MARKET INSIGHTS

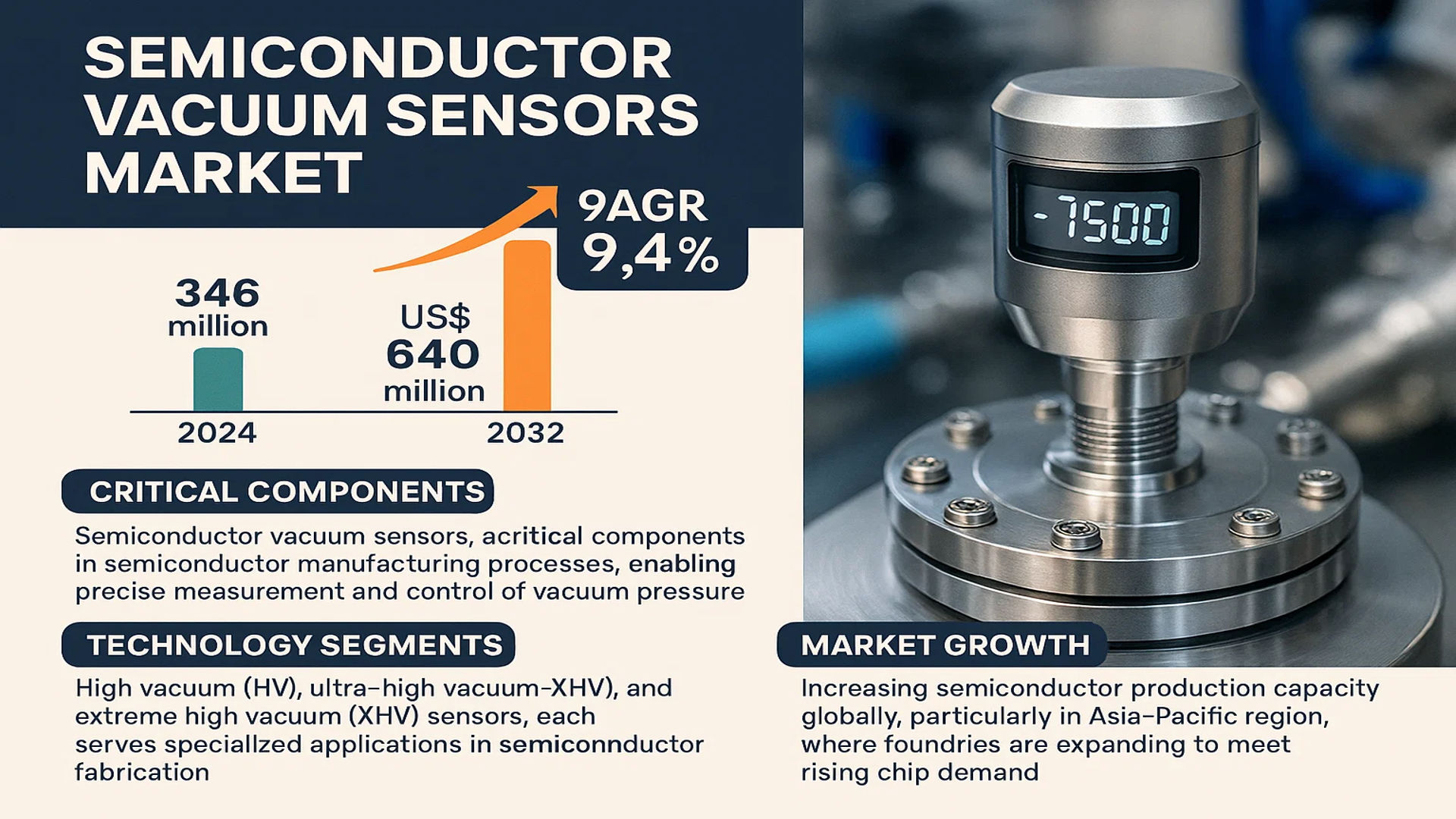

The global Semiconductor Vacuum Sensors Market was valued at 346 million in 2024 and is projected to reach US$ 640 million by 2032, at a CAGR of 9.4% during the forecast period.

