Specialty Gases for Semiconductor Market Overview

Specialty Gases for Semiconductor range from the pyrophoric and/or toxic specialty gases required for thin film deposition and doping processes (ammonia, methane, silane, germane, dichlorosilane, silicon tetrachloride, phosphine, diborane, arsine and others) through the reactive and corrosive gases needed in different etch processes (chlorine, fluorine, halocarbons, nitrogen trifluoride, etc.). The atmospheric gases (oxygen, hydrogen, nitrogen, argon and helium) are not covers in this report. The Specialty Gases for Semiconductor market covers Nitrogen Trifluoride, Silicon-Precursor Gases, Fluoroalkane, Ammonia, Others, etc. The typical players include SK Materials, Hyosung, Kanto Denka Kogyo, Merck (Versum Materials), PERIC, Mitsui Chemical, ChemChina, Shandong FeiYuan, etc.

This report provides a deep insight into the global Specialty Gases for Semiconductor market covering all its essential aspects. This ranges from a macro overview of the market to micro details of the market size, competitive landscape, development trend, niche market, key market drivers and challenges, SWOT analysis, value chain analysis, etc.

The analysis helps the reader to shape the competition within the industries and strategies for the competitive environment to enhance the potential profit. Furthermore, it provides a simple framework for evaluating and accessing the position of the business organization. The report structure also focuses on the competitive landscape of the Global Specialty Gases for Semiconductor Market, this report introduces in detail the market share, market performance, product situation, operation situation, etc. of the main players, which helps the readers in the industry to identify the main competitors and deeply understand the competition pattern of the market.

In a word, this report is a must-read for industry players, investors, researchers, consultants, business strategists, and all those who have any kind of stake or are planning to foray into the Specialty Gases for Semiconductor market in any manner.

Specialty Gases for Semiconductor Market Analysis:

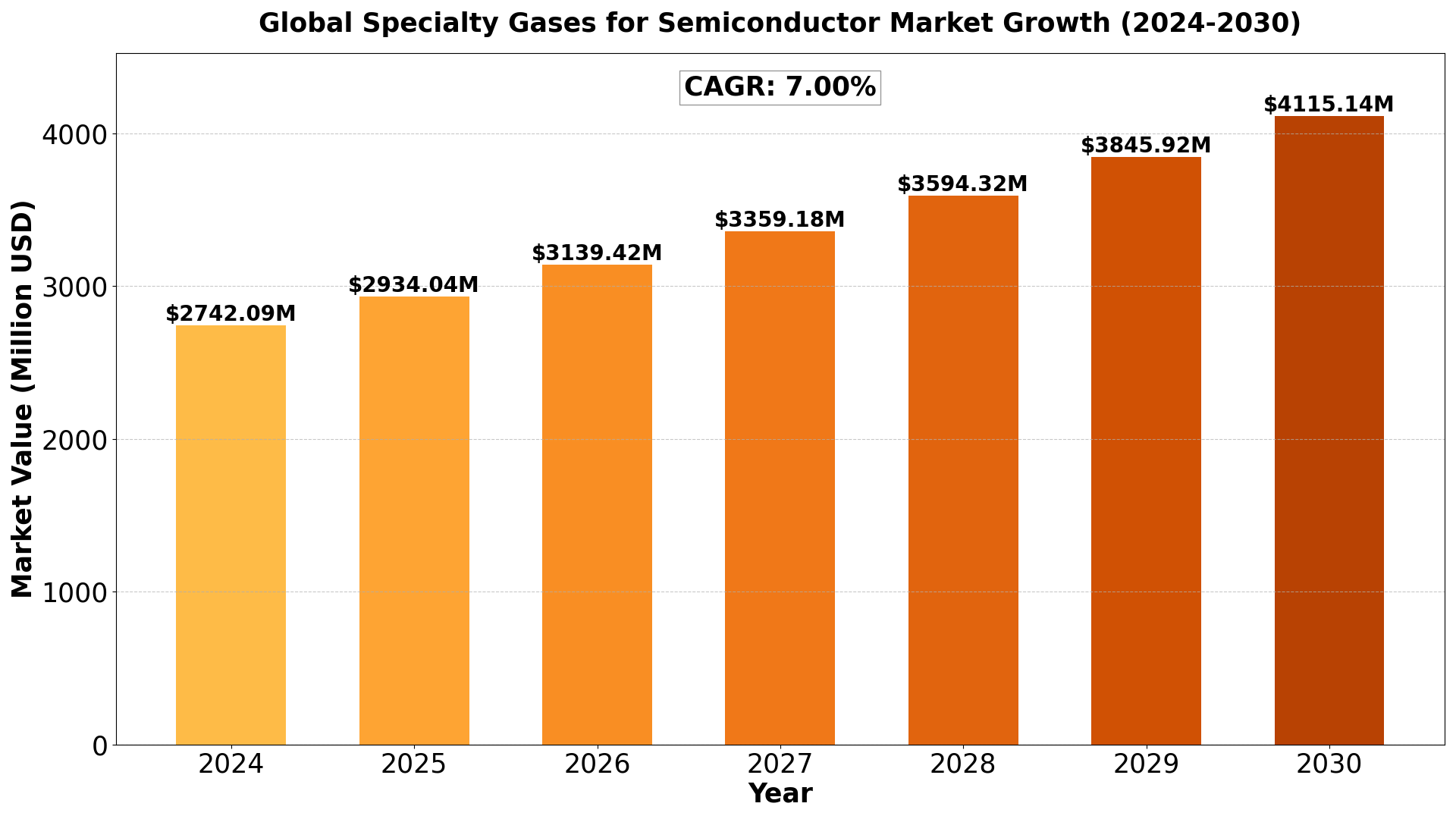

The Global Specialty Gases for Semiconductor Market size was estimated at USD 2562.70 million in 2023 and is projected to reach USD 4115.14 million by 2030, exhibiting a CAGR of 7.00% during the forecast period.

North America Specialty Gases for Semiconductor market size was USD 667.77 million in 2023, at a CAGR of 6.00% during the forecast period of 2024 through 2030.

Specialty Gases for Semiconductor Key Market Trends :

- Rising Demand for Advanced Semiconductor Manufacturing

- Increasing complexity in semiconductor chip design is driving the need for high-purity specialty gases in deposition and etching processes.

- Shift Towards Sustainable and Green Manufacturing

- Growing environmental concerns are pushing companies to adopt eco-friendly specialty gases and implement emission-reducing technologies.

- Technological Advancements in Semiconductor Fabrication

- Innovations such as EUV lithography and atomic layer deposition (ALD) are increasing the demand for ultra-high-purity specialty gases.

- Expanding Role of AI, IoT, and 5G Technologies

- The proliferation of AI-driven devices, IoT applications, and 5G infrastructure is boosting the semiconductor industry’s growth, thus driving the specialty gas market.

- Strong Growth in the Asia-Pacific Region

- Asia-Pacific remains the dominant region due to the presence of major semiconductor foundries and increasing investments in advanced chip production.

