MARKET INSIGHTS

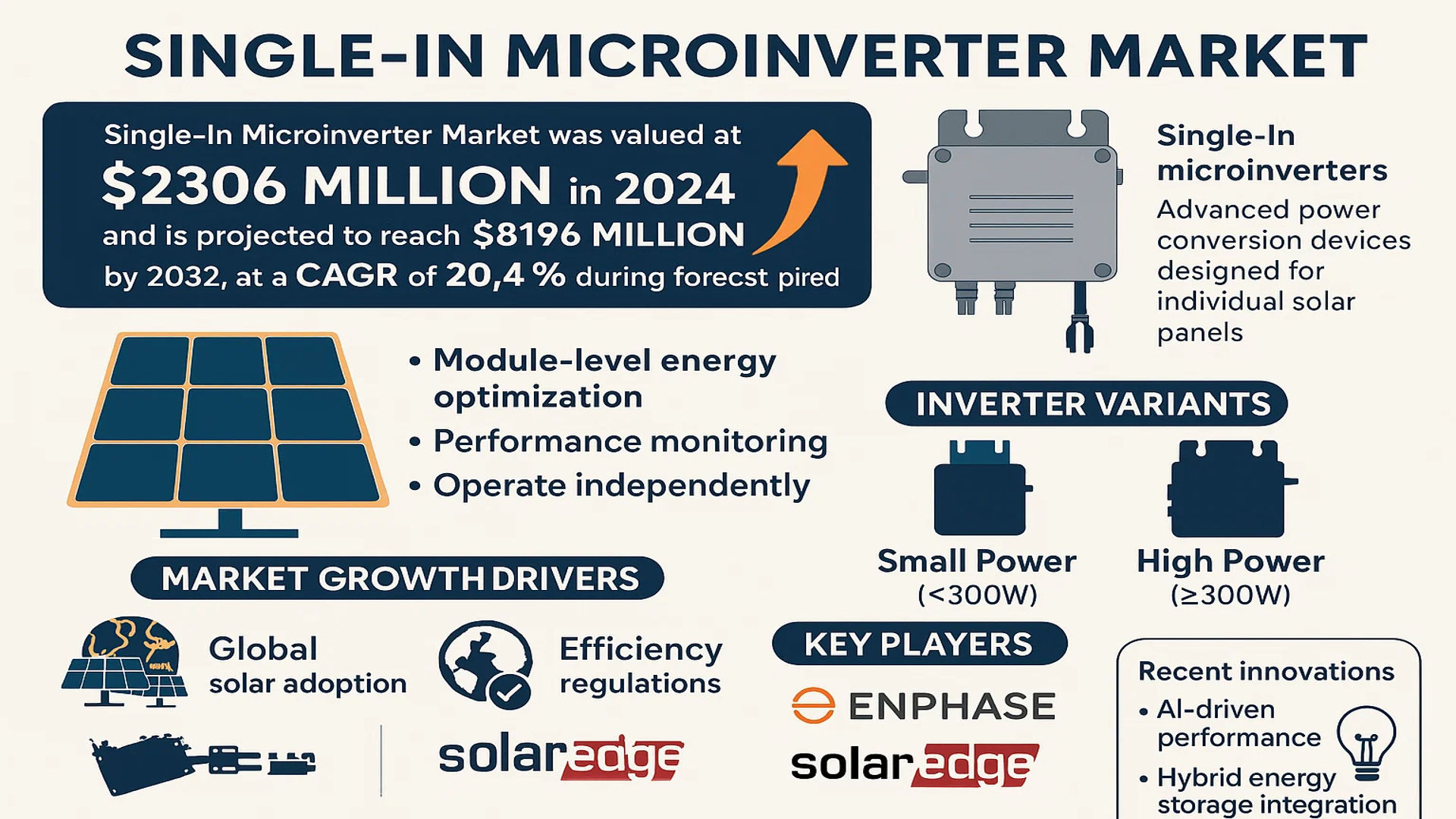

The global Single-In Microinverter Market was valued at 2306 million in 2024 and is projected to reach US$ 8196 million by 2032, at a CAGR of 20.4% during the forecast period.

Single-In microinverters are advanced power conversion devices designed for individual solar panels, enabling module-level energy optimization and performance monitoring. Unlike traditional string inverters, these systems operate independently, ensuring maximum power harvest even under partial shading or panel mismatch conditions. The technology includes variants such as small power inverters (typically below 300W) and high-power inverters (300W and above), catering to diverse residential and commercial applications.

