MARKET INSIGHTS

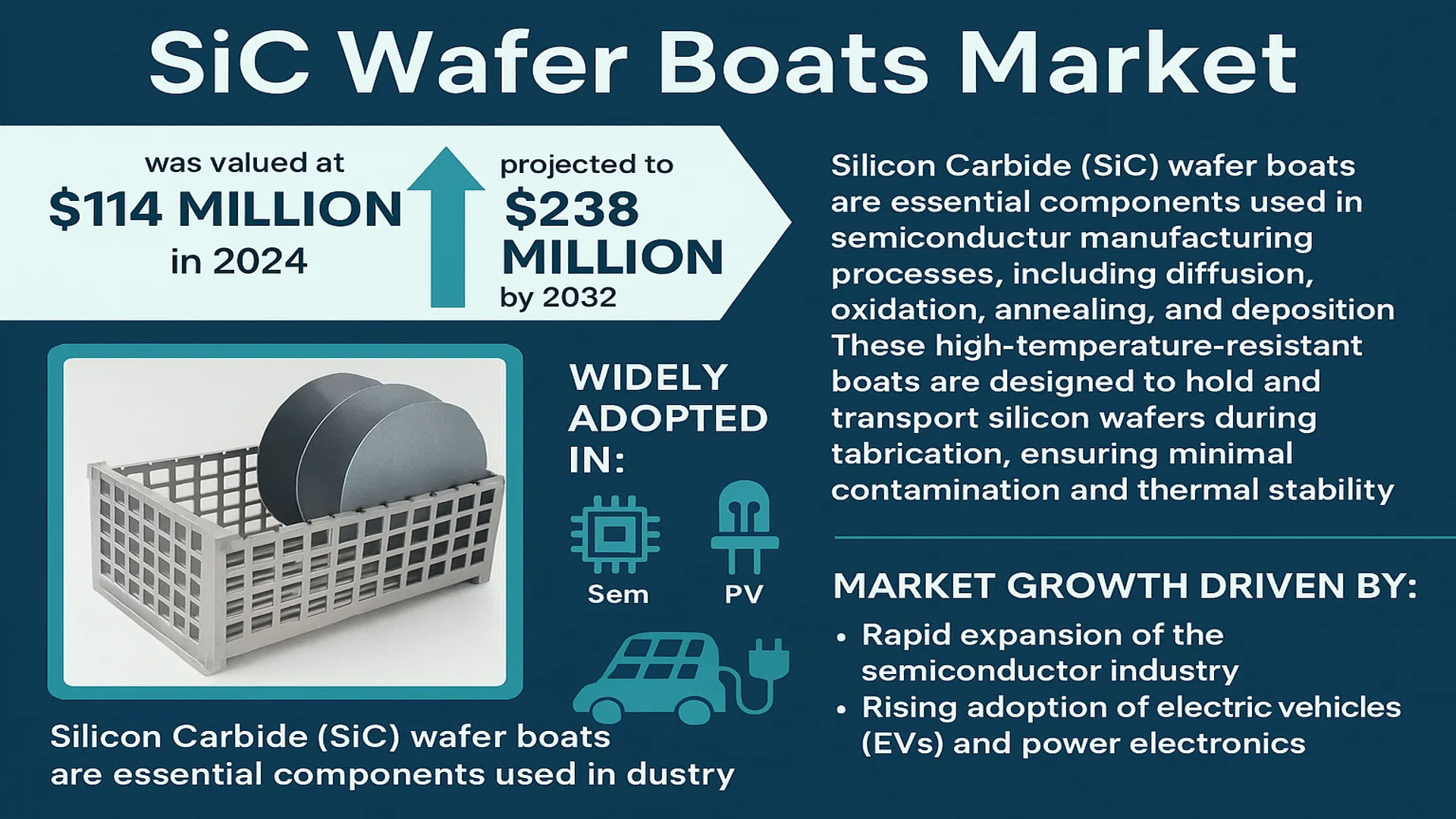

The global SiC Wafer Boats Market was valued at 114 million in 2024 and is projected to reach US$ 238 million by 2032, at a CAGR of 11.4% during the forecast period.

