Smart Grid Control Market Insights

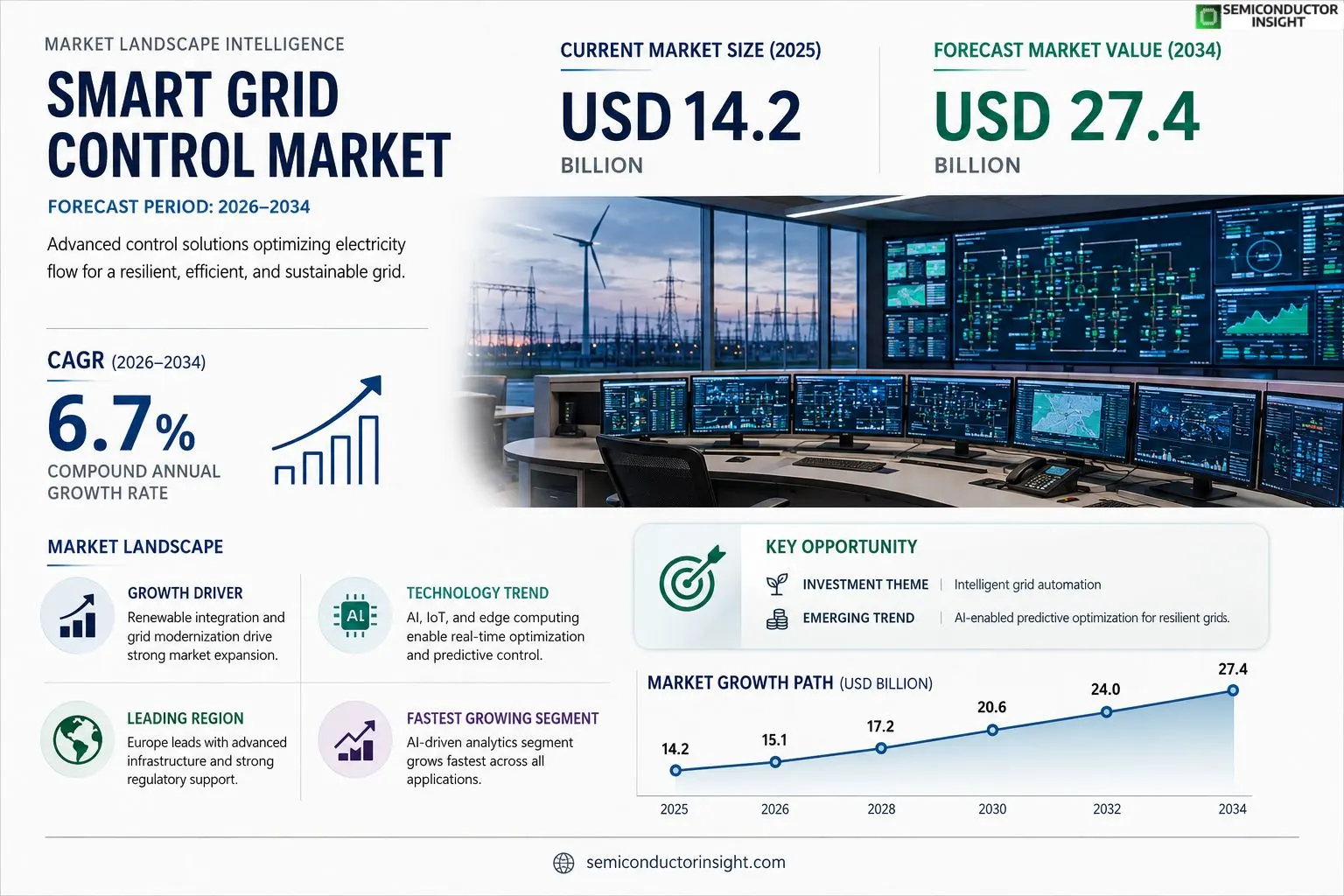

Smart Grid Control Market size was valued at USD 14.2 billion in 2025. The market is projected to grow from USD 15.1 billion in 2026 to USD 27.4 billion by 2034, exhibiting a CAGR of 6.7% during the forecast period.

Smart Grid Control refers to advanced hardware and software solutions that monitor, manage, and optimize electricity flow across modern power networks. These systems integrate real‑time data analytics, automated demand response, distributed energy resource coordination, and cybersecurity measures to ensure reliability and efficiency.The market is experiencing rapid growth due to several factors, including increased investment in renewable‑energy integration, rising demand for grid resiliency, and supportive regulatory frameworks worldwide. Furthermore, advancements in IoT sensors and AI‑driven analytics are accelerating adoption of Smart Grid Control solutions. Initiatives by key players such as Siemens AG, Schneider Electric, ABB Ltd., and General Electric are also expected to fuel expansion; for example, in March 2024 Siemens announced a strategic partnership with a leading utility to deploy its next‑generation control platform across Europe.

MARKET DRIVERS

Growing Renewable Energy Integration

The increasing penetration of solar and wind resources requires real‑time balancing, which positions Smart Grid Control Market as a critical enabler for grid stability. Utilities are adopting advanced control algorithms to manage variable generation while maintaining power quality.