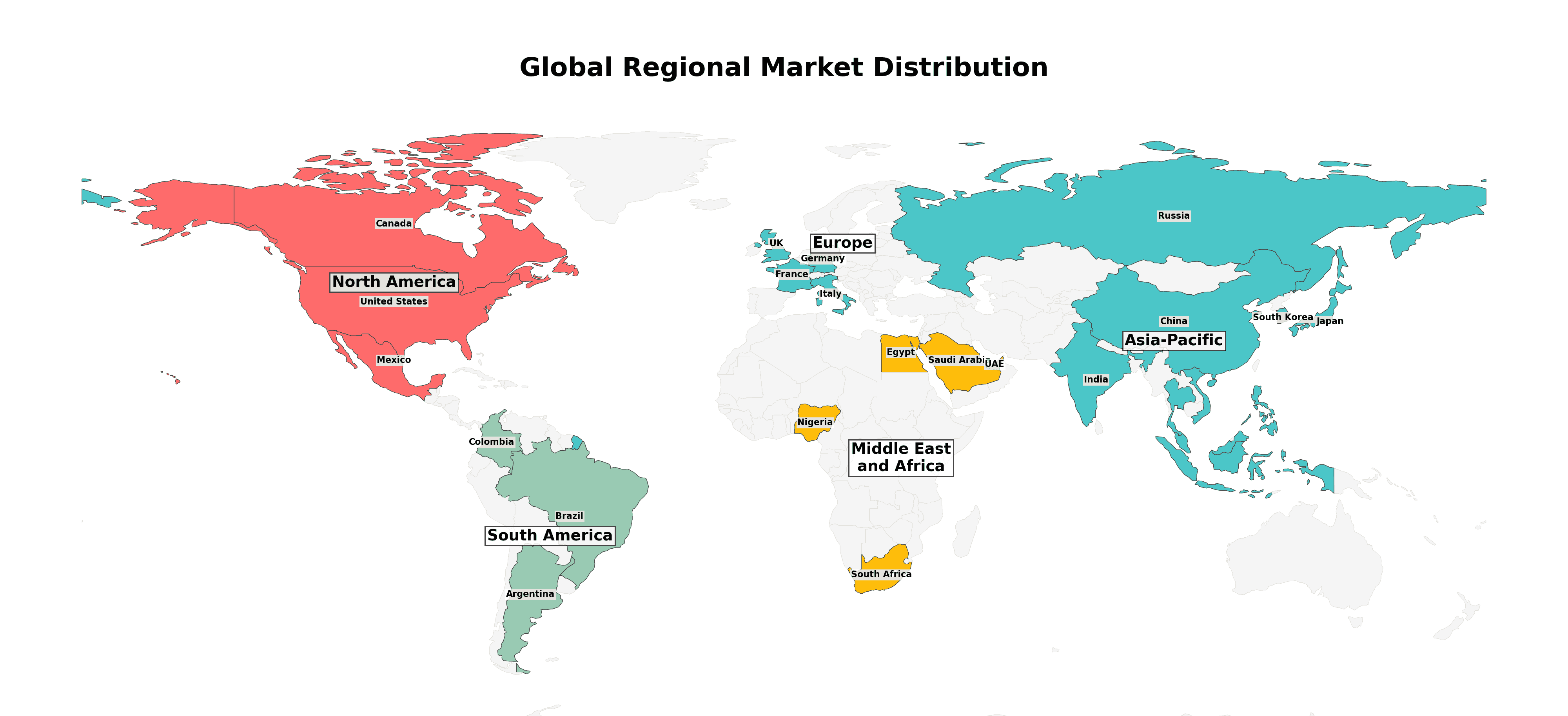

Specialty Gases for Semiconductor Market Regional Analysis :

-

North America:

Strong demand driven by EVs, 5G infrastructure, and renewable energy, with the U.S. leading the market.

-

Europe:

Growth fueled by automotive electrification, renewable energy, and strong regulatory support, with Germany as a key player.

-

Asia-Pacific:

Dominates the market due to large-scale manufacturing in China and Japan, with growing demand from EVs, 5G, and semiconductors.

-

South America:

Emerging market, driven by renewable energy and EV adoption, with Brazil leading growth.

-

Middle East & Africa:

Gradual growth, mainly due to investments in renewable energy and EV infrastructure, with Saudi Arabia and UAE as key contributors.

Specialty Gases for Semiconductor Market Segmentation :

The research report includes specific segments by region (country), manufacturers, Type, and Application. Market segmentation creates subsets of a market based on product type, end-user or application, Geographic, and other factors. By understanding the market segments, the decision-maker can leverage this targeting in the product, sales, and marketing strategies. Market segments can power your product development cycles by informing how you create product offerings for different segments.

Key Company

- SK Materials (SK specialty)

- Merck (Versum Materials)

- Taiyo Nippon Sanso

- Linde plc

- Kanto Denka Kogyo

- Hyosung

- PERIC

- Showa Denko

- Mitsui Chemical

- ChemChina

- Shandong FeiYuan

- Guangdong Huate Gas

- Central Glass

Market Segmentation (by Type)

- Nitrogen Trifluoride

- Silicon-Precursor Gases

- Fluoroalkane

- Ammonia

- Others

Market Segmentation (by Application)

- Consumer Electronics

- Automotive Electronics

- Networking & Communications

- Others

Drivers

- Increasing Semiconductor Production

- The surge in demand for consumer electronics, automotive electronics, and cloud computing is fueling the semiconductor industry’s expansion.

