MARKET INSIGHTS

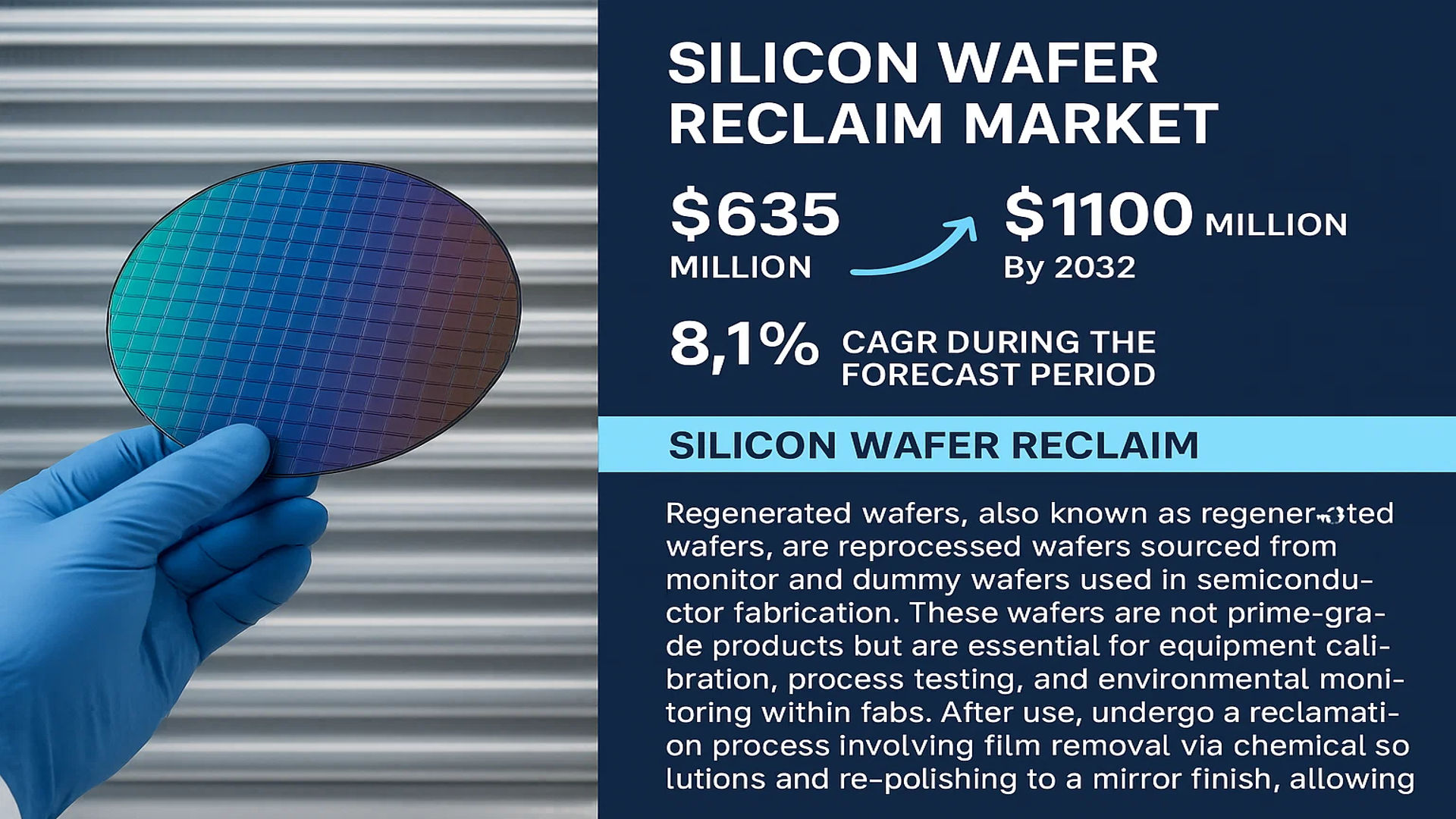

The global Silicon Wafer Reclaim Market was valued at 635 million in 2024 and is projected to reach US$ 1100 million by 2032, at a CAGR of 8.1% during the forecast period.