Regulatory Incentives for Modernization

Government policies that promote grid resilience and carbon reduction are accelerating investments in automated control platforms. Compliance mandates are prompting utilities to replace legacy SCADA systems with smarter, interoperable solutions.

➤ Industry analysts project a compound annual growth rate of around 9% for Smart Grid Control Market through 2030, driven by digital transformation initiatives.

Moreover, the expansion of electric vehicle charging infrastructure adds new demand for dynamic load management, further boosting the market’s growth trajectory.

MARKET CHALLENGES

Cybersecurity Vulnerabilities

As control layers become more networked, Smart Grid Control Market faces heightened risk of cyber attacks, potentially compromising grid reliability. Robust security frameworks are still evolving, creating hesitation among stakeholders.

Other Challenges

Integration Complexity

Legacy equipment often lacks standard communication protocols, making seamless integration costly and time‑consuming. Utilities must invest in middleware or replace aging assets to achieve full interoperability.In addition, the shortage of skilled personnel familiar with both power systems and IT increases project timelines and operational expenses.

MARKET RESTRAINTS

High Capital Expenditure

The upfront cost of deploying advanced control devices and communication infrastructure remains a significant barrier, particularly for smaller utilities with limited budgets.

Regulatory Approval Delays

Complex permitting processes and the need for extensive compliance testing can postpone rollout schedules, slowing market momentum.Furthermore, uncertainties around tariff structures for ancillary services can deter investment in sophisticated control solutions.

MARKET OPPORTUNITIES

Artificial Intelligence‑Driven Optimization

AI and machine‑learning models enable predictive load forecasting and automated response, creating a sizable opportunity for vendors that can embed these capabilities into Smart Grid Control Market offerings.

Edge Computing Expansion

Deploying compute resources at the network edge reduces latency and enhances resilience, positioning edge‑enabled controllers as a growth catalyst for the market.Additionally, the rise of microgrids and community energy projects opens new niches where localized control solutions can be monetized.

Smart Grid Control Market Trends

Renewable Energy Integration and Real‑Time Grid Optimization

Smart Grid Control Market is witnessing a decisive shift toward deeper renewable energy integration. Advanced control platforms now enable instantaneous balancing of wind and solar outputs with conventional generation, reducing reliance on fossil‑fuel peaking plants. Grid operators leverage high‑frequency data streams to adjust voltage and frequency in real time, improving overall system efficiency. This transition is reinforced by policy incentives that prioritize low‑carbon electricity, prompting utilities to adopt sophisticated monitoring and dispatch tools across transmission and distribution networks.

Other Trends

AI‑Driven Predictive Maintenance

Artificial intelligence is becoming a cornerstone of predictive maintenance within Smart Grid Control Market. Machine‑learning models analyze equipment performance metrics, detecting early signs of wear or malfunction before outages occur. By scheduling targeted interventions, utilities reduce downtime and extend asset life, leading to measurable cost savings. The integration of AI with edge computing further accelerates decision cycles, allowing localized devices to trigger corrective actions without central processor delay.

Cybersecurity and Distributed Energy Resource Coordination

As grid architectures become increasingly digital, Smart Grid Control Market places heightened emphasis on cybersecurity. Robust encryption, authentication protocols, and intrusion‑detection systems are now embedded directly into control software to shield critical infrastructure from evolving threats. Simultaneously, the market supports coordinated management of distributed energy resources (DERs) such as rooftop solar, battery storage, and electric vehicle chargers. Unified platforms ensure that DERs respond cohesively to grid signals, enhancing reliability while maintaining a secure communication environment.

COMPETITIVE LANDSCAPEKey Industry Players

Smart Grid Control Market Competitive Overview

Smart Grid Control Market is anchored by a handful of multinational giants that dominate both hardware and software segments. Siemens AG leads the landscape with an extensive SCADA and energy management portfolio, leveraging its strong presence in Europe and North America. Schneider Electric follows closely, offering integrated DMS and demand‑response solutions that benefit from its worldwide distribution network. ABB Ltd. and General Electric round out the top tier, each providing end‑to‑end automation platforms and advanced FLISR technologies that are critical for grid resilience. Hitachi Energy, the spin‑off from Hitachi Ltd., has accelerated its market share through strategic acquisitions and AI‑driven analytics, positioning itself as a key enabler for renewable‑rich grids. Collectively, these firms account for more than half of revenues, shaping standards, pricing structures, and the pace of innovation. Their scale enables cross‑border projects and long‑term service contracts, creating high entry barriers for smaller entrants and driving consolidation through joint ventures and licensing agreements.Beyond the dominant quartet, a diverse set of established and emerging companies contributes to niche and regional strengths. Toshiba Energy Systems and Mitsubishi Electric supply robust transmission‑level control equipment, while IBM and OSIsoft (now part of AVEVA) focus on data analytics and cloud‑based grid management platforms. Emerging pure‑play software firms such as AutoGrid, Opus One Solutions, and Greenlane offer demand‑response and distributed energy resource orchestration tools that attract utilities seeking agile, SaaS‑based deployments. Regional leaders including China’s State Grid Corporation, India’s Power Grid Corporation, and Brazil’s Enel Distribuição also expand the competitive mix with localized solutions and government‑backed projects. This breadth of participants ensures continuous innovation in AI‑enhanced forecasting, IoT sensor integration, and cybersecurity, keeping the market dynamic despite the dominance of the top tier.

