MARKET INSIGHTS

Silicon Photonics Wafer Foundry Service Market refers to the specialized manufacturing services that create optical and electronic components directly on silicon wafers. In short, it’s the intersection of light-based communication and semiconductor manufacturing, enabling chips to transmit data faster, while consuming less power, to meet the ever-growing demands of cloud computing, AI infrastructure, telecom networks, and next-generation sensing applications.

This differs from a standard electronic chip foundry that only deals with electrical signals. A silicon photonics foundry deals with materials, process methods and device topologies designed to guide and manipulate light at wafer scale. This makes the market particularly important for sectors that require small, fast and energy efficient data transport.

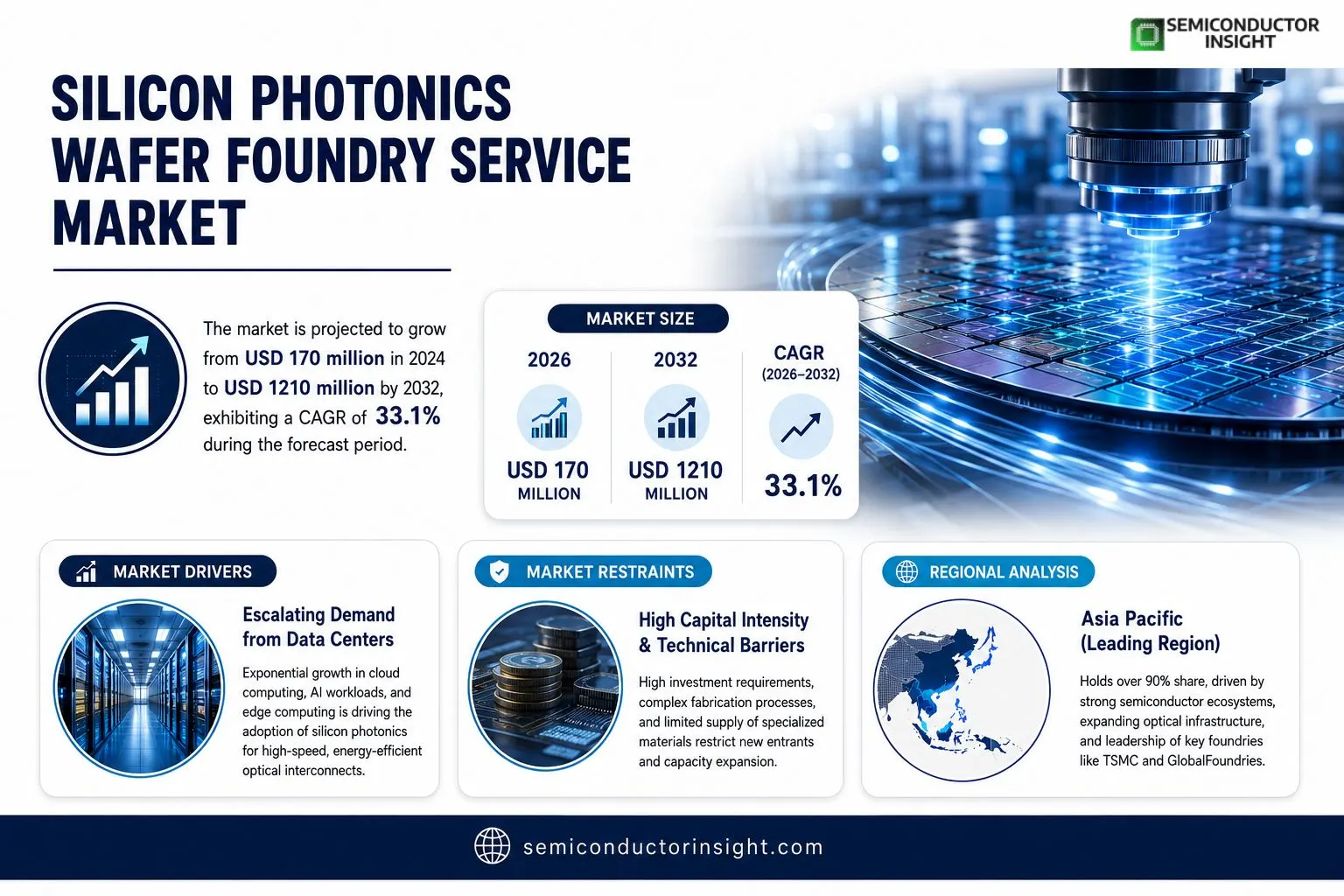

- Accounted for USD 170 million in 2024

- Likely to exceed USD 1210 million by 2032

- Reflecting a compound annual growth rate (CAGR) of 1%

The traditional approach of using purely electrical interconnects to move data is hitting its limits as digital systems get larger and more power hungry. And that’s where silicon photonics comes in. It keeps the standard silicon manufacturing base, but adds the ability to transmit information using photons instead of being limited to electrons.

This is important for businesses because it opens the door for faster communications, lower heat generation and better scalability for data centers, AI hardware, and high-performance computing and next-generation telecom systems. It generates a very specialized service market for precision and repeatability and advanced wafer processing for foundries.

Key Takeaways:

- Data centers remain the core application, supported by the growing need for faster optical links, lower latency, and power-efficient communication.

- Telecommunications holds a major end-user share, with 5G rollouts, cloud expansion, and bandwidth-heavy networks strengthening demand.

Asia Pacific leads the regional landscape, backed by strong semiconductor manufacturing capacity, expanding optical infrastructure, and faster adoption of advanced wafer foundry services

MARKET DYNAMICS

MARKET DRIVERS

Escalating Demand from Data Centers to Accelerate Market Expansion

