MARKET INSIGHTS

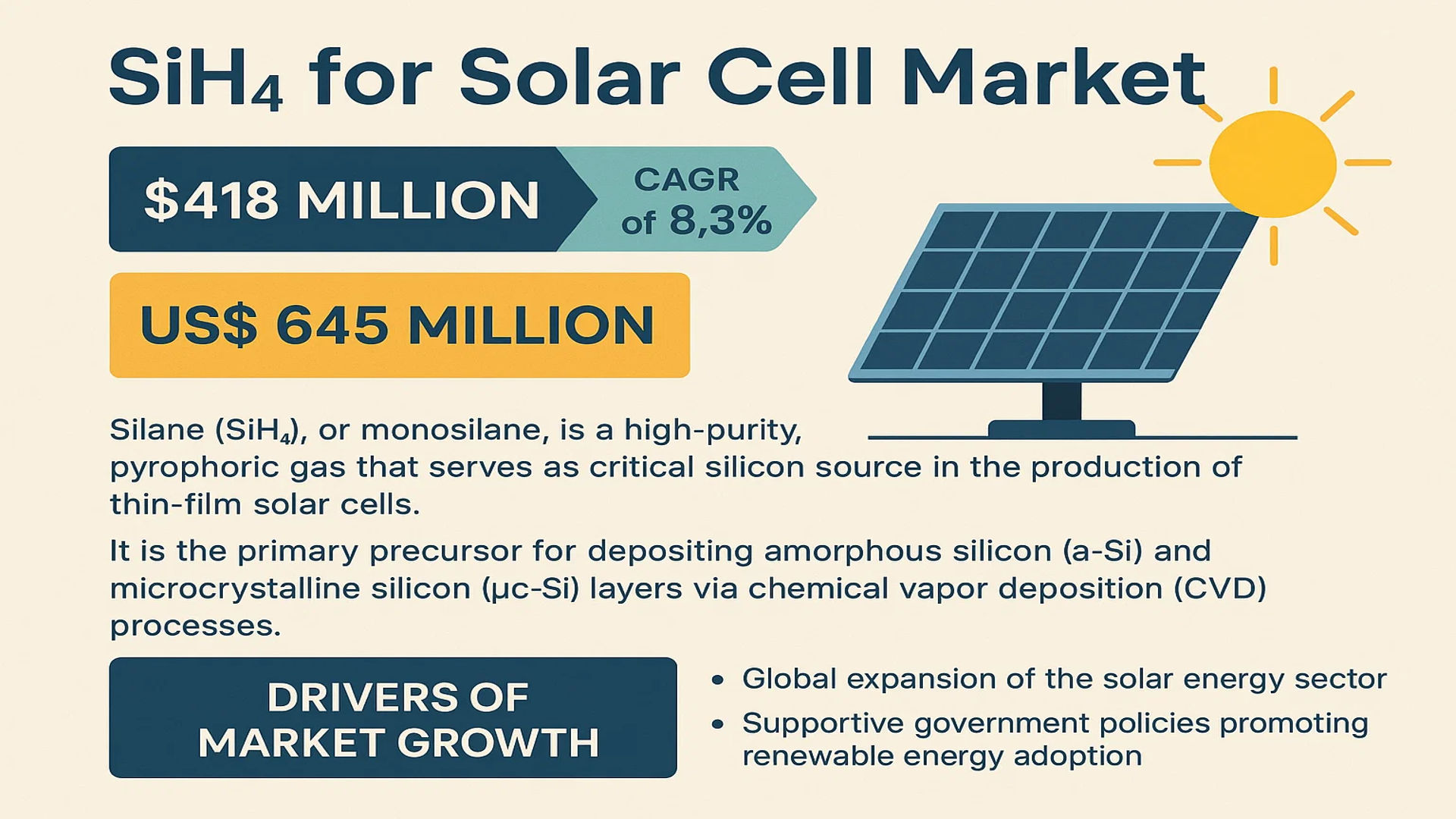

The global SiH4 for Solar Cell Market was valued at 418 million in 2024 and is projected to reach US$ 645 million by 2032, at a CAGR of 8.3% during the forecast period.