Silicon Carbide (SiC) wafer boats are essential components used in semiconductor manufacturing processes, including diffusion, oxidation, annealing, and deposition. These high-temperature-resistant boats are designed to hold and transport silicon wafers during fabrication, ensuring minimal contamination and thermal stability. They are widely adopted in semiconductor, LED, and photovoltaic (PV) applications due to their durability and superior heat resistance compared to traditional materials.

The market growth is primarily driven by the rapid expansion of the semiconductor industry, particularly with the rising adoption of electric vehicles (EVs) and power electronics. As the demand for 6-inch and 8-inch SiC wafers increases, manufacturers are scaling up production, further boosting the need for reliable wafer boats. Additionally, advancements in renewable energy technologies, such as solar power, are contributing to market expansion. Key players like CoorsTek, Ferrotec Taiwan Co, and Xi’an Zhongwei New Materials are investing in R&D to enhance product efficiency, supporting the industry’s long-term growth.

MARKET DYNAMICS

MARKET DRIVERS

Rapid Expansion of Electric Vehicle Industry to Fuel SiC Wafer Boat Demand

The accelerating global transition to electric vehicles (EVs) is creating unprecedented demand for silicon carbide (SiC) wafers, subsequently driving growth in the SiC wafer boat market. SiC power devices are becoming essential components in EV power electronics due to their superior thermal conductivity, high breakdown voltage, and energy efficiency advantages over traditional silicon-based solutions. With EV production projected to grow at a compound annual rate of nearly 30% through 2030, semiconductor manufacturers are rapidly scaling up SiC wafer production capacity. This expansion directly boosts the need for high-quality wafer boats that can withstand the extreme temperatures of SiC wafer processing without contaminating sensitive substrates.

Transition to Larger Wafer Sizes Boosts Equipment Investments

The semiconductor industry’s strategic shift from 6-inch to 8-inch SiC wafers is creating significant opportunities for wafer boat manufacturers. Larger wafer diameters offer substantial cost reductions through improved production yields, with 8-inch wafers providing nearly 80% more usable area compared to 6-inch versions. This transition requires semiconductor manufacturers to upgrade their processing equipment, including acquiring new wafer boats specifically designed for larger diameter substrates. Major SiC wafer producers have announced multi-billion dollar investments in 8-inch production facilities scheduled to come online within the next three years, ensuring sustained demand for advanced wafer boat solutions through the decade.

Government Support for Domestic Semiconductor Manufacturing Expands Market Potential

Strategic national initiatives aimed at strengthening semiconductor supply chains are providing significant tailwinds for the SiC wafer boat market. Multiple governments have introduced substantial funding programs and tax incentives to stimulate domestic semiconductor production capabilities, with particular emphasis on advanced materials like silicon carbide. These policies are not only increasing manufacturing capacity but also fostering technological innovation across the supply chain, including critical components like wafer boats.

➤ Industry analysts project that government semiconductor incentives worldwide could exceed $200 billion by 2025, with significant portions allocated to power electronics and wide bandgap materials.

The resulting expansion of fabrication facilities and increased R&D investment creates a favorable environment for wafer boat suppliers to develop next-generation products while expanding their customer base across multiple regions.

MARKET CHALLENGES

High Production Costs and Technical Limitations Create Barriers

While demand for SiC wafer boats is growing robustly, several technical and economic challenges could constrain market growth. The manufacturing of high-purity silicon carbide wafer boats requires specialized equipment and stringent quality controls to prevent contamination of sensitive semiconductor wafers. Production costs remain substantially higher compared to alternative materials, with high-purity SiC boats often costing 2-3 times more than equivalent quartz or silicon alternatives. These cost factors become particularly challenging when scaled to larger wafer sizes, where material expenses and manufacturing risks increase exponentially.