Silicon photonics wafer foundry services are experiencing robust growth driven by surging demand from hyperscale data centers requiring high-bandwidth optical interconnects. The exponential rise in cloud computing, AI workloads, and edge computing has created unprecedented needs for energy-efficient photonics solutions. Data centers globally are transitioning from traditional copper interconnects to silicon photonics-based solutions capable of handling 800Gbps and 1.6Tbps transmission speeds. This transition is fueled by silicon photonics’ superior performance metrics – offering 100x higher bandwidth density while consuming 50% less power compared to conventional solutions. Market projections indicate that silicon photonics adoption in data center interconnects will grow at over 40% CAGR through 2030, directly benefiting wafer foundry service providers.

Advancements in Heterogeneous Integration to Drive Technological Innovation

The silicon photonics ecosystem is being transformed by breakthroughs in heterogeneous integration technologies. Leading foundries are now offering advanced co-packaged optics solutions that combine silicon photonics dies with electronic ICs in 2.5D/3D configurations. This integration leap enables unprecedented performance in datacom and telecom applications while reducing package footprints by 70%. Recent developments include TSMC’s 300mm silicon photonics platform achieving wafer-scale integration with 7nm CMOS logic, demonstrating production yields exceeding 90%. Such innovations are crucial for meeting the performance demands of next-generation computing architectures and 5G/6G infrastructure. Furthermore, the ability to leverage existing semiconductor manufacturing infrastructure gives silicon photonics a significant edge vs alternative photonic integration approaches.

MARKET RESTRAINTS

High Capital Intensity and Technical Barriers Limit Market Entry

The silicon photonics wafer foundry sector faces significant entry barriers due to extraordinary capital requirements and specialized technical expertise needed. Establishing a production-grade silicon photonics foundry requires investments exceeding $1 billion for a 300mm facility with process capabilities below 45nm. Additionally, the intellectual property landscape is dominated by a few established players controlling over 200 key patents in silicon photonics design and manufacturing. New entrants must navigate complex technology transfer challenges while achieving production yields comparable to incumbent foundries (typically 70-90% for mature processes). This creates substantial risk for potential competitors considering market entry, reinforcing the oligopolistic nature of the industry where the top three players control 97% of revenue share.

