure that can support emerging workloads and data-intensive applications.

Advancements in Non-Volatile Memory Technologies Creating New Opportunities

Recent breakthroughs in 3D XPoint, ReRAM, and other emerging memory technologies are expanding the potential applications for SCM. The development of more cost-effective manufacturing processes is beginning to address previous barriers to widespread adoption. Memory and storage vendors are actively innovating to improve endurance characteristics and reduce power consumption while maintaining the performance advantages that differentiate SCM from conventional solutions. These technological improvements are making SCM more viable for mainstream applications beyond high-performance computing, significantly broadening the addressable market. As research continues into new materials and architectures, SCM is positioned to play an increasingly vital role in next-generation computing ecosystems.

MARKET RESTRAINTS

High Production Costs and Manufacturing Complexity Limit Widespread Adoption

The specialized manufacturing processes required for Storage Class Memory technologies result in significantly higher production costs compared to traditional memory solutions. Fabricating 3D XPoint and other emerging memory technologies demands advanced semiconductor equipment and specialized materials that are not yet fully optimized for mass production. These cost factors currently limit SCM adoption primarily to high-value enterprise applications where performance benefits outweigh the premium pricing. While manufacturing efficiencies are expected to improve over time, the current cost structure presents a substantial barrier to broader market penetration, particularly in price-sensitive consumer applications.

Technical Challenges in System Integration Constrain Deployment Flexibility

Integration of SCM into existing computing architectures presents unique engineering challenges that can delay adoption. The technology’s intermediate position between memory and storage requires careful consideration of system architectures and software interfaces to maximize performance benefits. Operating systems and applications often require modification to fully leverage SCM’s capabilities, creating additional layers of complexity in deployment. This integration challenge is particularly acute in legacy environments where retrofitting SCM solutions may not be cost-effective. Until ecosystem support becomes more standardized across platforms, these technical hurdles will continue to constrain market growth.

Limited Ecosystem Support and Developer Awareness Slow Market Maturation

The relatively recent introduction of SCM technologies has resulted in a lag in comprehensive ecosystem support compared to established memory and storage solutions. Many application developers are still optimizing their software to take advantage of SCM’s unique characteristics, and system integrators may lack the expertise to properly assess implementation scenarios. This knowledge gap can create hesitation among potential adopters concerned about technology lock-in or uncertain ROI. While leading hyperscalers and cloud providers are beginning to offer SCM-based services, broader ecosystem maturation will be essential for mainstream market expansion.

MARKET CHALLENGES

Intense Competition from Established Memory Technologies Creates Market Disruption

SCM must compete with continuing advancements in both DRAM and NAND flash technologies that threaten to erode its performance advantages. DRAM manufacturers are pushing density improvements and new interfaces like DDR5, while NAND flash providers continue to advance 3D stacking and quad-level cell technologies. These improvements in conventional memory create performance overlaps that challenge SCM’s value proposition in certain applications. The memory industry’s cyclical nature and intense price competition further complicate market positioning for SCM solutions, requiring vendors to carefully differentiate their offerings.

Supply Chain Volatility and Component Shortages Impact Market Stability

The semiconductor industry’s ongoing supply chain challenges directly affect SCM production capacity and lead times. Many SCM technologies rely on specialized fabrication facilities and materials that are vulnerable to geopolitical tensions and trade restrictions. The concentration of advanced manufacturing capabilities in limited geographic areas creates potential bottlenecks that could constrain market growth during periods of high demand. Furthermore, the equipment and process technology required for novel memory architectures often ties producers to specific supplier relationships, reducing flexibility in responding to supply disruptions.

Uncertainty in Standards Development Creates Adoption Risks

The lack of fully established industry standards for SCM technologies creates uncertainty that may delay purchasing decisions. Interface standards, endurance measurement methods, and reliability expectations continue to evolve as the technology matures. This standards ambiguity makes it difficult for enterprise buyers to conduct accurate comparisons between solutions or ensure long-term compatibility with future architectures. Until robust standards emerge to guide implementation and interoperability, some potential customers may defer decisions in favor of more mature alternatives with established ecosystem support.

MARKET OPPORTUNITIES

Emerging Edge Computing Applications Create New Use Cases for SCM

The rapid growth of edge computing and IoT deployments presents significant opportunities for Storage Class Memory adoption. Edge environments demand high-performance, persistent storage in space- and power-constrained locations where SCM’s characteristics are particularly valuable. Applications in 5G infrastructure, industrial automation, and autonomous systems increasingly require the low-latency data access that SCM provides. As edge computing architectures evolve to support more sophisticated processing closer to data sources, SCM is well-positioned to address the unique performance and reliability requirements of these distributed environments.