List of Key Smart Grid Control Companies Profiled

- Siemens AG

- Schneider Electric

- ABB Ltd.

- General Electric

- Hitachi Energy

- Toshiba Energy Systems

- Mitsubishi Electric

- IBM

- OSIsoft (AVEVA)

- AutoGrid

- Opus One Solutions

- Greenlane

- State Grid Corporation of China

- Power Grid Corporation of India

- Enel Distribuição

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Hardware Controllers

|

| By Application |

|

Renewable Integration

|

| By End User |

|

Utilities

|

| By Technology |

|

AI‑driven Analytics

|

| By Functionality |

|

Real‑time Monitoring

|

Regional Analysis: North America

United States

The continued rollout of AMI is a primary driver. Investments in smart meters and communication networks are creating a vast amount of data that necessitates sophisticated control and analytics platforms.

With increasing connectivity, cybersecurity has become paramount. The market for security solutions designed to protect grid control systems from cyber threats is witnessing substantial growth.

The integration of energy storage systems is becoming increasingly important for grid stability and reliability. Smart grid control solutions are crucial for managing the bidirectional flow of energy between the grid and storage assets.

Demand response programs are gaining traction as a way to optimize energy consumption and reduce peak loads. Smart grid control systems play a key role in enabling and managing these programs effectively.

Europe

The European Smart Grid Control Market is characterized by a strong emphasis on energy efficiency and sustainability. Driven by ambitious climate goals and supportive government policies, the region is witnessing significant investments in grid modernization. The integration of renewable energy sources, such as wind and solar power, is a major catalyst for growth, necessitating advanced control systems to manage the intermittent nature of these resources. The market is diverse, with varying levels of adoption across different countries. Key trends include the deployment of smart grids in urban areas, the development of virtual power plants (VPPs), and the growing use of blockchain technology for secure energy trading. Business strategies often involve collaborative projects between utilities, research institutions, and technology providers.

Asia-Pacific

Asia-Pacific represents the fastest-growing market for Smart Grid Control, driven by rapid economic development and increasing energy demand. Countries like China, India, and Japan are making significant investments in grid infrastructure to support their growing economies and ambitious decarbonization targets. The region is witnessing a surge in the deployment of smart meters and the adoption of advanced control systems. The focus is on enhancing grid reliability, improving energy efficiency, and integrating renewable energy sources. Key trends include the development of smart cities, the adoption of microgrids, and the use of big data analytics for grid optimization. Business strategies often involve partnerships between international technology providers and local utilities, with a focus on delivering cost-effective solutions.

South America

Smart Grid Control Market in South America is poised for growth, driven by increasing energy demand and a growing focus on grid modernization. Countries like Brazil and Chile are investing in grid infrastructure to improve reliability and support the integration of renewable energy sources. The market is relatively fragmented, with opportunities for both established technology providers and new entrants. Key trends include the deployment of smart meters, the development of smart grids in urban areas, and the adoption of energy management systems. Business strategies often involve partnerships with local utilities and governments to secure projects and navigate regulatory complexities.

Middle East & Africa

The Middle East & Africa region presents significant growth potential for Smart Grid Control Market, driven by rapid urbanization, increasing energy demand, and government initiatives to modernize grid infrastructure. Countries like Saudi Arabia, the UAE, and South Africa are investing heavily in smart grid technologies to improve reliability and support economic diversification. Key trends include the deployment of smart meters, the development of smart grids in urban areas, and the adoption of energy efficiency measures. Business strategies often involve collaborations with international technology providers and local developers to deliver comprehensive solutions.

Report Scope

This market research report provides a comprehensive analysis of the Smart Grid Control Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia‑Pacific, Latin America, and the Middle East & Africa, including country‑level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market‑entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real‑time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Smart Grid Control Market?

-> Smart Grid Control Market was valued at USD 14.2 billion in 2025 and is expected to reach USD 27.4 billion by 2034, exhibiting a CAGR of 6.7% during the forecast period.

Which key companies operate in Smart Grid Control Market?

-> Key players include Siemens AG, Schneider Electric, ABB Ltd., and General Electric, among others.

What are the key growth drivers?

-> Key growth drivers include increased investment in renewable‑energy integration, rising demand for grid resiliency, supportive regulatory frameworks, and advancements in IoT sensors and AI‑driven analytics.

Which region dominates the market?

-> Europe remains a dominant market due to advanced grid infrastructure and regulatory support, while Asia‑Pacific shows fast‑growing potential.

What are the emerging trends?

-> Emerging trends include integration of IoT sensors, AI‑driven analytics, and enhanced cybersecurity measures for grid operations.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...