MARKET INSIGHTS

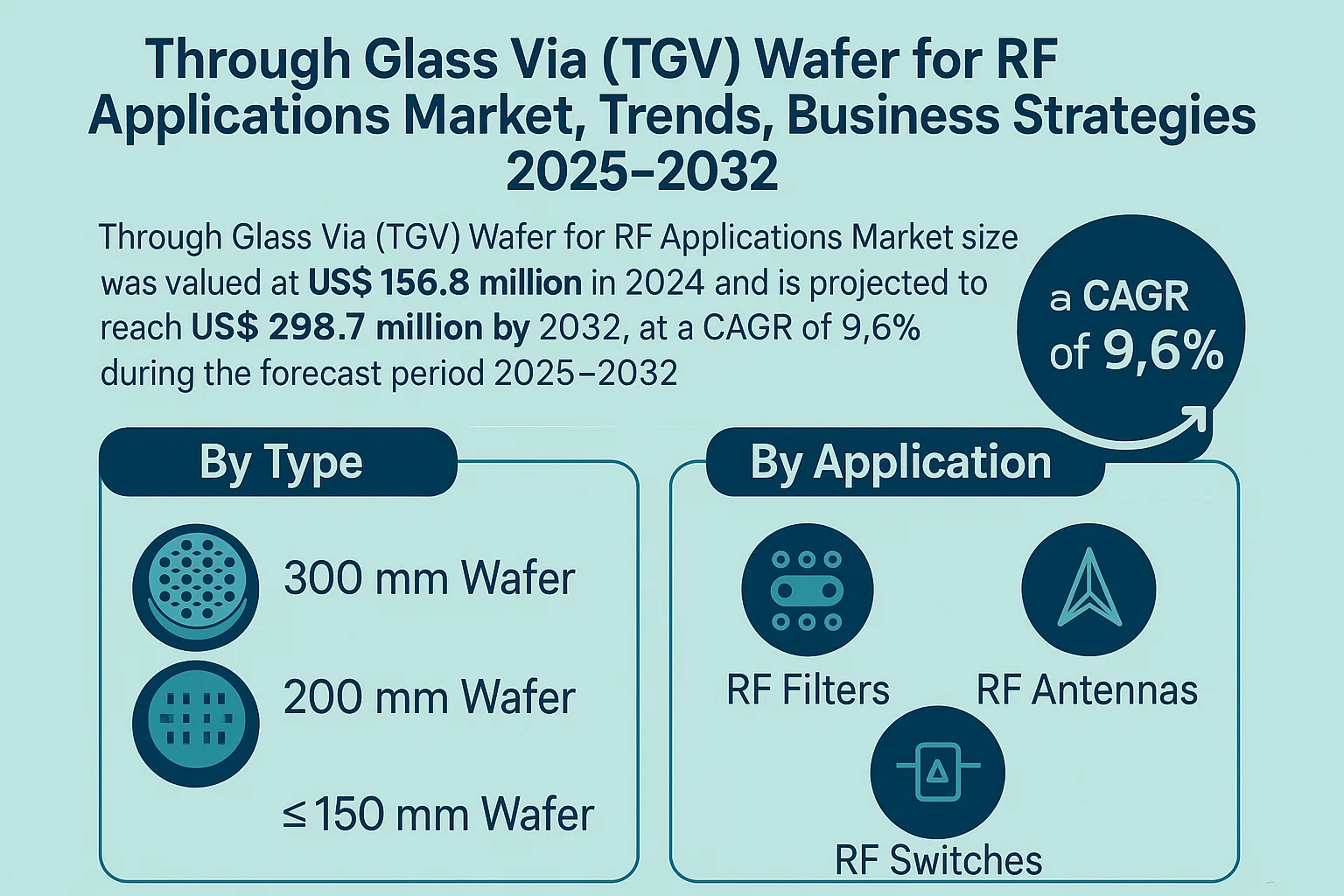

The global Through Glass Via (TGV) Wafer for RF Applications Market size was valued at US$ 156.8 million in 2024 and is projected to reach US$ 298.7 million by 2032, at a CAGR of 9.6% during the forecast period 2025-2032. This growth aligns with broader semiconductor industry trends, which saw a 4.4% expansion to USD 580 billion in 2022 despite macroeconomic challenges.