Semiconductor vacuum sensors are critical components in semiconductor manufacturing processes, enabling precise measurement and control of vacuum pressure. These sensors play a vital role in maintaining optimal conditions for processes such as chemical vapor deposition (CVD), atomic layer deposition (ALD), etching, and ion implantation. The technology segments include high vacuum (HV), ultra-high vacuum (UHV), and extreme high vacuum (XHV) sensors, each serving specialized applications in semiconductor fabrication.

The market growth is driven by increasing semiconductor production capacity globally, particularly in Asia-Pacific, where foundries are expanding to meet rising chip demand. However, cyclical fluctuations in the semiconductor industry, such as the 4.4% growth slowdown in 2022 reported by WSTS, create market volatility. Key players like NXP, Honeywell, and Agilent continue to innovate with more accurate and durable sensor solutions to support advanced semiconductor manufacturing nodes below 10nm.

MARKET DYNAMICS

MARKET DRIVERS

Expansion of Semiconductor Manufacturing to Fuel Vacuum Sensor Demand

The global semiconductor market has demonstrated remarkable resilience despite economic fluctuations, with vacuum sensors playing a critical role in fabrication processes. Semiconductor manufacturing requires ultra-precise vacuum environments, particularly for deposition and etching applications where pressure control directly impacts yield rates. The growing adoption of 3D NAND flash memory and advanced logic nodes below 10nm has increased vacuum system complexity, driving demand for high-performance sensors. With foundries investing over $150 billion annually in new fabrication facilities, vacuum monitoring equipment has become indispensable for maintaining process consistency across 300mm and emerging 450mm wafer production lines.

Automotive Semiconductor Boom Accelerating Market Growth

Automotive electronics now account for over 15% of total semiconductor demand, creating significant opportunities for vacuum sensor manufacturers. The transition toward electric vehicles and autonomous driving systems has dramatically increased the semiconductor content per vehicle, with modern EVs containing nearly triple the chips of conventional cars. This growth directly impacts vacuum sensor demand as sensor manufacturers develop specialized products for automotive-grade MEMS fabrication. The rising adoption of silicon carbide and gallium nitride power semiconductors for EV power electronics further compounds this demand, as these materials require precise vacuum environments during epitaxial growth and device processing.

Advanced Packaging Technologies Driving Next-Generation Requirements

The semiconductor industry’s shift toward advanced packaging techniques such as 2.5D/3D ICs and chiplet architectures is creating new technical requirements for vacuum measurement. Fan-out wafer-level packaging and through-silicon via (TSV) processes demand ultra-clean vacuum environments to prevent contamination during delicate interconnect formation. Emerging hybrid bonding technologies require vacuum levels below 10-7 mbar, pushing sensor manufacturers to develop more sensitive measurement solutions. This trend aligns with the broader industry movement toward heterogeneous integration, where vacuum sensors play a critical role in maintaining process control across diverse packaging methodologies.

MARKET RESTRAINTS

Technical Complexity in Extreme Vacuum Environments Limits Adoption

While semiconductor manufacturing continues advancing, vacuum sensor technology faces significant challenges in extreme high vacuum (XHV) applications. Modern atomic layer deposition (ALD) systems require pressure measurement capabilities below 10-9 mbar, pushing the limits of conventional sensor designs. Outgassing from sensor materials becomes problematic at these levels, potentially contaminating process chambers. Additionally, thermal management becomes increasingly difficult in XHV conditions, with temperature fluctuations causing measurement drift. These technical hurdles require substantial R&D investment, creating barriers for smaller manufacturers and potentially slowing innovation cycles in sensor technology.

High Ownership Costs Challenge Price-Sensitive Manufacturers

The total cost of ownership for semiconductor vacuum sensors often extends beyond initial purchase prices, creating adoption barriers. Premium vacuum sensor solutions for semiconductor fabs can exceed $10,000 per unit, with specialized XHV variants reaching significantly higher price points. These costs compound when considering calibration requirements, replacement diaphragms, and integration with factory automation systems. For smaller semiconductor firms and research facilities, these expenses can limit access to the latest sensor technologies, potentially creating performance gaps with larger competitors. The situation is particularly challenging in emerging semiconductor markets where capital budgets remain constrained.

MARKET CHALLENGES

Material Compatibility Issues in Advanced Semiconductor Processes

Vacuum sensor manufacturers face growing challenges in material selection as semiconductor processes become more chemically aggressive. The industry’s shift to novel etch chemistries containing high-fluorine compounds and the adoption of cobalt and ruthenium interconnect materials introduces compatibility concerns. Sensor diaphragms and seals must withstand exposure to these substances while maintaining measurement accuracy. Some advanced etch processes using plasma conditions exceeding 600°C create additional thermal stress on sensor components. These material challenges require continuous innovation in sensor design and protective coatings, adding complexity to product development cycles.