Other Challenges

Material Purity Requirements

The extreme purity standards required for semiconductor applications place stringent demands on SiC boat manufacturers. Even minute impurities or structural defects can compromise wafer quality, leading to strict rejection criteria that impact production yields and profitability. Maintaining consistent material properties across production batches continues to challenge suppliers.

Thermal Stress Management

SiC wafer boats must withstand repeated thermal cycling between room temperature and processing temperatures exceeding 1600°C without warping or degrading. Developing materials and designs that maintain dimensional stability through these extreme conditions requires ongoing engineering efforts and represents a persistent technical hurdle.

MARKET RESTRAINTS

Limited Supplier Base and Extended Qualification Processes Slow Adoption

The specialized nature of SiC wafer boat production has resulted in a concentrated supplier ecosystem with limited capacity to rapidly scale production. Semiconductor manufacturers typically require extensive qualification periods—often spanning 12-18 months—to validate new wafer boat suppliers or product iterations. These lengthy approval cycles create bottlenecks in the supply chain and can delay the adoption of innovative solutions even when technological advancements become available. The resulting supply-demand imbalance creates pricing pressures and limits market responsiveness to growing industry requirements.

Competition from Alternative Materials Presents Ongoing Challenge

While SiC wafer boats offer superior performance characteristics for many applications, alternative materials continue to capture market share in certain segments. Quartz remains widely used for lower-temperature processes due to its lower cost and established supply chains, while advanced graphite solutions have made inroads in specific high-temperature applications. These alternatives benefit from decades of process optimization and infrastructure development, making the value proposition for SiC boats more challenging in cost-sensitive applications despite their technical advantages.

MARKET OPPORTUNITIES

Emerging Applications in Power Electronics Create New Growth Frontiers

Beyond traditional semiconductor manufacturing, expanding applications for SiC power devices in renewable energy systems, industrial power conversion, and 5G infrastructure are creating additional demand levers for wafer boat suppliers. The renewable energy sector alone is projected to drive nearly 30% of SiC device demand growth through 2030, requiring corresponding increases in wafer production capacity. These diverse applications often have unique technical requirements, opening opportunities for specialized wafer boat designs tailored to specific end-use cases.

Technological Advancements Enable Next-Generation Products

Ongoing material science innovations are creating pathways for improved SiC wafer boat performance. Developments in sintering techniques and purity control methods are enabling boats with enhanced thermal properties and longer operational lifetimes. Some manufacturers have already demonstrated prototypes with 50% longer service life compared to conventional products, offering substantial total cost of ownership benefits for semiconductor producers. As these technologies mature and scale, they are expected to open premium market segments while driving broader adoption across the industry.

SIC WAFER BOATS MARKET TRENDS

Expansion of Silicon Carbide Applications in Power Electronics Driving Market Growth

The SiC Wafer Boats market is experiencing significant growth, fueled by the rising adoption of silicon carbide in power electronics, particularly in electric vehicles (EVs), renewable energy, and industrial applications. The superior thermal conductivity, high breakdown voltage, and energy efficiency of SiC wafers compared to traditional silicon make them ideal for high-power applications. Recent reports indicate that global SiC wafer revenue surpassed $750 million in 2022, with projections suggesting a compound annual growth rate (CAGR) of 11.4% through 2032. This surge is largely attributed to increasing demand from the EV sector, where SiC-based power modules enhance battery efficiency and reduce charging times.

Other Trends

Transition from 6-Inch to 8-Inch SiC Wafers

The semiconductor industry is steadily shifting from 6-inch to 8-inch SiC wafers as manufacturers seek to improve production efficiency and reduce costs. While 6-inch wafers currently dominate, industry leaders predict that 8-inch production will gain traction over the coming years, enabling higher throughput in wafer processing. China, in particular, is emerging as a key player in this transition, with several domestic firms accelerating their production capabilities to meet both local and international demand. This shift is expected to drive further investments in SiC wafer boat manufacturing, as larger wafers necessitate more durable and precise handling solutions.