Supply Chain Vulnerabilities

Silicon photonics manufacturing relies on specialized substrate materials and equipment facing supply constraints. The industry depends on ultra-low-loss silicon-on-insulator (SOI) wafers with stringent thickness uniformity requirements (±1% across 300mm wafers). Supply of these substrates remains concentrated with just two suppliers controlling over 80% of the global SOI wafer market. Similarly, critical deposition and etching equipment customized for photonics applications faces lead times exceeding 12 months. These supply chain bottlenecks create production uncertainty and limit capacity expansion potentials despite growing demand.

MARKET CHALLENGES

Design-Process Co-optimization Complexity Increases Development Costs

Silicon photonics product development presents unique challenges in design-process co-optimization due to tight coupling between device performance and fabrication parameters. Unlike conventional IC design where standardized PDKs (Process Development Kits) exist, photonics designers must account for nanometer-scale variations in waveguide dimensions that can alter optical properties by 10-15%. This requires extensive characterization and modeling efforts, increasing typical design cycles to 12-18 months versus 6-9 months for comparable electronic ICs. Furthermore, foundries must maintain specialized process control for features like sidewall roughness (<2nm RMS) and etch depth uniformity (±3nm) that have minimal impact in conventional semiconductor manufacturing but critically affect optical device performance.

Test and Packaging Bottlenecks

Final test and packaging account for 40-60% of total silicon photonics product costs—far higher than electronic ICs—creating significant cost challenges. Fiber alignment tolerances below 500nm require specialized active alignment equipment costing $1-2 million per unit. Additionally, thermal management challenges in co-packaged optics solutions demand novel materials and assembly techniques still in development. These factors contribute to package costs often exceeding $100 per unit, hindering adoption in price-sensitive applications.

MARKET OPPORTUNITIES

Emerging Applications in LiDAR and Biomedical Sensing to Open New Frontiers

Beyond datacom applications, silicon photonics is poised to disrupt multiple high-growth sectors including automotive LiDAR and biomedical sensing. The LiDAR market is transitioning from bulky mechanical systems to solid-state solutions where silicon photonics enables compact, reliable designs suitable for mass-market automotive integration. Emerging frequency-modulated continuous wave (FMCW) LiDAR architectures benefit particularly from integrated photonics, with performance metrics showing 10x improvement in resolution compared to conventional time-of-flight systems. Similarly, in biomedical applications, silicon photonics biosensors demonstrate detection limits below 1pg/mm² for label-free molecular diagnostics—performance comparable to gold-standard techniques but at significantly lower cost and with potential for disposable use.

Government Investments in Photonics Ecosystems to Accelerate Market Growth

National photonics initiatives are creating favorable conditions for silicon photonics foundry expansion globally. Several governments have recognized photonics as a critical technology area, with dedicated funding programs exceeding $2 billion collectively. These initiatives aim to establish complete photonics value chains encompassing design tools, fabrication facilities, and packaging infrastructure. Such investments are particularly crucial for bridging the “valley of death” between research prototypes and volume manufacturing—a significant challenge for emerging photonics companies. The resulting ecosystem development will enable broader access to advanced fabrication capabilities beyond the current leading-edge foundries.

SILICON PHOTONICS WAFER FOUNDRY SERVICE MARKET TRENDS

Exponential Growth in Data Center Applications Fuels Market Expansion

The silicon photonics wafer foundry service market is experiencing unprecedented growth, primarily driven by the increasing demand for high-speed data transmission in hyperscale data centers. With cloud computing and AI workloads requiring bandwidths exceeding 400G per port, silicon photonics has emerged as the preferred solution due to its superior performance and energy efficiency compared to traditional electrical interconnects. The global market, valued at 170 million in 2024, is projected to expand at a CAGR of 33.1% through 2032, reaching an estimated value of 1,210 million. This growth is further propelled by the need for low-latency communication in emerging applications such as machine learning and high-performance computing. Foundries are responding with capacity expansions, with leading players TSMC and GlobalFoundries allocating significant portions of their advanced packaging budgets to photonic integrated circuits (PICs).

