MARKET INSIGHTS

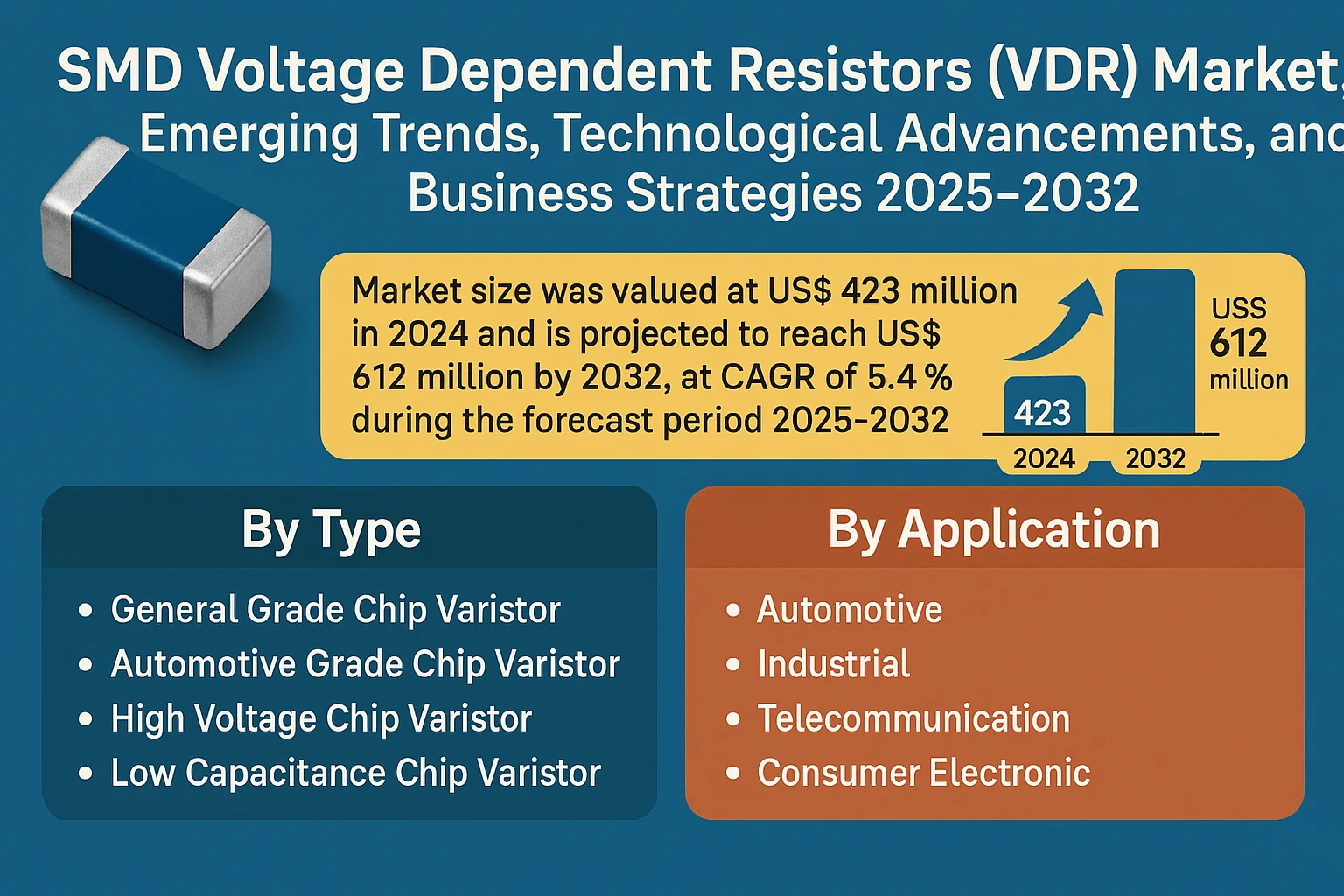

The global SMD Voltage Dependent Resistors (VDR) Market size was valued at US$ 423 million in 2024 and is projected to reach US$ 612 million by 2032, at a CAGR of 5.4% during the forecast period 2025-2032. The U.S. market accounted for 28% of global revenue in 2024, while China is expected to witness the fastest growth with a projected CAGR of 7.5% through 2032.

SMD Varistors (Surface Mount Device Varistors) are voltage-dependent resistors designed to protect electronic circuits from voltage spikes and transient surges. These components are critical in applications requiring miniaturized circuit protection, offering advantages such as fast response time, compact size, and high energy absorption capacity. The market includes two primary product types: General Grade Chip Varistors for standard applications and Automotive Grade Chip Varistors meeting stringent automotive reliability standards.