Silane (SiH4), or monosilane, is a high-purity, pyrophoric gas that serves as a critical silicon source in the production of thin-film solar cells. It is the primary precursor for depositing amorphous silicon (a-Si) and microcrystalline silicon (µc-Si) layers via chemical vapor deposition (CVD) processes. Its high deposition rates and ability to form uniform, high-quality films at relatively low processing temperatures make it an indispensable material for manufacturing efficient and cost-effective photovoltaic modules.

The market’s robust growth is primarily fueled by the global expansion of the solar energy sector and supportive government policies promoting renewable energy adoption. Furthermore, continuous technological advancements in photovoltaic cell efficiency, which demand ultra-high-purity precursors like SiH4, are a significant growth driver. The market is also characterized by the presence of key global players, including REC Silicon, Linde plc, and Air Liquide, who are investing in capacity expansions to meet the rising demand from solar panel manufacturers worldwide.

MARKET DYNAMICS

MARKET DRIVERS

Global Expansion of Solar Energy Capacity to Drive SiH4 Demand

The global solar energy sector is experiencing unprecedented growth, with installed capacity projected to exceed 2,500 GW by 2030. This expansion is primarily driven by national renewable energy targets and declining solar module costs, which have fallen by over 80% in the past decade. SiH4 serves as a critical precursor in thin-film solar cell manufacturing, particularly for amorphous silicon (a-Si) and microcrystalline silicon (µc-Si) technologies. The compound’s ability to enable high-purity silicon deposition at relatively low temperatures makes it indispensable for producing efficient photovoltaic modules. Government initiatives worldwide, including tax incentives and subsidies for solar installations, are accelerating market adoption and consequently driving demand for high-quality silane gas.

Technological Advancements in Photovoltaic Manufacturing to Boost Market Growth

Continuous innovation in photovoltaic technology is significantly enhancing the efficiency and cost-effectiveness of solar cells, thereby increasing the demand for high-purity SiH4. Recent developments in plasma-enhanced chemical vapor deposition (PECVD) processes have improved deposition rates and film quality, allowing manufacturers to achieve higher conversion efficiencies exceeding 22% for thin-film technologies. The transition toward larger substrate sizes and roll-to-roll manufacturing processes requires consistent and high-volume SiH4 supply. Furthermore, the integration of tandem cell structures combining amorphous and microcrystalline silicon layers has created additional demand for precisely controlled silane gas applications in multi-junction solar cells.

Growing Preference for Thin-Film Solar Technologies to Accelerate Market Expansion

Thin-film solar technologies are gaining increased market share due to their advantages in building-integrated photovoltaics (BIPV), flexible applications, and performance under low-light conditions. The global thin-film solar market is expected to grow at a compound annual growth rate of approximately 15% through 2030, creating substantial demand for SiH4. These technologies demonstrate superior performance in high-temperature environments and offer better aesthetic integration compared to conventional crystalline silicon modules. The development of lightweight and flexible solar panels for automotive, aerospace, and portable applications further drives the need for high-purity silane gas in manufacturing processes.

MARKET CHALLENGES

High Production Costs and Energy-Intensive Manufacturing Processes to Challenge Market Growth

The production of electronic-grade SiH4 involves complex and energy-intensive processes that significantly impact manufacturing costs. The Siemens process and fluidized bed reactor methods require substantial capital investment and operational expenses, with energy consumption accounting for approximately 40-50% of total production costs. These high costs are particularly challenging in price-sensitive markets where solar manufacturers face intense competition and margin pressures. The requirement for ultra-high purity levels exceeding 6N (99.9999%) adds further complexity and expense to the manufacturing process, creating barriers for new market entrants and limiting production scalability.

Other Challenges

Supply Chain Vulnerabilities

The SiH4 market faces significant supply chain challenges due to the concentrated nature of production facilities and specialized transportation requirements. The compound’s pyrophoric nature necessitates specialized containment and handling systems throughout the supply chain, increasing logistics costs and complexity. Geographic concentration of production facilities in specific regions creates vulnerability to disruptions from natural disasters, geopolitical tensions, or regulatory changes.