The market growth is primarily driven by accelerating global solar adoption, particularly in distributed generation systems, alongside stringent efficiency regulations. Furthermore, rising demand for real-time monitoring and maintenance capabilities in photovoltaic systems has increased the preference for microinverters. Key players like Enphase Energy and SolarEdge Technologies continue to dominate the market, with recent innovations focusing on AI-driven performance analytics and hybrid energy storage integration.

MARKET DYNAMICS

MARKET DRIVERS

Growing Adoption of Solar Energy Systems Accelerates Market Expansion

The global push toward renewable energy adoption, particularly solar photovoltaic (PV) systems, is driving substantial growth in the single-in microinverter market. Residential and small-scale commercial solar installations have seen a compound annual growth rate exceeding 25% over the past five years, creating robust demand for module-level power electronics. With single-in microinverters offering up to 25% higher energy yields compared to traditional string inverters in partially shaded conditions, their value proposition resonates strongly with installers and end-users seeking maximum system efficiency.

Advancements in Module-Level Monitoring Technology Fuel Demand

Modern single-in microinverters now incorporate sophisticated monitoring capabilities that provide real-time performance data for individual panels. This technological evolution enables proactive maintenance, with systems detecting efficiency drops as small as 5% at the module level. As smart home integration becomes more prevalent, these monitoring features are being seamlessly incorporated into home automation systems, increasing consumer appeal. The ability to track and optimize each panel’s performance through mobile applications has become a key differentiator in purchase decisions.

Furthermore, regulatory support for distributed energy generation continues to strengthen market prospects. Many regions now mandate module-level rapid shutdown capabilities for safety compliance – a feature inherently provided by microinverter systems. This regulatory tailwind has been particularly influential in North American markets, where building codes increasingly require such safety measures.

MARKET RESTRAINTS

Higher System Costs Compared to String Inverters Limit Market Penetration

While offering superior performance characteristics, single-in microinverters typically command a price premium of 20-30% over conventional string inverter solutions. This cost differential remains a significant barrier to adoption in price-sensitive markets, particularly in developing economies where upfront cost weighs heavily in purchasing decisions. The requirement for multiple microinverters in medium-to-large installations further compounds this challenge, as system costs scale linearly with panel count.

Installation Complexity Presents Operational Challenges

The distributed nature of microinverter systems introduces installation complexities not present in centralized inverter architectures. Each panel requires individual microinverter mounting and wiring, increasing labor time by approximately 15-20% compared to string inverter installations. This complexity is particularly pronounced in retrofit applications, where existing mounting systems may not readily accommodate microinverter hardware. Furthermore, maintenance access to roof-mounted microinverters can prove challenging, potentially increasing service costs over the system lifetime.

MARKET OPPORTUNITIES

Emerging Battery Storage Integration Creates New Growth Avenues

The rapid growth of residential energy storage systems presents a significant opportunity for single-in microinverter manufacturers. New hybrid microinverter designs capable of DC-coupled battery integration are gaining traction, with adoption rates forecast to triple over the next five years. These systems provide homeowners with enhanced energy independence while optimizing self-consumption of solar generation. The ability to manage both PV production and battery storage at the module level offers unprecedented flexibility in energy management.

Expansion in Emerging Markets Offers Untapped Potential

Developing economies with growing electricity demand and unreliable grid infrastructure represent substantial growth opportunities. Markets in Southeast Asia and Latin America are experiencing annual solar installation growth exceeding 30%, with distributed generation playing an increasingly important role in electrification strategies. Localized manufacturing initiatives and innovative financing models are helping overcome cost barriers, making microinverter technology more accessible in these regions. The modular nature of microinverter systems makes them particularly suitable for the gradual expansion common in developing solar markets.

MARKET CHALLENGES

Reliability Concerns in Harsh Environmental Conditions

Microinverters mounted directly beneath solar panels must endure extreme temperature fluctuations, with operating environments regularly exceeding 60°C in warm climates. While manufacturers have made significant durability improvements, field data indicates failure rates remain 2-3 times higher than centralized inverters in high-temperature regions. Addressing these reliability challenges through improved thermal management and robust component selection will be critical for maintaining consumer confidence and minimizing warranty claims.