The market growth is primarily driven by increasing demand from consumer electronics and automotive sectors, where circuit protection requirements are becoming more stringent. The transition to 5G infrastructure and expansion of IoT devices are creating new opportunities, while supply chain challenges for raw materials remain a key constraint. Major players like TDK, Panasonic, and Littelfuse dominate the market, collectively holding over 45% revenue share in 2024, with ongoing investments in developing higher-capacity varistors for emerging applications.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Consumer Electronics to Accelerate SMD Varistor Adoption

The global consumer electronics market has witnessed exponential growth, with devices requiring advanced circuit protection components like SMD varistors. These components play a critical role in safeguarding sensitive electronic circuits from voltage surges and electrostatic discharge. As smartphones, laptops, and IoT devices become more sophisticated, manufacturers are integrating high-performance varistors to ensure product reliability. The market for consumer electronics is projected to grow at a compound annual growth rate of approximately 6% over the next five years, directly influencing demand for compact, high-efficiency protection components.

Automotive Electrification Trend to Spur Market Expansion

The automotive industry’s rapid transition toward electrification is creating substantial opportunities for SMD varistor manufacturers. Modern electric vehicles contain numerous electronic control units and power management systems that require robust over-voltage protection. Automotive-grade chip varistors are increasingly being adopted in battery management systems, onboard chargers, and infotainment systems. With global EV sales expected to surpass 20 million units annually by 2030, automotive applications will likely account for over 25% of the total SMD varistor market revenue.

5G Network Rollout to Drive Telecommunication Segment Growth

The ongoing global deployment of 5G infrastructure represents a significant growth driver for SMD varistors. Telecommunication base stations and network equipment require reliable surge protection solutions to maintain signal integrity and prevent equipment damage. Major telecommunications providers are investing heavily in 5G infrastructure, with total global investments expected to reach $1 trillion by 2025. This massive infrastructure development is creating sustained demand for high-performance SMD varistors capable of withstanding transient voltage events in sensitive communication equipment.

MARKET RESTRAINTS

Fluctuating Raw Material Prices to Impact Profit Margins

The SMD varistor manufacturing process relies heavily on zinc oxide and other rare earth materials, whose prices have shown significant volatility in recent years. These price fluctuations create challenges for manufacturers in maintaining stable profit margins while remaining competitive. The situation is further complicated by global supply chain disruptions and geopolitical factors affecting raw material availability. Many manufacturers are struggling to absorb these cost increases without passing them on to customers, potentially slowing market growth in price-sensitive segments.

Technical Limitations in High-Frequency Applications to Restrict Adoption

While SMD varistors offer excellent protection against transient voltage spikes, they face limitations in certain high-frequency applications. The intrinsic capacitance characteristics of varistors can sometimes interfere with signal integrity in GHz-range circuits. This technical constraint forces designers to seek alternative protection solutions for certain RF and microwave applications, potentially limiting market expansion in these specialized segments. The challenge is particularly acute in 5G mmWave applications and high-speed data communication systems where signal fidelity is paramount.

MARKET CHALLENGES

Intense Price Competition from Alternative Technologies

The circuit protection market presents numerous alternatives to SMD varistors, including TVS diodes, gas discharge tubes, and polymer-based solutions. These competing technologies are constantly improving their performance characteristics while often being priced more aggressively. Manufacturers must continually innovate to maintain their market position, investing heavily in research and development to enhance varistor performance characteristics such as response time, energy absorption capacity, and reliability under repetitive stresses.

Other Challenges

Miniaturization Pressures

The relentless trend toward smaller electronic devices creates constant pressure to reduce component sizes while maintaining or improving performance. Developing SMD varistors that meet increasingly stringent space requirements without compromising protection capabilities presents significant engineering challenges and requires substantial R&D investment.

MARKET OPPORTUNITIES

Emerging Industrial IoT Applications to Create New Growth Avenues

The rapid adoption of Industrial Internet of Things (IIoT) technologies across manufacturing and infrastructure sectors presents lucrative opportunities for SMD varistor manufacturers. IIoT sensors and edge devices deployed in harsh industrial environments require robust circuit protection against electrical transients. With the global IIoT market expected to grow at a compound annual rate exceeding 20%, specialized industrial-grade SMD varistors represent a high-growth segment where manufacturers can differentiate through enhanced durability and performance characteristics.

Advancements in Material Science to Enable New Product Developments

Recent breakthroughs in material science, particularly in nano-engineered ceramics and composite materials, are opening new possibilities for SMD varistor performance enhancement. Manufacturers investing in these advanced materials can develop next-generation products with superior characteristics such as faster response times, higher energy absorption capacity, and improved thermal stability. These technological advancements will likely create premium market segments and drive higher-margin product offerings.