Silicon Wafer Reclaim, also known as regenerated wafers, are reprocessed wafers sourced from monitor and dummy wafers used in semiconductor fabrication. These wafers are not prime-grade products but are essential for equipment calibration, process testing, and environmental monitoring within fabs. After use, they undergo a reclamation process involving film removal via chemical solutions and re-polishing to a mirror finish, allowing them to be reused multiple times until they fall below the required thickness specifications.

The market is experiencing robust growth driven by the increasing cost pressures in semiconductor manufacturing and the industry’s strong focus on sustainability and waste reduction. The relentless expansion of the global semiconductor industry, particularly in regions like Asia-Pacific, which held over 65% of the market share in 2024, is a primary growth driver. Furthermore, the rising adoption of reclaimed wafers by both Integrated Device Manufacturers (IDMs) and foundries, owing to their significant cost savings of up to 50% compared to new prime wafers, is propelling market expansion. Key players such as RS Technologies, Kinik, and Phoenix Silicon International dominate the market with extensive service portfolios and global reclamation facilities.

MARKET DYNAMICS

MARKET DRIVERS

Rising Semiconductor Production and Cost Efficiency Demands Accelerate Market Adoption

The global semiconductor industry’s relentless expansion, projected to reach $1.4 trillion in annual revenue by 2030, creates unprecedented demand for silicon wafers. With prime wafers costing between $500-$2,000 depending on specifications, semiconductor manufacturers face intense pressure to reduce production costs while maintaining quality standards. Silicon wafer reclaim services address this need by providing high-quality regenerated wafers at approximately 30-50% lower cost than new prime wafers. This substantial cost advantage becomes increasingly critical as semiconductor fabrication facilities (fabs) consume millions of wafers annually for equipment calibration, process monitoring, and testing procedures. The current semiconductor shortage has further intensified focus on operational efficiency, making wafer reclaim services an essential component of cost management strategies across foundries and integrated device manufacturers.

Sustainability Initiatives and Circular Economy Practices Drive Industry Acceptance

Environmental sustainability has become a core business imperative across the semiconductor industry, with major manufacturers committing to carbon neutrality and circular economy principles. The production of virgin silicon wafers involves energy-intensive processes consuming approximately 250-300 kWh per wafer while generating significant carbon emissions. Reclaim processes demonstrate superior environmental performance, requiring only 40-60 kWh per wafer and reducing water consumption by nearly 70%. This environmental advantage aligns with industry-wide sustainability targets and corporate social responsibility commitments. Leading semiconductor companies have incorporated wafer reclaim programs into their environmental management systems, recognizing that each reclaimed wafer prevents the equivalent of 5-7 kg of CO2 emissions compared to new wafer production. The alignment between economic benefits and environmental stewardship creates a powerful driver for market growth as companies seek to demonstrate progress toward sustainability goals while improving operational efficiency.

Technological Advancements in Reclaim Processes Enhance Performance and Reliability

Recent technological innovations in wafer reclaim processes have significantly improved the quality and performance characteristics of regenerated wafers. Advanced polishing techniques now achieve surface roughness measurements below 0.2 nm, rivaling the specifications of prime wafers. Improved cleaning methodologies utilizing megasonic and SCROD technologies ensure particle counts remain below 10 particles per wafer at 0.2μm sensitivity. These advancements have enabled reclaimed wafers to maintain consistent performance through multiple reclaim cycles, with modern processes allowing 5-7 reclamation cycles before wafers reach minimum thickness specifications. The reliability improvements have been particularly notable in advanced node applications, where reclaim wafers now demonstrate defect densities below 0.05/cm², making them suitable for even the most sensitive process monitoring applications. This technological progression has transformed reclaimed wafers from marginal alternatives to trusted components in semiconductor manufacturing workflows.