Other Trends

Technological Convergence Driving Hybrid Integration

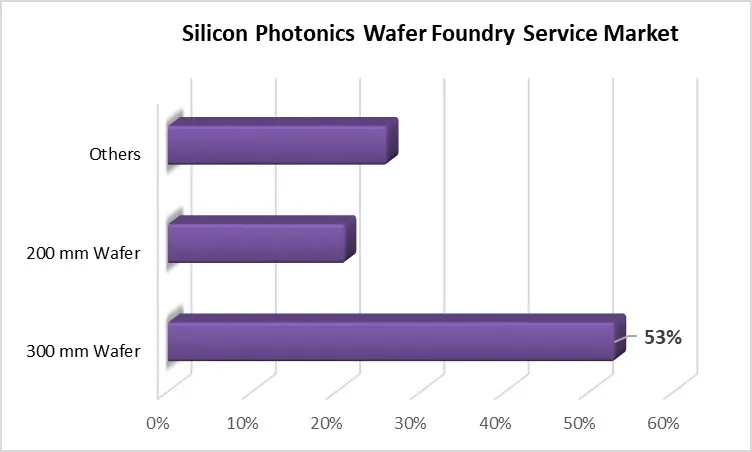

The semiconductor industry is witnessing a paradigm shift toward heterogeneous integration of electronic and photonic components on single substrates. This trend is accelerating the adoption of silicon photonics wafer foundry services, as designers seek to combine the strengths of CMOS electronics with optical communication capabilities. Foundries are increasingly offering multi-project wafer (MPW) services to lower the entry barrier for photonics startups and research institutions, with 300mm wafer processing now accounting for over 60% of production capacity. Recent breakthroughs in co-packaged optics (CPO) architectures are further blurring the lines between electronic and photonic integration, requiring foundries to develop novel processes that can simultaneously handle both technologies without compromising yield or performance.

Regional Consolidation and Supply Chain Evolution

The silicon photonics wafer foundry market exhibits an unusually concentrated supply chain, with three dominant players controlling 97% of global revenue. TSMC maintains market leadership with 68% share, capitalizing on its advanced packaging expertise to offer seamless integration of photonic and electronic components. Meanwhile, GlobalFoundries’ 26% market share reflects its strong position in high-volume manufacturing for data center applications. This consolidation is driving smaller players to specialize in niche applications such as LiDAR and biomedical sensing, where standard manufacturing processes may not suffice. The geographic concentration of production capacity in Asia-Pacific creates both opportunities and challenges—while benefiting from established semiconductor ecosystems, the industry remains vulnerable to regional disruptions and trade tensions that could impact the global photonics supply chain.

COMPETITIVE LANDSCAPE

Key Industry Players

Foundries Accelerate Innovation to Meet Surging Demand for Silicon Photonics Solutions

The global silicon photonics wafer foundry service market exhibits a highly concentrated competitive structure, dominated by a handful of semiconductor manufacturing giants. TSMC leads the market with an impressive 68.08% revenue share in 2022, leveraging its advanced 300mm wafer fabrication capabilities and strategic partnerships with major data center operators. The company’s dominance stems from its ability to deliver high-volume production while maintaining precision for photonic integrated circuits.GlobalFoundries follows as the second-largest player, capturing 26.75% market share through its specialized 200mm Silicon Photonics platform. The foundry has strengthened its position by focusing on emerging applications beyond data centers, including automotive LiDAR and healthcare photonics. Meanwhile, Silex Microsystems maintains a niche presence with 2.29% share, specializing in MEMS-based photonic solutions for specialized applications.Recent industry developments highlight intense competition. TSMC announced plans to expand its silicon photonics capacity by 40% in 2024 to meet growing AI infrastructure demands, while GlobalFoundries secured a $3.5 billion contract with a leading cloud provider for next-generation photonic wafers. These moves underscore how foundries are racing to scale production while advancing process technologies.Smaller players like Tower Semiconductor and Advanced Micro Foundry are pursuing differentiation through customized solutions and hybrid integration approaches. The European ecosystem, represented by VTT and IHP Microelectronics, focuses on R&D-intensive low-volume production, particularly for quantum photonics applications.