Rising Semiconductor and LED Industry Investments

Increasing investments in next-generation semiconductor fabrication are boosting the demand for SiC wafer boats, particularly in diffusion, oxidation, and deposition processes. The semiconductor segment accounts for the largest share of the market, with LED and photovoltaic applications also contributing to growth. Industry trends indicate that advancements in 5G technology, IoT devices, and high-performance computing are further accelerating the need for reliable SiC-based components. Additionally, vertical wafer boats are gaining popularity due to their space efficiency in advanced semiconductor manufacturing setups, offering enhanced thermal stability for precise process control.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Expansion and Innovation Drive Market Competition

The global SiC Wafer Boats market is characterized by a moderately fragmented competitive landscape with dominant players focusing on product innovation and geographical expansion to gain a larger market share. As the market grows at a promising CAGR of 11.4%, competition intensifies, particularly in regions like Asia-Pacific, where demand for semiconductor manufacturing equipment is surging.

CoorsTek stands as a market leader, leveraging its extensive R&D capabilities and global supply chain to provide high-performance SiC wafer handling solutions. The company holds a significant revenue share, particularly in the semiconductor and LED segments. Similarly, Ferrotec Taiwan Co. has emerged as a key player, specializing in advanced ceramic solutions for wafer processing, supported by strong demand from the Taiwanese semiconductor industry.

Meanwhile, Chinese manufacturers like Xi’an Zhongwei New Materials and Zhejiang Dongxin New Material are rapidly expanding their market presence, driven by domestic semiconductor and solar energy sector growth. Their competitive pricing strategies and increasing production capacities position them as significant contenders in the global arena.

On the innovation front, companies such as Kallex and 3X Ceramic Parts are enhancing their product offerings with vertically integrated manufacturing processes and customized solutions for specialized industrial applications. These strategic initiatives are expected to fuel further market consolidation as larger players look to strengthen their technological edge.

List of Key SiC Wafer Boats Companies Profiled

- CoorsTek (U.S.)

- Ferrotec Taiwan Co. (Taiwan)

- Kallex (China)

- 3X Ceramic Parts (China)

- FCT (Tangshan) (China)

- Xi’an Zhongwei New Materials (China)

- Zhejiang Dongxin New Material (China)

- Shandong Huamei New Material (China)

Segment Analysis:

By Type

Horizontal Segment Leads Due to Superior Thermal Stability and High Load Capacity

The market is segmented based on type into:

- Horizontal

- Vertical

By Application

Semiconductor Segment Dominates Driven by Increasing SiC Adoption in Power Electronics

The market is segmented based on application into:

- Semiconductor

- Sub-sectors: Power devices, RF devices, and others

- LED

- Sub-sectors: Commercial lighting, automotive lighting, and others

- PV

- Sub-sectors: Solar cells, photovoltaic modules, and others

By Process Type

Diffusion Process Segment Holds Major Share for Wafer Manufacturing Applications

The market is segmented based on process type into:

- Diffusion process

- Dry oxidation process

- Wet oxidation process

- Annealing process

- Deposition process

By Wafer Size

6-Inch Segment Remains Prevalent While 8-Inch Gaining Traction

The market is segmented based on wafer size into:

- 4-inch

- 6-inch

- 8-inch

- Others

Regional Analysis: SiC Wafer Boats Market

Asia-Pacific

The Asia-Pacific region dominates the global SiC Wafer Boats market, accounting for over 50% of global consumption in 2024. This leadership position is driven by China’s aggressive semiconductor manufacturing expansion, Japan’s established SiC substrate production capabilities (with companies like CoorsTek and 3X Ceramic Parts), and South Korea’s advanced semiconductor ecosystem. The region’s growth is further accelerated by massive investments in electric vehicle production, which requires SiC power electronics. China alone is expected to maintain a 15% annual growth rate in SiC wafer production capacity through 2030, creating sustained demand for wafer boats in diffusion and deposition processes.