Technological Convergence with Power Optimizers Creates Competitive Pressure

The emergence of module-level power optimizers combined with hybrid inverters presents an increasingly competitive alternative to microinverter systems. These solutions offer many of the performance benefits of microinverters while maintaining aspects of centralized architecture. As this technology matures and costs decline, microinverter manufacturers must continue innovating to maintain their value proposition, particularly in the mid-range power segment where competition is most intense.

SINGLE-IN MICROINVERTER MARKET TRENDS

Modular Solar Adoption Fueling Single-In Microinverter Demand

The global shift toward distributed solar energy systems is driving significant demand for single-in microinverters, which optimize power output at the individual panel level. Unlike traditional string inverters, these devices enable module-level maximum power point tracking (MPPT), improving efficiency by 5-25% in partially shaded or unevenly oriented installations. With residential solar installations projected to grow at over 8% annually through 2030, the market for single-in solutions is expanding correspondingly. Recent technological advancements include integrated diagnostic capabilities and cloud-based monitoring platforms that provide real-time performance analytics for each photovoltaic panel.

Other Trends

Smart Grid Integration

Utilities worldwide are increasingly favoring microinverter-equipped systems due to their grid-support functionalities, including reactive power control and rapid shutdown compliance. Single-in microinverters now incorporate smart grid communication protocols that allow distributed energy resources to participate in demand response programs. This capability is becoming critical as over 30 countries have implemented net metering policies that reward distributed generation.

Technological Advancements Reinventing Product Capabilities

Manufacturers are overcoming traditional limitations of microinverters through innovations in wide-bandgap semiconductors (GaN and SiC) that boost efficiency above 97% while reducing form factors by 40-50%. New hybrid architectures combine the benefits of microinverters with DC optimizers, creating systems that deliver module-level optimization while minimizing balance-of-system costs. Furthermore, the integration of AI-driven predictive maintenance algorithms helps identify underperforming panels before significant energy losses occur, addressing a key concern in operations and maintenance budgets.

COMPETITIVE LANDSCAPE

Key Industry Players

Solar Technology Leaders Compete Through Innovation and Strategic Expansion

The global single-in microinverter market features a dynamic competitive landscape, with a mix of established solar technology giants and emerging innovators. Enphase Energy currently dominates the market, holding approximately 40% of global revenue share in 2024. Their leadership stems from patented microinverter technology and comprehensive monitoring solutions that set industry benchmarks for reliability and efficiency.

SMA Solar Technology and SolarEdge Technologies represent significant competitors, together accounting for nearly 30% of the market. These companies have gained traction through vertical integration strategies, offering complete solar solutions that combine microinverters with energy storage and smart energy management systems. Their growth reflects the increasing demand for holistic residential solar solutions across North America and Europe.

The market also includes agile innovators like Hoymiles and APsystems, who are disrupting traditional pricing models with cost-competitive offerings. These companies are gaining market share in price-sensitive regions, particularly in Asia-Pacific, where solar adoption is accelerating due to government incentives and rising electricity costs.

Meanwhile, industrial conglomerates such as ABB Group and Siemens are leveraging their established electrical infrastructure expertise to develop microinverter solutions for commercial applications. Their entry strengthens competition in the high-power segment, where reliability and grid integration capabilities are paramount.

List of Key Single-In Microinverter Companies Profiled

- Enphase Energy Inc. (U.S.)

- SolarEdge Technologies (Israel)

- SMA Solar Technology (Germany)

- ABB Group (Switzerland)

- Siemens AG (Germany)

- BENY Electric (China)

- Hoymiles (China)

- APsystems (U.S.)

- Texas Instruments (U.S.)

- Delta Energy Systems (Taiwan)

Segment Analysis:

By Type

High Power Inverter Segment Leads Market Due to Rising Demand for Commercial Applications

The market is segmented based on type into:

- Small Power Inverter

- Subtypes: Sub-300W, 300W-500W

- High Power Inverter

- Subtypes: 500W-800W, Above 800W

By Application

Residential Segment Dominates Owing to Increased Solar Adoption in Homes

The market is segmented based on application into:

- Residential

- Commercial

By Connectivity

Grid-Tied Systems Account for Major Share Due to Higher Installation Rates

The market is segmented based on connectivity into:

- Grid-Tied Systems

- Off-Grid Systems

- Hybrid Systems

By Component

Integrated Solutions Gain Traction Due to Plug-and-Play Convenience

The market is segmented based on component into:

- Standalone Microinverters

- Integrated Microinverter Systems

- Monitoring Hardware

Regional Analysis: Single-In Microinverter Market

Asia-Pacific

The Asia-Pacific region dominates the global Single-In Microinverter market, accounting for the largest share of both revenue and installations in 2024. China, Japan, and India are the key contributors, driven by robust government incentives, rapid urbanization, and the push for renewable energy adoption. China, in particular, leads with an annual solar capacity addition of over 50 GW, supported by policies like the 14th Five-Year Plan. Japan’s Feed-in-Tariff (FIT) scheme has also fueled residential solar installations, where microinverters are increasingly preferred for their efficiency in limited rooftop spaces. While cost sensitivity remains a challenge, the region’s focus on distributed energy systems ensures sustained demand.

North America

North America is the second-largest market, with the U.S. contributing over 80% of regional demand. The Inflation Reduction Act (IRA) of 2022, which allocates $369 billion for clean energy investments, has accelerated residential and commercial solar adoption. States like California and Texas are hotspots due to high solar irradiance and supportive net metering policies. Enphase Energy, a U.S.-based leader, holds a significant market share, leveraging advanced module-level power electronics (MLPE) technology. However, competition from string inverters and supply chain constraints pose challenges to market expansion.

Europe

Europe’s Single-In Microinverter market is fueled by stringent energy efficiency mandates and the EU’s Green Deal, which targets 40% renewable energy penetration by 2030. Germany, the U.K., and the Netherlands lead adoption, with rooftop solar installations growing at a CAGR of 12%. Microinverters are favored for their performance in shaded or complex roof structures, common in European urban areas. Regulatory pressures to phase out fossil fuels and incentives like tax rebates further drive demand. However, higher upfront costs compared to centralized inverters remain a barrier in price-sensitive markets.

South America

South America is an emerging market, with Brazil and Chile as the primary growth drivers. Brazil’s distributed generation (DG) policies, including net metering exemptions for solar systems under 5 MW, have spurred residential adoption. Chile’s Atacama Desert, with its high solar potential, is attracting commercial-scale projects. However, economic instability and limited financing options slow market penetration. Despite this, the region’s untapped solar potential and gradual policy improvements present long-term opportunities.

Middle East & Africa

The MEA market is nascent but promising, with growth concentrated in the UAE, Saudi Arabia, and South Africa. The UAE’s Dubai Clean Energy Strategy 2050 and Saudi Arabia’s Vision 2030 emphasize solar energy, though large-scale projects currently dominate. Microinverters gain traction in off-grid and hybrid systems across Africa, where modularity and reliability are critical. High temperatures and dust conditions in the region demand robust product designs, creating opportunities for specialized suppliers. However, low awareness and funding gaps hinder rapid adoption.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Single-In Microinverter markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Single-In Microinverter market was valued at USD 2,306 million in 2024 and is projected to reach USD 8,196 million by 2032, growing at a CAGR of 20.4%.

- Segmentation Analysis: Detailed breakdown by product type (Small Power Inverter, High Power Inverter), application (Residential, Commercial), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant. Asia-Pacific dominates due to rapid solar adoption, while North America leads in technological innovation.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of smart monitoring systems, AI-driven optimization, and evolving industry standards for solar energy conversion.

- Market Drivers & Restraints: Evaluation of factors driving market growth (rising solar adoption, government incentives) along with challenges (supply chain constraints, regulatory hurdles).

- Stakeholder Analysis: Insights for component suppliers, solar panel manufacturers, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Single-In Microinverter Market?

-> Single-In Microinverter Market was valued at 2306 million in 2024 and is projected to reach US$ 8196 million by 2032, at a CAGR of 20.4% during the forecast period.

Which key companies operate in Global Single-In Microinverter Market?

-> Key players include Enphase Energy, SolarEdge Technologies, ABB Group, SMA Solar Technology, Hoymiles, APsystems, and Delta Energy Systems, among others.

What are the key growth drivers?

-> Key growth drivers include rising solar energy adoption, government incentives for renewable energy, and demand for module-level monitoring in residential applications.

Which region dominates the market?

-> North America currently leads in market share, while Asia-Pacific is projected as the fastest-growing region due to solar expansion in China and India.

What are the emerging trends?

-> Emerging trends include integration with smart home systems, advanced monitoring software, and higher efficiency microinverters with >96% conversion rates.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...