Through Glass Via (TGV) wafers are specialized glass substrates featuring vertical electrical interconnects, enabling high-frequency signal transmission with minimal loss—a critical requirement for 5G and advanced RF applications. These wafers come in varying diameters (150mm, 200mm, and 300mm) and find applications in RF filters, antennas, switches, and front-end modules. Their superior thermal stability and low dielectric loss make them preferable to traditional silicon-based solutions in high-frequency scenarios.

The market is driven by accelerating 5G infrastructure deployment, which demands higher performance RF components. While the Americas and Europe showed strong semiconductor growth (17% and 12.6% respectively in 2022), Asia-Pacific remains the dominant region for TGV adoption due to concentrated electronics manufacturing. Recent developments include Corning’s 2023 expansion of TGV production capacity to meet rising demand from smartphone and IoT device manufacturers. Other key players like LPKF and Samtec are investing in laser-based via formation technologies to improve yield rates.

MARKET DYNAMICS

MARKET DRIVERS

5G Network Expansion Accelerates Demand for Advanced RF Components

The global rollout of 5G networks continues to drive substantial demand for Through Glass Via (TGV) wafers in RF applications. With 5G infrastructure requiring higher frequency operations and improved signal integrity, TGV technology offers superior performance over traditional silicon solutions. Current estimates indicate over 1.7 billion 5G subscribers worldwide as telecom operators invest heavily in network upgrades. This creates a direct demand for TGV wafers used in RF filters, antennas, and front-end modules that can handle higher frequencies with minimal signal loss. Leading manufacturers are expanding production capacities to meet this surging demand, with several new fabrication facilities announced recently to support 5G component production.

Miniaturization Trend in Electronics Boosts TGV Adoption

The relentless push for smaller, more compact electronic devices is creating significant opportunities for TGV wafer technology. Unlike conventional interconnects, TGVs enable vertical integration while maintaining excellent RF performance, making them ideal for space-constrained applications. The mobile device sector, representing over 60% of RF component demand, requires increasingly compact solutions without compromising performance. TGV wafers provide the necessary combination of high-frequency operation, thermal stability, and dimensional scalability that next-generation smartphones and IoT devices demand. Recent product launches incorporating TGV-based RF modules demonstrate the technology’s growing acceptance in mainstream consumer electronics.

Automotive Radar and Connectivity Fuels Specialty Wafer Demand

Advancements in automotive technology, particularly in advanced driver assistance systems (ADAS) and vehicle-to-everything (V2X) communication, are generating new applications for TGV wafers. The automotive RF component market is projected to grow substantially as autonomous features become standard, requiring reliable high-frequency signal processing. TGV wafers offer distinct advantages in these applications due to their excellent thermal properties and signal integrity at millimeter-wave frequencies. With over 50 million vehicles expected to incorporate level 2+ autonomy features by 2025, the demand for specialized RF solutions utilizing TGV technology will continue its upward trajectory.

MARKET RESTRAINTS

High Manufacturing Costs Limit Widespread Adoption

While TGV wafer technology offers superior performance characteristics, its adoption faces significant cost-related challenges. The specialized processing equipment and highly controlled manufacturing environments required for TGV production result in substantially higher costs compared to conventional silicon-based solutions. Current estimates suggest TGV wafer costs are approximately 30-40% higher than standard alternatives, creating a barrier to entry for cost-sensitive applications. This price differential has restricted TGV usage primarily to high-performance segments where the benefits justify the premium, delaying broader market penetration.

Technical Complexity in Mass Production Creates Bottlenecks

The sophisticated manufacturing processes required for TGV wafers present significant technical challenges in achieving high-volume production. Precise via formation in glass substrates, metallization processes, and thermal management considerations require advanced equipment and skilled operators. These complexities have resulted in relatively low yield rates compared to traditional wafer technologies, further exacerbating cost pressures. As the industry works to optimize production methods, the current limitations in manufacturing scalability represent a key restraint on market growth.

Material Limitations Challenge Performance Boundaries

While glass substrates offer numerous advantages for RF applications, certain material properties present inherent limitations. The brittle nature of glass complicates handling during fabrication and packaging processes, potentially reducing yields. Additionally, while superior to silicon for many RF applications, glass substrates must continually improve to meet the escalating performance requirements of next-generation communication systems. Research into advanced glass formulations and hybrid approaches continues, but current material constraints remain a limiting factor for the most demanding applications.

MARKET OPPORTUNITIES

Emerging 6G Research Creates Future Growth Potential

The nascent development of 6G wireless technology presents significant long-term opportunities for TGV wafer manufacturers. Early research indicates that 6G systems will operate at even higher frequencies than 5G, potentially into the sub-terahertz range. This performance requirement plays directly to the strengths of TGV technology, which maintains excellent signal integrity at these extreme frequencies. Major technology firms and research institutions are already investing in 6G component development, with TGV-based solutions positioned as leading candidates for future RF front-end implementations.