Cloud Service Providers Driving Innovation in Memory-Centric Architectures

Leading cloud providers are pioneering new computing architectures that rebalance traditional memory and storage hierarchies, creating substantial opportunities for SCM adoption. Emerging memory-centric designs that address data movement bottlenecks align perfectly with SCM’s capabilities. Hyperscalers are increasingly evaluating SCM for high-performance database services, distributed caching layers, and accelerated machine learning pipelines. As cloud infrastructure continues to evolve toward more memory-driven architectures, SCM adoption in data center environments is expected to accelerate significantly.

Automotive and Aerospace Sectors Present Long-Term Growth Potential

Next-generation vehicle architectures and autonomous systems require high-reliability, high-performance storage solutions that can withstand demanding environmental conditions. SCM’s persistence and fast access characteristics make it well-suited for automotive applications ranging from advanced driver assistance systems to vehicle-to-everything communications. Similarly, aerospace and defense applications with stringent reliability requirements represent promising growth opportunities as these industries modernize their computing infrastructure. While qualification cycles in these sectors are lengthy, they represent substantial long-term market potential for SCM technologies.

STORAGE CLASS MEMORY MARKET TRENDS

Hybrid Memory Architectures Drive Adoption of Storage Class Memory

The increasing demand for high-performance computing across data centers, enterprise storage, and consumer electronics is fueling the growth of Storage Class Memory (SCM). As a hybrid memory architecture bridging DRAM and NAND flash, SCM offers unique advantages in speed, persistence, and power efficiency. Recent advancements in 3D XPoint, ReRAM, and MRAM technologies have pushed read/write speeds below 10 nanoseconds with endurance exceeding 10^7 cycles, making SCM increasingly viable for tiered memory solutions. The market is projected to grow at a compound annual growth rate of over 45% through 2032, driven by data-intensive applications in AI analytics and 5G networks.

Other Trends

Enterprise Storage Optimization

Enterprise adoption of SCM is accelerating as organizations seek to reduce latency in transactional databases and real-time analytics. Major cloud service providers now utilize SCM in tiered storage architectures, where it serves as a performance buffer between DRAM and SSDs. Persistent memory modules from Intel and Micron demonstrate 8x higher bandwidth compared to traditional NAND while maintaining byte-addressability. This hybrid approach reduces total cost of ownership by up to 30% for high-IOPS workloads.

Integration in Edge Computing Devices

The proliferation of edge computing necessitates energy-efficient memory solutions capable of handling localized data processing. SCM’s low power consumption (under 1W per GB for active modules) and non-volatility make it ideal for IoT endpoints and mobile devices. Automotive applications are emerging as a key growth sector, where SCM enables faster boot times and crash-safe data logging in autonomous vehicles. Recent developments show 25% faster neural network inference times when using SCM cache architectures versus conventional setups.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Players Drive Innovation in the Expanding Storage Class Memory Market

The global Storage Class Memory (SCM) market remains competitive and technology-driven, with semiconductor giants and emerging players striving to capitalize on high-performance memory demand. The market is currently dominated by top-tier memory manufacturers who are investing aggressively in SCM development, given its potential to bridge the gap between DRAM and NAND flash storage. KIOXIA (formerly Toshiba Memory) and Samsung currently maintain strong positions due to their vertical integration, extensive R&D capabilities, and early-mover advantage in 3D XPoint and other SCM technologies.

Intel Corporation previously played a pioneering role with its Optane memory solutions before discontinuing production, while Micron Technology continues advancing alternative SCM solutions through partnerships. The competitive intensity is further heightened by specialist firms like Everspin Technologies, which focuses exclusively on MRAM-based storage class memory applications for enterprise and industrial use cases.

Asian manufacturers are rapidly closing the technology gap, with SK Hynix Semiconductor and ChangXin Memory Technologies increasing their SCM investments to reduce dependence on foreign memory technologies. Market dynamics are shifting as companies explore different SCM approaches – from phase-change memory (PCM) to resistive RAM (ReRAM) and magnetoresistive RAM (MRAM) – each with distinct advantages for specific applications.

List of Key Storage Class Memory Companies Profiled

- KIOXIA (Japan)

- Samsung (South Korea)

- Hewlett Packard Enterprise (U.S.)

- Everspin Technologies (U.S.)

- Crossbar Inc. (U.S.)

- Micron Technology (U.S.)

- Western Digital Corp (U.S.)

- Intel Corporation (U.S.)

- Sony (Japan)

- SK Hynix Semiconductor (South Korea)

Segment Analysis:

By Type

Solid State Drive Segment Leads Due to High Performance and Persistent Storage Capabilities

The market is segmented based on type into:

- Solid State Drive

- Persistent Memory

By Application

Computer Applications Dominate With Increasing Demand for High-Speed Data Processing

The market is segmented based on application into:

- Mobile Phone

- Tablet

- Computer

- Others

By Technology

3D XPoint Technology Gains Traction for Superior Speed and Endurance

The market is segmented based on technology into:

- 3D XPoint

- ReRAM

- PCM

- MRAM

- Others

By End User

Enterprise Sector Accounts for Significant Share Due to Data Center Expansion

The market is segmented based on end user into:

- Enterprise

- Consumer Electronics

- Automotive

- Healthcare

- Others

Regional Analysis: Storage Class Memory Market

North America

North America, led by the U.S., dominates the Storage Class Memory (SCM) market, driven by robust investments in high-performance computing and enterprise data centers. The region benefits from strong R&D initiatives by key players like Intel, Micron Technology, and Western Digital, which continue to push the boundaries of SCM technology. A growing emphasis on AI-driven applications and cloud infrastructure modernization fuels demand for SCM solutions that bridge the gap between traditional DRAM and NAND flash. Enterprise adoption is particularly high due to the need for low-latency, persistent storage in financial services and hyperscale data centers. However, cost sensitivity remains a barrier for wider SCM deployment in cost-conscious industries.