Cleanroom Integration and Maintenance Complexities

Integrating vacuum sensors into semiconductor cleanroom environments presents numerous operational challenges. Sensor placement must minimize particulate generation while providing accurate pressure readings across multiple process chamber zones. Maintenance procedures often require breaking vacuum seals, potentially introducing contaminants. Furthermore, the trend toward cluster tools with multiple process chambers complicates vacuum system design, requiring sensors to operate reliably across varied pressure regimes. These integration challenges increase equipment downtime and require specialized training for fab technicians, adding to operational costs.

MARKET OPPORTUNITIES

Emerging Compound Semiconductor Applications Create New Markets

The rapid growth of compound semiconductor manufacturing presents significant opportunities for vacuum sensor providers. Gallium arsenide, gallium nitride, and silicon carbide processes often require specialized vacuum conditions different from traditional silicon. For instance, MOCVD reactors used in LED and power device production demand precise pressure control during epitaxial growth. As these technologies penetrate 5G infrastructure, electric vehicles, and renewable energy applications, demand for compatible vacuum sensors is projected to grow at nearly 12% annually. Sensor manufacturers developing solutions tailored to these unique process requirements stand to gain substantial market share in this expanding segment.

Smart Factory Integration Opens Data Analytics Potential

The semiconductor industry’s adoption of Industry 4.0 principles creates opportunities to enhance vacuum sensor functionality. Modern sensors equipped with IoT connectivity can provide real-time process analytics, predictive maintenance alerts, and automated calibration features. Integration with manufacturing execution systems (MES) allows for dynamic pressure control adjustments based on wafer processing histories. Leading semiconductor equipment manufacturers increasingly prioritize sensors with embedded intelligence, creating a competitive advantage for providers offering advanced data capabilities. This trend aligns with broader fab automation initiatives aimed at improving yield and reducing human intervention in critical processes.

SEMICONDUCTOR VACUUM SENSORS MARKET TRENDS

Miniaturization and Enhanced Precision Drive Market Expansion

The semiconductor vacuum sensors market is witnessing significant growth due to the increasing demand for miniaturized and high-precision components in semiconductor manufacturing. Advanced processes like Atomic Layer Deposition (ALD) and Low-Pressure Chemical Vapor Deposition (LPCVD) require ultra-sensitive vacuum control, driving the adoption of next-generation sensors. The global semiconductor vacuum sensors market, valued at $346 million in 2024, is projected to reach $640 million by 2032, growing at a CAGR of 9.4%. This surge is fueled by the need for tighter tolerances in semiconductor fabrication, where even slight pressure variations can impact yield rates. Manufacturers are investing in MEMS-based vacuum sensors that offer improved accuracy and faster response times, enabling real-time adjustments during complex processes.

Other Trends

Integration of IoT and Industry 4.0

The rise of smart factories and Industry 4.0 initiatives is transforming vacuum monitoring through IoT-enabled sensors. These devices provide continuous data streams for predictive maintenance and process optimization, reducing downtime in semiconductor production lines. Recent developments include wireless vacuum sensors that communicate with centralized control systems, allowing engineers to monitor chamber pressures remotely. With semiconductor fabs increasingly adopting automated process control, the demand for intelligent vacuum sensing solutions has grown by over 18% annually in advanced manufacturing regions like North America and East Asia.

Transition to Extreme High Vacuum (XHV) Technologies

As semiconductor nodes shrink below 5nm, the industry is shifting toward Extreme High Vacuum (XHV) environments requiring pressures below 10−9 mbar. This transition is creating specialized demand for XHV-compatible sensors with exceptionally low outgassing properties. Leading manufacturers are developing ceramic-sealed sensors and non-evaporable getter materials to maintain stable measurements in these challenging conditions. The XHV sensor segment now represents 22% of total market revenue, with applications expanding beyond traditional semiconductor processing to quantum computing research and space-grade component testing. Meanwhile, ongoing R&D in molecular drag gauge technology promises to improve measurement accuracy at these ultra-low pressures.