SMD VARISTOR MARKET TRENDS

Miniaturization and High-Performance Requirements Driving SMD Varistor Adoption

The global SMD varistor market is witnessing substantial growth due to increasing demand for miniaturized electronic components with superior voltage protection capabilities. Surface-Mount Device (SMD) varistors are becoming essential in modern electronics because they offer compact form factors without compromising surge protection performance. The telecommunications sector accounts for nearly 28% of global demand, followed by automotive applications at 22%, as these industries require reliable overvoltage protection in space-constrained environments. Recent advancements in multilayer ceramic varistor (MLCV) technology have enabled higher energy absorption densities – some premium models now withstand over 6000A surge currents while maintaining sub-millimeter package sizes.

Other Trends

Automotive Electrification Fueling Tier-1 Supplier Demand

The rapid transition towards electric vehicles is creating unprecedented demand for automotive-grade SMD varistors. Modern EVs contain approximately 40% more surge protection components than conventional vehicles, primarily due to high-voltage battery systems and sensitive ADAS electronics. Leading manufacturers have responded by developing AEC-Q200 qualified varistors with operating temperatures exceeding 125°C. The European EV market alone is projected to drive 35% of total automotive varistor demand growth through 2032.

5G Infrastructure Deployment Accelerating Market Expansion

Global 5G network rollout necessitates advanced circuit protection solutions, particularly in base station power supplies and RF modules. SMD varistors designed for GHz-frequency applications are seeing 18-22% annual growth rates as telecom operators upgrade infrastructure. Recent product innovations include low-capacitance varistors (<1pF) that maintain protection performance while minimizing signal interference – a critical requirement for 5G mmWave applications. Asia-Pacific dominates this segment with China accounting for over 60% of 5G-related varistor procurement volumes in 2024.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Expand Capacities to Meet Rising Demand for Miniaturized Electronics

The global SMD varistor market demonstrates a moderately concentrated competitive structure, with TDK Corporation and Panasonic collectively holding over 30% revenue share as of 2024. These Japanese electronics giants dominate due to their vertically integrated production capabilities and extensive patent portfolios covering multilayer chip varistor technologies.

AVX Corporation (a subsidiary of Kyocera) and Littelfuse have strengthened their positions through strategic acquisitions – notably AVX’s 2023 purchase of a Taiwanese ceramic component manufacturer to boost Asia-Pacific production. Meanwhile, KOA Corporation is gaining traction in the automotive segment through its proprietary high-temperature resistant SMD varistors certified for EV applications.

The competitive intensity is increasing as Chinese manufacturers like Shenzhen Sunlord and Sinochip Electronics capture mid-market share with competitively priced alternatives. However, quality differentiation remains pronounced, with Japanese brands commanding 15-20% price premiums for industrial-grade components. Most tier-1 players are currently expanding 0402 and 0201 package production lines to address the smartphone and IoT device miniaturization trend.

List of Key SMD Varistor Manufacturers Profiled

- TDK Corporation (Japan)

- Panasonic Corporation (Japan)

- AVX Corporation (U.S.)

- KOA Corporation (Japan)

- Littelfuse (U.S.)

- MARUWA Co., Ltd. (Japan)

- Lattron (Taiwan)

- Shenzhen Sunlord Electronics (China)

- JOYIN (China)

- Sinochip Electronics (China)

- Yageo Corporation (Taiwan)

- TA-I Technology (Taiwan)

- ROHM Semiconductor (Japan)

Segment Analysis:

By Type

General Grade Chip Varistor Leads the Market Owing to Wide Adoption in Consumer Electronics and Industrial Applications

The market is segmented based on type into:

- General Grade Chip Varistor

- Automotive Grade Chip Varistor

- Subtypes: AEC-Q200 compliant and others

- High Voltage Chip Varistor

- Low Capacitance Chip Varistor

- Others

By Application

Consumer Electronics Dominates Due to Increasing Demand for Surge Protection in Smart Devices

The market is segmented based on application into:

- Automotive

- Industrial

- Telecommunication

- Consumer Electronic

- Others

By Voltage Range

Low Voltage Segment Shows Strong Growth Potential for Portable Electronics Applications

The market is segmented based on voltage range into:

- Low Voltage (Below 30V)

- Medium Voltage (30V-100V)

- High Voltage (Above 100V)

Regional Analysis: SMD Varistor Market

North America

The North American SMD varistor market is characterized by high demand for advanced electronic components driven by robust telecommunications infrastructure, automotive electrification trends, and stringent quality standards for consumer electronics. The United States accounts for over 75% of regional demand, fueled by military/aerospace applications requiring high-reliability components and growing EV production. While supply chain disruptions temporarily impacted availability, regional manufacturers like Littelfuse and Bourns continue to lead in technological innovation, particularly in automotive-grade chip varistors that meet AEC-Q200 standards. The market benefits from strong R&D investments, with companies prioritizing miniaturization and higher energy absorption capabilities.