MARKET CHALLENGES

Technical Limitations in Advanced Node Applications Constrain Market Penetration

While silicon wafer reclaim services have demonstrated excellent performance in mature process technologies, they face significant technical challenges in advanced node applications below 7nm. The extreme precision required for EUV lithography and atomic-layer deposition processes demands wafer specifications that push the limits of reclaim technology. Surface nanotopography requirements below 5nm and wafer flatness specifications exceeding 0.5μm present substantial hurdles for reclaim processes. Additionally, the presence of subsurface damage from previous process cycles can create variability issues in critical dimension control, particularly in finFET and gate-all-around transistor architectures. These technical limitations become more pronounced as the industry progresses toward 3nm and 2nm nodes, where even minor variations in wafer properties can significantly impact yield and device performance.

Other Challenges

Quality Consistency and Performance Variability

Maintaining consistent quality across multiple reclaim cycles presents ongoing challenges for the industry. Each processing cycle introduces potential variations in thickness uniformity, surface roughness, and mechanical properties. The cumulative effect of multiple reclaim cycles can lead to increased wafer bow and warp, particularly for thinner wafers used in advanced packaging applications. This variability requires sophisticated metrology and classification systems, adding complexity and cost to reclaim operations. The industry continues to address these challenges through improved process control and advanced monitoring techniques, but inherent variability remains a constraint for applications requiring extreme consistency.

Supply Chain Complexity and Traceability Requirements

The distributed nature of wafer reclaim operations creates complex logistics and traceability challenges. Wafers may undergo reclaim processing at multiple facilities across different regions, complicating quality assurance and documentation processes. Increasing regulatory requirements for material traceability, particularly in automotive and medical applications, demand sophisticated tracking systems that can maintain chain-of-custody records across multiple reclaim cycles. These requirements add administrative overhead and operational complexity that can offset some of the cost advantages offered by reclaim services.

MARKET RESTRAINTS

Stringent Quality Requirements and Certification Hurdles Limit Market Expansion

The semiconductor industry’s rigorous quality standards present significant barriers to wider adoption of reclaimed wafers. Major semiconductor manufacturers maintain stringent qualification processes that require extensive testing and validation before approving reclaimed wafers for production use. These qualification procedures typically involve multiple lot evaluations, reliability testing, and process compatibility studies that can span 6-12 months. The certification costs, often exceeding $500,000 per technology node, create substantial financial barriers for reclaim service providers. Additionally, the industry’s move toward more specialized wafer types, including silicon-on-insulator and engineered substrates, further complicates the reclaim process and requires development of specialized expertise and equipment. These factors collectively restrain market growth by limiting the speed at which reclaim services can expand into new applications and customer segments.

Volatility in Prime Wafer Pricing Affects Reclaim Service Economics

The economic viability of wafer reclaim services is intrinsically linked to prime wafer pricing, which has demonstrated significant volatility in recent years. Prime wafer prices fluctuated by approximately 25-35% during 2022-2024 due to supply chain disruptions, raw material cost variations, and capacity constraints. This pricing volatility creates challenges for reclaim service providers in maintaining stable pricing models and predictable margins. When prime wafer prices decrease, the cost advantage of reclaimed wafers narrows, reducing their attractiveness to cost-conscious manufacturers. Conversely, during periods of prime wafer shortage, reclaim providers face capacity constraints and increased competition for source materials. This economic sensitivity requires reclaim service providers to maintain flexible business models and sophisticated pricing strategies to navigate market fluctuations effectively.

Limited Availability of Quality Source Materials Constrains Production Capacity

The availability of high-quality monitor and dummy wafers for reclaim processing presents a fundamental constraint on market growth. Not all used wafers are suitable for reclaim processing, with acceptance rates typically ranging from 60-75% depending on previous usage conditions and initial wafer quality. The increasing trend toward thinner wafers and more aggressive process conditions further reduces the pool of reclaimable materials. Additionally, geographic concentration of semiconductor manufacturing creates logistical challenges in collecting and transporting used wafers to reclaim facilities. These factors combine to create a supply-constrained environment where reclaim capacity often cannot keep pace with growing demand, particularly during periods of high semiconductor production volumes.