Technical Handling and Safety Concerns

SiH4’s extreme reactivity with air and moisture presents substantial safety challenges during storage, transportation, and handling. The compound spontaneously ignites in air, requiring specialized equipment and rigorous safety protocols throughout the manufacturing and application processes. These safety considerations necessitate significant investment in infrastructure and training, adding to operational costs and complicating market expansion in regions with less developed industrial safety standards.

MARKET RESTRAINTS

Competition from Alternative Solar Technologies to Restrain Market Growth

The rapid advancement of competing photovoltaic technologies presents significant restraints for the SiH4 market. Monocrystalline and polycrystalline silicon technologies continue to dominate the solar market with approximately 95% market share, offering higher efficiencies and established manufacturing infrastructure. Perovskite solar cells are emerging as a disruptive technology with rapidly improving efficiencies exceeding 25% in laboratory settings and lower manufacturing costs. These alternatives reduce the relative market share of thin-film technologies that utilize SiH4, thereby limiting the growth potential for silane gas in solar applications despite overall market expansion.

Environmental Regulations and Sustainability Concerns to Deter Market Expansion

Stringent environmental regulations governing chemical manufacturing and greenhouse gas emissions present substantial restraints for SiH4 production. The manufacturing process generates significant carbon emissions and requires careful management of byproducts and waste streams. Increasing global focus on environmental, social, and governance (ESG) criteria is driving manufacturers toward more sustainable alternatives and processes. Regulatory requirements for chemical safety, emissions control, and waste management add compliance costs and operational complexities, particularly in regions with rigorous environmental protection standards.

Economic Volatility and Raw Material Price Fluctuations to Limit Market Growth

The SiH4 market is susceptible to economic cycles and raw material price volatility, particularly silicon metal and hydrogen costs. Fluctuations in energy prices directly impact production costs, as manufacturing processes are energy-intensive. Global economic uncertainties and trade policy changes affect investment decisions in solar manufacturing capacity, creating demand variability for upstream materials including silane gas. These economic factors create challenging conditions for long-term planning and investment in production capacity expansion.

MARKET OPPORTUNITIES

Advancements in Thin-Film Photovoltaic Technologies Driving Market Evolution

The global shift towards renewable energy has catalyzed significant innovation in photovoltaic technologies, particularly within the thin-film solar cell segment where silane (SiH4) is indispensable. Recent advancements focus on enhancing deposition techniques to improve film uniformity and reduce material waste. Chemical Vapor Deposition (CVD) and Plasma-Enhanced Chemical Vapor Deposition (PECVD) processes have seen substantial refinement, allowing for higher conversion efficiencies in amorphous silicon (a-Si) and microcrystalline silicon (µc-Si) cells. These technological improvements are critical because they directly impact the Levelized Cost of Energy (LCOE), making solar power more competitive with traditional energy sources. Furthermore, the integration of tandem cell structures, which combine multiple thin-film layers to capture a broader spectrum of sunlight, is gaining traction. This architectural innovation relies heavily on high-purity silane to create defect-free interfaces between layers, pushing cell efficiencies beyond 20% in commercial production settings. The relentless pursuit of higher efficiency and lower production costs ensures that silane remains at the forefront of photovoltaic material science.

Other Trends

Expansion of Solar Manufacturing Capacity in Asia-Pacific

The Asia-Pacific region, particularly China, has solidified its position as the global epicenter for solar panel manufacturing, accounting for over 80% of the world’s production capacity. This massive scale of operations creates a correspondingly huge demand for upstream materials like silane. Domestic production of electronic-grade silane has expanded rapidly to reduce reliance on imports and secure the supply chain for photovoltaic manufacturers. National policies actively supporting renewable energy infrastructure, coupled with significant investments in new fabrication plants (fabs), are propelling this growth. While this regional concentration boosts efficiency and reduces costs through economies of scale, it also introduces supply chain vulnerabilities that global markets must navigate, making the stability of silane production a critical factor for the entire solar industry.