Medical Imaging Advancements Open New Application Verticals

The healthcare sector represents a promising growth area for TGV wafer technology, particularly in advanced medical imaging systems. Emerging diagnostic techniques using high-frequency electromagnetic waves require components with precise signal handling capabilities. The combination of excellent RF performance and biocompatibility makes TGV technology attractive for next-generation medical devices. Recent prototypes of compact imaging systems demonstrate the potential for TGV-based solutions in portable diagnostic equipment, an area projected to experience strong growth as healthcare becomes more decentralized.

Automotive Innovation Drives Specialized Market Segments

Beyond conventional RF applications, the automotive industry’s electrification and autonomy trends are creating specialized opportunities for TGV technology. High-performance sensors, LiDAR systems, and vehicle communication networks increasingly require components that can operate reliably in harsh environmental conditions. TGV wafers’ thermal stability and vibration resistance make them well-suited for these demanding applications. As automotive manufacturers accelerate their investments in next-generation vehicle technologies, specialized TGV-based components are positioned to capture a growing share of this high-value market.

MARKET CHALLENGES

Supply Chain Vulnerabilities Impact Production Stability

The TGV wafer manufacturing process relies on specialized materials and equipment from a limited number of global suppliers. Recent disruptions in the semiconductor supply chain have highlighted the vulnerability of this concentrated supply network. Certain critical materials used in TGV production, including high-purity glass substrates and specialized metallization compounds, face periodic shortages. These supply constraints create production bottlenecks and cost fluctuations that challenge manufacturers’ ability to maintain stable output and pricing.

Technology Competition from Alternative Solutions

TGV technology faces ongoing competitive pressure from alternative approaches to high-frequency RF component design. Advanced packaging techniques using silicon and compound semiconductors continue to evolve, narrowing the performance gap with TGV solutions in certain applications. Additionally, emerging technologies like integrated photonics present potential long-term competition in specific high-frequency applications. While TGVs maintain distinct advantages in many use cases, the rapid pace of innovation in competing technologies requires continuous improvement to maintain market position.

Standardization and Qualification Hurdles Delay Market Entry

The relatively recent introduction of TGV technology means industry standards and qualification processes are still evolving. Many potential customers require extensive reliability testing and lengthy qualification procedures before adopting new component technologies. The absence of established industry-wide standards for TGV-based components can prolong this qualification process, delaying product adoption cycles. Additionally, differing requirements across application sectors and geographic markets create further complexity in achieving broad market acceptance.

THROUGH GLASS VIA (TGV) WAFER FOR RF APPLICATIONS MARKET TRENDS

5G Network Expansion Drives Growth in TGV Wafer Demand

The rapid global rollout of 5G networks is significantly increasing demand for Through Glass Via (TGV) wafers in radio frequency (RF) applications. With 5G requiring higher frequency bands between 24 GHz and 100 GHz, TGV technology provides essential benefits including superior signal integrity and thermal performance compared to traditional through-silicon vias. The market for TGV wafers in RF applications is projected to grow at a CAGR exceeding 15% through 2030, driven by increasing adoption in 5G infrastructure and smartphones. Major semiconductor foundries are investing heavily in advanced packaging technologies to meet the performance requirements of next-generation wireless communication systems.

Other Trends

Miniaturization of RF Components

Ongoing miniaturization of RF components is creating substantial opportunities for TGV wafer adoption. As device manufacturers push for smaller form factors while maintaining performance, TGV technology enables more compact RF module designs with improved electrical characteristics. The trend is particularly evident in mobile devices, where RF front-end modules utilizing TGV wafers can achieve a footprint reduction of up to 40% compared to conventional packaging solutions. This miniaturization capability is becoming increasingly critical as smartphones incorporate more RF components to support multiple frequency bands and carrier aggregation.

Advanced Packaging Adoption in Automotive Radars

The automotive industry’s shift toward autonomous driving technologies is accelerating adoption of TGV wafers in radar applications. High-frequency radar systems for advanced driver assistance systems (ADAS) require the low-loss dielectric properties and thermal stability that glass substrates provide. With the automotive radar market expected to reach over 180 million units annually by 2027, TGV wafer suppliers are seeing growing demand from tier-1 automotive suppliers. The technology’s ability to integrate multiple RF functions into compact modules makes it particularly suitable for next-generation 77 GHz radar systems, where space constraints and signal integrity are critical factors.