MARKET OPPORTUNITIES

Expansion into Emerging Semiconductor Applications Creates New Growth Pathways

The rapid growth of new semiconductor applications beyond traditional computing and memory presents significant opportunities for wafer reclaim services. The compound annual growth rate of 15-20% in power semiconductors, RF devices, and MEMS sensors creates substantial demand for cost-effective wafer solutions. These applications often utilize larger wafer sizes (200mm and 300mm) and mature process technologies where reclaim services demonstrate strong technical and economic advantages. The automotive semiconductor market, projected to reach $80 billion by 2030, particularly represents a promising opportunity due to its cost sensitivity and quality requirements that align well with reclaim capabilities. Additionally, the growing silicon carbide and gallium nitride markets offer new avenues for reclaim technology adaptation, though these materials present unique technical challenges that require specialized reclaim processes.

Geographic Expansion and Regional Supply Chain Development Offer Strategic Growth

The ongoing reorganization of global semiconductor supply chains creates substantial opportunities for regional reclaim service expansion. Government initiatives supporting domestic semiconductor capabilities in multiple regions are driving investment in supporting industries, including wafer services. The current geographic concentration of reclaim capacity in established semiconductor regions presents opportunities for development in emerging manufacturing hubs. Regions showing semiconductor industry growth rates exceeding 20% annually represent particularly attractive markets for reclaim service expansion. Additionally, the trend toward regional supply chain resilience reduces logistical costs and improves responsiveness, creating competitive advantages for locally-based reclaim operations. This geographic expansion opportunity is further enhanced by the relatively lower capital requirements for reclaim facilities compared to new wafer manufacturing plants, enabling faster market entry and scalability.

Technology Innovation and Process Integration Enable Value Creation

Continuous innovation in reclaim processes and equipment creates opportunities for enhanced value proposition and market differentiation. Advanced metrology systems incorporating AI and machine learning algorithms enable more precise classification and process optimization, improving yield and quality consistency. Development of specialized reclaim processes for emerging materials and applications allows service providers to capture premium market segments. Integration of reclaim services with other wafer management solutions, including inventory optimization and logistics services, creates opportunities for comprehensive value propositions that address broader customer needs. These innovations enable reclaim service providers to move beyond cost-based competition and develop differentiated offerings based on technical capability, reliability, and service quality.

SILICON WAFER RECLAIM MARKET TRENDS

Sustainability and Cost Efficiency Driving Market Adoption

The global silicon wafer reclaim market is experiencing robust growth, primarily fueled by the semiconductor industry’s relentless pursuit of cost reduction and operational efficiency. With prime wafers representing a significant portion of manufacturing expenses, reclaim services offer substantial savings, often reducing costs by 30% to 50% compared to new prime wafers. This economic advantage is crucial for foundries and Integrated Device Manufacturers (IDMs) operating in highly competitive environments with thin profit margins. Furthermore, the industry’s growing emphasis on sustainability and circular economy principles has elevated the importance of wafer reclamation. By extending the lifecycle of monitor and dummy wafers through multiple reclamation cycles—typically 5 to 7 times before reaching minimum thickness specifications—companies significantly reduce electronic waste and raw material consumption. This trend aligns with global environmental, social, and governance (ESG) initiatives, making wafer reclaim services not just an economic choice but a strategic sustainability imperative for leading semiconductor manufacturers.

Other Trends

Technological Advancements in Reclaim Processes

Recent technological innovations in wafer reclamation processes are significantly enhancing the quality and applicability of reclaimed wafers. Advanced chemical-mechanical polishing (CMP) techniques and ultra-precise metrology systems have improved surface quality to near-prime specifications, with surface roughness measurements now achieving less than 0.2 nm Ra on 300mm wafers. These improvements allow reclaimed wafers to be used in more demanding applications, including advanced process control and equipment calibration for sub-10nm technology nodes. The integration of artificial intelligence and machine learning in reclaim facilities has optimized process parameters in real-time, reducing material loss during polishing and improving overall yield. This technological evolution is critical as semiconductor manufacturing moves toward more advanced nodes where equipment calibration and process monitoring require wafers with increasingly stringent specifications.