COMPETITIVE LANDSCAPE

Key Industry Players

Global Leaders Drive Innovation in Semiconductor Vacuum Sensor Technology

The global semiconductor vacuum sensors market exhibits a dynamic competitive landscape, with established multinational corporations competing alongside specialized sensor manufacturers. NXP Semiconductors and Danaher Corporation currently dominate the market, collectively accounting for over 25% of global revenue as of 2024. Their leadership position stems from comprehensive product portfolios spanning various vacuum measurement ranges and proven reliability in semiconductor manufacturing environments.

Several Japanese and European manufacturers are making significant inroads in this space. ULVAC Technologies, a pioneer in vacuum science, has strengthened its market position through advanced sensor solutions tailored for next-generation semiconductor fabrication processes. Similarly, Sensirion has gained traction with its MEMS-based vacuum sensors that offer superior accuracy in challenging fabrication environments.

The market has witnessed increased strategic activity in recent years, with several notable developments. Agilent Technologies expanded its vacuum measurement capabilities through targeted acquisitions, while Honeywell partnered with leading semiconductor equipment manufacturers to integrate its sensors directly into fabrication systems. Such moves are reshaping the competitive dynamics as companies seek to offer complete vacuum solutions rather than standalone sensors.

Emerging players like VACOM and Okazaki Manufacturing are carving out niche positions by focusing on specialized applications such as extreme high vacuum (XHV) measurements below 10-12 mbar, an area seeing growing demand in advanced logic and memory chip production.

List of Key Semiconductor Vacuum Sensor Companies

- NXP Semiconductors N.V. (Netherlands)

- Danaher Corporation (U.S.)

- ULVAC Technologies, Inc. (Japan)

- Sensirion AG (Switzerland)

- Agilent Technologies, Inc. (U.S.)

- Honeywell International Inc. (U.S.)

- VACOM GmbH (Germany)

- Okazaki Manufacturing Company (Japan)

- Balluff GmbH (Germany)

- Nidec Corporation (Japan)

- CyberOptics Corporation (U.S.)

Technology differentiation remains crucial in this market, with leaders investing heavily in R&D to enhance sensor accuracy, response time, and durability. The shift toward Industry 4.0 has further intensified competition as companies race to develop smart vacuum sensors with advanced diagnostics and predictive capabilities. These innovations are becoming critical differentiators as semiconductor fabs demand higher precision and reliability to support advanced node manufacturing.

Segment Analysis:

By Type

Ultra-high Vacuum (UHV) Segment Dominates Due to Critical Use in Advanced Semiconductor Fabrication

The market is segmented based on type into:

- High Vacuum (HV)

- Ultra-high Vacuum (UHV)

- Extreme High Vacuum (XHV)

By Application

Deposition Segment Leads as Semiconductor Vacuum Sensors Ensure Process Stability in Thin Film Formation

The market is segmented based on application into:

- Deposition

- Subtypes: CVD, PVD, ALD, and others

- Etching and Cleaning

- Implantation of Ion

- Handling of Wafers

- Lithography

- Wafer Inspection and Metrology

By Technology

Pirani Gauge Technology Holds Significant Share Due to Wide Measurement Range and Reliability

The market is segmented based on technology into:

- Pirani Gauge

- Capacitance Manometer

- Cold Cathode Gauge

- Hot Cathode Gauge

- Others

Regional Analysis: Semiconductor Vacuum Sensors Market

Asia-Pacific

The Asia-Pacific region dominates the global semiconductor vacuum sensors market, accounting for over 45% of revenue share in 2024. This leadership position stems from massive semiconductor manufacturing clusters in Taiwan, South Korea, China, and Japan, where companies like TSMC, Samsung, and SK Hynix operate cutting-edge fabrication plants (fabs). Governments across the region are actively supporting semiconductor self-sufficiency through initiatives like China’s $150 billion semiconductor investment fund and India’s $10 billion chip manufacturing incentives. While cost sensitivity drives demand for mid-range vacuum sensors in smaller fabs, advanced nodes below 7nm require ultra-high precision sensors—creating a dual-tier market structure. Taiwan alone hosts 22% of global semiconductor production capacity, creating concentrated demand for vacuum measurement technologies.