Europe

Europe maintains a steady growth trajectory in SCM adoption, supported by stringent data privacy regulations (e.g., GDPR) that necessitate reliable and secure persistent memory solutions. Countries like Germany and France lead in industrial applications, leveraging SCM for Industry 4.0 and IoT-driven manufacturing. The region sees increasing collaboration between academia and corporations to develop next-generation SCM technologies. Sustainability concerns are gradually influencing SCM adoption, with enterprises prioritizing energy-efficient memory architectures. While market penetration remains lower than in North America, EU-backed semiconductor initiatives aim to strengthen the region’s position in the global SCM supply chain.

Asia-Pacific

The Asia-Pacific region is the fastest-growing SCM market, propelled by China’s aggressive semiconductor self-sufficiency goals and South Korea’s leadership in memory production through giants like Samsung and SK Hynix. China alone accounts for over 30% of the regional market, driven by government subsidies and expanding hyperscale data center deployments. Japan remains a key innovator in niche SCM applications, particularly for enterprise storage solutions. While price sensitivity limits widespread adoption in developing markets, the proliferation of 5G and edge computing is creating new opportunities for cost-effective SCM implementations across mobile and IoT applications.

South America

South America presents emerging potential for SCM technology, primarily in Brazil and Chile where financial institutions and cloud service providers are early adopters. Market growth remains constrained by limited local semiconductor manufacturing capabilities and reliance on imported solutions. Economic instability in key markets slows enterprise investment in next-gen memory technologies, though increasing digital transformation initiatives offer long-term opportunities. The lack of specialized IT infrastructure and skilled personnel further hinders rapid SCM adoption compared to more developed regions.

Middle East & Africa

The MEA region shows nascent but promising growth in SCM adoption, particularly in UAE and Saudi Arabia where smart city initiatives and oil/gas sector digitization create demand for high-performance memory solutions. Government-led technology investments drive early-stage deployments in financial hubs like Dubai and Tel Aviv. However, the market faces challenges including limited local technical expertise and preference for established memory solutions over newer SCM technologies. Infrastructure development for AI and cloud computing may accelerate SCM uptake in the coming years, though the region currently represents a small fraction of global demand.

Report Scope

This market research report provides a comprehensive analysis of the Global Storage Class Memory (SCM) market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global Storage Class Memory market was valued at US$ 2.89 billion in 2024 and is projected to reach US$ 5.67 billion by 2032.

- Segmentation Analysis: Detailed breakdown by product type (Solid State Drive, Persistent Memory), application (Mobile Phone, Tablet, Computer, Others), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa. The U.S. market is estimated at USD million in 2024, while China is projected to reach USD million by 2032.

- Competitive Landscape: Profiles of leading market participants including KIOXIA, Samsung, Micron Technology, Intel Corporation, and SK Hynix Semiconductor, covering their product portfolios, market shares, and strategic initiatives.

- Technology Trends & Innovation: Assessment of emerging SCM technologies, integration with AI/ML systems, and advancements in non-volatile memory architectures.

- Market Drivers & Restraints: Evaluation of factors such as growing demand for high-performance computing, data center expansion, and challenges related to high production costs.

- Stakeholder Analysis: Strategic insights for memory manufacturers, OEMs, cloud service providers, and investors regarding market opportunities and challenges.

The research methodology combines primary interviews with industry experts and analysis of verified market data from authoritative sources to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Storage Class Memory Market?

-> Storage Class Memory Market size was valued at US$ 2.89 billion in 2024 and is projected to reach US$ 5.67 billion by 2032, at a CAGR of 9.0% during the forecast period 2025-2032.

Which key companies operate in Global Storage Class Memory Market?

-> Key players include KIOXIA, Samsung, Micron Technology, Intel Corporation, SK Hynix Semiconductor, Western Digital, and Hewlett Packard Enterprise, among others.

What are the key growth drivers?

-> Key growth drivers include increasing demand for high-speed data processing, expansion of data centers, and adoption in AI/ML applications.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, driven by semiconductor manufacturing in South Korea, China, and Taiwan, while North America remains a technology leader.

What are the emerging trends?

-> Emerging trends include development of next-gen SCM solutions, integration with cloud infrastructure, and advancements in 3D XPoint technology.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...