List of Key Silicon Photonics Wafer Foundry Service Providers

- TSMC (Taiwan)

- GlobalFoundries (U.S.)

- Silex Microsystems (Sweden)

- Tower Semiconductor (Israel)

- Advanced Micro Foundry (Singapore)

- VTT Technical Research Centre (Finland)

- SilTerra (Malaysia)

- IHP Microelectronics (Germany)

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

300 mm wafer segment dominates the Silicon Photonics Wafer Foundry Service Market because it enables high-volume manufacturing, lower production costs per chip, and seamless compatibility with advanced CMOS fabrication facilities.

As silicon photonics moves from research laboratories into commercial deployment for AI data centres, cloud computing, high-speed optical transceivers, and telecommunications, foundries increasingly rely on 300 mm wafer platforms to maximise throughput while maintaining tight process control and consistent device performance. |

| By Application |

|

Data center segment dominates the Silicon Photonics Wafer Foundry Service Market because hyperscale cloud operators and enterprise data centers are rapidly adopting silicon photonics-based optical interconnects to handle the unprecedented growth in digital traffic.

Traditional copper-based connections struggle to deliver the bandwidth, energy efficiency, and transmission speeds required for AI clusters, cloud computing, high-performance computing (HPC), and large-scale storage networks. |

| By End-User |

|

In order to handle the explosive growth of internet traffic, AI workloads, 5G connectivity, and hyperscale data transmission, global network operators and cloud service providers are rapidly expanding high-speed optical communication infrastructure, which is why the telecommunications segment dominates the Silicon Photonics Wafer Foundry Service Market.

Silicon photonics is the ideal platform for next-generation telecom networks because it allows for quicker, more affordable, and lower-power optical transceivers than traditional technologies. |

After Segment Table

Regional Analysis: Silicon Photonics Wafer Foundry Service Market

North America

The North American region, led by the U.S., is a significant hub for silicon photonics wafer foundry services, driven by strong demand from data centers, telecom infrastructure, and advanced computing applications. With the CHIPS and Science Act allocating $52 billion to strengthen domestic semiconductor manufacturing capabilities, investments in photonics integration are accelerating. The U.S. boasts mature foundry ecosystems (e.g., GlobalFoundries), but reliance on Asia-based giants like TSMC remains due to their superior fabrication capabilities. While North America has a growing R&D focus on photonics, scaling up localized production remains a challenge because of high operational costs and competition for semiconductor talent.

Europe

Europe maintains a robust research-driven approach to silicon photonics, with key players like IHP Microelectronics and VTT advancing specialized foundry services. The EU’s Horizon Europe program has prioritized photonics innovation, particularly for applications in quantum computing and medical devices. However, despite strong technological expertise, Europe’s foundry market remains fragmented compared to Asia-Pacific, with smaller-scale production facilities dominating. Partnerships with Asian foundries are common due to limitations in high-volume manufacturing. Environmental regulations also influence adoption, pushing the development of low-energy photonics solutions.