- Growth in Artificial Intelligence and 5G Technologies

- The rapid adoption of AI, IoT, and 5G is driving the need for advanced semiconductor chips, which in turn increases the demand for specialty gases.

- Rising Demand for Advanced Lithography Techniques

- The adoption of extreme ultraviolet (EUV) lithography and other next-gen semiconductor fabrication processes is pushing the need for ultra-high-purity gases.

Restraints:

- High Costs of Specialty Gases

- The production and purification of specialty gases require significant investment, making them expensive for semiconductor manufacturers.

- Stringent Environmental Regulations

- Regulations on toxic and hazardous gases used in semiconductor fabrication can lead to increased compliance costs and operational challenges.

- Supply Chain Disruptions

- The semiconductor industry’s dependency on a complex global supply chain can lead to shortages and increased lead times for specialty gases.

Opportunities:

- Expansion of Semiconductor Manufacturing in Emerging Markets

- Countries like India, Vietnam, and Malaysia are investing in semiconductor manufacturing, creating new opportunities for specialty gas suppliers.

- Development of Eco-Friendly Specialty Gases

- Growing environmental concerns are driving the research and adoption of low-global-warming-potential (GWP) gases.

- Increase in Strategic Partnerships and Acquisitions

- Leading companies are forming alliances to strengthen their specialty gas portfolios and expand their global presence.

Challenges:

- Fluctuations in Raw Material Prices

- The cost of raw materials used in specialty gas production is volatile, impacting overall profitability.

- Technical Complexities in Manufacturing Ultra-Pure Gases

- The demand for high-purity gases requires sophisticated purification technologies, making production challenging and costly.

- Geopolitical and Trade Restrictions

- Trade barriers and geopolitical tensions between key semiconductor-producing regions can impact the supply and pricing of specialty gases.

Key Benefits of This Market Research:

- Industry drivers, restraints, and opportunities covered in the study

- Neutral perspective on the market performance

- Recent industry trends and developments

- Competitive landscape & strategies of key players

- Potential & niche segments and regions exhibiting promising growth covered

- Historical, current, and projected market size, in terms of value

- In-depth analysis of the Specialty Gases for Semiconductor Market

- Overview of the regional outlook of the Specialty Gases for Semiconductor Market:

Key Reasons to Buy this Report:

- Access to date statistics compiled by our researchers. These provide you with historical and forecast data, which is analyzed to tell you why your market is set to change

- This enables you to anticipate market changes to remain ahead of your competitors

- You will be able to copy data from the Excel spreadsheet straight into your marketing plans, business presentations, or other strategic documents

- The concise analysis, clear graph, and table format will enable you to pinpoint the information you require quickly

- Provision of market value (USD Billion) data for each segment and sub-segment

- Indicates the region and segment that is expected to witness the fastest growth as well as to dominate the market

- Includes in-depth analysis of the market from various perspectives through Porters five forces analysis

- Provides insight into the market through Value Chain

- Market dynamics scenario, along with growth opportunities of the market in the years to come

- 6-month post-sales analyst support

Customization of the Report

In case of any queries or customization requirements, please connect with our sales team, who will ensure that your requirements are met.

FAQs

Q: What are the key driving factors and opportunities in the Specialty Gases for Semiconductor market?

A: The major drivers include the growing semiconductor industry, technological advancements, and increasing demand for high-purity gases. Opportunities lie in emerging markets, eco-friendly gas innovations, and strategic industry collaborations.

Q: Which region is projected to have the largest market share?

A: The Asia-Pacific region is expected to dominate the market, driven by the presence of leading semiconductor manufacturers in China, South Korea, Taiwan, and Japan.

Q: Who are the top players in the global Specialty Gases for Semiconductor market?

A: Leading companies include SK Materials, Merck (Versum Materials), Taiyo Nippon Sanso, Linde plc, Kanto Denka Kogyo, Hyosung, PERIC, and others.

Q: What are the latest technological advancements in the industry?

A: Innovations such as extreme ultraviolet (EUV) lithography, atomic layer deposition (ALD), and the development of low-GWP specialty gases are transforming the industry.

Q: What is the current size of the global Specialty Gases for Semiconductor market?

A: The market was valued at USD 2,562.70 million in 2023 and is projected to reach USD 4,115.14 million by 2030, growing at a CAGR of 7.00%.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...