Increasing Demand for High-Purity Grades and Supply Chain Diversification

As solar cell manufacturers target higher efficiencies and longer product lifespans, the specification for ultra-high-purity silane (≥6N) is becoming standard rather than exceptional. Impurities, even at parts-per-billion levels, can create recombination centers within the silicon lattice that drastically reduce cell performance and longevity. This has compelled gas producers to invest heavily in advanced purification and analytical technologies to meet these stringent requirements. Concurrently, geopolitical and logistical concerns are prompting a strategic trend towards supply chain diversification. While China dominates production, other regions are developing their own silane capabilities to mitigate risk. This is not just about geographic spread but also involves exploring alternative production pathways, such as the direct synthesis from metallurgical-grade silicon, to create a more resilient and cost-effective supply network for this critical precursor gas.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Focus on High-Purity Production and Strategic Alliances to Secure Market Position

The global SiH4 for Solar Cell market exhibits a semi-consolidated structure, characterized by the presence of a few dominant multinational corporations alongside several specialized regional manufacturers. This dynamic is driven by the critical need for ultra-high-purity silane gas, which requires significant capital investment in production facilities and stringent quality control processes. REC Silicon ASA stands as a preeminent leader, largely due to its vertically integrated operations and massive production capacity, particularly from its Moses Lake facility in the United States. The company’s ability to supply high-volume, electronic-grade monosilane has made it a preferred partner for major thin-film solar panel manufacturers globally.

Similarly, Linde plc and Air Liquide S.A. have secured substantial market shares. Their dominance is not solely based on production volume but is heavily supported by their extensive global distribution networks and technical expertise in gas handling and purification. These companies provide integrated gas solutions, which is a significant value-add for solar cell producers who require a reliable and safe supply of this highly pyrophoric material. Their growth is further propelled by long-term supply agreements with key players in the photovoltaic industry.

Furthermore, these leading entities are aggressively pursuing growth through capacity expansions and technological partnerships. For instance, investments in new production plants in Asia-Pacific are aimed at capturing the burgeoning demand from the region’s massive solar manufacturing base. New product developments are also focusing on enhancing purification technologies to achieve even higher purity levels, which directly translates to improved solar cell efficiency.

Meanwhile, other significant players like Taiyo Nippon Sanso Corporation and Mitsubishi Chemical Group Corporation are strengthening their positions through strategic mergers and acquisitions. These moves are designed to consolidate expertise and expand their geographical footprint, ensuring they remain competitive in a market that is increasingly sensitive to supply chain logistics and cost-efficiency.

List of Key SiH4 for Solar Cell Companies Profiled

- REC Silicon ASA (Norway)

- Linde plc (Ireland)

- Air Liquide S.A. (France)

- Taiyo Nippon Sanso Corporation (Japan)

- Mitsubishi Chemical Group Corporation (Japan)

- SK Materials Co., Ltd. (South Korea)

- Henan Silane Technology Development Co., Ltd. (China)

- Wacker Chemie AG (Germany)

- Wolfspeed, Inc. (U.S.)

Segment Analysis:

By Purity Grade

Purity ≥6N Segment Dominates the Market Due to its Critical Role in High-Efficiency Solar Cell Production

The market is segmented based on purity grade into:

- Purity ≥6N

- Purity <6N

By Deposition Technology

Plasma-Enhanced Chemical Vapor Deposition (PECVD) Leads Due to its Superior Film Quality and Scalability

The market is segmented based on deposition technology into:

- Plasma-Enhanced Chemical Vapor Deposition (PECVD)

- Low-Pressure Chemical Vapor Deposition (LPCVD)

- Atmospheric Pressure Chemical Vapor Deposition (APCVD)

- Others

By Application

Thin-Film Solar Cells Segment Leads Due to High Adoption in Building-Integrated Photovoltaics and Flexible Panels

The market is segmented based on application into:

- Amorphous Silicon (a-Si) Thin-Film Solar Cells

- Microcrystalline Silicon (µc-Si) Thin-Film Solar Cells

- Tandem or Multi-Junction Solar Cells

By End-User

Solar Panel Manufacturers Segment Leads Due to Direct Consumption in Mass Production

The market is segmented based on end-user into:

- Solar Panel Manufacturers

- Research & Development Institutes

- Semiconductor Fabrication Plants (for other applications)