Material and Process Innovations Enhance Performance

Recent material and process innovations are improving TGV wafer performance characteristics for RF applications. Development of specialized glass compositions with tailored dielectric properties and coefficient of thermal expansion (CTE) values has enabled better matching with semiconductor materials. Advanced via formation techniques now achieve aspect ratios exceeding 10:1 while maintaining excellent sidewall quality, allowing for higher density interconnects. These technological improvements have positioned TGV as a preferred solution for high-frequency applications where insertion loss and signal distortion must be minimized. The ability to achieve via diameters below 30 μm while maintaining high yields is expanding the technology’s applicability across a broader range of RF components.

COMPETITIVE LANDSCAPE

Key Industry Players

Through Glass Via (TGV) Wafer for RF Applications Market Sees Intensified Competition Amid Growing Demand for 5G and IoT

The Through Glass Via (TGV) Wafer for RF Applications market is characterized by a moderately consolidated competitive environment, with Corning Incorporated emerging as the dominant player due to its technological expertise in glass substrates and strong supply chain relationships. The company commands an estimated 28% revenue share in the 300 mm wafer segment, which remains the most sought-after product type for advanced RF applications.

LPKF Laser & Electronics and Samtec have gained significant traction in recent years through specialized TGV fabrication techniques, particularly for high-frequency RF front-end modules used in 5G infrastructure. Their growth stems from strategic partnerships with semiconductor packaging leaders and investments in laser drilling technologies that enable finer via geometries below 50 μm diameter.

The market has witnessed increased M&A activity, exemplified by Xiamen Sky Semiconductor‘s acquisition of niche TGV technology providers to expand its portfolio for millimeter-wave applications. Meanwhile, Japanese firm Tecnisco has leveraged its heritage in precision glass processing to capture 15% of the Asian TGV wafer market, particularly for automotive radar applications.

While the competitive landscape remains challenging for smaller players, companies like Microplex and Plan Optik have carved out specialized niches in low-loss dielectric glass formulations for high-power RF applications. Their success demonstrates how technological differentiation can overcome scale disadvantages in this emerging market segment.

List of Key Through Glass Via (TGV) Wafer Manufacturers

- Corning Incorporated (U.S.)

- LPKF Laser & Electronics (Germany)

- Samtec (U.S.)

- KISO WAVE Co., Ltd. (Japan)

- Xiamen Sky Semiconductor (China)

- Tecnisco (Japan)

- Microplex (Germany)

- Plan Optik (Germany)

- NSG Group (Japan)

- Allvia (U.S.)

Segment Analysis:

By Type

300 mm Wafer Segment Leads Due to Superior Manufacturing Efficiency in RF Applications

The market is segmented based on type into:

- 300 mm Wafer

- 200 mm Wafer

- ≤ 150 mm Wafer

By Application

RF Front End Modules Segment Dominates Owing to Increasing Demand for 5G Devices

The market is segmented based on application into:

- RF Filters

- RF Antennas

- RF Switches

- RF Front End Modules

By End User

Telecommunications Sector Accounts for Major Share with Rapid 5G Infrastructure Rollout

The market is segmented based on end user into:

- Telecommunications

- Consumer Electronics

- Automotive

- Aerospace & Defense

Regional Analysis: Through Glass Via (TGV) Wafer for RF Applications Market

North America

North America remains a leading force in the TGV wafer market, driven by substantial investments in 5G infrastructure and advanced semiconductor technologies. The U.S., in particular, accounts for over 60% of the regional market share, owing to key players like Corning and Samtec focusing on wafer-level packaging innovations. Government initiatives, such as the CHIPS and Science Act (2022), which allocates $52 billion to domestic semiconductor manufacturing, are accelerating demand for TGV wafers in RF front-end modules and antennas. Challenges persist, however, with stringent fabrication standards and high production costs limiting adoption among smaller manufacturers. The region’s emphasis on miniaturization and high-frequency performance in aerospace and defense applications further solidifies its position as a technological leader in this space.

Europe

Europe’s TGV wafer market is characterized by strong R&D collaborations and regulatory support for semiconductor sovereignty. Countries like Germany and France are investing heavily in glass interposer technologies to reduce reliance on Asian supply chains, with the EU Chips Act (2023) committing €43 billion to bolster local production. The automotive sector is a key growth driver here, as 5G-enabled vehicles demand high-performance RF filters and switches embedded in TGV wafers. Plan Optik and LPKF dominate the regional landscape, specializing in laser-drilled vias for precision applications. However, slower adoption in Eastern Europe due to fragmented infrastructure and lower R&D expenditure creates regional disparities in market penetration.