Asia-Pacific

The Asia-Pacific region dominates the global silicon photonics wafer foundry market, with over 97% market share controlled by TSMC, GlobalFoundries, and Silex Microsystems. Taiwan’s TSMC is the clear leader, leveraging its advanced semiconductor infrastructure for photonics integration. China and Japan are aggressively expanding domestic foundry capabilities to reduce reliance on foreign suppliers—programs like China’s “Big Fund” aim to strengthen local semiconductor self-sufficiency. The region benefits from high-volume demand driven by hyperscale data centers and government-backed 5G deployments, making it the epicenter for both fabrication and end-use consumption.

South America

South America’s participation in the silicon photonics wafer foundry market is minimal, largely due to limited semiconductor infrastructure and investment constraints. Brazil and Argentina show nascent interest in photonics R&D for niche applications in agriculture and healthcare sensors, but a lack of scale-up capabilities restricts commercial foundry development. Most regional demand is met through imports from U.S. or Asia-based suppliers. However, with increasing digital transformation initiatives, particularly in Brazil, long-term opportunities may emerge for localized low-volume production.

Middle East & Africa

The Middle East & Africa region is in the early stages of silicon photonics adoption, with investments focused on data center expansions in Gulf Cooperation Council (GCC) countries like the UAE and Saudi Arabia. Saudi Arabia’s Vision 2030 plan has identified semiconductor and photonics technologies as growth areas, though local foundry services remain underdeveloped. Africa’s market is constrained by limited infrastructure, but select nations (e.g., South Africa) are exploring photonics for telecommunications. The region largely depends on imported wafer solutions, with slow but steady growth anticipated from smart city initiatives and connectivity projects.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Silicon Photonics Wafer Foundry Service markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Silicon Photonics Wafer Foundry Service market was valued at USD 170 million in 2024 and is projected to reach USD 1210 million by 2032, growing at a CAGR of 33.1% during the forecast period.

- Segmentation Analysis: Detailed breakdown by wafer size (300mm, 200mm, Others), application (Data Center, Non-Data Center), and end-user industry to identify high-growth segments and investment opportunities. In 2024, 300mm wafers accounted for the largest market share due to higher production efficiency.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. Asia-Pacific dominates the market with over 90% of production capacity concentrated in this region.

- Competitive Landscape: Profiles of leading market participants including TSMC (68.08% market share), GlobalFoundries (26.75%), and Silex Microsystems (2.29%), covering their product offerings, R&D focus, manufacturing capacity expansion plans, and recent developments.

- Technology Trends & Innovation: Assessment of hybrid integration techniques, co-packaged optics, AI-optimized photonic designs, and advanced fabrication methods enabling higher yield rates and lower costs.

- Market Drivers & Restraints: Evaluation of factors such as rising demand for high-speed data transmission in data centers versus challenges like high initial capital investment and complex fabrication processes.

- Stakeholder Analysis: Strategic insights for photonic IC designers, foundry service providers, system integrators, and investors regarding the evolving value chain and partnership opportunities.

The research methodology combines primary interviews with industry experts and analysis of verified market data from financial reports, trade associations, and government publications to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Silicon Photonics Wafer Foundry Service Market?

->Silicon Photonics Wafer Foundry Service Market was valued at 170 million in 2024 and is projected to reach US$ 1210 million by 2032, at a CAGR of 33.1% during the forecast period.

Which key companies operate in Global Silicon Photonics Wafer Foundry Service Market?

-> Key players include TSMC, GlobalFoundries, Silex Microsystems, Tower Semiconductor, Advanced Micro Foundry, VTT, SilTerra, and IHP Microelectronics.

What are the key growth drivers?

-> Key growth drivers include exploding data center traffic, adoption of co-packaged optics, and increasing demand for high-bandwidth communication systems.

Which region dominates the market?

-> Asia-Pacific dominates the market with over 90% production share, led by Taiwan (TSMC) and Singapore (GlobalFoundries).

What are the emerging trends?

-> Emerging trends include heterogeneous integration of photonics with CMOS, AI-optimized photonic designs, and increasing adoption of 300mm wafer platforms.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...