Regional Analysis: SiH4 for Solar Cell Market

Asia-Pacific

Asia-Pacific dominates the global SiH4 for solar cell market, accounting for over 75% of consumption volume. This leadership is driven by China’s massive photovoltaic manufacturing base, which produced over 80% of the world’s solar panels in 2023. The region’s focus on cost-effective thin-film technologies, particularly amorphous silicon (a-Si) cells, creates sustained demand for high-purity monosilane. Government initiatives, such as India’s Production Linked Incentive (PLI) scheme for solar module manufacturing and China’s continued investment in renewable infrastructure, further propel market growth. However, intense price competition among local manufacturers pressures profit margins for both solar cells and the specialty gases required for their production.

North America

The North American market is characterized by technological innovation and high-value applications. While the region represents a smaller volume share compared to Asia-Pacific, it commands premium pricing for ultra-high-purity SiH4 grades used in advanced heterojunction and tandem solar cell research. The U.S. Inflation Reduction Act has allocated billions in tax credits and manufacturing incentives for domestic solar production, stimulating demand for upstream materials like monosilane. Stringent safety regulations governing the handling and transportation of pyrophoric gases like SiH4 add compliance costs but also create barriers to entry that benefit established suppliers with robust safety protocols.

Europe

Europe’s market is driven by research-intensive applications and sustainability mandates. The European Green Deal and REPowerEU plan have accelerated solar adoption, with ambitious targets to deploy over 320 GW of solar capacity by 2025. This has increased demand for SiH4, particularly from manufacturers of building-integrated photovoltaics (BIPV) where thin-film technologies are preferred. European chemical companies lead in developing recycling and recovery systems for silane gases, addressing environmental concerns. However, high energy costs and stringent chemical regulations under REACH create production challenges, making the region increasingly dependent on imports from other global suppliers.

Middle East & Africa

This emerging market shows potential driven by massive solar investments in Gulf Cooperation Council countries. Saudi Arabia’s Vision 2030 includes the development of gigawatt-scale solar projects, while the UAE continues to expand its Mohammed bin Rashid Al Maktoum Solar Park. These developments create opportunities for SiH4 suppliers, though the region currently lacks local production facilities. Most monosilane is imported, adding logistical complexity and cost. The market remains in early stages, with growth constrained by limited local manufacturing expertise and the technical challenges of handling specialty gases in high-temperature environments.

South America

South America represents a developing market with growth potential concentrated in Brazil and Chile. Brazil’s distributed generation tax incentives have stimulated residential and commercial solar installations, driving demand for photovoltaic components. Chile’s abundant solar resources support utility-scale projects that increasingly incorporate thin-film technologies. However, economic volatility and limited local production capabilities restrict market growth. Most SiH4 is imported, subject to currency fluctuations and complex import regulations. The region shows long-term promise but requires significant infrastructure development and regulatory stabilization to realize its solar potential fully.

Report Scope

This market research report provides a comprehensive analysis of the global and regional SiH4 for Solar Cell markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, purity grade, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging photovoltaic technologies, fabrication techniques, deposition processes, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for chemical suppliers, solar cell manufacturers, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global SiH4 for Solar Cell Market?

-> SiH4 for Solar Cell Market was valued at 418 million in 2024 and is projected to reach US$ 645 million by 2032, at a CAGR of 8.3% during the forecast period.

Which key companies operate in Global SiH4 for Solar Cell Market?

-> Key players include REC Silicon, Linde plc, Air Liquide, Taiyo Nippon Sanso, and Mitsubishi Chemical, among others.

What are the key growth drivers?

-> Key growth drivers include global renewable energy expansion, increasing solar cell production capacity, and technological advancements in thin-film photovoltaic manufacturing.

Which region dominates the market?

-> Asia-Pacific is the dominant market region, accounting for over 65% of global SiH4 consumption for solar cell applications, driven by China’s massive solar manufacturing capacity.

What are the emerging trends?

-> Emerging trends include development of higher purity SiH4 grades, integration of advanced deposition technologies, and sustainable production methods for silane gas.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...