Geographic Shift and Supply Chain Resilience

The geographic redistribution of semiconductor manufacturing capacity is creating new opportunities and challenges for the wafer reclaim market. While Taiwan, South Korea, and China dominate semiconductor production, accounting for approximately 65% of global capacity, recent initiatives in North America and Europe to rebuild domestic semiconductor capabilities are driving demand for local reclaim services. The U.S. CHIPS and Science Act has catalyzed significant investments in domestic semiconductor manufacturing, with projections indicating that U.S.-based wafer reclaim capacity will need to expand by approximately 40% to support new fabrication facilities. This geographic diversification is reducing reliance on Asian supply chains and creating a more resilient ecosystem. Additionally, the increasing complexity of semiconductor manufacturing processes, particularly with the adoption of extreme ultraviolet (EUV) lithography and 3D packaging technologies, requires more frequent equipment monitoring and calibration, thereby driving higher consumption of monitor wafers and subsequently increasing the volume of wafers available for reclamation.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Focus on Technological Advancements and Geographic Expansion to Secure Market Position

The global silicon wafer reclaim market exhibits a semi-consolidated competitive structure, characterized by the presence of several established players alongside numerous regional and specialized participants. RS Technologies is recognized as a dominant force, largely due to its extensive production capabilities, technological expertise in wafer reclamation processes, and a robust global supply chain that serves major semiconductor hubs in Asia, North America, and Europe.

Kinik and Phoenix Silicon International also command significant market shares, a position bolstered by their strong relationships with leading foundries and Integrated Device Manufacturers (IDMs). Their growth is further driven by continuous investments in advanced polishing and cleaning technologies, which enhance wafer quality and extend the usable life of reclaimed products.

Furthermore, strategic initiatives such as capacity expansions, partnerships with semiconductor fabrication plants, and the development of proprietary reclamation techniques are pivotal strategies these companies employ to capture a larger portion of the market. These efforts are crucial as the demand for cost-effective monitor and dummy wafers continues to rise alongside global semiconductor production.

Meanwhile, other key players like Hamada Rectech and Mimasu Semiconductor Industry are strengthening their positions through focused research and development aimed at improving yield rates and reducing the environmental impact of the reclamation process. Their commitment to sustainability and operational efficiency resonates with the industry’s growing emphasis on circular economy practices, providing a competitive edge.

List of Key Silicon Wafer Reclaim Companies Profiled

- RS Technologies (Japan)

- Kinik (Taiwan)

- Phoenix Silicon International (Taiwan)

- Hamada Rectech (Japan)

- Mimasu Semiconductor Industry (Japan)

- GST (China)

- Scientech (U.S.)

- Pure Wafer (U.K.)

- TOPCO Scientific Co. LTD (Taiwan)

- Ferrotec (U.S.)

- Xtek semiconductor (Huangshi) (China)

- Shinryo (Japan)

- KST World (South Korea)

- Vatech Co., Ltd. (South Korea)

- OPTIM Wafer Services (Germany)

Segment Analysis:

By Type

Monitor Wafers Segment Dominates the Market Due to High Frequency of Equipment Calibration and Testing

The market is segmented based on type into:

- Monitor Wafers

- Dummy Wafers

By Application

Foundry Segment Leads Due to Extensive Semiconductor Manufacturing and Process Optimization Needs

The market is segmented based on application into:

- IDM (Integrated Device Manufacturers)

- Foundry

- Others

By Wafer Size

300mm Wafers Hold Significant Share Owing to Their Dominance in Advanced Semiconductor Fabrication

The market is segmented based on wafer size into:

- 200mm

- 300mm

- Others

By Reclaim Process

Chemical Mechanical Polishing (CMP) is the Predominant Process for Achieving Required Surface Finish

The market is segmented based on reclaim process into:

- Chemical Mechanical Polishing (CMP)

- Etching

- Others

Regional Analysis: Silicon Wafer Reclaim Market

Asia-Pacific

The Asia-Pacific region dominates the global silicon wafer reclaim market, accounting for over 60% of global consumption volume. This leadership position is driven by the region’s massive semiconductor manufacturing capacity, particularly in Taiwan, South Korea, and China. The region benefits from extensive foundry operations from companies like TSMC and Samsung, which generate substantial volumes of monitor and dummy wafers requiring reclamation. China’s semiconductor industry expansion, supported by government initiatives like the “Made in China 2025” policy, has significantly increased demand for cost-effective reclaimed wafers. While Japan maintains advanced reclamation technologies through companies like Mimasu Semiconductor Industry, cost sensitivity across the region makes reclaimed wafers particularly attractive for equipment testing and process monitoring applications. The concentration of semiconductor fabrication facilities creates a robust ecosystem for wafer reclamation services, with both local and international players establishing operations throughout the region.