North America

North America maintains strong demand for high-end semiconductor vacuum sensors, particularly in research-intensive facilities and leading-edge logic chip production. The CHIPS and Science Act has allocated $52 billion to revitalize domestic semiconductor manufacturing, with Intel, Micron, and Texas Instruments expanding fab capacity. Arizona’s semiconductor corridor and New York’s Tech Valley are emerging as key hubs requiring advanced vacuum monitoring solutions. Unlike Asia’s volume-driven market, North American buyers prioritize sensor accuracy and integration with Industry 4.0 systems. Strict export controls on sensitive semiconductor technologies also influence vacuum sensor specifications, with manufacturers needing to comply with ITAR regulations for defense-related applications.

Europe

Europe’s semiconductor vacuum sensor market benefits from specialized equipment manufacturers like ASML and long-standing expertise in industrial measurement technologies. The EU Chips Act projects €43 billion in public-private semiconductor investments through 2030, focusing on advanced packaging and specialty chips where vacuum control is critical. Germany’s semiconductor valley in Dresden and Italy’s MEMS sensor clusters create targeted demand. European manufacturers emphasize environmentally sustainable sensor designs aligned with the EU Green Deal, leading to innovations in energy-efficient vacuum monitoring. However, the region faces challenges from high energy costs impacting fab operations and fragmented standardization across national markets.

South America

South America represents a developing market with growth potential but currently limited semiconductor manufacturing infrastructure. Brazil’s CEITEC and Argentina’s INVAP represent early-stage domestic capabilities, primarily requiring mid-range vacuum sensors for assembly and test operations rather than full-scale fab tools. The region shows increasing demand for vacuum sensors in scientific research applications, particularly in nuclear and space programs. Economic instability and import dependency hinder market expansion, though nearshoring trends could boost local semiconductor investments. Chile’s emerging lithium battery industry may create adjacent opportunities for vacuum sensor applications in materials processing.

Middle East & Africa

The MEA region demonstrates nascent semiconductor ambitions, with Saudi Arabia’s $6 billion semiconductor initiative and Israel’s strong fabless chip design ecosystem driving select vacuum sensor demand. UAE’s Dubai Industrial City and Abu Dhabi’s G42 are investing in specialized semiconductor applications like AI chips, which require precision vacuum environments. Africa’s market remains largely untapped outside South Africa’s semiconductor packaging operations, though Morocco’s automotive chip production shows early growth signals. Infrastructure limitations and lack of technical workforce present barriers, but sovereign wealth fund investments could accelerate semiconductor industry development in the long term.

Report Scope

This market research report provides a comprehensive analysis of the Global Semiconductor Vacuum Sensors Market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The market was valued at USD 346 million in 2024 and is projected to reach USD 640 million by 2032, growing at a CAGR of 9.4%.

- Segmentation Analysis: Detailed breakdown by product type (High Vacuum, Ultra-high Vacuum, Extreme High Vacuum), application (Deposition, Etching and Cleaning, Lithography, etc.), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, with country-level analysis. Asia-Pacific dominates the market due to semiconductor manufacturing growth.

- Competitive Landscape: Profiles of leading market participants, including their product portfolios, R&D focus, manufacturing capabilities, and recent developments. Key players include NXP, Nidec, Danaher, Honeywell, and Agilent.

- Technology Trends & Innovation: Assessment of emerging sensor technologies, integration with Industry 4.0, and advancements in semiconductor fabrication processes.

- Market Drivers & Restraints: Evaluation of factors such as rising semiconductor demand, miniaturization trends, alongside challenges like supply chain disruptions and high R&D costs.

- Stakeholder Analysis: Strategic insights for sensor manufacturers, semiconductor equipment providers, and investors regarding market opportunities.

The research employs primary interviews with industry experts and analysis of verified market data to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Semiconductor Vacuum Sensors Market?

-> Semiconductor Vacuum Sensors Market was valued at 346 million in 2024 and is projected to reach US$ 640 million by 2032, at a CAGR of 9.4% during the forecast period.

Which key companies operate in this market?

-> Major players include NXP, Nidec, Danaher, Honeywell, Agilent, ULVAC, and Sensirion.

What are the key growth drivers?

-> Growth is driven by increasing semiconductor production, demand for precision manufacturing, and adoption of advanced fabrication technologies.

Which region dominates the market?

-> Asia-Pacific leads the market due to high semiconductor manufacturing activity, particularly in China, South Korea, and Taiwan.

What are the emerging trends?

-> Key trends include development of MEMS-based sensors, integration with IoT platforms, and demand for ultra-high vacuum solutions for advanced nodes.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...