Asia-Pacific

As the dominant global producer and consumer of TGV wafers, Asia-Pacific is projected to maintain a CAGR exceeding 12% through 2032. China’s aggressive expansion in semiconductor fabrication, backed by national champions like Xiamen Sky Semiconductor, accounts for nearly half of regional output. Japan and South Korea follow closely, with companies like Tecnisco and KISO WAVE advancing wafer thinning and via-filling techniques for high-frequency RF applications. While cost-effective manufacturing fuels growth, intellectual property concerns and geopolitical tensions pose risks. Emerging demand from India’s telecom sector and Southeast Asia’s electronics hubs presents untapped opportunities, though technological maturity lags behind established markets.

South America

South America’s TGV wafer market remains nascent, constrained by limited semiconductor infrastructure and reliance on imports. Brazil shows moderate growth in RF applications for satellite communications, with local demand growing at ~8% annually. Argentina and Chile are exploring partnerships with Asian suppliers to modernize their telecom networks, but economic instability and currency fluctuations deter large-scale investments. The absence of local TGW wafer manufacturers forces regional players to depend on higher-priced imports, slowing adoption rates despite increasing 5G rollout commitments across major urban centers.

Middle East & Africa

This region represents a high-growth potential market, albeit from a small base, with the UAE and Saudi Arabia leading TGV wafer adoption for smart city and telecom infrastructure projects. Dubai’s 6G Initiative (2030) and Saudi Vision 2030 are catalysing demand for advanced RF components, prompting collaborations with global players like NSG Group and Allvia. However, limited domestic manufacturing capabilities and reliance on foreign technology transfer hinder rapid scaling. South Africa shows early-stage interest in TGV applications for mining and IoT devices, but funding constraints and underdeveloped supply chains delay meaningful market expansion. The region’s strategic focus on digital transformation suggests long-term growth, though immediate opportunities remain concentrated in high-value urban developments.

Report Scope

This market research report provides a comprehensive analysis of the Global Through Glass Via (TGV) Wafer for RF Applications market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The market was valued at US$ 156.8 million in 2024 and is projected to reach US$ 298.7 million by 2032, growing at a CAGR of 9.6 %.

- Segmentation Analysis: Detailed breakdown by product type (300 mm Wafer, 200 mm Wafer, ≤150 mm Wafer), application (RF Filters, RF Antennas, RF Switches, RF Front End Modules), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant. Asia-Pacific is expected to dominate the market due to semiconductor manufacturing growth.

- Competitive Landscape: Profiles of leading market participants including Corning, LPKF, Samtec, KISO WAVE Co., Ltd., Xiamen Sky Semiconductor, Tecnisco, Microplex, Plan Optik, NSG Group, and Allvia, including their product offerings, R&D focus, and recent developments.

- Technology Trends & Innovation: Assessment of emerging TGV technologies, integration with advanced packaging solutions, and evolving industry standards for RF applications.

- Market Drivers & Restraints: Evaluation of factors driving market growth such as 5G deployment and IoT expansion, along with challenges including high manufacturing costs and supply chain constraints.

- Stakeholder Analysis: Insights for semiconductor manufacturers, foundries, RF component suppliers, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Through Glass Via (TGV) Wafer for RF Applications Market?

-> Through Glass Via (TGV) Wafer for RF Applications Market size was valued at US$ 156.8 million in 2024 and is projected to reach US$ 298.7 million by 2032, at a CAGR of 9.6% during the forecast period 2025-2032.

Which key companies operate in Global Through Glass Via (TGV) Wafer for RF Applications Market?

-> Key players include Corning, LPKF, Samtec, KISO WAVE Co., Ltd., Xiamen Sky Semiconductor, Tecnisco, Microplex, Plan Optik, NSG Group, and Allvia.

What are the key growth drivers?

-> Key growth drivers include 5G network expansion, increasing demand for advanced RF packaging solutions, and growth in IoT and wireless communication devices.

Which region dominates the market?

-> Asia-Pacific is the dominant market due to strong semiconductor manufacturing presence, particularly in China, Japan, and South Korea.

What are the emerging trends?

-> Emerging trends include development of wafer-level packaging solutions, integration with MEMS devices, and adoption in millimeter-wave applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...