North America

North America represents a mature but steadily growing market for silicon wafer reclaim services, characterized by high technological standards and stringent quality requirements. The United States, home to major IDMs like Intel and GlobalFoundries, maintains significant reclaim wafer demand for process monitoring and equipment calibration. The region’s market is distinguished by its focus on advanced reclamation technologies that can handle increasingly complex wafer structures, including those with advanced node geometries. Environmental regulations and sustainability initiatives have driven adoption of reclaim services as semiconductor manufacturers seek to reduce waste and improve resource efficiency. Recent investments in domestic semiconductor manufacturing through legislation such as the CHIPS and Science Act are expected to further boost demand for reclaim services as new fabrication facilities come online and require monitor wafers for equipment qualification and process monitoring.

Europe

Europe maintains a technologically advanced silicon wafer reclaim market focused on high-quality standards and environmental sustainability. The region’s strong automotive and industrial semiconductor sectors, particularly in Germany and France, generate consistent demand for reclaimed wafers used in process control and equipment maintenance. European semiconductor manufacturers emphasize circular economy principles, making wafer reclamation an integral part of their sustainability strategies. Strict environmental regulations under the EU’s Waste Electrical and Electronic Equipment directive encourage proper handling and recycling of semiconductor materials, including silicon wafers. The presence of research institutions and equipment manufacturers supports innovation in reclamation processes, particularly for specialized wafer types used in power semiconductors and MEMS applications. While the market is smaller than Asia-Pacific in volume terms, it commands premium pricing for high-quality reclaim services.

South America

The South American silicon wafer reclaim market remains in its early development stages, characterized by limited local semiconductor manufacturing capacity. Brazil represents the most significant market in the region, primarily serving the automotive and consumer electronics industries. Most reclaim activities are handled by international service providers rather than local specialized companies. The market faces challenges related to infrastructure limitations and the relatively small size of the semiconductor industry compared to other regions. However, growing electronics manufacturing and gradual industrialization present opportunities for market development. Economic volatility and currency fluctuations sometimes hinder investment in reclamation infrastructure, but the fundamental cost advantages of using reclaimed wafers continue to drive interest among the region’s limited semiconductor operations.

Middle East & Africa

The Middle East and Africa region represents an emerging market for silicon wafer reclaim services, with very limited local semiconductor manufacturing capacity. Israel stands as an exception, with a developed high-tech sector that includes semiconductor design and limited manufacturing activities. The region primarily depends on imported reclaimed wafers or services provided by international companies. While there is growing recognition of the economic and environmental benefits of wafer reclamation, the lack of substantial semiconductor fabrication infrastructure limits market size. Some countries in the Gulf region are making strategic investments in technology sectors, which could eventually lead to increased demand for reclaim services. However, the market currently remains niche and served primarily through international supply chains rather than local reclamation operations.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Silicon Wafer Reclaim markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Silicon Wafer Reclaim Market?

-> Silicon Wafer Reclaim Market was valued at 635 million in 2024 and is projected to reach US$ 1100 million by 2032, at a CAGR of 8.1% during the forecast period.

Which key companies operate in Global Silicon Wafer Reclaim Market?

-> Key players include RS Technologies, Kinik, Phoenix Silicon International, Hamada Rectech, and Mimasu Semiconductor Industry, among others.

What are the key growth drivers?

-> Key growth drivers include rising semiconductor manufacturing activity, cost-efficiency of reclaimed wafers, and sustainability initiatives in electronics production.

Which region dominates the market?

-> Asia-Pacific is the dominant market, driven by semiconductor manufacturing hubs in China, Taiwan, South Korea, and Japan.

What are the emerging trends?

-> Emerging trends include advanced reclamation technologies for thinner wafers, increased adoption in foundries, and integration with Industry 4.0 manufacturing processes.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...