North America

North America maintains strong technological leadership in SiC wafer boat manufacturing, with U.S.-based firms like Ferrotec and Kallex developing advanced vertical wafer boat designs for 8-inch wafer processing. The region benefits from close R&D collaboration between semiconductor equipment manufacturers and material science innovators. While production volumes are smaller than Asia-Pacific, North America captures premium market segments through specialized solutions for high-temperature applications in aerospace and defense sectors. Recent CHIPS Act funding is stimulating additional capacity expansions in domestic semiconductor fabrication, which will drive future demand.

Europe

Europe’s SiC Wafer Boats market is characterized by precision engineering and stringent quality standards, with German and French manufacturers leading in customized solutions for automotive-grade SiC devices. The region’s strong focus on renewable energy applications, particularly in photovoltaic and industrial power systems, creates stable demand for durable wafer boats. However, higher production costs compared to Asian competitors limit volume growth. European suppliers are increasingly forming technological partnerships with Asian foundries to maintain market relevance while addressing cost pressures through automation and process innovations.

Middle East & Africa

This emerging market shows promise with new semiconductor initiatives in Israel and renewable energy projects in the Gulf region, though overall adoption remains limited by underdeveloped local semiconductor ecosystems. Strategic investments in technology transfer agreements with European and Asian partners are helping to establish initial manufacturing capabilities. The market is expected to grow as part of broader economic diversification plans, particularly in UAE and Saudi Arabia, where sovereign wealth funds are allocating capital to advanced materials sectors.

South America

South America represents the smallest regional market for SiC Wafer Boats, constrained by limited semiconductor manufacturing infrastructure. Brazil shows modest growth potential through its developing electronics industry and renewable energy sector imports. However, economic volatility and lack of specialized suppliers restrict market expansion. Most wafer boats in the region are imported from global manufacturers, with some local distribution partnerships emerging to serve niche industrial applications in Argentina and Chile.

Report Scope

This market research report provides a comprehensive analysis of the Global SiC Wafer Boats Market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global SiC Wafer Boats market was valued at USD 114 million in 2024 and is projected to reach USD 238 million by 2032, growing at a CAGR of 11.4%.

- Segmentation Analysis: Detailed breakdown by product type (Horizontal, Vertical), application (Semiconductor, LED, PV), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with China, Japan, and the US as key markets.

- Competitive Landscape: Profiles of leading market participants including Kallex, CoorsTek, Ferrotec Taiwan Co, and FCT(Tangshan), covering their product portfolios, market share, and strategic developments.

- Technology Trends & Innovation: Assessment of the transition from 6-inch to 8-inch SiC wafers and advancements in semiconductor fabrication processes.

- Market Drivers & Restraints: Evaluation of factors such as EV market growth and semiconductor industry expansion, along with challenges in manufacturing scalability.

- Stakeholder Analysis: Strategic insights for manufacturers, suppliers, and investors regarding market opportunities in the evolving SiC ecosystem.

The report employs both primary and secondary research methodologies, including expert interviews and analysis of verified market data, to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global SiC Wafer Boats Market?

-> SiC Wafer Boats Market was valued at 114 million in 2024 and is projected to reach US$ 238 million by 2032, at a CAGR of 11.4% during the forecast period.

Which key companies operate in Global SiC Wafer Boats Market?

-> Key players include Kallex, CoorsTek, Ferrotec Taiwan Co, FCT(Tangshan), and Xi’an Zhongwei New Materials.

What are the key growth drivers?

-> Key growth drivers include rising demand from the EV sector, semiconductor industry expansion, and technological advancements in wafer fabrication.

Which region dominates the market?

-> Asia-Pacific leads the market, with China emerging as a key growth region due to increasing semiconductor manufacturing activities.

What are the emerging trends?

-> Emerging trends include transition to 8-inch wafers, increasing adoption in power electronics, and growing investments in SiC manufacturing capacity.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...