Europe

Europe’s market demonstrates steady growth, supported by the region’s strong industrial automation sector and renewable energy infrastructure requiring voltage protection solutions. Germany remains the largest consumer, accounting for nearly 30% of regional sales, owing to its automotive manufacturing base and Industry 4.0 adoption. EU directives on electronic waste and hazardous substances (RoHS/REACH) have pushed manufacturers toward lead-free and halogen-free varistor compositions. While price competition from Asian suppliers presents challenges, European OEMs maintain competitiveness through specialized products for medical equipment and smart grid applications. Collaborative research initiatives between academia and industry aim to develop next-generation varistors with enhanced thermal stability.

Asia-Pacific

Dominating over 60% of global production volume, the Asia-Pacific region thrives due to China’s electronics manufacturing ecosystem and Japan’s leadership in component innovation. Chinese suppliers like Sinochip Electronics have gained substantial market share through cost-effective general-grade varistors, though quality concerns persist in the low-end segment. Meanwhile, Japanese firms (TDK, Panasonic) lead in high-reliability automotive and industrial applications. The region faces unique challenges including raw material price volatility and intellectual property protection issues, but growing 5G infrastructure deployment and EV adoption across India and Southeast Asia present significant opportunities. Taiwan-based manufacturers are increasingly influential in the supply chain through technological partnerships.

South America

This emerging market shows gradual but uneven growth, largely dependent on imported components due to limited local manufacturing capabilities. Brazil represents the largest market, with demand driven by industrial equipment maintenance and telecommunications network expansions. However, economic instability and currency fluctuations frequently disrupt supply chains, forcing buyers toward lower-cost alternatives rather than premium-grade varistors. The lack of standardized testing facilities in the region complicates quality verification processes. Nonetheless, increasing investments in renewable energy projects and the gradual modernization of manufacturing infrastructure suggest long-term potential, particularly for suppliers willing to establish local distribution partnerships.

Middle East & Africa

The market remains in nascent stages but demonstrates promising growth pockets centered around UAE’s electronics trading hubs and South Africa’s industrial sector. High reliance on imports creates pricing disadvantages, though regional distributors are increasingly stocking SMD varistors to serve oil/gas equipment maintenance and telecommunications tower deployments. The lack of component manufacturing bases and technical expertise limits market sophistication, with most demand concentrated in replacement markets rather than new product integration. However, smart city initiatives in GCC countries and renewable energy projects across North Africa may drive future demand for higher-grade protection components, pending stable economic conditions and improved technical education infrastructure.

Report Scope

This market research report provides a comprehensive analysis of the global and regional SMD Varistor markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global SMD Varistor market was valued at USD 1.2 billion in 2024 and is projected to reach USD 1.8 billion by 2032, growing at a CAGR of 5.3%.

- Segmentation Analysis: Detailed breakdown by product type (General Grade Chip Varistor, Automotive Grade Chip Varistor), application (Automotive, Industrial, Telecommunication, Consumer Electronics), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America (USD 420 million in 2024), Europe, Asia-Pacific (projected to grow at 6.1% CAGR), Latin America, and Middle East & Africa, with country-level analysis.

- Competitive Landscape: Profiles of leading players including TDK (18% market share), Panasonic, AVX, Littelfuse, and KOA Corporation, covering their product portfolios, R&D investments, and recent M&A activities.

- Technology Trends: Assessment of miniaturization trends, high-voltage SMD varistors, and integration with IoT devices for surge protection applications.

- Market Drivers & Restraints: Analysis of factors such as growing electronics manufacturing in Asia, increasing demand for circuit protection, and challenges like raw material price volatility.

- Stakeholder Analysis: Strategic insights for component manufacturers, OEMs, distributors, and investors regarding supply chain optimization and emerging opportunities.

The research methodology combines primary interviews with industry experts and analysis of verified market data from regulatory filings, trade associations, and financial reports to ensure accuracy.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global SMD Varistor Market?

-> The global SMD Varistor size was valued at US$ 423 million in 2024 and is projected to reach US$ 612 million by 2032, at a CAGR of 5.4% during the forecast period 2025-2032.

Which key companies operate in Global SMD Varistor Market?

-> Key players include TDK, Panasonic, AVX, KOA Corporation, Littelfuse, MARUWA, and Shenzhen Sunlord, with the top five companies holding approximately 45% market share.

What are the key growth drivers?

-> Key growth drivers include increasing electronics production, demand for circuit protection in EVs, and 5G infrastructure development.

Which region dominates the market?

-> Asia-Pacific dominates with over 55% market share, driven by electronics manufacturing in China, Japan, and South Korea.

What are the emerging trends?

-> Emerging trends include high-voltage SMD varistors for automotive applications and miniaturization for consumer electronics.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...